Navigating the complexities of personal finance often involves making strategic decisions about where your money resides. For many, a checking account with a major institution like Chase serves as the primary hub for daily transactions, bill payments, and direct deposits. However, circumstances can change, prompting the need to close an account. Whether you’re consolidating finances, seeking better terms elsewhere, or simply streamlining your banking relationships, understanding the precise steps to close your Chase checking account is crucial. This guide provides a professional, insightful, and engaging roadmap to ensure a smooth and financially sound transition, keeping your personal financial health at the forefront.

Understanding Your Motivation for Account Closure

Before initiating the closure process, it’s beneficial to reflect on the reasons driving your decision. Recognizing your motivations not only helps in planning but also reinforces whether closing the account is indeed the best financial move for your unique situation. This internal assessment can uncover overlooked factors and help you avoid future regrets.

Streamlining Finances and Reducing Fees

One of the most common reasons individuals opt to close a checking account is to streamline their financial landscape. Juggling multiple accounts, especially if they’re not actively used, can lead to unnecessary complexity and, more critically, avoidable fees. Many banks, including Chase, impose monthly service fees if certain balance requirements aren’t met or if direct deposit thresholds aren’t maintained. If an account is dormant or rarely used, these cumulative charges can erode your savings over time. Closing such an account can simplify your financial oversight and free you from unnecessary costs, allowing your money to work harder for you elsewhere. This move aligns with sound financial principles of efficiency and cost management.

Dissatisfaction with Service or Features

Another significant driver for account closure stems from a dissatisfaction with the current banking experience. This could range from subpar customer service, inconvenient branch access, or a lack of desired digital banking features. In today’s competitive financial market, consumers have a plethora of choices, and loyalty is often predicated on value and convenience. If Chase’s offerings no longer align with your evolving needs or expectations, exploring alternatives and subsequently closing your account is a rational response. This move empowers you to seek out a financial institution that better caters to your personal banking preferences and technological demands, ultimately improving your daily financial interactions.

Transitioning to a New Financial Institution

Sometimes, the decision to close a Chase checking account is part of a broader strategy to transition to an entirely new financial institution. This might be prompted by a move to a new city where Chase’s branch network is less robust, or perhaps a new bank is offering more attractive interest rates, lower fees, or specialized services like robust investment platforms or tailored credit card rewards. The allure of a sign-up bonus, improved mobile banking, or a more community-focused banking experience can also be powerful motivators. Successfully transitioning requires careful planning to ensure uninterrupted access to funds and services during the switch, making the closure of the old account a final, critical step in the process.

Consolidating Accounts

For individuals who have accumulated multiple checking accounts over the years – perhaps from different life stages or financial goals – consolidation can be a compelling reason for closure. Having too many accounts can fragment your financial picture, making it harder to track spending, manage cash flow, and achieve overarching financial objectives. By consolidating, you centralize your funds, gain a clearer overview of your financial health, and potentially qualify for better perks or higher interest rates with a single, primary bank due to a larger aggregate balance. This strategic move streamlines your financial management, making it easier to monitor, budget, and plan for your future.

Essential Preparatory Steps Before Closing Your Account

Closing a checking account is more than just telling the bank you want out; it requires meticulous preparation to prevent financial disruptions and potential headaches. Overlooking these critical steps can lead to bounced payments, unexpected fees, or difficulties accessing your funds. Think of this as a pre-flight checklist for your financial transition.

Transferring Funds and Settling Debts

The absolute first step is to ensure that all funds you wish to retain are transferred out of your Chase checking account. This means initiating transfers to a new bank account, a savings account, or even withdrawing cash. Simultaneously, it’s imperative to settle any outstanding debts linked to the account. Check for any pending debit card transactions, uncashed checks you’ve written, or recurring payments that might still be processed. Any transactions that post after you attempt to close an account can complicate the process, potentially leading to overdraft fees or delays. Aim for a zero balance, or a nominal amount to cover any unforeseen final debits, before officially requesting closure.

Updating Direct Deposits and Automatic Payments

One of the most critical and often overlooked aspects of closing a checking account is redirecting all direct deposits and automatic payments. This includes your salary, government benefits, investment dividends, and any other regular inflows. Contact your employer’s payroll department, Social Security Administration, or other payers to update your banking information to your new account.

