Deciding to close a bank account or a credit card is a significant financial move that requires more than a simple phone call. Whether you are streamlining your portfolio, moving to a different institution with better interest rates, or consolidating your debt, the process of closing a Capital One account must be handled with precision to avoid negative impacts on your credit score and financial health.

As one of the largest financial institutions in the United States, Capital One offers a variety of products ranging from 360 Checking and Savings accounts to high-tier travel rewards credit cards. Each of these products has a different set of implications when terminated. In this guide, we will explore the strategic steps necessary to close your account professionally while safeguarding your financial reputation.

Strategic Preparation: Clearing the Path for a Clean Break

Before you initiate the closure of any financial account, you must perform “financial hygiene.” Simply cutting up a card or withdrawing your balance is insufficient. You must ensure that the “pipes” of your personal economy are redirected to avoid missed payments or returned deposits.

Auditing Recurring Transactions and Direct Deposits

The modern financial life is built on automation. From monthly subscriptions like Netflix and Spotify to essential utilities and insurance premiums, many of our expenses are tethered to specific account numbers or credit cards. Before closing your Capital One account, review at least three to six months of statements. Identify every recurring charge and update them with your new banking information.

Equally important is the redirection of income. If your employer utilizes direct deposit, it can take one to two pay cycles for a change to take effect. If you close your Capital One account before your HR department updates their system, your paycheck may be rejected and returned to your employer, causing a significant delay in your liquidity.

Addressing Pending Transactions and Residual Interest

A common mistake in account closure is failing to account for “trailing interest” or pending transactions. For credit cards, interest is often calculated daily. Even if you pay your statement balance in full, you might see a small interest charge on the following statement for the period between the statement closing date and the date your payment was received.

For checking and savings accounts, ensure that every check you have written has cleared. A “zombie” check that hits a closed account can lead to returned item fees and may even be reported to ChexSystems, which could make it difficult for you to open bank accounts at other institutions in the future.

Transferring Your Remaining Balance

Once you are certain that all transactions have cleared, you must move your capital. For Capital One 360 accounts, this is easily done through an Electronic Funds Transfer (EFT) to an external bank. It is advisable to leave a small buffer of $20 to $50 in the account until the very final day of closure to cover any unforeseen micro-transactions. If you are closing a credit card with a rewards balance (Venture miles or Savor cash back), ensure you redeem or transfer those rewards before closing, as most rewards are forfeited the moment the account is shut down.

The Execution: Formal Methods for Account Termination

Capital One provides several channels for account closure. The method you choose may depend on whether you are dealing with a depository account (Banking) or a line of credit (Credit Card).

Closing Your Account Online or via the Mobile App

For many Capital One 360 Checking and Savings customers, the process can be initiated through the digital banking portal. If the account balance is zero and there are no pending holds, the “Account Services” or “Settings” menu often provides an option to close the account. However, this is not always available for credit card accounts. Capital One frequently requires a direct conversation for credit products to ensure the customer understands the implications of the closure and to offer potential alternatives.

Contacting Customer Service via Phone

The most definitive way to close a Capital One account is by speaking with a representative. For credit cards, you can call 1-800-227-4825. For banking inquiries, the number is 1-888-464-0727. When you call, be prepared for a “retention pitch.” Banks are incentivized to keep customers, and the representative may offer to waive fees or provide a rewards bonus to keep the account open. If your mind is made up, remain firm and professional. Request that the account be closed at “the customer’s request”—this specific phrasing can be beneficial if the closure is ever reviewed by a credit analyst.

Formalizing the Request in Writing

While digital and phone closures are standard, sending a certified letter is the “gold standard” for financial record-keeping. A brief letter stating your name, account number (only the last four digits for security), and the request to close the account provides a paper trail. This is particularly useful if a bank error occurs and the account remains active, potentially accruing monthly maintenance fees or inactivity fees that you would otherwise be liable for.

