In the dynamic landscape of personal finance, managing your bank accounts effectively is paramount. While opening a new account often comes with a sense of excitement and new possibilities, the process of closing an existing one can sometimes feel daunting. Yet, there are numerous legitimate reasons why individuals choose to close a bank account – from consolidating finances and avoiding fees to responding to poor service or managing an estate. Regardless of your motivation, approaching account closure systematically and knowledgeably is crucial to prevent headaches, unexpected charges, and potential financial disruptions.

This guide aims to demystify the process of closing a bank account, providing you with a professional, insightful, and engaging roadmap to navigate this often-overlooked aspect of personal financial management. We’ll explore the common reasons for closure, the essential preparatory steps, the actual process, potential pitfalls to avoid, and what to do once the account is officially shut down, ensuring a smooth and secure transition.

Why You Might Consider Closing a Bank Account

Deciding to close a bank account isn’t always a negative reflection on your financial institution; often, it’s a strategic move to optimize your financial ecosystem. Understanding the common reasons can help you ascertain if it’s the right decision for your current circumstances.

High Fees or Poor Service

One of the most frequent catalysts for account closure is dissatisfaction with the bank’s fee structure or the quality of service provided. Hidden maintenance fees, excessive ATM charges, or a sudden increase in minimum balance requirements can quickly erode your savings or simply become a nuisance. Similarly, a pattern of unhelpful customer support, inconvenient branch hours, or a cumbersome online banking experience can push customers to seek alternatives where their business is more valued. Evaluating these factors regularly can lead you to a financial institution that better aligns with your needs and expectations.

Consolidating Finances

Many individuals find themselves with multiple bank accounts accumulated over time – perhaps from different life stages, former employers, or simply an experimental phase with various financial products. Consolidating these accounts into one or two primary accounts can significantly simplify financial management. It makes tracking spending, managing budgets, and monitoring overall financial health much easier. Fewer accounts mean less paperwork, fewer passwords to remember, and a clearer overall financial picture, reducing the likelihood of overlooking dormant accounts or unexpected fees.

Moving or Changing Banks

Life changes often necessitate financial adjustments. Moving to a new city, state, or even country might mean that your current bank no longer has a convenient branch network, or perhaps you’ve found a local credit union or community bank that offers more personalized service and better rates. Sometimes, people simply outgrow their current bank, finding that a different institution offers better investment opportunities, loan products, or technology that better suits their evolving financial goals. Proactively switching banks ensures you always have a banking partner that meets your contemporary needs.

Deceased Account Holder’s Estate

When an account holder passes away, closing their bank account becomes a critical step in settling their estate. This process, often handled by an executor or administrator, requires careful adherence to legal procedures, including providing a death certificate, letters testamentary, and sometimes probate court orders. The funds in the account must be properly distributed according to the will or state laws of intestacy. This is a sensitive and often complex process that requires meticulous attention to detail to ensure all assets are accounted for and legally transferred.

Avoiding Inactivity Fees or Fraud Risk

Dormant accounts can pose two significant problems: inactivity fees and heightened fraud risk. Many banks charge monthly or annual fees on accounts that show no activity for an extended period, slowly eroding any remaining balance. More critically, an unused account, especially one with a low balance or old personal information, can become a target for identity theft or fraud if not properly monitored. Closing such accounts eliminates these risks, tidying up your financial footprint and protecting your assets.

Essential Preparatory Steps Before Closing

Before you even think about contacting your bank, a thorough preparation phase is crucial. Skipping these steps can lead to significant inconvenience, missed payments, or unexpected charges. Think of it as untangling a complex web of financial connections.

Review Your Account Activity (Direct Deposits & Automatic Payments)

This is perhaps the most critical preparatory step. Your bank account is likely connected to a multitude of financial transactions. You need to identify every single direct deposit (e.g., salary, government benefits, investment dividends) and automatic payment (e.g., utilities, loan payments, subscriptions, insurance premiums). Go through at least six months’ worth of statements, or even a full year, to capture less frequent transactions. Make a comprehensive list of all these incoming and outgoing payments. This list will be your checklist for updating information with relevant parties.

