Managing your personal finances requires agility. As your financial goals evolve, the banking institutions that once served you may no longer align with your needs. Whether you are seeking higher interest rates, looking to avoid monthly maintenance fees, or simply consolidating your accounts for better oversight, knowing how to close a Chase checking account efficiently is a vital financial skill.

While Chase is one of the “Big Four” banks in the United States, offering a vast network of ATMs and branches, many consumers eventually find that more specialized financial tools or high-yield accounts suit their long-term wealth-building strategies better. Closing a major bank account, however, is not as simple as clicking a “delete” button. It requires a strategic approach to ensure your liquidity is protected and your credit remains untarnished.

1. Essential Pre-Closure Financial Housekeeping

Before you initiate the closure of your Chase checking account, you must perform a thorough audit of your current financial workflow. Abruptly closing an account without preparation can lead to missed payments, “zombie” accounts that reactivate due to incoming transfers, and potential hits to your ChexSystems report.

Audit Your Automatic Payments and Direct Deposits

The most common mistake in account closure is forgetting a recurring subscription or a utility payment. Review at least three to six months of bank statements to identify every automated clearing house (ACH) transfer. This includes gym memberships, streaming services, insurance premiums, and mortgage payments. You must transition these to your new financial institution at least one full billing cycle before closing the Chase account. Simultaneously, notify your employer’s payroll department to redirect your direct deposit. Because payroll updates can take one to two pay cycles, it is wise to keep a small buffer of cash in your Chase account until the first deposit successfully lands in your new bank.

