Understanding the Components of Salary Computation

When we talk about computing salary, we’re delving into the fundamental mechanics of compensation within the business world. It’s more than just assigning a number; it involves a systematic approach that considers various factors to ensure fairness, accuracy, and compliance. At its core, salary computation is the process of calculating an employee’s gross pay, which then forms the basis for deductions to arrive at their net or take-home pay. This process is critical for both employers, who need to manage payroll accurately and efficiently, and employees, who need to understand how their earnings are determined.

Gross Pay: The Starting Point

Gross pay represents the total amount of money an employee earns before any deductions are taken out. This is the foundational figure from which all other salary calculations stem. Understanding how gross pay is determined is the first step in demystifying salary computation.

Base Salary Calculation

The most straightforward component of gross pay is the base salary. This is the agreed-upon fixed amount an employee receives for their work, typically expressed as an annual figure, hourly rate, or a salary for a specific pay period (e.g., weekly, bi-weekly, monthly).

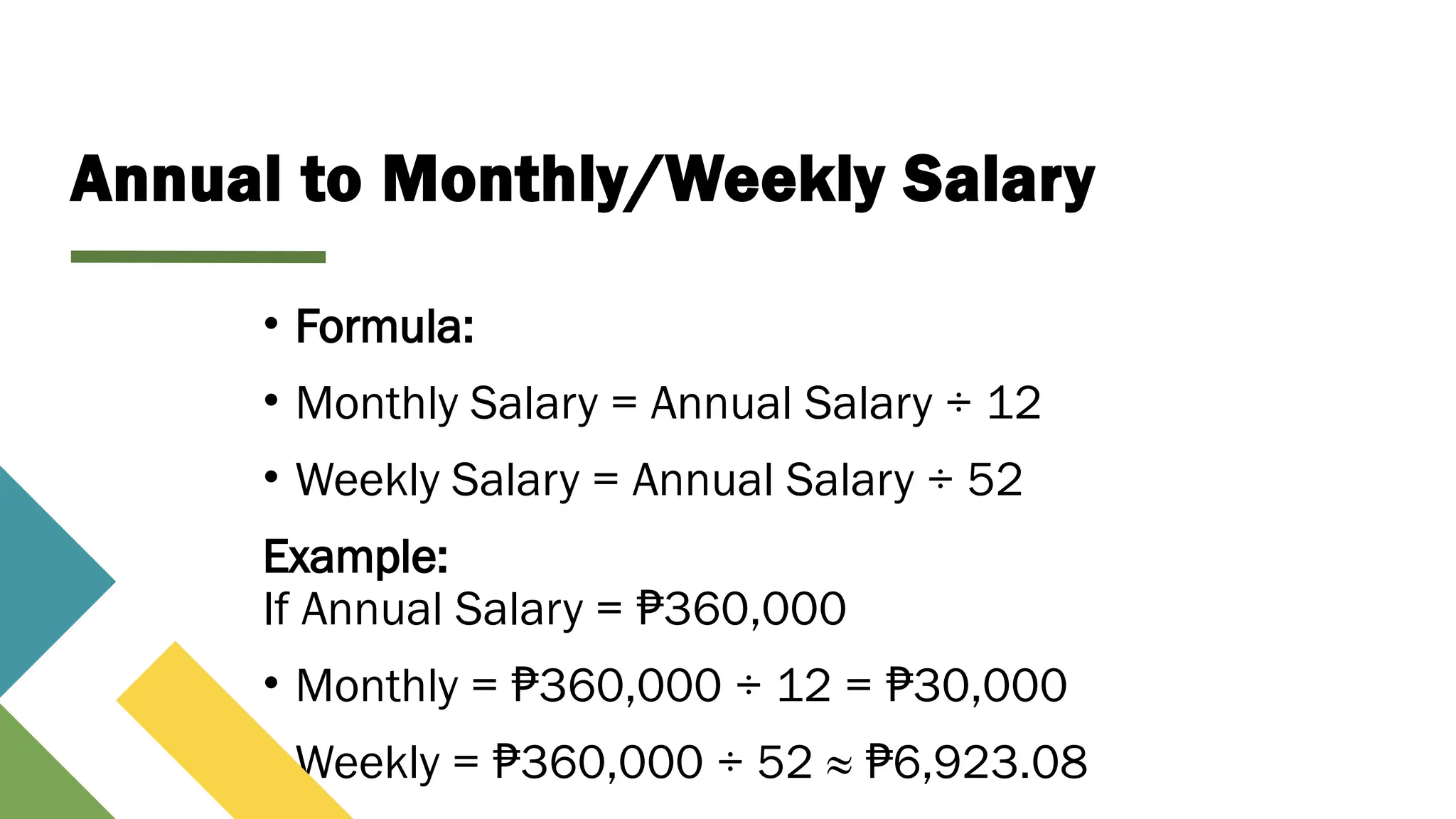

- Annual Salary: For salaried employees, the annual salary is divided by the number of pay periods in a year. For instance, a $60,000 annual salary paid bi-weekly (26 pay periods) would result in a gross pay of $60,000 / 26 = $2,307.69 per pay period.

- Hourly Wage: For hourly employees, gross pay is calculated by multiplying their hourly rate by the number of hours worked. If an employee earns $20 per hour and works 40 hours in a week, their gross pay for that week is $20 * 40 = $800.

- Overtime Pay: When employees work beyond their standard hours, they are often entitled to overtime pay, which is typically calculated at a higher rate (e.g., 1.5 times the regular hourly rate). For example, if an hourly employee works 45 hours at $20/hour with overtime at 1.5x, their gross pay would be (40 hours * $20/hour) + (5 hours * $30/hour) = $800 + $150 = $950.

Additional Compensation and Bonuses

Beyond the base salary, employees may receive additional forms of compensation that contribute to their gross pay. These can include performance-based bonuses, commissions, shift differentials, and stipends.

- Performance Bonuses: These are discretionary or contractually obligated payments awarded based on individual, team, or company performance. The computation of bonuses can vary widely, from a fixed percentage of salary to a tiered structure based on achievement levels.

