Student loans can be a significant financial obligation, often spanning years or even decades after graduation. For many, they represent a complex web of interest rates, servicers, and repayment plans. However, staying informed about your student loans is not just a recommendation; it’s a fundamental necessity for sound financial health. Regularly checking your student loan details empowers you to make informed decisions, avoid costly mistakes, and navigate your path to financial freedom with confidence.

Whether you’re still in school, just starting repayment, or decades into your career, understanding the specifics of your loans is paramount. This comprehensive guide will walk you through the essential steps and platforms to access, understand, and manage your student loan information, ensuring you always have a clear picture of your financial obligations.

Understanding Your Student Loan Landscape

Before diving into where and how to check your loans, it’s crucial to understand the fundamental differences in the types of student loans available. This distinction profoundly impacts where you’ll look for information and the options available to you.

Federal vs. Private Loans: Knowing the Difference

The most critical distinction in the student loan world is between federal and private loans. Each type comes with its own set of rules, benefits, and administrative processes.

Federal Student Loans are funded by the U.S. government. They often come with more flexible repayment options, such as Income-Driven Repayment (IDR) plans, deferment, forbearance, and potential forgiveness programs. Examples include Stafford Loans (Direct Subsidized and Unsubsidized), PLUS Loans, and Perkins Loans (though new Perkins loans are no longer issued). These loans are typically serviced by specific companies contracted by the Department of Education.

Private Student Loans, on the other hand, are offered by banks, credit unions, and other private lenders. They generally have fewer borrower protections and repayment flexibilities compared to federal loans. Their terms, interest rates, and fees are set by the individual lender and depend heavily on the borrower’s creditworthiness. While they can sometimes offer lower interest rates for borrowers with excellent credit, they lack the safety nets inherent in federal programs.

Understanding which type of loan you have is the first step in knowing where to direct your search for information.

Why Regular Checking is Crucial for Financial Health

Many borrowers make the mistake of “set it and forget it” with their student loans, only engaging when a payment is due. This passive approach can lead to several pitfalls:

- Missing Important Updates: Repayment plans, servicer assignments, interest rates, and federal policy changes can all impact your loans. Regular checking ensures you’re aware of these shifts.

- Preventing Default: Unforeseen financial hardships can make payments challenging. Knowing your options, like deferment or forbearance, before missing payments can protect your credit score and prevent default.

- Catching Errors: Mistakes happen. An incorrect interest rate, misapplied payment, or inaccurate balance can cost you money over time. Vigilance allows you to spot and rectify these errors promptly.

- Optimizing Repayment Strategies: As your financial situation changes, your ideal repayment strategy might evolve. Staying informed about your balances and interest accrual allows you to explore options like refinancing, consolidation, or making extra payments strategically.

- Tax Benefits: Understanding your interest paid throughout the year is vital for claiming potential tax deductions.

In essence, checking your student loans regularly is an act of financial self-care, providing clarity and control over a significant part of your financial future.

Key Platforms for Accessing Your Loan Information

Once you understand the type of loans you possess, you can efficiently navigate the platforms designed to provide you with your loan details.

For Federal Student Loans: The Official Gateways

The U.S. Department of Education provides centralized resources for managing federal student loans.