Clear Outstanding Transactions

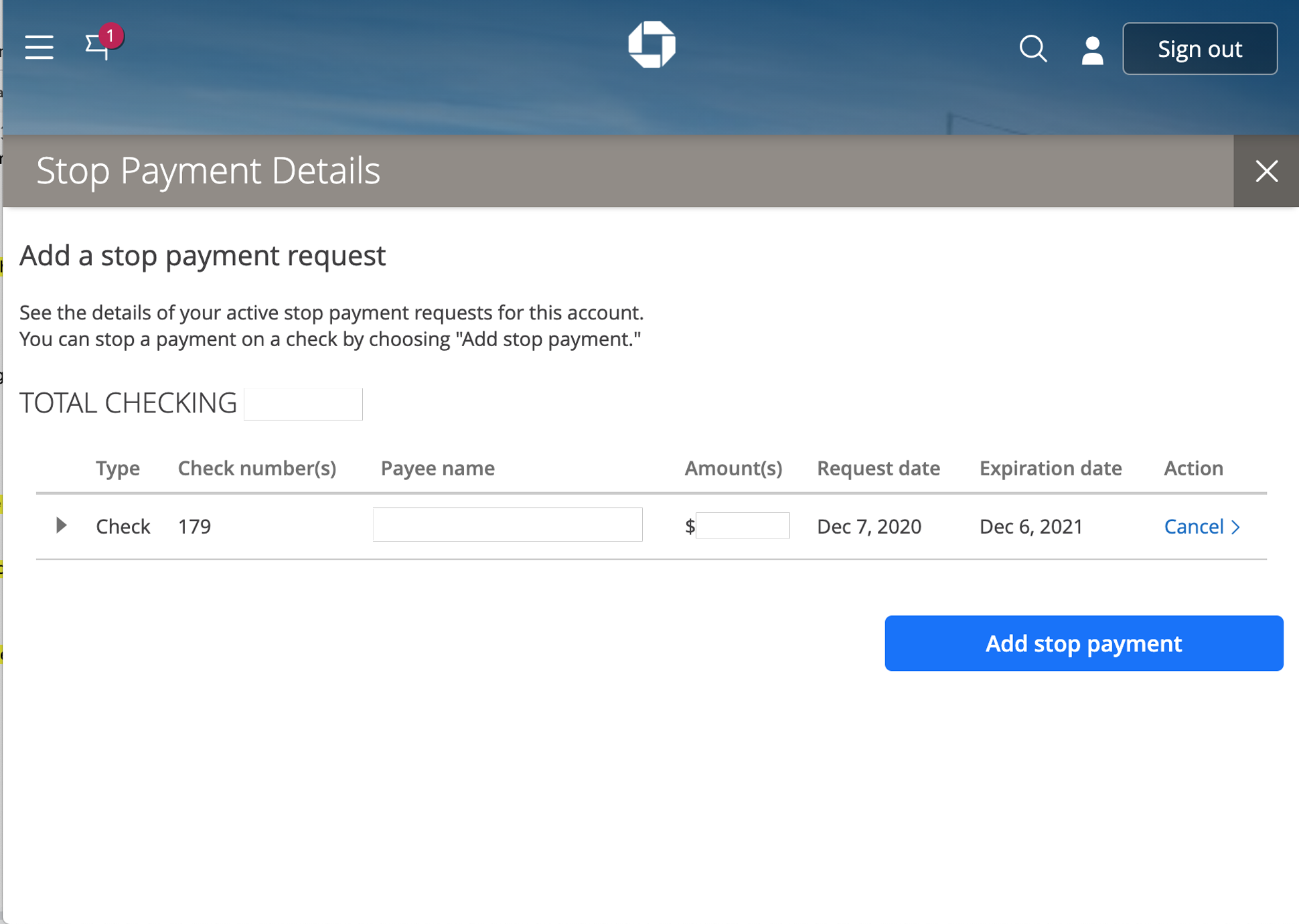

A “pending” transaction is the primary enemy of a smooth account closure. If you have recently written a check or used your debit card for a purchase that hasn’t cleared, Chase will likely deny your request to close the account. Ensure that every check you’ve written has been cashed. If a check remains outstanding for a long period, contact the recipient to ensure they process it, or consider placing a stop-payment order if the check is lost, though this often incurs a fee.

Strategic Balance Transfer

Once your automated payments have been moved and all transactions have cleared, you should transfer the bulk of your funds to your new account. However, avoid zeroing out the account entirely if you are not closing it the same day. Many Chase accounts require a minimum daily balance to waive monthly service fees (often ranging from $12 to $25). If your balance hits zero and a fee is assessed before the account is officially closed, you will be left with a negative balance, which complicates the closure process.

2. Methods to Close Your Chase Account

Chase offers several channels for account closure, catering to different preferences for speed and documentation. Choosing the right method depends on your comfort level with digital tools versus face-to-face interaction.

Closing via Secure Message Center (The Digital Approach)

For those who prefer a paper trail without the need for a phone call, the Chase Secure Message Center is an effective tool. Log into your Chase online banking portal or the mobile app, navigate to the “Secure Messages” section, and compose a new message. Clearly state that you wish to close your specific checking account (include the last four digits of the account number).

This method is highly professional as it provides a time-stamped record of your request. However, be aware that Chase may reply with a series of retention questions or ask you to call a specific line if there are complicating factors like a negative balance or linked investment accounts.

Closing by Phone (The Direct Approach)

If you want immediate confirmation, calling Chase’s customer service line is the most direct route. You can reach their general support at 1-800-935-9935. When speaking with a representative, be firm but polite. Banks are incentivized to retain customers, so you may be offered fee waivers or other incentives to stay. If your mind is made up, simply reiterate that you are consolidating your finances and wish to proceed with the closure. Ensure you ask for a confirmation number and the name of the representative you spoke with for your records.

Closing in Person (The Traditional Approach)

For individuals with complex banking relationships—such as those with linked business accounts, safe deposit boxes, or certificates of deposit—visiting a local branch is often the best choice. Meeting with a personal banker allows you to settle any final fees on the spot and receive a printed receipt confirming the account is closed. This “wet-ink” confirmation is the gold standard for financial record-keeping, ensuring that no “zombie” activity can occur later without your knowledge.

3. Navigating Potential Pitfalls and Financial Risks

The process of closing an account is fraught with minor technicalities that can have outsized financial consequences if ignored. Understanding the mechanics of how banks handle closures can save you from unnecessary stress.