- Commissions: Common in sales roles, commissions are payments based on a percentage of sales made or revenue generated. The commission structure needs to be clearly defined, outlining the rate, the sales volume it applies to, and any payout thresholds.

- Shift Differentials: Some employers offer higher pay rates for employees working undesirable shifts (e.g., night shifts, weekends). This differential is typically a fixed amount or a percentage added to the base hourly rate for hours worked during those specific shifts.

- Stipends and Allowances: These are fixed sums provided to employees for specific purposes, such as travel, meals, or professional development. While often treated differently for tax purposes, they are generally included in the overall compensation calculation.

Deductions: Reducing Gross to Net

Once gross pay is established, various deductions are made to arrive at the net salary, the amount an employee actually receives. These deductions can be mandatory (statutory) or voluntary.

Statutory Deductions

These are legally required withholdings from an employee’s paycheck. They are critical for ensuring compliance with government regulations.

- Income Tax: This is the most significant statutory deduction. The amount withheld depends on the employee’s taxable income, filing status, and the tax brackets set by the relevant tax authorities (e.g., federal, state, local income tax). Employers use tax forms (like W-4 in the US) to determine the correct withholding amount.

- Social Security and Medicare Taxes (FICA in the US): These are payroll taxes that fund social insurance programs. A portion is paid by the employee and a matching portion by the employer. There are often annual wage bases or caps for these taxes.

- Other Statutory Deductions: Depending on the jurisdiction, other mandatory deductions might include contributions to state-specific unemployment insurance funds, disability insurance, or other social welfare programs.

Voluntary Deductions

These are deductions that an employee chooses to have withheld from their paycheck. They often relate to benefits or savings plans.

- Health Insurance Premiums: If an employee enrolls in a company-sponsored health insurance plan, the cost of their premium is typically deducted from their pay. This can be for medical, dental, or vision coverage.

- Retirement Plan Contributions: Contributions to employer-sponsored retirement plans, such as 401(k)s (in the US) or similar schemes, are common voluntary deductions. Employees choose the percentage or dollar amount they wish to contribute, which can sometimes be pre-tax, reducing their taxable income.

- Life Insurance Premiums: Similar to health insurance, employees may elect to have premiums for supplemental life insurance policies deducted from their pay.

