Cancelling a credit card, particularly one like Credit One, is a financial decision that warrants careful consideration. While it might seem like a straightforward task, the implications can ripple across your personal finance landscape, affecting everything from your credit score to your ongoing financial planning. This comprehensive guide will walk you through the strategic thinking, preparation, process, and post-cancellation vigilance required to ensure a smooth and financially sound outcome.

The Strategic Decision: Why Cancel a Credit Card?

Before you pick up the phone to Credit One, it’s crucial to understand why you’re making this decision and what its potential ramifications are. Cancelling a credit card is not merely an administrative task; it’s a strategic move in your personal finance journey.

Assessing Your Financial Landscape

Your current financial situation should be the primary driver behind any decision to cancel a credit card. Are you struggling with debt and looking to simplify your financial life? Are you trying to improve your credit score by reducing your overall credit utilization, or perhaps you’ve matured financially and found better credit products? Understanding your broader financial goals—whether it’s saving for a down payment, paying off existing debt, or optimizing your credit portfolio—will provide the necessary context. For example, if you have multiple cards and are trying to streamline, Credit One, often a starter card for those building credit, might be an obvious choice to let go if you’ve qualified for more favorable terms elsewhere. Conversely, if it’s one of your oldest accounts, cancelling it could have an unexpected negative impact.

Common Reasons for Credit Card Cancellation

People decide to cancel credit cards for a variety of valid financial reasons. High annual fees that outweigh the benefits are a frequent motivator; Credit One cards often carry annual fees, sometimes without robust rewards programs to justify them. Poor rewards programs or a lack of benefits can also make a card less appealing compared to newer options. Debt consolidation efforts might lead you to close accounts to prevent further spending. Perhaps you’ve simply upgraded to a better card with lower interest rates, superior rewards, or more comprehensive benefits, rendering your Credit One card redundant. Alternatively, for those struggling with impulse spending, closing an accessible line of credit can be a disciplined move towards financial responsibility. Each of these reasons stems from a careful evaluation of the card’s financial utility in your portfolio.

The Impact on Your Credit Score

This is perhaps the most critical financial aspect to consider. Your credit score is influenced by several factors, and cancelling a card can affect a few of them:

- Credit Utilization Ratio: This is the amount of credit you’re using compared to your total available credit. If you cancel a card, your total available credit decreases. If your balances on other cards remain the same, your utilization ratio will go up, which can negatively impact your score. It’s generally recommended to keep this ratio below 30%.

- Average Age of Accounts: Lenders like to see a long history of responsible credit use. If your Credit One card is one of your oldest accounts, closing it could reduce the average age of your credit accounts, potentially lowering your score. FICO models typically keep closed accounts on your report for up to 10 years, but their age impact can diminish over time.

- Types of Credit: Having a mix of credit (revolving accounts like credit cards and installment loans like mortgages or car loans) is beneficial. Closing a credit card primarily impacts your revolving credit.

Understanding these dynamics allows you to strategically time your cancellation and take proactive steps, such as paying down other balances, to mitigate any negative impact.

Preparing for Cancellation: Essential Pre-Steps

Once you’ve decided to cancel your Credit One credit card, a few preparatory steps are essential to avoid financial headaches and ensure a smooth exit. These steps safeguard your credit, prevent forgotten expenses, and streamline the cancellation process itself.