Understanding the Financial Implications: Credit Scores and History

Closing a bank account has zero impact on your credit score, but closing a credit card is a different story. In the world of personal finance, the “age” and “capacity” of your credit lines are vital metrics.

How Closing a Credit Card Affects Your Credit Utilization

Your credit utilization ratio—the amount of credit you are using compared to your total available credit—accounts for 30% of your FICO score. If you close a Capital One credit card with a $10,000 limit, your total available credit across all cards drops by that amount. If you carry balances on other cards, your utilization percentage will instantly spike, which can cause your credit score to drop. Before closing a card, calculate how it will affect your overall utilization.

The Importance of Credit History Length

The length of your credit history accounts for 15% of your score. If your Capital One card is one of your oldest accounts, closing it will eventually reduce the “average age” of your accounts. While closed accounts in good standing stay on your credit report for ten years, the loss of that open line of credit can eventually lower the maturity of your credit profile.

Strategic Decisions for Bank Accounts vs. Credit Cards

From a financial tool perspective, bank accounts are utilitarian. If a bank account no longer serves your needs or charges unnecessary fees, there is rarely a downside to closing it once your new banking infrastructure is in place. Credit cards, however, are strategic assets. If your Capital One card has no annual fee, it is often financially savvier to leave it open and use it for a small purchase once every six months to keep it active, thereby preserving your credit score’s integrity.

Post-Closure Protocol: Protecting Your Identity and Financial Records

The process does not end when the representative hangs up the phone. Vigilance in the weeks following a closure is essential for maintaining your financial security.

