Navigating the landscape of higher education financing is often as complex as the degree itself. For many graduates, the transition from the classroom to the professional world is marked by the looming presence of student debt. However, the first step toward financial freedom is not necessarily making a massive payment, but rather gaining absolute clarity on what you owe. Understanding how to check your student loan balance is a foundational skill in personal finance that allows you to strategize, save on interest, and eventually clear your balance.

In this guide, we will explore the systematic ways to track down every dollar of your debt, differentiate between various loan types, and utilize financial tools to keep your repayment journey on track.

1. Navigating the Federal Student Aid Ecosystem

For the vast majority of American students, debt is primarily held by the federal government. Because federal loans offer specific protections, such as income-driven repayment (IDR) plans and Public Service Loan Forgiveness (PSLF), knowing exactly where you stand within the federal system is critical.

Utilizing StudentAid.gov

The definitive source for federal student loan information is StudentAid.gov. This portal acts as a central repository for all loans issued through the U.S. Department of Education. To access your balance, you will need your FSA ID—a username and password combination that serves as your legal signature.

Once logged in, your “Dashboard” provides a high-level overview of your total balance, including both the principal amount and the accrued interest. It is important to note that this dashboard is updated periodically, but it may have a slight lag compared to your servicer’s real-time data.

Identifying Your Loan Servicer

While the federal government owns your debt, they outsource the management of your payments to “servicers” like Nelnet, Mohela, or Aidvantage. On StudentAid.gov, you can find a specific section labeled “My Loan Servicers.”

