Managing your personal finances effectively often requires more than just budgeting and investing; it involves the active curation of your financial tools. As the banking landscape evolves with higher interest rates, better digital interfaces, and more competitive fee structures, staying with a legacy bank out of habit can be a costly mistake. Closing a bank account is a significant financial move that, if executed poorly, can lead to missed payments, “zombie” accounts, and unnecessary fees.

This guide provides a comprehensive, professional roadmap for closing your bank accounts while maintaining your financial integrity and ensuring a seamless transition to a new institution.

Phase 1: Pre-Closure Preparation and Financial Auditing

Before you notify your bank of your intent to leave, you must conduct a thorough audit of your current financial workflow. A bank account is rarely an isolated silo; it is usually the hub of a complex web of automated transactions.

Identifying All Linked Transactions

The most common mistake consumers make when closing an account is overlooking a recurring “invisible” payment. You should review at least twelve months of bank statements to identify every automated clearing house (ACH) transfer, subscription, and utility payment linked to the account. This includes annual subscriptions that you might have forgotten about, such as professional memberships or insurance premiums. Creating a comprehensive spreadsheet of these outflows is the first step in ensuring a clean break.

Redirecting Direct Deposits and Automated Payments

Once you have identified your recurring transactions, the sequence of moving them is critical. Start by redirecting your primary income sources, such as employer direct deposits, Social Security benefits, or investment dividends. It is advisable to wait until at least one full pay cycle has successfully landed in your new account before moving to the next step.

Simultaneously, update your payment information for “high-stakes” bills. Missing a mortgage payment or an insurance premium due to a closed account can have immediate negative consequences for your credit score or coverage status. For smaller subscriptions, like streaming services, you can afford a bit more flexibility, but the goal is to leave nothing tied to the old account.

Managing the Final Balance and Avoiding Overdrafts

It is tempting to withdraw all funds immediately, but this is a tactical error. You should leave a “cushion” of funds in the old account for at least 30 to 60 days to cover any lingering transactions you may have missed. During this period, avoid using the old account for any new purchases. Calculate the exact amount needed to meet the bank’s minimum balance requirement to avoid monthly maintenance fees while the account remains open. This balance acts as a buffer against accidental overdrafts during the transition period.

Phase 2: Selecting and Transitioning to a New Financial Institution

Closing an account is usually motivated by the search for a better financial partner. Whether you are seeking higher yields on your savings or lower overhead for your business, the selection process should be data-driven.

Evaluating High-Yield Options and Fee Structures

In the current economic climate, the disparity between traditional “brick-and-mortar” interest rates and online-first high-yield savings accounts (HYSA) is vast. When choosing your next institution, prioritize those with competitive Annual Percentage Yields (APY) and transparent fee schedules. Look for “fee-free” checking options that do not require high minimum balances or complex monthly requirements. Additionally, ensure the institution is FDIC-insured (for banks) or NCUA-insured (for credit unions), providing the fundamental safety net for your capital.

The “Parallel Run” Strategy

Financial professionals recommend a “parallel run” strategy when switching banks. This involves keeping both the old and new accounts active simultaneously for one to two months. During the first month, fund the new account and begin moving your automated payments. During the second month, observe the old account to ensure no “stray” transactions occur. This overlap minimizes the risk of a “failed payment” fee from a biller or a “non-sufficient funds” (NSF) fee from the old bank. It is the most conservative and effective way to manage a total transition of your liquid assets.

Phase 3: Executing the Account Closure

Once your new account is fully functional and the old account has been dormant for a full billing cycle, you are ready to execute the formal closure.

Methods of Closure: Digital vs. In-Person

While many modern banks allow you to close accounts via a mobile app or online portal, this is not always the most secure or definitive method. For larger institutions, visiting a branch in person allows you to speak with a personal banker, receive immediate confirmation, and walk away with a printed receipt of the closure.

If you choose to close the account over the phone, ensure you are speaking with a representative in the “Account Retention” or “Closing” department. Be firm but polite; their job is to convince you to stay with promotional offers. If those offers do not align with your long-term financial goals, proceed with the closure and request an email confirmation immediately.