StudentAid.gov: Your Primary Federal Loan Hub

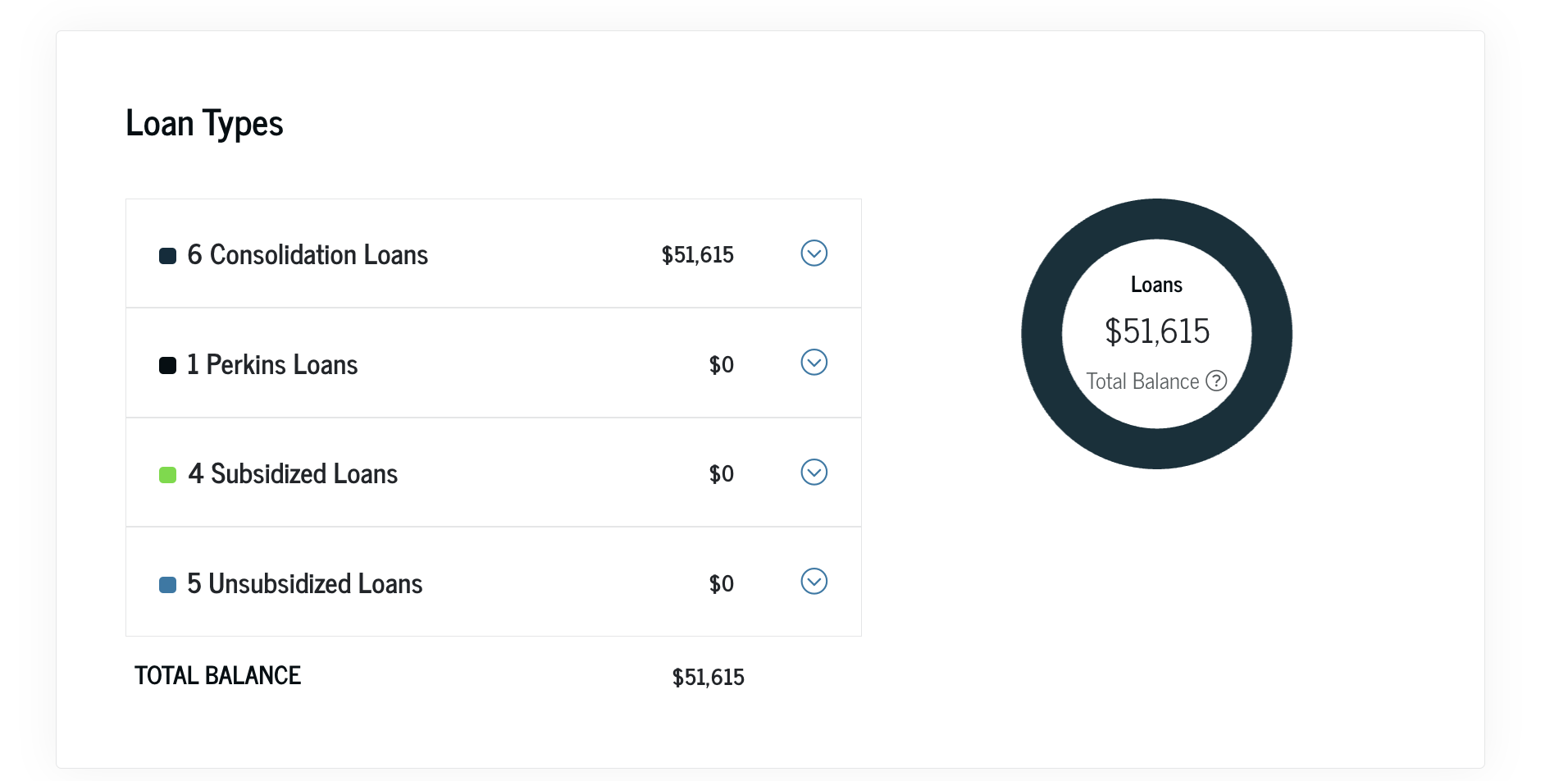

For virtually all federal student loans, StudentAid.gov is your starting point. This comprehensive portal allows you to:

- View All Your Federal Loans: It consolidates information on all federal loans you’ve ever taken out, regardless of when or where you received them.

- Identify Your Loan Servicer(s): This is crucial. While StudentAid.gov lists your loans, your day-to-day management and payments are handled by a loan servicer. The site will tell you which servicer is assigned to each of your loans.

- Check Loan Balances: Get an up-to-date overview of your principal balances.

- Review Interest Rates: See the interest rate for each individual federal loan.

- Access Payment History: Track your past payments and their application.

- Explore Repayment Plans: Evaluate different income-driven repayment plans and use calculators to estimate payments.

- Apply for Deferment or Forbearance: If eligible, you can initiate these processes through the site.

To access your information, you’ll need to log in using your FSA ID (Federal Student Aid ID), which is the same ID you used to fill out the FAFSA. If you’ve forgotten it, you can retrieve it on the site.