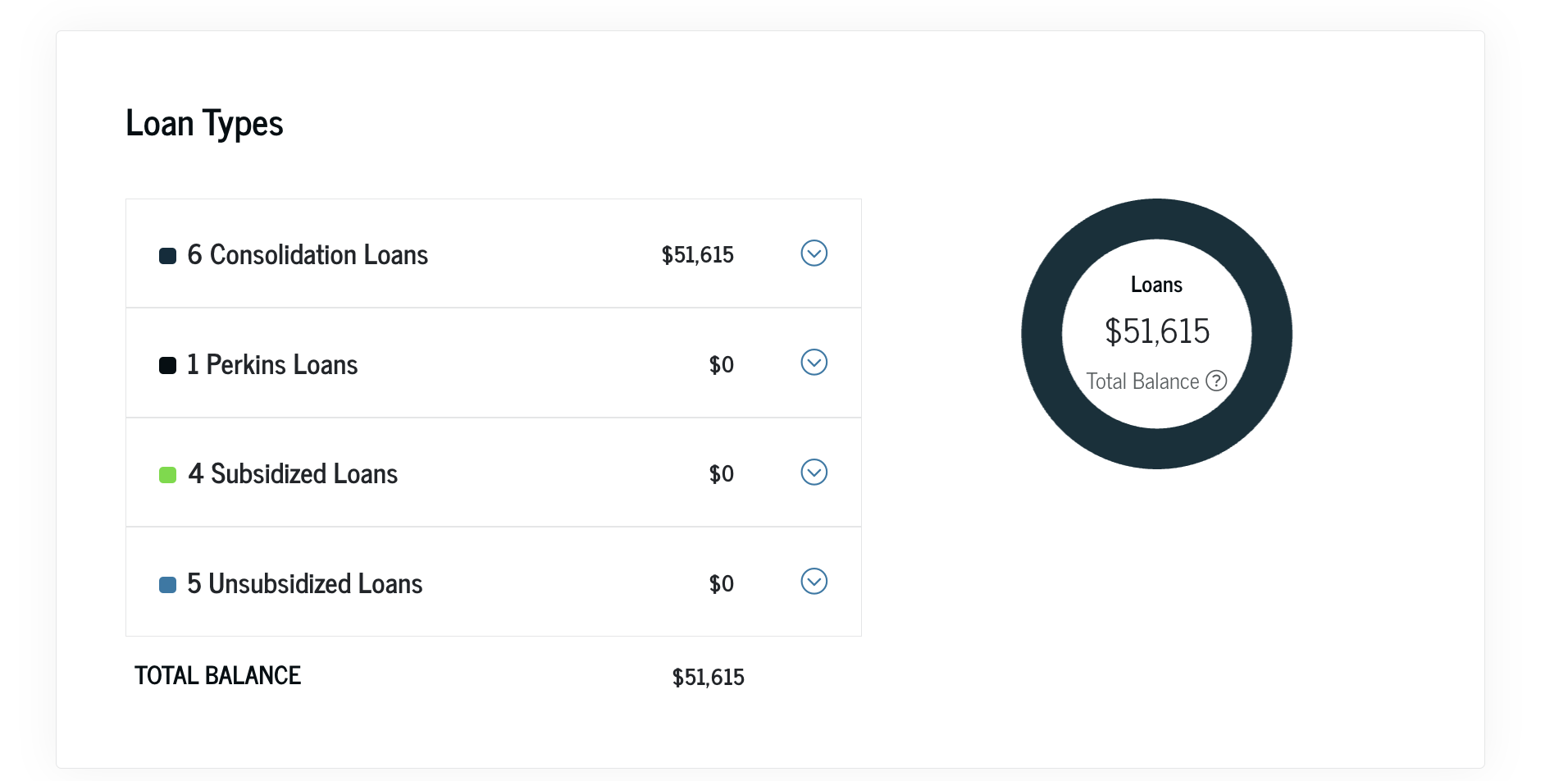

Identifying your servicer is vital because they are the entity you will actually pay. Each servicer has its own portal where you can see a detailed breakdown of your individual “loan groups” or “tokens.” Often, what looks like one large loan is actually a collection of several smaller loans from different semesters, each with its own interest rate.

Understanding Principal vs. Interest

When checking your balance, you must distinguish between the principal (the original amount borrowed) and the accrued interest. In the world of personal finance, interest is the cost of borrowing. If you are in a period of deferment or a specific repayment plan where your payments don’t cover the interest, your total balance can actually grow—a process known as negative amortization. Regularly checking your balance helps you identify if your debt is “snowballing” in the wrong direction.

2. Uncovering Private Student Loan Balances

Private student loans are issued by banks, credit unions, or online lenders. Unlike federal loans, there is no centralized government database for private debt. This can make tracking these balances more difficult, especially if your loans have been sold to different financial institutions over the years.

Leveraging Your Credit Report

If you are unsure who holds your private student loans, the most effective strategy is to pull your credit report. Under the Fair Credit Reporting Act, you are entitled to a free credit report from each of the three major bureaus (Equifax, Experian, and TransUnion) via AnnualCreditReport.com.

Your credit report lists every open line of credit in your name. By scanning the “Account” or “Trade Line” sections, you can identify lenders you might have forgotten. The report will show the original loan amount, the current balance, and the status of the account.

Using Private Lender Portals and Mobile Apps

Once you have identified your private lenders (e.g., SoFi, Sallie Mae, Earnest), you should create accounts on their specific websites. Most modern private lenders offer robust mobile apps that provide real-time balance updates and push notifications for upcoming due dates.

Private loans often have variable interest rates, meaning your balance and monthly payment can fluctuate based on market conditions. Monitoring these balances monthly is essential for ensuring that your budget can accommodate potential rate hikes.

Contacting Lenders Directly

If a loan has been transferred or is in default, it may not appear clearly on a standard dashboard. In these cases, proactive communication is key. Calling the lender’s customer service department allows you to request a “Verification of Debt” or a “Payoff Statement.” A payoff statement is particularly useful because it calculates the exact amount required to close the account on a specific date, accounting for the “per diem” interest that accumulates daily.

3. Financial Tools for Debt Tracking and Management

Once you know how to find your balances, the next step is consolidation—not necessarily of the loans themselves, but of the information. Manually logging into five different websites every month is a recipe for oversight.