- Union Dues: For employees who are part of a labor union, union dues are usually deducted from their salary.

- Garnishments: In certain legal circumstances, a portion of an employee’s salary may be legally required to be withheld and paid to a third party (e.g., for child support, court judgments, or tax levies). These are often considered mandatory but are a result of specific legal orders rather than general statutory requirements.

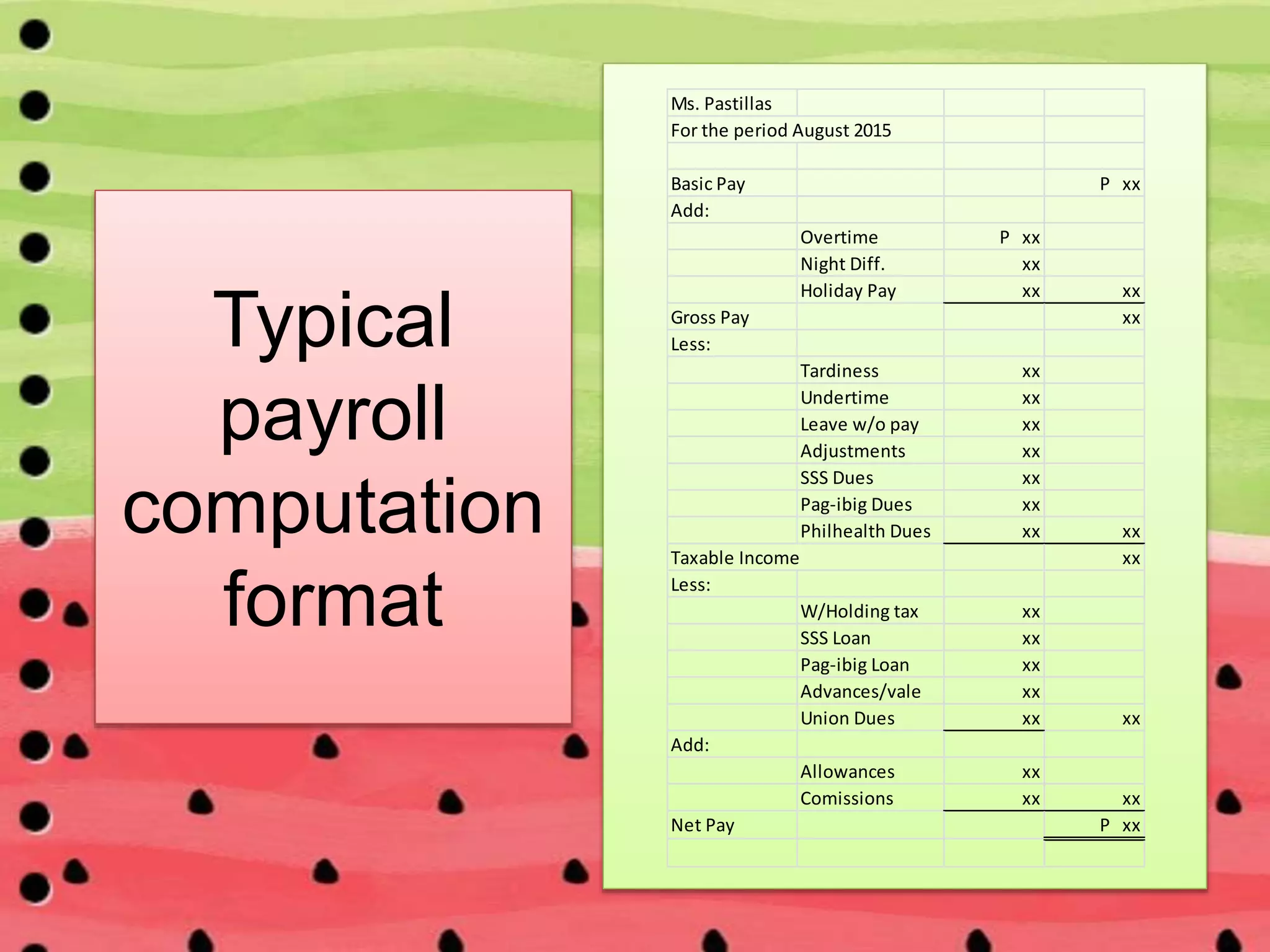

Net Pay: The Take-Home Amount

Net pay, also known as take-home pay, is the amount of money an employee receives after all statutory and voluntary deductions have been subtracted from their gross pay. It’s the figure that appears on the employee’s pay stub and is directly deposited into their bank account or issued as a physical check.