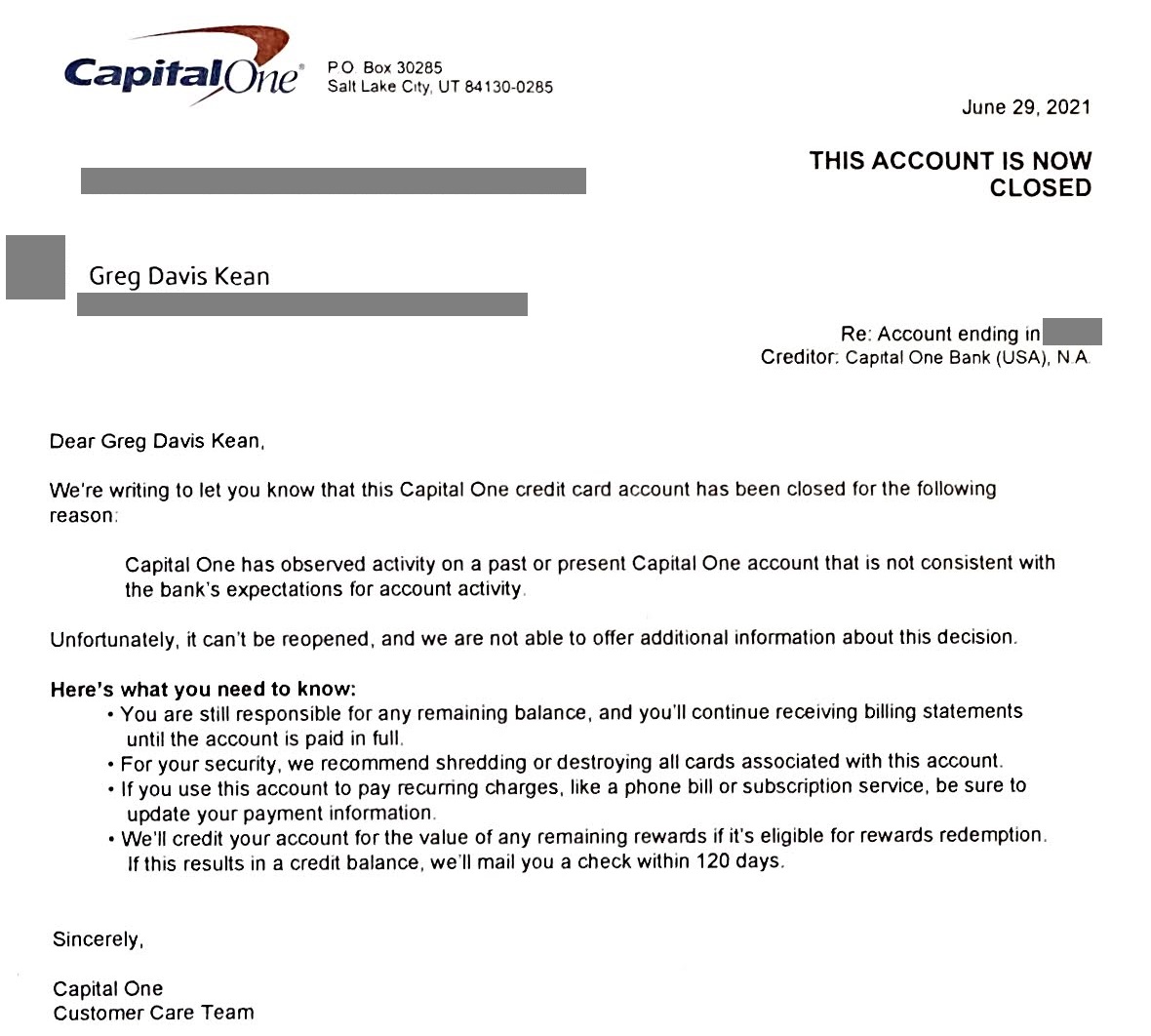

Requesting a Written Confirmation

Always demand a formal closure letter. This document should state that the account is closed and has a zero balance. If a fraudulent charge appears on the account later, or if the bank mistakenly reports it as “closed by grantor” (which can look negative to future lenders), this letter is your primary evidence to dispute the error with credit bureaus like Equifax, Experian, and TransUnion.

Safely Disposing of Physical Cards and Checkbooks

Metal credit cards, which are common with the Capital One Venture and Venture X, cannot be destroyed with standard kitchen scissors. You should ask Capital One for a prepaid envelope to return the card for secure destruction, or use heavy-duty shears. For checking accounts, shred all remaining checks. A single lost check from a “closed” account can be used by bad actors to attempt identity theft or check fraud, creating a massive administrative headache for you.

Monitoring Your Credit Report for Updates

It typically takes 30 to 60 days for a credit card closure to reflect on your credit report. Monitor your report using tools like Credit Wise (Capital One’s own tool, which often remains accessible even after closure) or AnnualCreditReport.com. Ensure the status is listed as “Closed at Consumer’s Request.”

Evaluating Alternatives: When to Pivot Instead of Closing

Sometimes, the desire to close an account stems from a specific pain point—like a high annual fee—rather than a desire to leave the bank entirely. In the Money niche, we call this “Product Optimization.”