Your Loan Servicer’s Website: For Detailed Management

Once you’ve identified your loan servicer(s) through StudentAid.gov, you’ll then go directly to their website for more granular details and to actively manage your loans. Common federal loan servicers include:

- Nelnet

- MOHELA

- Aidvantage (formerly Navient and other servicers)

- Edfinancial Services

- Great Lakes (now often serviced by Nelnet)

Each servicer has its own online portal where you can:

- Make payments, set up auto-pay, or change payment methods.

- Access your monthly statements.

- View your specific loan terms, current interest accrued, and payment due dates.

- Update contact information.

- Communicate directly with a customer service representative.

It’s highly recommended to create an account with each of your loan servicers and regularly check these portals.

For Private Student Loans: Directly with Your Lender

Private student loans are not part of the federal system, meaning StudentAid.gov will not have information about them.

Your Original Lender’s Website

To check your private student loans, you must go directly to the website of the bank or financial institution that issued the loan. Common private lenders include:

- Sallie Mae

- Discover

- Wells Fargo

- Citizens Bank

- PNC Bank

- Many local credit unions

If you remember the lender, simply navigate to their website and log into your account. There, you’ll find your current balance, interest rate, payment schedule, and historical data.

Leveraging Your Credit Report

If you’re unsure who your private loan lender is, your credit report is an excellent resource. Both federal and private student loans appear on your credit report. You are entitled to a free copy of your credit report from each of the three major credit bureaus (Equifax, Experian, TransUnion) once every 12 months via AnnualCreditReport.com.

Reviewing your credit report will list all creditors, including student loan lenders, along with account numbers and balances. This can help you identify forgotten private loans and then direct you to the correct lender’s website.

Deciphering Your Loan Statements and Details

Once you’ve accessed your loan information, understanding the terminology and key metrics is essential to truly grasping your financial situation. Don’t just glance at the balance; dig deeper.

Understanding Key Terms and Data Points

Familiarize yourself with the following common terms you’ll encounter on your loan statements or online portals:

- Principal Balance: The original amount of money you borrowed, minus any payments that have been applied directly to the principal.

- Interest Rate: The percentage charged on the principal balance. This can be fixed (stays the same throughout the loan life) or variable (can change over time).

- Accrued Interest: The interest that has accumulated since your last payment or the last time interest was capitalized. If not paid, accrued interest can be added to your principal balance (capitalized), increasing the total amount you owe.

- Loan Servicer: The company that manages your loan, processes payments, and handles administrative tasks.

- Payment Due Date: The date your monthly payment is expected.

- Repayment Plan: The specific schedule for how you’re paying back your loan. For federal loans, options range from Standard (10 years) to various Income-Driven Repayment (IDR) plans (e.g., SAVE, PAYE, IBR, ICR), Graduated, and Extended plans.

- Grace Period: A period after you graduate, leave school, or drop below half-time enrollment when you don’t have to make payments. Federal loans typically have a six-month grace period.

- Deferment/Forbearance: Temporary periods during which you can postpone loan payments. Interest may or may not accrue during these periods, depending on the loan type and program.

Reviewing Your Payment History and Identifying Potential Errors

Beyond just knowing your current balance, scrutinizing your payment history provides valuable insights.

- Verify Payment Application: Ensure your payments are being applied correctly and on time. Check that the amount you paid matches what was recorded and that it was applied to the correct loan.

- Track Interest Capitalization: Be aware of when and if accrued interest is being added to your principal balance. This can happen after periods of deferment or forbearance, or if you switch repayment plans, and it increases your total debt.

- Spot Discrepancies: Look for any unexpected charges, unrecorded payments, or incorrect interest calculations. If you find an error, contact your servicer immediately with documentation (bank statements, payment confirmations). Prompt action can prevent minor issues from becoming major problems.

Strategies for Effective Loan Management and Repayment

Regularly checking your student loans is just the first step; the ultimate goal is to manage them effectively towards repayment.

Consolidating Your Information for a Holistic View

With multiple loans, possibly from different servicers or lenders, it can be challenging to keep everything straight.

- Spreadsheets: Create a simple spreadsheet to list each loan, its type (federal/private), servicer/lender, current balance, interest rate, and minimum monthly payment. Update it quarterly.