-

Calculation Formula: The basic formula for net pay is:

Net Pay = Gross Pay – Total Deductions

Where Total Deductions = Sum of all Statutory Deductions + Sum of all Voluntary Deductions -

Importance of Accuracy: Ensuring the accuracy of net pay calculations is paramount. Errors can lead to employee dissatisfaction, legal issues, and damage to an employer’s reputation. Payroll software and systems are designed to handle these complex calculations, but human oversight and regular audits are still essential.

-

Pay Stubs and Transparency: A detailed pay stub is crucial for explaining the net pay. It should clearly itemize the gross pay, each type of deduction, and the final net amount. This transparency helps employees understand their compensation and build trust.

Advanced Considerations in Salary Computation

While the core of salary computation involves gross pay and deductions, several advanced factors can influence the final figures and require careful consideration. These often pertain to specific employment scenarios, tax implications, and benefit structures that go beyond basic wage calculations.

Understanding Tax Implications and Withholding Strategies

Taxation is perhaps the most complex aspect of salary computation, impacting both employers and employees significantly. Proper understanding and application of tax laws are vital for compliance and optimizing take-home pay.

Taxable Income vs. Gross Income

It’s crucial to distinguish between gross income and taxable income. Gross income is the total earnings before any deductions. Taxable income is the portion of gross income that is subject to income tax. This difference arises due to various deductions and credits allowed by tax laws.

- Pre-Tax Deductions: Contributions to certain retirement plans (like traditional 401(k)s) and premiums for employer-sponsored health insurance are often pre-tax deductions. This means they are subtracted from gross income before income tax is calculated, thereby reducing the employee’s taxable income and their overall tax liability.

- Tax Credits and Deductions: Employees can claim various tax credits and deductions on their individual tax returns, which are not typically handled during payroll withholding but affect their final tax obligation. However, some payroll systems might allow for adjustments based on specific tax situations if permitted by law.

Withholding Allowances and Adjustments

Tax forms, such as the W-4 form in the United States, allow employees to adjust their withholding. This is done by claiming allowances (or dependents) or making additional withholding requests.

- Allowances: Generally, more allowances mean less tax is withheld from each paycheck. Employees with dependents or significant deductions may claim more allowances.

- Additional Withholding: If an employee anticipates owing more tax at the end of the year (perhaps due to significant side income or investments), they can request additional tax to be withheld from each paycheck to avoid a large tax bill.

- Impact on Take-Home Pay: The choices made regarding withholding directly impact an employee’s net pay. Claiming too many allowances can lead to insufficient withholding and a tax liability at year-end, while claiming too few can result in over-withholding and an unnecessarily smaller paycheck.

Employer’s Role in Tax Withholding

Employers are responsible for withholding the correct amount of taxes based on the information provided by the employee and current tax regulations. They then remit these withheld taxes to the appropriate government agencies.

- Accuracy is Key: Incorrect withholding can lead to penalties for the employer and tax problems for the employee. Payroll software and systems are designed to ensure accurate calculations based on tax tables and employee-provided data.

- Reporting Obligations: Employers have annual reporting obligations, such as issuing W-2 forms (in the US) to employees and filing necessary tax returns with government agencies.

Benefit Administration and Its Impact on Salary Computation

Employee benefits are a significant part of total compensation and play a crucial role in salary computation, often through voluntary deductions or employer contributions.

Understanding Various Benefit Types

Benefits can range from essential health coverage to perks that enhance employee well-being and financial security.

- Health, Dental, and Vision Insurance: As mentioned, employee premiums are often deducted. The employer’s contribution to these plans also represents a cost that, while not directly deducted from an employee’s salary, contributes to their overall compensation package.