Equally important is identifying and updating all automatic payments and subscriptions. This encompasses utilities, mortgage/rent, loan payments, insurance premiums, streaming services, gym memberships, and any other recurring bills linked to your Chase checking account. Failure to update these can result in missed payments, late fees, and potential damage to your credit score. Create a comprehensive list by reviewing at least six months of your bank statements to identify every recurring transaction. Set up new payments with your new bank account before closing the old one to ensure continuity.

Reviewing Account Activity and Statements

Before you finalize the closure, take the time to thoroughly review your recent account activity and statements. Look for any discrepancies, unfamiliar transactions, or potential errors that need to be resolved while the account is still active. Ensure all checks you’ve written have cleared and that no outstanding deposits are pending. Download and save digital copies of at least the past year’s statements, or more if legally required for tax purposes or personal records. These documents are vital for future reference, tax filing, or disputing any post-closure issues that might arise. Having a complete historical record is a cornerstone of responsible financial management.

Saving Important Records

Beyond statements, consider saving any other important records related to your Chase account. This could include account agreements, fee schedules, correspondence with customer service, or any specific details about linked services (like specific savings accounts, credit cards, or investment accounts within Chase). Digital copies are often sufficient and environmentally friendly, but ensure they are backed up securely. Having these records readily accessible can be invaluable if you encounter any issues during or after the closure process, providing proof of your actions and account terms.

Navigating the Chase Account Closure Process

Once your preparatory steps are complete, you’re ready to formally initiate the closure of your Chase checking account. Chase offers several avenues for this, each with its own nuances. Understanding these options and what to expect will help you choose the most convenient and efficient method.

Online, Phone, or In-Person Options

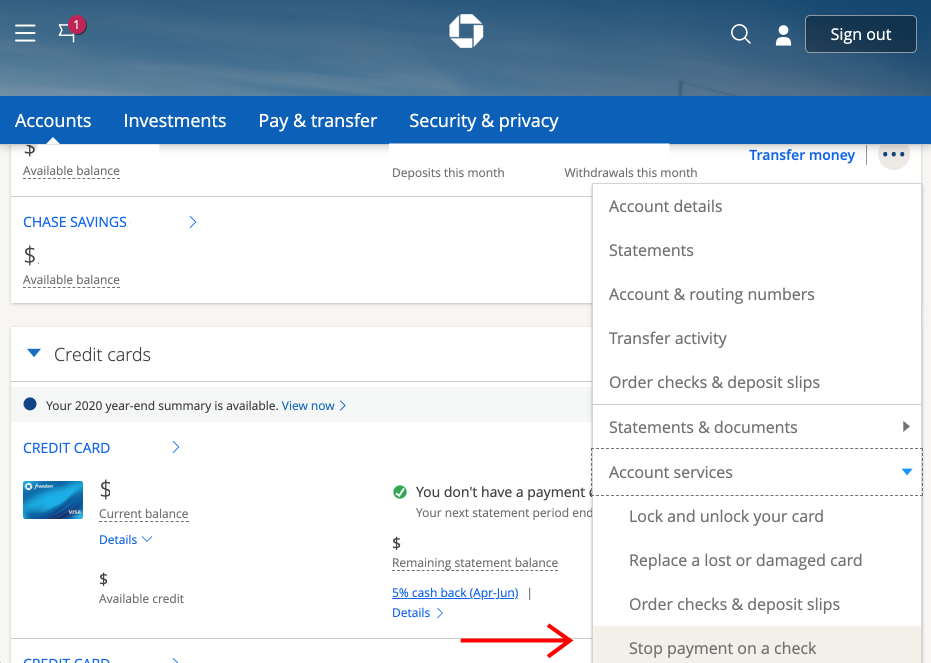

Chase typically provides a few methods to close an account:

- Online: For some accounts and situations, Chase might allow closure through their secure online banking portal. This is often the most convenient if available, requiring you to log in and navigate to your account settings or a dedicated “close account” section. However, online closure might be restricted if there are complex issues or specific balance requirements.

- Phone: You can call Chase customer service to request account closure. Be prepared to verify your identity thoroughly (account numbers, Social Security number, address, security questions). This method allows you to speak directly with a representative who can guide you through the process and answer immediate questions. The main number for Chase customer service can typically be found on their website or the back of your debit card.