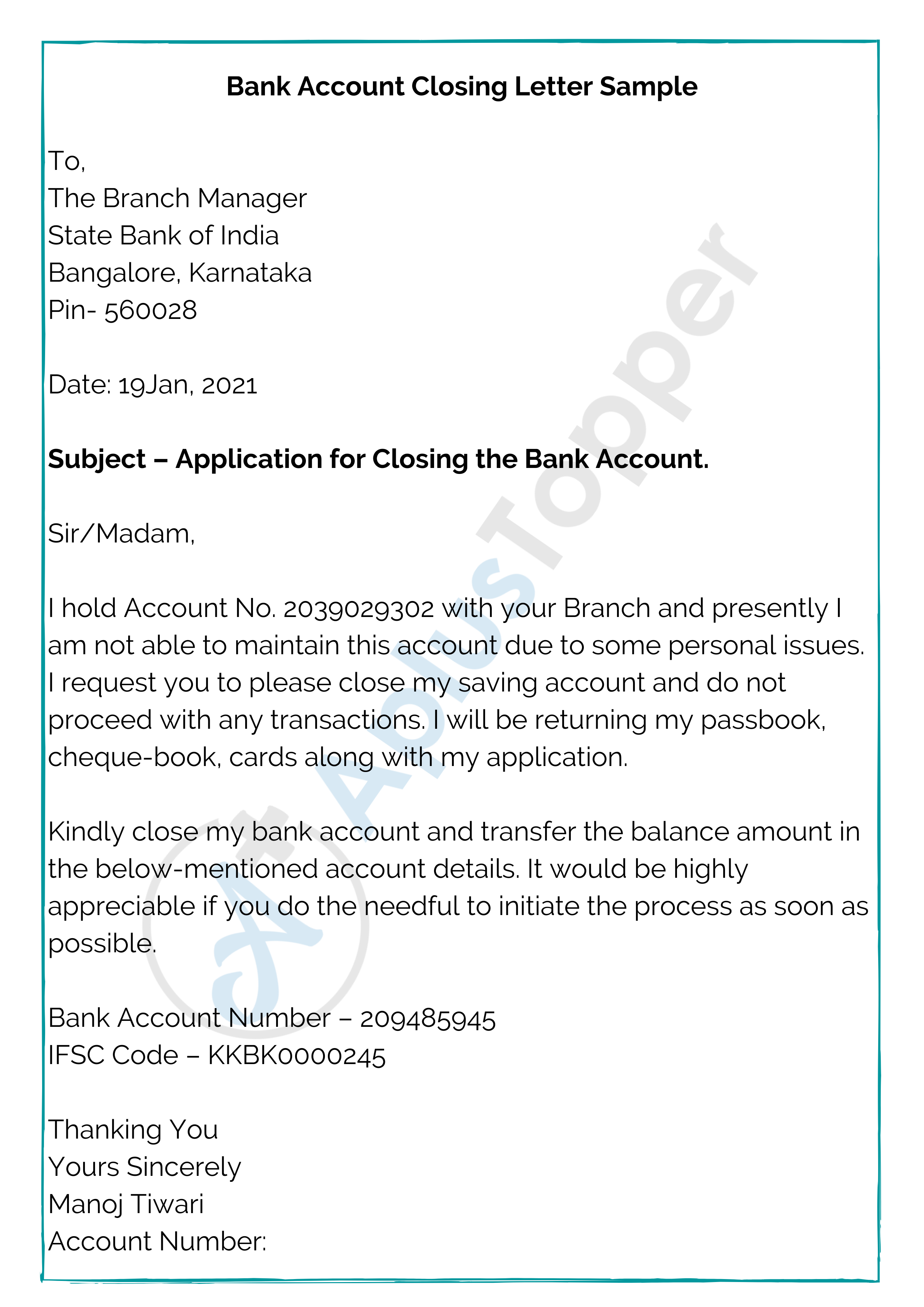

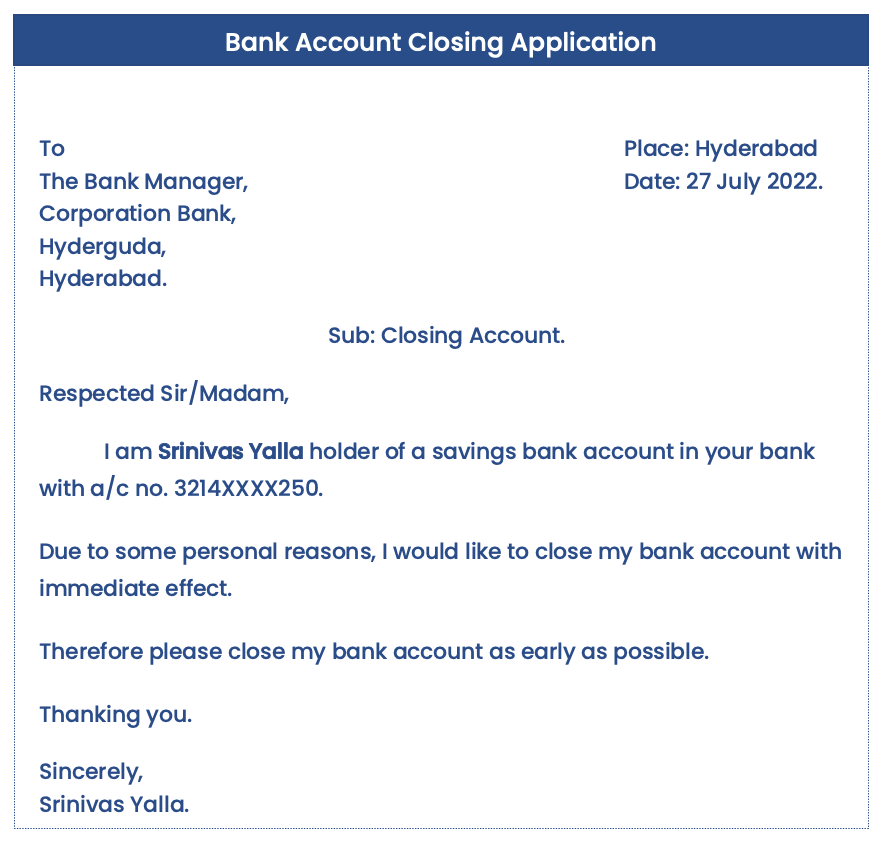

Essential Documentation and Written Requests

For the highest level of financial security, many experts recommend sending a formal account closure letter via certified mail with a return receipt requested. This creates a legal paper trail. Your letter should include:

- Your full name and current address.

- The account number(s) to be closed.

- A formal request to stop all future transactions.

- Instructions on how to handle the remaining balance (e.g., “Send a check to the address on file”).

- A request for a written confirmation that the account balance is zero and the account is closed in good standing.

Handling Business and Joint Accounts

Closing business or joint accounts requires additional steps. For a business account, the bank may require a “Corporate Resolution” or minutes from a board meeting authorizing the closure, depending on your business structure (LLC, S-Corp, etc.). For joint accounts, most institutions require the consent and signatures of both account holders. It is vital to coordinate this with your partner or co-owner to ensure that both parties are aware of the timing and the destination of the remaining funds.

Phase 4: Post-Closure Safeguards and Long-Term Impact

The process does not end the moment you receive a closure confirmation. There are several administrative and systemic factors to monitor to ensure the closure remains permanent and beneficial.

Monitoring for “Zombie Accounts” and Reopening Risks

A “zombie account” occurs when a closed account is automatically reopened by the bank because a stray ACH transaction or a late-arriving check was presented for payment. When the bank “helpfully” reopens the account to process the transaction, they may charge you an overdraft fee and a monthly maintenance fee.