- Retirement Plans (401(k), IRA, Pension): Employee contributions are deducted, often pre-tax. Employer matching contributions are a significant benefit that effectively increases the employee’s total compensation, even if it doesn’t appear in their immediate paycheck.

- Life and Disability Insurance: Similar to health insurance, premiums can be deducted, and employer contributions can add value.

- Paid Time Off (PTO) and Sick Leave: While not directly computed as part of a regular paycheck deduction, PTO and sick leave are forms of compensation that employees accrue. When used, they are paid out at the employee’s regular rate, impacting the variability of their monthly earnings.

- Stock Options and Equity: For some employees, particularly in tech or startup environments, stock options or restricted stock units (RSUs) can be a substantial part of their compensation. The valuation and vesting schedules of these are complex and have significant financial implications, though their direct computation in a regular salary cycle might be limited to the exercise or vesting date.

The Financial Implications of Benefits

Benefits have a direct financial impact on both the employee and the employer.

- Employee Perspective: Benefits can significantly increase an employee’s net worth and financial security. A comprehensive benefits package can be as valuable as a higher salary for some individuals.

- Employer Perspective: The cost of benefits is a major expense for businesses. These costs need to be factored into the overall compensation budget and the company’s financial planning. The structure of benefit plans (e.g., self-funded vs. fully insured) can also influence how they are accounted for and communicated.

Payroll Processing Systems and Automation

In today’s business environment, manual salary computation is largely a relic of the past. Modern payroll processing relies heavily on sophisticated systems and automation to ensure accuracy, efficiency, and compliance.

Features of Modern Payroll Systems

Payroll software goes far beyond simple arithmetic; it integrates with human resources, accounting, and time-tracking systems.

- Automated Calculations: These systems automatically compute gross pay, overtime, deductions, and net pay based on employee data, pay rates, hours worked, and configured rules for taxes and benefits.

- Tax Compliance: Payroll software is regularly updated to reflect changes in tax laws, tax tables, and reporting requirements, helping employers remain compliant.

- Direct Deposit and Electronic Payments: Most systems facilitate direct deposit, enabling employees to receive their net pay automatically and securely into their bank accounts.

- Reporting and Analytics: Robust reporting features provide detailed payroll summaries, tax reports, and insights into labor costs, which are invaluable for financial management.

- Employee Self-Service Portals: Many systems offer employee portals where individuals can view pay stubs, update personal information, and access tax forms, enhancing transparency and reducing administrative burden.

The Role of Automation in Reducing Errors and Costs

Automation in payroll processing brings significant advantages.

- Minimizing Human Error: Automated calculations reduce the risk of manual errors that can lead to incorrect payments, under or over-withholding of taxes, and compliance issues.

- Increased Efficiency: Automating routine tasks frees up HR and finance staff to focus on more strategic activities rather than being bogged down by manual data entry and calculations.

- Cost Savings: While there is an initial investment in payroll software, the long-term cost savings from reduced errors, increased efficiency, and improved compliance often outweigh the expenditure.

- Scalability: Automated systems can easily scale with the growth of a company, handling a larger number of employees and more complex payroll scenarios without a proportional increase in administrative effort.

Legal and Ethical Considerations in Salary Computation

Beyond the technicalities of calculation, the process of computing salary is deeply intertwined with legal frameworks and ethical responsibilities. Ensuring fairness, compliance, and transparency is not just good practice; it’s often a legal requirement and a cornerstone of good corporate citizenship.

Compliance with Labor Laws and Regulations

Labor laws are designed to protect employees and ensure fair treatment in the workplace. Salary computation must adhere strictly to these regulations.

Minimum Wage Laws

Every jurisdiction has a minimum wage, which is the lowest hourly rate an employer can legally pay. Salary computations for hourly employees must ensure their earnings never fall below this threshold for any standard work period. For salaried employees, their fixed salary, when annualized and divided by the standard hours they are expected to work, must also meet or exceed the equivalent minimum wage for their position and location.

- Federal, State, and Local Minimums: It’s crucial to be aware of all applicable minimum wage laws, as the highest rate often prevails. For example, if a city has a higher minimum wage than the state, employers in that city must adhere to the city’s higher rate.

