Understanding how interest is calculated is one of the most vital components of financial literacy. Whether you are managing a credit card balance, planning for a mortgage, or looking to grow your wealth through a high-yield savings account, the “monthly” figure is often the most important metric. While financial institutions almost always advertise interest rates in annual terms (APR), your financial life moves in monthly cycles.

Computing the interest rate per month allows you to peel back the curtain on your bank statements and understand exactly where your money is going. This guide provides an in-depth look at the formulas, the logic, and the real-world applications of monthly interest calculations to help you take full control of your personal finances.

Understanding the Fundamentals of Interest Rates

Before diving into the mathematics of monthly calculations, it is essential to distinguish between the different types of interest and how they are presented by financial institutions.

Nominal vs. Effective Interest Rates

The rate you see on a loan agreement or a savings account advertisement is typically the Nominal Annual Percentage Rate (APR). However, this number can be misleading because it does not always account for the frequency of compounding. The Effective Annual Rate (EAR), or Annual Percentage Yield (APY) in the context of savings, reflects the actual interest earned or paid when compounding is taken into account. When you compute interest per month, you are essentially breaking down the nominal rate into its “periodic” component.

Simple Interest vs. Compound Interest

The method of computation changes drastically depending on whether you are dealing with simple or compound interest.

- Simple Interest: This is calculated only on the principal amount (the original sum of money). It is common in short-term personal loans or specific types of consumer financing.

- Compound Interest: This is “interest on interest.” Most modern financial products—including credit cards, mortgages, and investment accounts—use compound interest. In these cases, the interest earned in one month is added to the principal, and the next month’s interest is calculated based on that new, higher balance.

The Step-by-Step Guide to Computing Monthly Interest

Calculating your monthly interest rate is a two-part process: first, you determine the periodic rate, and second, you apply that rate to your balance using the appropriate formula.

Converting Annual Percentage Rate (APR) to Monthly

To find the monthly interest rate from an annual rate, the simplest method is to divide the annual rate by the number of months in a year.

The Formula:

Monthly Interest Rate = Annual Percentage Rate / 12

For example, if you have a credit card with an 18% APR, your monthly interest rate is:

0.18 / 12 = 0.015 (or 1.5% per month)

While this gives you the rate, the actual dollar amount depends on how the bank applies that 1.5% to your balance.