Transfer Funds Out (Or Zero Out the Balance)

Once you’ve identified all recurring transactions, the next step is to ensure the account balance is either transferred to a new account or completely withdrawn. It’s generally advisable to move your funds out of the account before officially requesting closure. This can be done via electronic transfer (ACH), wire transfer, or by withdrawing cash. If you plan to close the account in person, you might be able to withdraw the remaining balance at that time. Ensure you leave no residual funds, as many banks have policies on how they handle small remaining balances after closure, which might involve a check that could get lost or expire.

Open a New Account (If Needed)

If you’re closing your account because you’re switching banks, make sure your new account is fully operational and ready to receive deposits and make payments before you initiate the closure of the old one. This provides a safe harbor for your funds and allows you to gradually transition your direct deposits and automatic payments without any interruption in service. Having the new account active is vital for a smooth shift of your financial life.

Obtain Necessary Documents

Banks typically require specific identification and documentation to close an account, especially if you’re doing it in person or if the account belongs to a deceased individual. Always have a valid government-issued ID (driver’s license, passport) handy. If it’s a joint account, both account holders might need to be present or provide written consent. For estate-related closures, you’ll need the death certificate, letters testamentary, and any other relevant legal documents as mandated by your bank or local laws. Contact your bank beforehand to confirm their specific requirements.

Confirm Outstanding Debts or Loans Linked to the Account

It’s essential to check if any loans, credit cards, or other financial products are directly linked to or secured by the account you intend to close. Closing an account that serves as collateral for a loan could trigger default clauses or require immediate repayment. Similarly, some overdraft protection services or lines of credit might be tied to your checking account. Ensure all these connections are severed or transferred to a new account before proceeding with closure to avoid any unforeseen financial penalties or complications.

The Step-by-Step Process of Closing Your Account

With all your preparatory steps completed, you’re now ready to engage with your bank. The actual process of closing an account is usually straightforward, but understanding the nuances can make a significant difference.

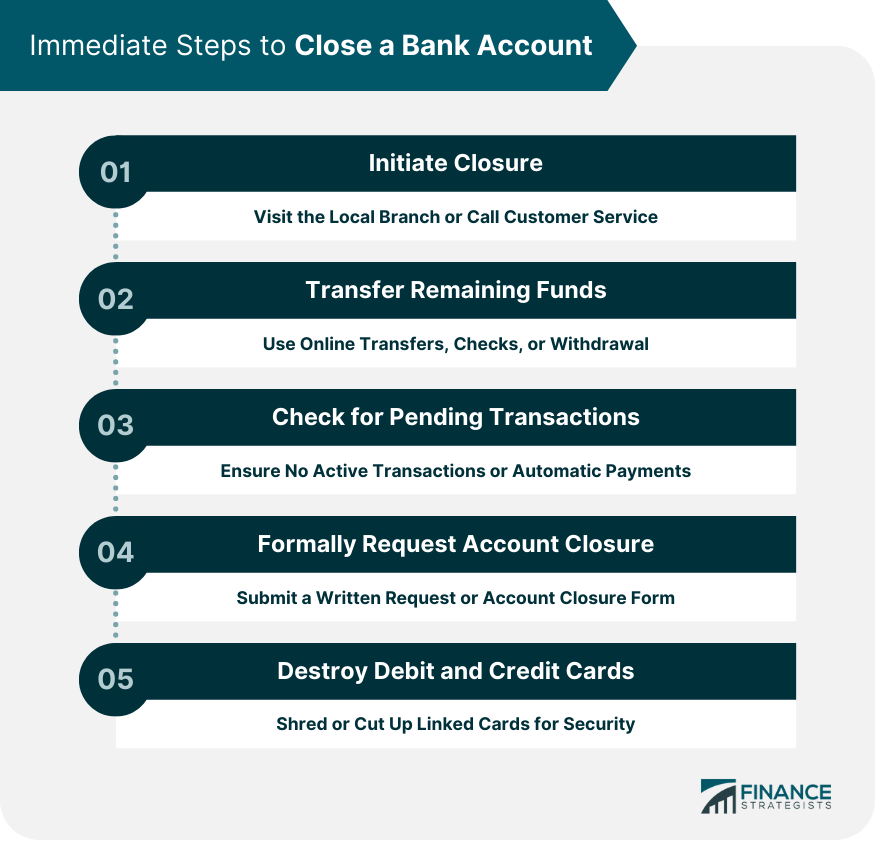

Contact Your Bank (Online, Phone, or In-Person)

You have several avenues to initiate the closure process, each with its own advantages.