- Exempt vs. Non-Exempt Employees: Labor laws often distinguish between “exempt” and “non-exempt” employees. Non-exempt employees are entitled to overtime pay, while exempt employees (typically those in executive, administrative, or professional roles meeting specific salary and duty tests) are not. Misclassifying an employee can lead to significant legal liabilities.

Overtime Regulations

The rules governing overtime pay are critical for accurate salary computation.

- Overtime Rate: Most jurisdictions mandate that non-exempt employees receive a premium rate (commonly 1.5 times their regular rate of pay) for hours worked beyond a standard workweek (often 40 hours).

- Calculating Regular Rate: The “regular rate of pay” for overtime calculations isn’t always just the base hourly wage. It can include other forms of compensation like shift differentials, non-discretionary bonuses, and commissions earned during the pay period. Accurately calculating this regular rate is essential for correct overtime payments.

- Record Keeping: Employers are legally required to keep accurate records of all hours worked by non-exempt employees to ensure correct overtime calculation and payment.

Equal Pay and Non-Discrimination

Salary computation must be conducted in a manner that prevents discrimination based on protected characteristics.

- Equal Pay for Equal Work: Laws like the Equal Pay Act (in the US) require that men and women be given equal pay for equal work in the same establishment. This means that salary decisions should be based on factors like experience, qualifications, performance, and seniority, not on gender or other protected attributes.

- Prohibition of Discriminatory Practices: Salary structures and computation methods should not indirectly or directly discriminate against employees based on race, religion, national origin, sex, age, disability, or other protected classes. Regular audits of pay scales and salary increases can help identify and rectify potential disparities.

Ethical Considerations in Salary Computation

Beyond legal mandates, ethical practices build trust and foster a positive work environment.

Transparency and Communication

Employees have a right to understand how their salary is computed. Open communication about pay practices is vital.

- Clear Job Descriptions and Salary Ranges: Providing clear job descriptions that outline responsibilities and expectations, along with transparent salary ranges for positions, can set fair expectations from the outset.

- Detailed Pay Stubs: As discussed earlier, pay stubs should be comprehensive, detailing gross pay, all deductions, and the net pay calculation. This allows employees to verify the accuracy of their pay.

- Explaining Compensation Decisions: When employees have questions about their salary, employers should be prepared to explain the factors that influence compensation decisions, such as performance reviews, market data, and internal equity.

Fairness and Equity

Ensuring fairness in pay is not just about legal compliance; it’s about creating an environment where employees feel valued and respected.

- Internal Equity: Employees in similar roles with comparable experience and performance should receive similar compensation within the organization. Inconsistent pay for similar work can lead to resentment and decreased morale.

- External Equity: Compensation should also be competitive with the external market for similar roles. If an organization consistently pays below market rates, it will struggle to attract and retain talent.

- Performance-Based Recognition: While base pay needs to be fair and competitive, performance-based bonuses, raises, and other incentives can be powerful tools for recognizing and rewarding high achievement, further enhancing the perception of fairness.

Auditing and Review Processes

Regularly auditing and reviewing salary computation processes are essential for maintaining accuracy, compliance, and ethical standards.

Internal Audits

These are performed by employees within the organization, often by the HR or finance department.

- Regular Payroll Checks: Conducting periodic checks of payroll data, comparing calculations against source documents (e.g., time sheets, benefit enrollment forms), and reconciling discrepancies.

- Compliance Reviews: Ensuring that all salary computations and payroll practices align with current labor laws and company policies.

- Equity Analysis: Analyzing pay data to identify any potential pay gaps or inconsistencies that might indicate discrimination or internal inequity.

External Audits and Reviews

Sometimes, organizations may engage external auditors or consultants.

- Third-Party Payroll Audits: An independent review by an external firm can provide an unbiased assessment of payroll processes and identify areas for improvement.

- Legal Counsel Consultation: Consulting with legal experts specializing in labor law can ensure that all compensation practices are compliant and robust.

- Benchmarking: Using external data to benchmark salaries and benefits against industry standards helps ensure external equity and competitiveness.

By diligently addressing legal mandates and upholding ethical principles, organizations can build robust, fair, and trustworthy salary computation systems that benefit both the company and its employees.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.