Debt Aggregation and Budgeting Software

In the realm of personal finance technology, tools like Rocket Money, YNAB (You Need A Budget), or Empower (formerly Personal Capital) are invaluable. By linking your loan accounts to these platforms via secure APIs, you can see your total net worth in one place. These tools visualize your debt-to-income ratio and track your progress over time, providing a psychological boost as you see the total balance decrease.

Creating a Customized Debt Spreadsheet

For the detail-oriented borrower, a customized spreadsheet remains the gold standard. By tracking your balances in Excel or Google Sheets, you can run “what-if” scenarios. For example, you can calculate how much faster you would reach a zero balance if you contributed an extra $100 per month toward your highest-interest loan.

A comprehensive spreadsheet should include:

- Loan name and servicer.

- Total current balance.

- Interest rate (fixed or variable).

- Minimum monthly payment.

- The “Daily Interest Formula” (Balance x Interest Rate / 365).

The Role of Net Worth Tracking

Checking your student loan balance should not be done in a vacuum. It is one half of the net worth equation (Assets – Liabilities = Net Worth). As you pay down your student loan balance, your net worth increases, even if your bank account balance stays the same. Shifting your mindset to view debt repayment as a “guaranteed return on investment” can change your emotional relationship with your student loan balance.

4. Why Frequency and Timing Matter

Checking your balance once a year is insufficient for proactive financial management. The timing of your checks can influence your payment strategy and your credit score.

The Impact of Capitalization Events

There are specific moments when checking your balance is non-negotiable. These include the end of a grace period, the end of a deferment, or when changing repayment plans. During these times, “interest capitalization” can occur, where unpaid interest is added to the principal balance. This increases the base upon which future interest is calculated. By checking your balance before these events, you can choose to pay off the accrued interest to prevent it from compounding.

Monthly Audits for Payment Accuracy

Loan servicers are not infallible. Errors in payment processing or the misapplication of overpayments (paying the wrong loan group) occur more often than one might think. By checking your balance shortly after your monthly payment clears, you can verify that the funds were applied according to your instructions—specifically toward the principal of the highest-interest loan if you are using the “Debt Avalanche” method.

Credit Score Sensitivity

Your student loan balance significantly impacts your credit utilization and your “total debt” profile. If you are planning to apply for a mortgage or an auto loan, knowing your exact student loan balance allows you to provide accurate information to underwriters. Furthermore, seeing the balance drop consistently is a sign of “successful credit history,” which bolsters your score over the long term.

5. Strategic Next Steps After Checking Your Balance

Knowledge is only power when it is applied. Once you have the figures in front of you, you must decide how to interact with that debt to improve your overall financial position.

Assessing Refinancing Opportunities

If you check your private student loan balance and notice high interest rates (e.g., 8% or higher), and your credit score has improved since you first took out the loans, you may be a candidate for refinancing. Refinancing involves taking out a new loan with a private lender at a lower interest rate to pay off the old ones. This can save you thousands of dollars over the life of the loan, though it is important to remember that refinancing federal loans into private ones means losing federal protections.

Evaluating Income-Driven Repayment (IDR)

If your federal loan balance is high relative to your income, your check-in might reveal that you are struggling to make progress. In this case, checking your balance is the first step toward applying for an IDR plan. These plans cap your payments at a percentage of your discretionary income and offer forgiveness after 20 or 25 years of qualifying payments.

Establishing a “Freedom Date”

The final benefit of knowing your exact balance and interest rate is the ability to calculate your “Freedom Date.” Using an online debt calculator, you can input your balance to see exactly when the debt will be gone. This transforms an abstract, daunting number into a concrete timeline.

Conclusion

Checking your student loan balance is more than a clerical task; it is an act of financial self-advocacy. By navigating federal portals, uncovering private debt through credit reports, and utilizing modern financial tools, you move from a state of “debt stress” to a state of “debt management.”

In the world of personal finance, what is measured is managed. When you know exactly where your student debt stands, you gain the power to make informed decisions about budgeting, investing, and career moves. Whether your balance is $5,000 or $500,000, the path to $0 begins with the simple, disciplined act of looking at the numbers.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.