- In-Person: Visiting a branch is often the most direct method, allowing you to speak with a representative, get immediate answers to questions, and often complete the process on the spot. Bring all necessary identification and documentation.

- Phone: Many banks allow account closures over the phone. Be prepared for security questions to verify your identity. This can be convenient if you no longer live near a branch.

- Online/Mail: Some banks offer online portals or require a written request sent via mail. If using mail, send it certified with a return receipt requested for proof of delivery. This method can be slower but provides a written record.

Always confirm the specific method preferred or required by your bank.

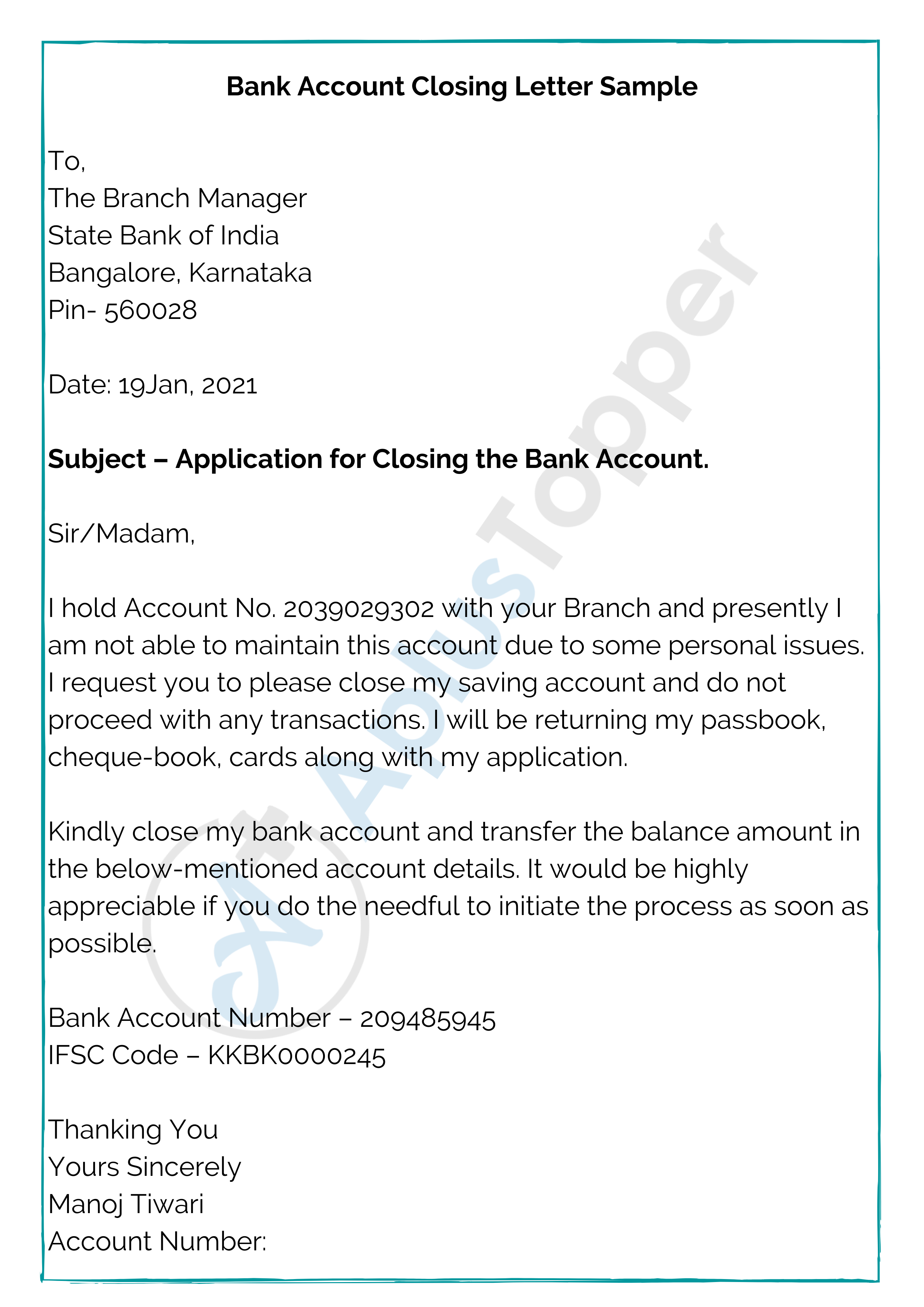

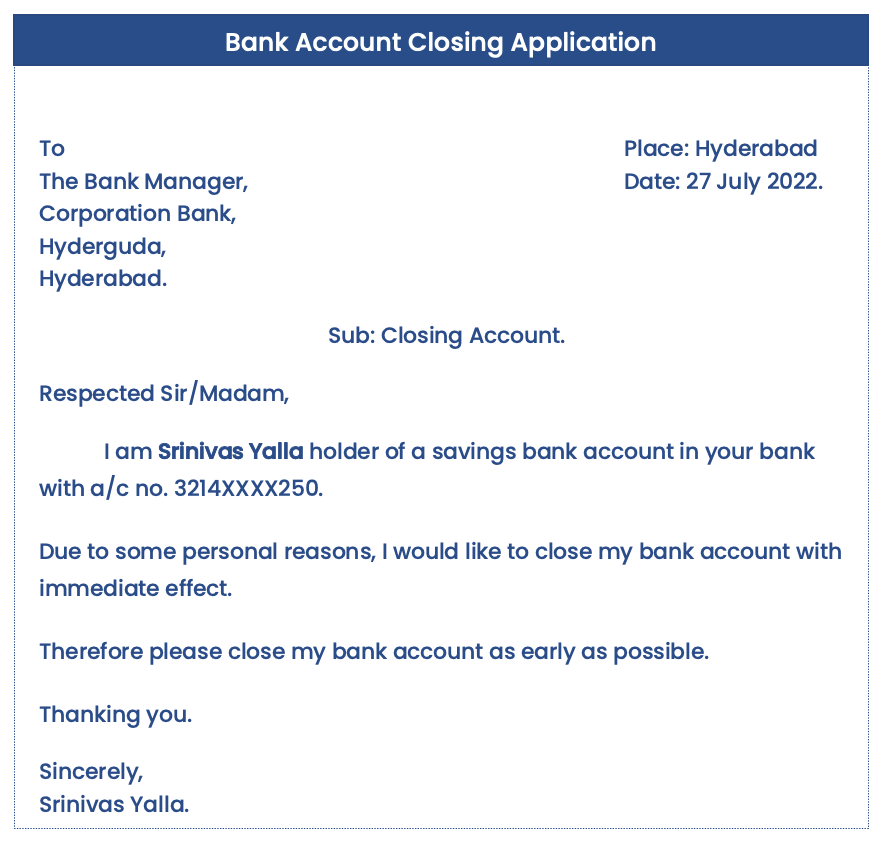

Submit Your Request (Written Confirmation Recommended)

Regardless of how you contact your bank, it’s highly advisable to get your request for account closure in writing. If closing in person, ask for a written confirmation or a letter acknowledging the closure. If closing by phone, follow up with a brief letter confirming your request and the date it was made. If you use mail, your certified return receipt serves this purpose. A written record serves as proof and can be invaluable if any issues arise later. Clearly state the account number(s) you wish to close and the effective date.

Verify Account Balance is Zero

Before the bank finalizes the closure, double-check that the account balance is absolutely zero. Any remaining positive balance might be mailed to you as a check, which could be delayed or lost. A negative balance (due to an unexpected charge or uncollected fee) would prevent closure until settled. Ensure all outstanding checks have cleared and all pending transactions are complete. It’s a good practice to transfer funds out well in advance to allow all outstanding items to clear.