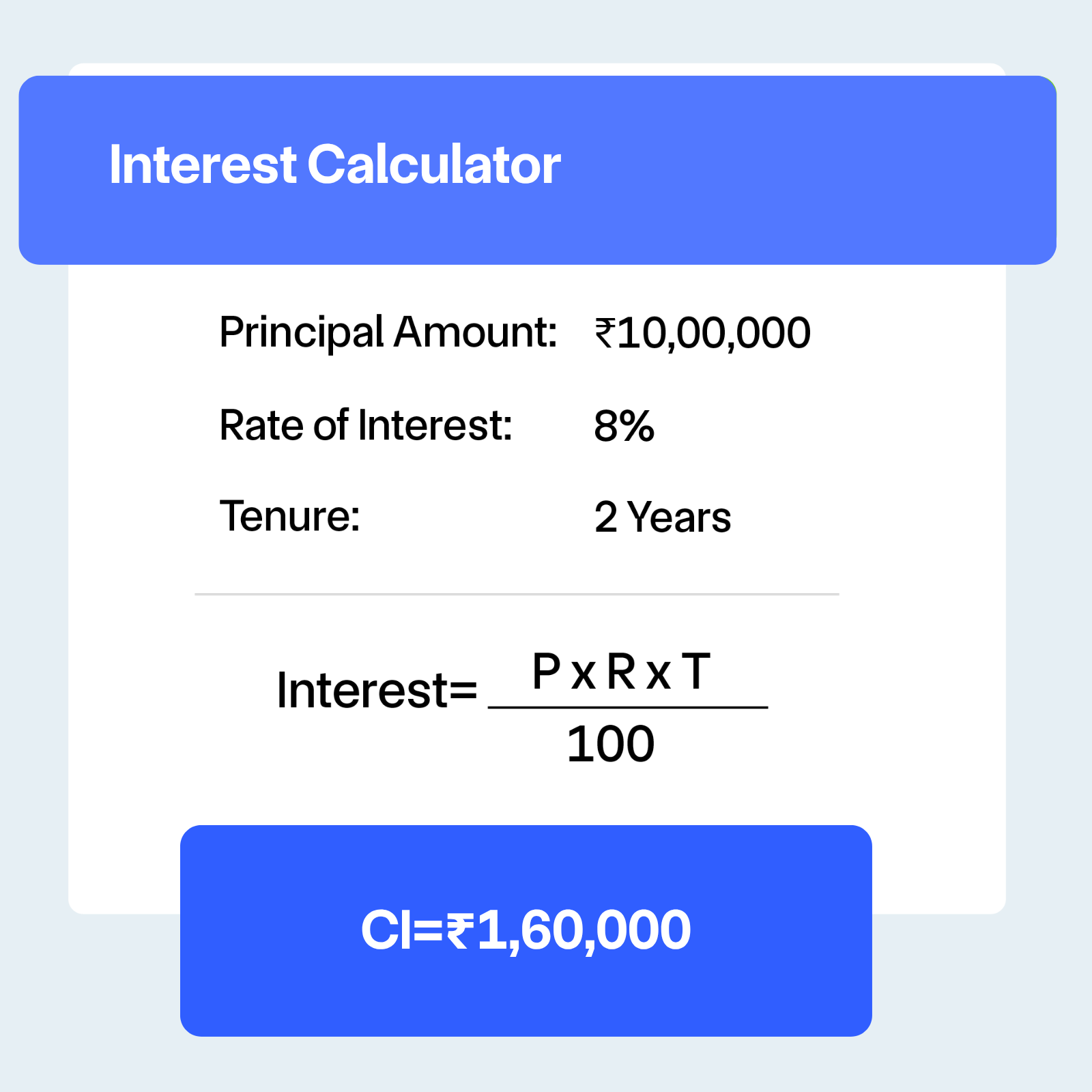

Calculating Simple Monthly Interest

If you are working with a simple interest loan, the calculation is straightforward. You multiply the principal by the monthly rate.

The Formula:

Interest Amount = Principal × Monthly Rate

If you owe $10,000 on a simple interest loan with a 12% APR (1% per month), your interest for that month would be:

$10,000 × 0.01 = $100

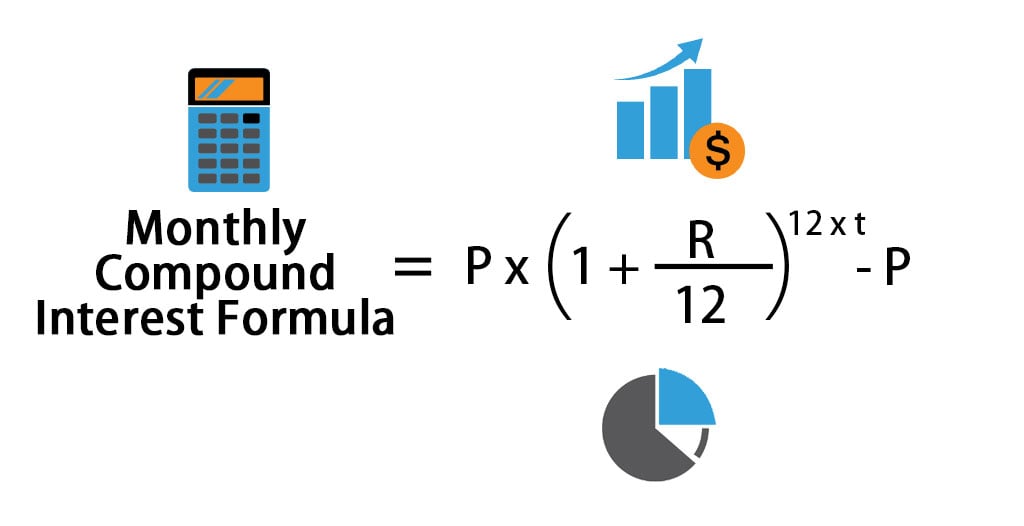

The Mechanics of Compound Monthly Interest

Compound interest is slightly more complex because the balance changes every period. To find the future value of an investment or the total growth of a debt over several months, you use the compound interest formula.