To prevent this, ensure you receive a “Letter of Finality” or a closing statement showing a zero balance. Continue to monitor your mail for at least 90 days post-closure for any statements or notices from the old bank. If you see a “zombie” transaction, contact the bank immediately to dispute the reopening.

Understanding the Impact on Your Credit Score and ChexSystems

One of the most common misconceptions is that closing a checking or savings account will hurt your credit score. Unlike credit cards, bank accounts do not typically appear on your FICO or VantageScore reports. However, they do impact your ChexSystems report.

ChexSystems is a consumer reporting agency that tracks “mishandled” bank accounts. If you close an account with a negative balance or unpaid fees, it will be reported here, making it extremely difficult to open a bank account elsewhere for up to five years. By ensuring your account is closed with a zero or positive balance and in “good standing,” you protect your banking reputation.

Record Keeping and Final Tax Statements

Finally, maintain your records. You will still need your 1099-INT forms for tax season to report any interest earned on the account prior to its closure. Since you will likely lose access to the online banking portal once the account is closed, download the last two years of statements and your final tax documents before you initiate the closure. Store these in a secure digital vault or a physical filing system for at least seven years, as per standard financial record-keeping recommendations.

By following this structured approach, you transform a potentially chaotic administrative task into a strategic financial upgrade. Closing a bank account is not just about leaving an old institution; it is about taking active control of your capital and ensuring your financial tools are working as hard as you are.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.