- Financial Aggregation Apps: Many personal finance apps (e.g., Mint, Empower (formerly Personal Capital), YNAB) allow you to link all your financial accounts, including student loans, providing a consolidated dashboard. While useful for an overview, always verify details on the official servicer sites.

Having all your loan data in one place makes it easier to track progress, plan payments, and strategize for accelerated repayment.

Exploring Repayment Options and Optimizing Your Plan

Your current repayment plan might not be the most advantageous for your current financial situation.

- Income-Driven Repayment (IDR) for Federal Loans: If you have federal loans and your income is modest compared to your debt, IDR plans can significantly lower your monthly payments. Plans like SAVE (Saving on a Valuable Education) cap payments at a percentage of your discretionary income and offer potential for interest subsidies and forgiveness after a certain period. Regularly check if you qualify for a more favorable IDR plan or if your income changes warrant an adjustment.

- Refinancing Private Loans (or Federal to Private): If you have private loans and your credit score has improved since you first took them out, you might be eligible to refinance for a lower interest rate, potentially saving thousands over the life of the loan. Some borrowers also refinance federal loans into private loans to secure a lower interest rate, but this means forfeiting federal protections (IDR, forgiveness, etc.), so it requires careful consideration.

- Accelerated Repayment Strategies: If your goal is to pay off loans faster, knowing your individual loan details (especially interest rates) allows you to implement strategies like the “debt avalanche” (paying off highest interest loans first) or “debt snowball” (paying off smallest balance loans first). Making extra payments, even small ones, can significantly reduce the total interest paid and shorten your repayment term.

Setting Up Alerts and Reminders

To ensure you never miss a payment or an important update:

- Enroll in Auto-Pay: Most servicers offer an interest rate reduction (typically 0.25%) for enrolling in automatic payments. This also ensures on-time payments.

- Set Calendar Reminders: Create recurring reminders for payment due dates, annual IDR recertification, and periodic loan reviews.

- Sign Up for Servicer Alerts: Opt-in for email or text alerts from your servicer for upcoming payments, statement availability, and critical account changes.

What to Do If You Can’t Find Your Loan Information

Sometimes, despite your best efforts, finding all your loan details can be a challenge, especially for older loans or if you’ve had multiple servicers over the years. Don’t panic; there are still avenues to explore.

Reviewing Your Credit Reports Annually

As mentioned previously, your credit report is a goldmine of information. It lists all your active and sometimes even paid-off accounts, including both federal and private student loans. Visit AnnualCreditReport.com to get your free reports from Equifax, Experian, and TransUnion. Examine them carefully for any student loans you don’t recognize or that are missing from your current records. Your credit report will provide the name of the lender or servicer, which you can then contact directly.

Contacting Your Previous Schools’ Financial Aid Offices

If you attended multiple institutions, or if your loans are very old, your former school’s financial aid office might still have records of the loans you took out while enrolled there. They can often provide you with the original lender or servicer information, particularly for federal loans or campus-based loans like Perkins.

Reaching Out to the Department of Education

If you are certain you had federal student loans but cannot access your StudentAid.gov account or find your information, you can contact the Federal Student Aid Information Center (FSAIC) at 1-800-4-FEDAID (1-800-433-3243). They can assist with FSA ID issues, explain your loan history, and help you locate your servicer.

Seeking Professional Financial Advice

If your student loan situation is particularly complex—perhaps involving old defaulted loans, complicated repayment history, or significant balances across various types of loans—consider consulting a non-profit credit counselor or a financial advisor specializing in student loan debt. They can help you untangle your loan landscape, understand your options, and develop a personalized repayment strategy. Ensure any advisor you choose is reputable and transparent about their fees.

Conclusion

Taking the initiative to regularly check and understand your student loans is one of the most proactive steps you can take for your financial well-being. It transforms a potentially daunting obligation into a manageable part of your financial plan. By utilizing the official government platforms for federal loans, directly engaging with private lenders, and diligently reviewing your statements, you gain the clarity needed to make informed decisions. This continuous engagement empowers you to navigate repayment options, identify cost-saving opportunities, and ultimately accelerate your journey toward becoming debt-free. Don’t let uncertainty be a burden; take control by knowing exactly where you stand with your student loans.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.