- In-Person: Visiting a Chase branch is often recommended, especially if you have a remaining balance you wish to withdraw as cash or a cashier’s check, or if you prefer face-to-face assistance. Bring valid government-issued identification (e.g., driver’s license, passport) and your debit card. A branch representative can guide you through the forms and ensure all necessary steps are taken on the spot.

Choose the method that best suits your comfort level and the specifics of your account. For absolute certainty and immediate resolution, an in-person visit is often the most foolproof.

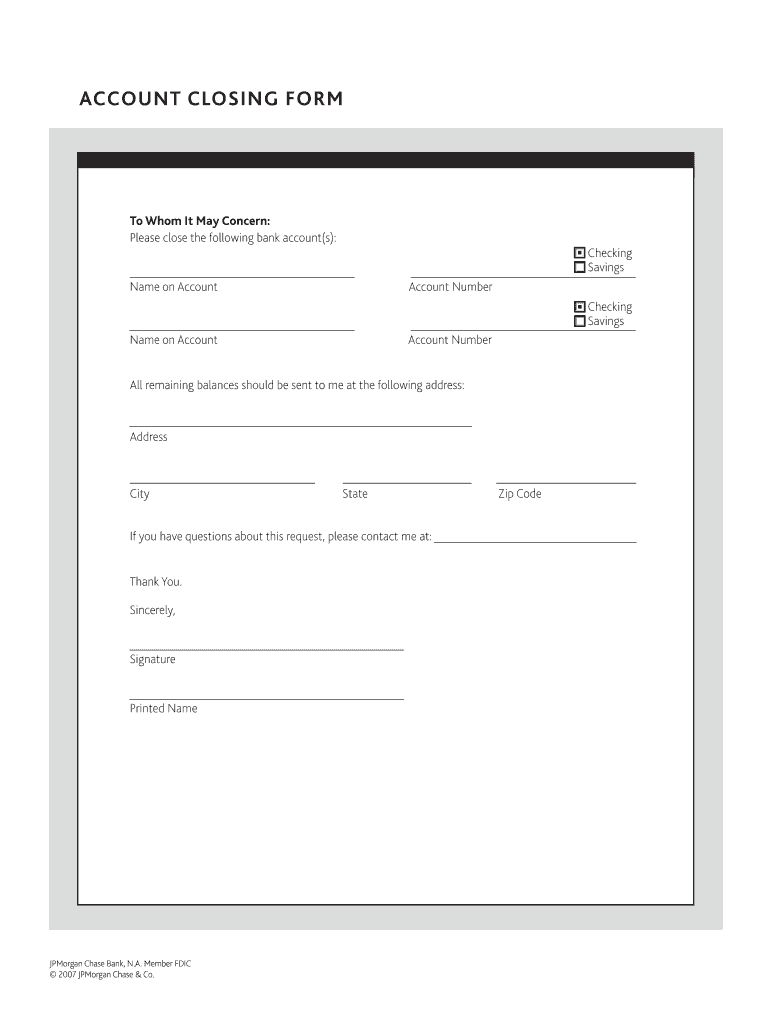

Required Information and Documentation

Regardless of the method you choose, be prepared to provide specific information to verify your identity and authorize the account closure. This typically includes:

- Your Chase checking account number(s).

- Your full name and current address.

- Your Social Security Number.

- A valid form of government-issued photo identification (e.g., driver’s license, passport) if closing in person.

- The reason for closure (though this is primarily for their internal records and not a barrier to closure).

Ensure you have all this information readily available to expedite the process. If you’re closing over the phone, have your account information handy before you call.

Verifying Account Balance and Potential Fees

Before the final closure, the Chase representative will likely review your account balance. If there’s a remaining balance, you’ll need to decide how to disburse it – direct transfer to another bank, cashier’s check, or cash withdrawal (if in person). Be aware of any potential fees that might apply during closure. While closing a standard checking account usually doesn’t incur a direct “closure fee,” you might still be subject to fees if your account has a negative balance due to past overdrafts or if you’re requesting a wire transfer for the remaining funds. Clarify any final charges with the representative to avoid surprises. Ensure that you leave enough funds to cover any pending transactions that haven’t yet cleared, as this is a common pitfall.