The “Zombie Account” Phenomenon

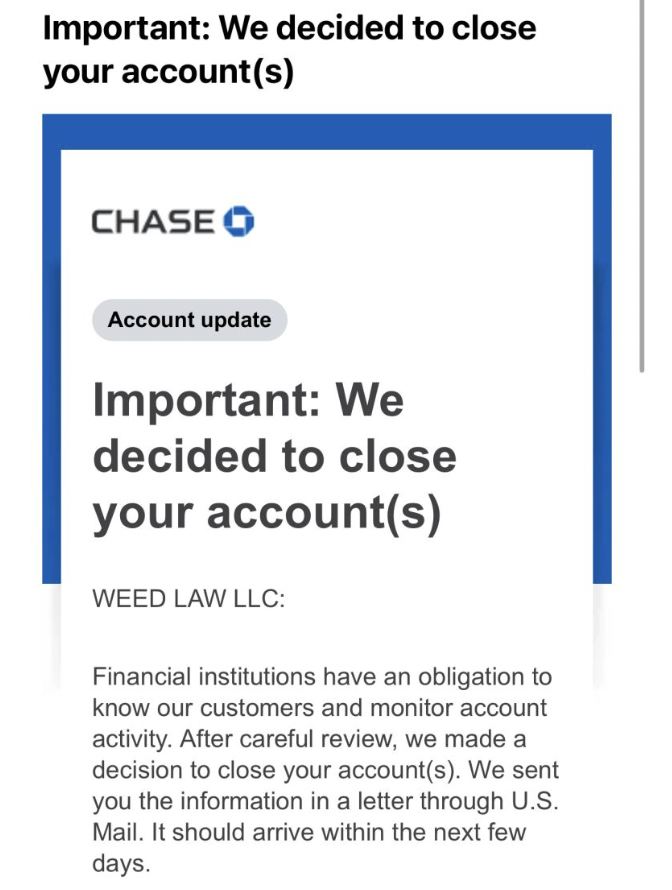

A “zombie account” occurs when an account you thought was closed is automatically reopened by the bank because a merchant attempted to charge a recurring payment or a direct deposit was sent to the old account number. To prevent this, ensure you have received a formal “Account Closed” letter from Chase. Once an account is truly closed in their system, most modern banking protocols will reject incoming ACH requests, but it is your responsibility to ensure no stray authorizations remain.

Managing Negative Balances and Overdrafts

Chase will not allow you to close an account that has a negative balance. If you have overdrawn your account, you must first bring the balance to zero (or positive). If you ignore a negative balance, Chase may eventually “charge off” the account and report the incident to ChexSystems. This is a specialized credit reporting agency used by banks. A negative mark on ChexSystems can make it incredibly difficult to open a checking or savings account at any other financial institution for up to five years.

Impact on Credit Scores

A common misconception in personal finance is that closing a checking account affects your FICO score. Because checking accounts are not lines of credit, closing one has no direct impact on your credit score. However, if you have a “standard” overdraft protection line of credit linked to that checking account, closing it will result in the closure of a credit line. This could slightly lower your total available credit and affect your credit utilization ratio, though the impact is usually negligible for most consumers.

4. Strategic Financial Planning Post-Chase

Once the Chase account is successfully closed, the focus shifts to optimizing your new financial setup. This is an opportunity to move away from “legacy banking” and toward modern wealth-building tools.

Evaluating High-Yield Savings Accounts (HYSA)

Traditional “Big Bank” checking accounts rarely offer competitive interest rates. As of the current market, many online-only institutions offer High-Yield Savings Accounts with APYs (Annual Percentage Yields) significantly higher than the national average. By moving your “idle” cash from a Chase checking account into a HYSA, you allow your money to work for you through the power of compound interest.

Assessing Neo-Banks vs. Traditional Institutions

The rise of “Neo-banks” or FinTech companies offers another alternative. These platforms often feature superior budgeting tools, no-fee structures, and seamless integration with investment platforms. However, they may lack the physical infrastructure of a bank like Chase. As a savvy financial consumer, you must weigh the benefit of “zero fees” against the convenience of having a physical branch for cash deposits or notary services.

5. Final Verification and Documentation

The final stage of closing your Chase checking account is the most critical for your long-term financial security: the verification of the closure.

Obtaining Written Confirmation

Never assume an account is closed just because you can no longer see it in your mobile app. Request a final statement and a formal letter of closure. Keep these documents in your physical or digital “Financial Life” folder for at least seven years. Should a dispute arise regarding a missed payment or an identity theft issue in the future, this documentation serves as your primary defense.

Proper Disposal of Physical Materials

Once the account is officially shuttered, your Chase debit cards and unused checks become liability risks. Do not simply throw them in the trash. Use a cross-cut shredder for all checks and cut through the EMV chip and magnetic stripe of your debit cards. This prevents “dumpster diving” identity thieves from accessing your old account information, ensuring that your transition from Chase is as secure as it is efficient.

By following this structured approach, you transition from a passive consumer to an active manager of your capital, ensuring that your banking choices always serve your broader financial objectives.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.