The Formula:

A = P(1 + r/n)^(nt)

Where:

- A = the total amount (principal + interest)

- P = the principal amount

- r = the annual interest rate (decimal)

- n = the number of times interest compounds per year (for monthly, n = 12)

- t = the time in years

To find just the interest for a single month within a compounding cycle, you apply the monthly rate to the current balance (which includes previously accrued interest).

Real-World Applications: Loans and Savings

The theory of interest calculation becomes most valuable when applied to the specific financial products we use daily.

Credit Card Interest Mechanics

Credit cards are unique because they often calculate interest based on your Average Daily Balance. Instead of just looking at your balance at the end of the month, the bank looks at what you owed every single day.

To compute this, the bank first finds your Daily Periodic Rate (DPR) by dividing your APR by 365. They then multiply this daily rate by your average balance and the number of days in the billing cycle. This is why even a small increase in your balance early in the month can result in significantly higher interest charges than the same increase at the end of the month.

Amortized Loans: Mortgages and Car Loans

When you pay off a mortgage or an auto loan, you are likely using an amortization schedule. In this scenario, your monthly payment remains the same, but the ratio of interest to principal shifts over time.

In the early stages of a 30-year mortgage, the vast majority of your monthly payment goes toward interest. This is because the interest is calculated on the total remaining balance. As you pay down the principal, the monthly interest calculation (Principal × Monthly Rate) results in a smaller number, allowing more of your payment to go toward the principal. Understanding this helps homeowners see the immense value of making even small “principal-only” extra payments early in the loan term.

Yield on Savings and Investments

For investors, computing monthly interest is about tracking growth. If you have a high-yield savings account offering a 4.5% APY, your money isn’t just sitting there; it’s compounding. By understanding the monthly rate, you can project your monthly “passive income.”

However, remember the difference between APR and APY. If a bank says “4.5% APY,” they have already factored in the effects of monthly compounding. If they say “4.5% APR compounded monthly,” your actual yield (APY) will be slightly higher (approximately 4.59%).

Tools and Strategies for Managing Monthly Interest

In the modern era, you don’t need to do all these calculations by hand on the back of an envelope. Utilizing digital tools can provide precision and help you strategize.

Using Spreadsheets for Financial Accuracy

Software like Microsoft Excel or Google Sheets is incredibly powerful for calculating interest. There are built-in functions designed specifically for this:

- =PMT: Calculates the payment for a loan based on constant payments and a constant interest rate.

- =IPMT: Returns the interest payment for a given period for an investment based on periodic, constant payments and a constant interest rate.

- =FV: Returns the future value of an investment.

By setting up a simple spreadsheet, you can create your own “what-if” scenarios. For instance, you can calculate how much interest you would save over the life of a loan if you increased your monthly payment by just $50.

Strategies to Minimize Interest Expense

Once you understand how to compute monthly interest, the goal is usually to minimize it on debts and maximize it on assets.

- The Snowball vs. Avalanche Method: When you calculate the monthly interest on multiple debts, the “Avalanche” method suggests paying off the debt with the highest interest rate first. This mathematically minimizes the total interest paid over time.

- Timing Your Credit Card Payments: Since many cards use average daily balances, paying your bill earlier in the cycle—even before the due date—can lower your average balance and reduce the interest charged.

- Refinancing: If you compute your monthly interest and realize you are paying a significant amount, it may be time to look for a lower APR. A 2% difference in an annual rate might seem small, but when compounded monthly over years, it represents thousands of dollars.

Empowerment Through Financial Literacy

Computing the interest rate per month is more than just a math exercise; it is an act of financial empowerment. When you look at a loan statement and can identify exactly how much of your hard-earned money is being diverted to interest, you are better equipped to make informed decisions.

By mastering these formulas and understanding the nuances of compounding, you move from being a passive consumer to an active manager of your wealth. Whether you are aggressively paying down debt or strategically building a retirement nest egg, the ability to calculate and understand monthly interest is the foundation upon which financial freedom is built. Mastery of your money starts with the math, and the math starts with the monthly rate.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.