Receiving Confirmation of Closure

Once the closure request is processed, it is absolutely essential to obtain official confirmation in writing. This could be an email, a letter mailed to your address, or a printed document if you close in person. This confirmation serves as your proof that the account has been officially closed and that you are no longer responsible for it. The confirmation should clearly state the date of closure and that the account balance is zero. Keep this document in your financial records indefinitely. Without official confirmation, you run the risk of the account remaining open (perhaps with a small balance that could accrue fees), or difficulties resolving any future disputes.

Post-Closure Best Practices and Considerations

Closing your Chase checking account doesn’t mean your responsibilities end the moment you receive confirmation. A few crucial follow-up steps and ongoing practices are vital for maintaining your financial hygiene and security.

Monitoring Your Credit Report

Although closing a checking account doesn’t directly impact your credit score in the same way closing a credit card might, indirect effects can arise if bills linked to the closed account are missed. Therefore, it’s wise to monitor your credit report in the months following the closure. Ensure that all your recurring payments, which you transferred to your new account, are being processed correctly and that no late payments appear due to oversight during the transition. You can obtain a free copy of your credit report from AnnualCreditReport.com once every 12 months from each of the three major credit bureaus (Equifax, Experian, and TransUnion). This vigilance helps safeguard your financial reputation.

Retaining Confirmation Records

As mentioned earlier, the written confirmation of your account closure is a critical document. Do not discard it. Keep it with your other important financial records, either digitally backed up or in a secure physical location. This record is your proof that you fulfilled your obligations and that the account is officially closed. Should any future discrepancies arise, such as an attempt by Chase or a third party to claim an outstanding balance or to reactivate the account, your confirmation document will be your primary defense. Think of it as your “get out of jail free” card for any post-closure challenges.

What to Do with Old Debit Cards and Checks

Once your account is definitively closed and all funds are transferred, your old Chase debit card and any unused checks become obsolete. For security reasons, it’s paramount to destroy them properly. Do not simply throw them in the trash. Cut up your debit card through the chip and magnetic stripe to render it unusable. Shred any unused checks to prevent unauthorized access to your old account information. This small but important step prevents fraud and protects your personal information from falling into the wrong hands.

Common Pitfalls and How to Avoid Them

Even with careful planning, some common mistakes can derail a smooth account closure. Being aware of these pitfalls can help you navigate the process without incident and protect your financial well-being.

Overlooking Pending Transactions

One of the most frequent errors is underestimating the time it takes for transactions to clear. A debit card purchase or a check written a few days before you attempt to close the account might still be pending. If you close the account with a zero balance before these transactions clear, they will likely be rejected, potentially leading to fees for you (from the merchant) and complications with Chase. Always allow a buffer period—at least 5-7 business days after your last transaction—before attempting to close the account. Confirm with the bank representative that no pending debits or credits are outstanding.

Not Updating Recurring Payments

As highlighted in the preparatory steps, failing to update all direct deposits and automatic payments is a major pitfall. A missed salary deposit can cause significant financial stress, while missed bill payments can incur late fees and negatively impact your credit score. The key is to be exhaustive: review multiple months of statements to catch every single recurring transaction. Start the update process with your new bank account well in advance of closing the old one, ensuring a seamless transition and avoiding any service interruptions or financial penalties. Set reminders and double-check with billers to confirm they have the new banking information.

Unexpected Fees

While direct closure fees are uncommon, unexpected fees can still arise. These might include minimum balance fees if you dip below a certain threshold before closure, overdraft fees if a pending transaction overdraws the account, or fees for specific services like expedited wire transfers for your remaining balance. Always inquire about any potential final fees when speaking with a Chase representative. Aim to have a clear, confirmed zero balance or a final positive balance that can be transferred without additional cost. Proactive communication and careful account review are your best defense against unexpected charges.

Closing a Chase checking account, while seemingly straightforward, requires a structured approach rooted in sound personal finance principles. By understanding your motivations, meticulously preparing, diligently navigating the closure process, and adhering to post-closure best practices, you can ensure a smooth transition. This level of financial diligence not only prevents costly mistakes but also empowers you with greater control over your financial landscape, paving the way for a healthier and more streamlined monetary future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.