Request Confirmation of Closure

Once the process is complete, ask your bank for a formal letter or email confirming that the account has been successfully closed. This document should clearly state the account number, the date of closure, and confirm that there is no outstanding balance or pending liabilities associated with the account. Keep this confirmation in your financial records indefinitely. It is your ultimate proof that you are no longer responsible for that account.

What to Do with Debit Cards and Checkbooks

After your account is confirmed closed, securely destroy any associated debit cards and unused checkbooks. This prevents unauthorized use and reduces the risk of fraud. Shredding is recommended for checks and cutting up debit cards through the magnetic strip and chip is advisable. Do not simply throw them away intact.

Potential Pitfalls and How to Avoid Them

Even with careful planning, closing a bank account can present unforeseen challenges. Being aware of these common pitfalls allows you to proactively mitigate them.

Forgetting Recurring Payments

The most common and frustrating oversight is forgetting to update a recurring payment. This can lead to missed utility bills, late loan payments, or cancelled subscriptions, potentially incurring late fees, service interruptions, or damage to your credit score. This is why the initial step of reviewing all account activity is so crucial. Set reminders to update every single payment.

Overlooking Direct Deposits

Similarly, neglecting to reroute direct deposits can cause delays in receiving your salary, benefits, or other regular income. This can disrupt your personal cash flow and potentially lead to financial hardship. Inform your employer, government agencies, or other payors well in advance of the new account details and confirm the effective date of the change.

Insufficient Funds Charges

Attempting to close an account with outstanding debits or pending transactions can lead to an overdraft. If an automated payment or a check clears after you’ve moved all funds out, it could result in insufficient funds (NSF) charges, which are often hefty. These charges can prevent the account from closing until they are paid, trapping you in a cycle of fees. Ensure a small buffer of funds remains until you’re absolutely certain all transactions have cleared.

Account Reopening After Closure

In rare instances, an account might be “reopened” if a previously uncleared transaction or a charge that was missed somehow posts after the closure. While this is uncommon with modern banking systems, it can happen if a bank makes an error or a merchant charges you much later. The confirmation letter of closure is your defense against such occurrences. If an account is reopened, contact your bank immediately with your documentation.

Fraud and Identity Theft Concerns

If you are closing an account due to suspected fraud or identity theft, the process becomes even more critical. In such cases, alert your bank to the reason for closure immediately. They may have specific procedures, such as freezing the account first, investigating transactions, and guiding you on reporting to relevant authorities. Ensure all your personal information is updated and secured with your new financial institution.

What to Do After Your Account is Closed

The process doesn’t end the moment you receive your confirmation letter. A few final steps ensure your financial transition is complete and secure.

Monitor Your Credit Report

For several months after closing an account, it’s a good practice to monitor your credit report. While closing a checking or savings account doesn’t directly impact your credit score like a credit card closure, it’s a general best practice to check for any unexpected activity. This helps you confirm that no unauthorized transactions or accounts have been opened in your name, and that all linked services have indeed stopped attempting to charge the closed account. You can typically get a free credit report from each of the three major credit bureaus annually.

Keep Records of Closure

Store your account closure confirmation letter and any related correspondence (like your written request) in a safe place with your other important financial documents. This record serves as definitive proof that the account was properly closed and that you are no longer responsible for it. While issues are rare, having this documentation readily available can save you significant time and stress if a dispute or inquiry ever arises in the future.

Update All Linked Services

Beyond direct deposits and recurring payments, think about other services that might be linked to your old bank account. This could include online payment platforms (like PayPal or Venmo), e-commerce websites where your bank account was stored as a payment method, or even investment accounts where funds were transferred to and from. Proactively updating these linkages with your new account information ensures a smooth continuation of all your digital financial activities and prevents future failed transactions.

Conclusion

Closing a bank account, while seemingly a simple administrative task, requires a thoughtful and systematic approach. By understanding the reasons behind such a decision, meticulously preparing, following the correct procedures, and being aware of potential pitfalls, you can ensure a seamless financial transition. This guide has provided you with the necessary insights and steps to navigate this process confidently. Taking control of your financial architecture, down to the smallest detail of account management, is a hallmark of responsible personal finance. With careful planning and execution, you can close your bank account with peace of mind, knowing your financial house is in order.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.