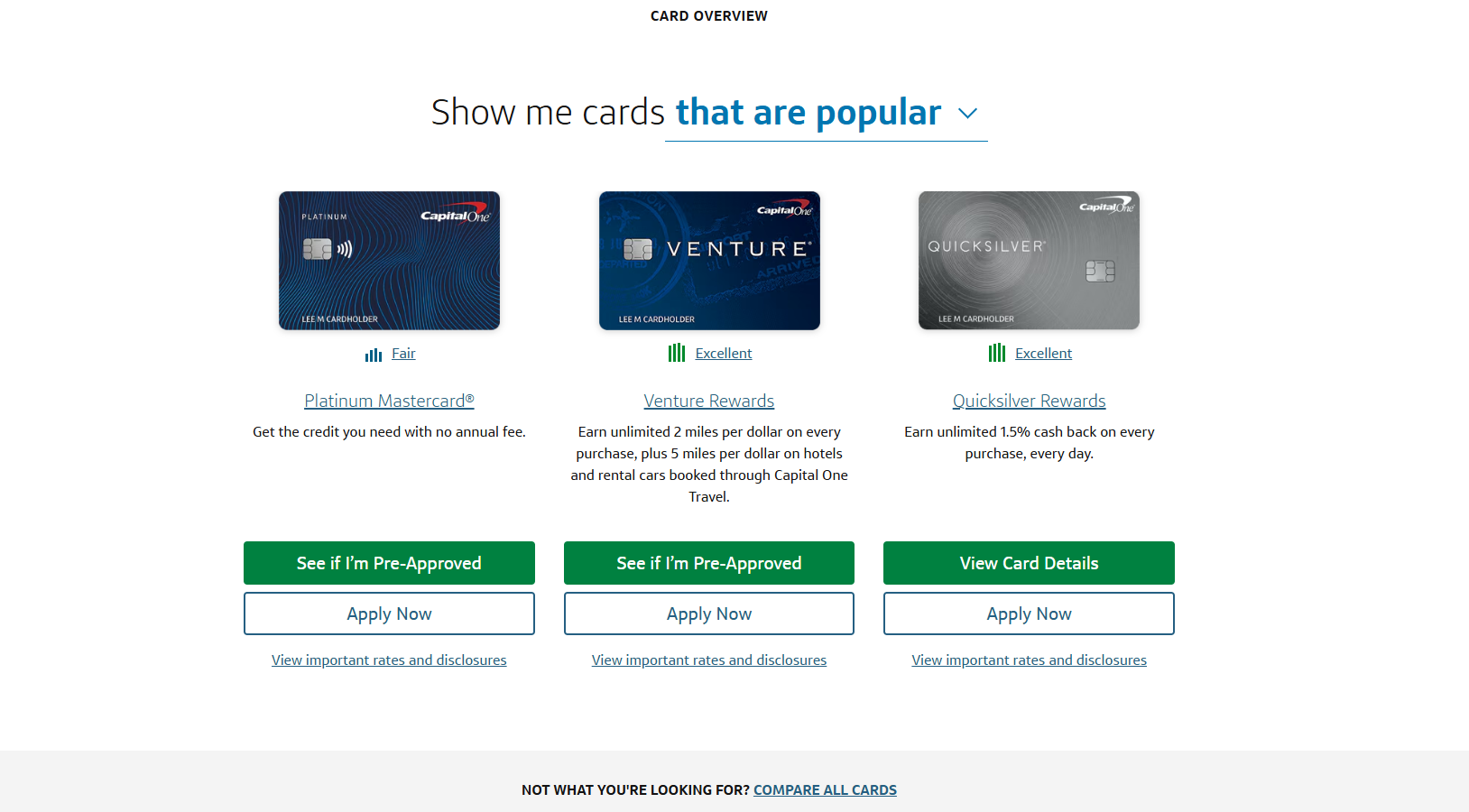

Product Switching and Account Downgrades

If you are closing a Capital One Venture X because the $395 annual fee is no longer justifiable, ask about a “Product Change.” Capital One often allows users to “downgrade” a high-fee card to a no-fee version, such as the VentureOne or the Quicksilver. This allows you to keep the credit line, the account age, and the available credit without paying the annual fee.

Consolidating Multiple Capital One Accounts

If you have multiple Capital One accounts and find them difficult to manage, you can sometimes consolidate your credit limits. While Capital One’s policies on “merging” credit lines vary, it is worth asking if you can move the credit limit from the card you wish to close onto a card you intend to keep. This mitigates the damage to your credit utilization ratio while still allowing you to simplify your financial life.

In conclusion, closing a Capital One account is a multi-step financial operation. By meticulously auditing your transactions, understanding the impact on your credit score, and maintaining a paper trail, you ensure that your exit from the institution is as smooth and professional as your entry. Always prioritize the long-term health of your credit profile over the short-term convenience of a quick closure.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.