Zeroing Out Your Balance

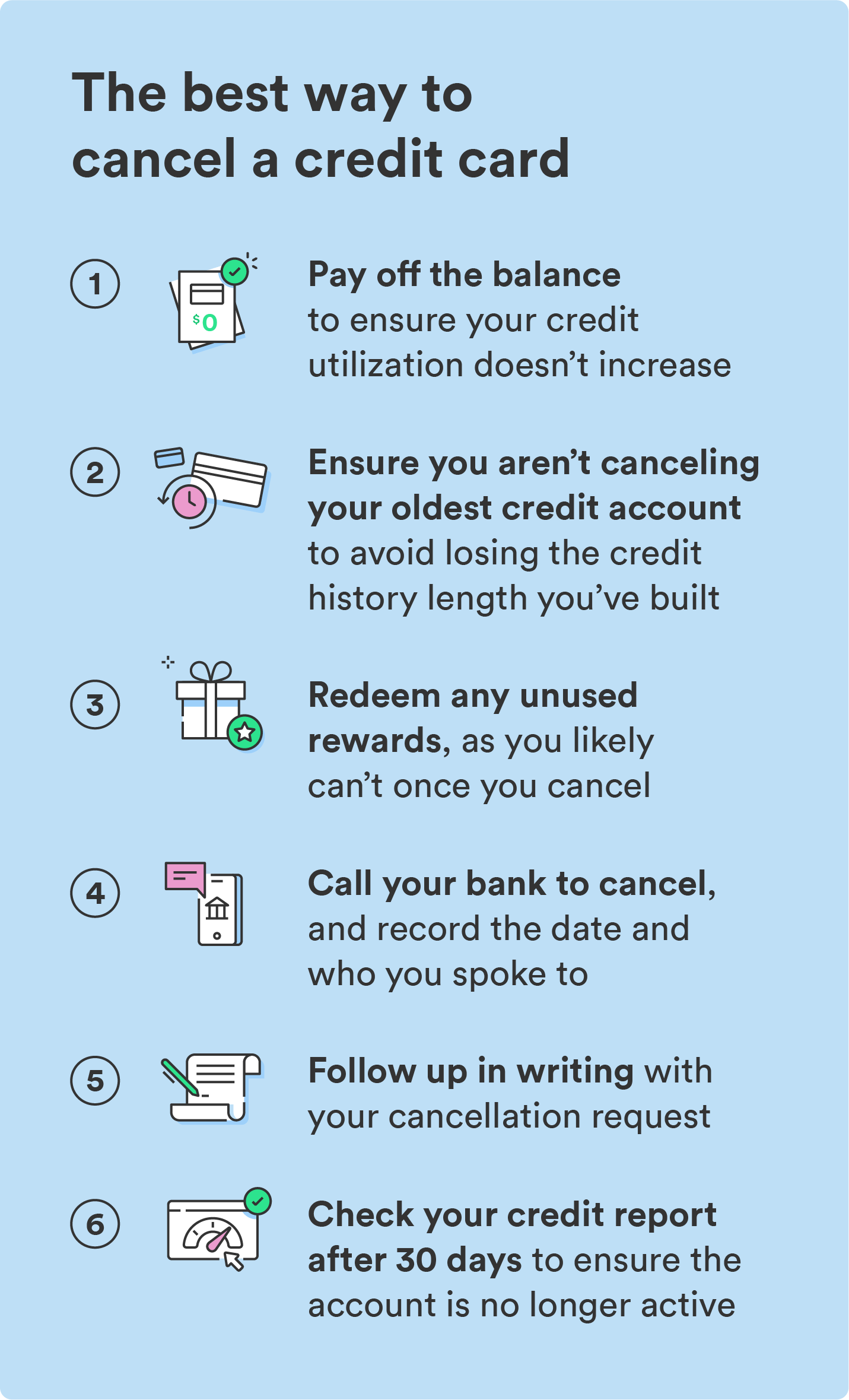

This is non-negotiable. You cannot cancel a credit card with an outstanding balance. Before initiating the cancellation process, ensure your Credit One account has a zero balance. Pay off every cent, including any accrued interest or pending fees. If you have a small remaining balance, paying it off quickly can prevent further interest charges. Waiting for the payment to clear and confirm a zero balance on your online statement or by calling customer service is crucial before proceeding to the next steps. Attempting to cancel with a balance will only prolong the process and potentially lead to continued interest and fees.

Redeeming Rewards and Benefits

Credit One often offers cash back rewards or other benefits, though they might be less robust than those found with prime credit cards. Before closing your account, check if you have any unredeemed rewards, points, or cash back. Once the account is closed, any remaining rewards will likely be forfeited. Log in to your online account or call customer service to inquire about your rewards balance and the process for redeeming them. This small step can recover value that you’ve already earned, ensuring you don’t leave money on the table.

Updating Automatic Payments and Subscriptions

In today’s digital world, many of us link our credit cards to recurring payments for subscriptions (Netflix, Spotify), utilities, gym memberships, or even insurance premiums. Before cancelling your Credit One card, make a comprehensive list of all services that automatically charge this card. You’ll need to update these payment methods with a different credit card or bank account. Failing to do so can lead to missed payments, service interruptions, late fees, and potential damage to your credit score if those missed payments are reported to credit bureaus. This proactive step prevents unnecessary hassle and ensures your essential services continue uninterrupted.

Gathering Necessary Information

When you contact Credit One, you’ll need to verify your identity and account details. Have your account number, personal identification information (like your Social Security number), and any security questions readily available. If you have a recent statement, it can also be helpful. Being prepared with this information will make the conversation with customer service more efficient and prevent delays. Knowing your last payment date and amount can also be useful for confirming the zero balance.

The Step-by-Step Process to Cancel Your Credit One Card

With your preparations complete, it’s time to formally initiate the cancellation of your Credit One credit card. This process typically involves direct communication with the bank and careful documentation.

Contacting Credit One Bank

The most effective way to cancel a credit card is usually by phone. While some banks allow online cancellation, Credit One, like many issuers, prefers a verbal confirmation. Call the customer service number located on the back of your card or on your monthly statement. Be prepared for retention efforts; the representative may try to convince you to stay by offering incentives like lower interest rates, waived fees, or balance transfer options. Politely but firmly reiterate your intention to close the account. While less common, you can also send a certified letter requesting cancellation, but this is a slower process and harder to confirm immediately. Using a phone call allows for real-time interaction and immediate confirmation of account status.

What to Say and Ask

When you speak to the representative, clearly state, “I would like to close my credit card account, [your account number], immediately.”

Here are key questions to ask:

- “Please confirm that my balance is zero.”

- “Will there be any remaining fees after cancellation?” (e.g., prorated annual fee, outstanding interest)

- “Can you provide a confirmation number for this cancellation?”

- “Will you send me a written confirmation of the account closure?” (A closure letter or email is ideal for your records.)

- “How long will it take for the account to reflect as closed on my credit report?”

Be polite but firm. Do not be swayed by offers if your decision is final and well-considered. The goal is a clear, unequivocal closure of the account.

Documenting the Cancellation

Documentation is crucial for your financial records and for resolving any potential disputes later. During your phone call, note down:

- The date and time of the call.

- The name of the customer service representative you spoke with.

- The confirmation number provided for the cancellation.

- Any specific instructions or details shared by the representative.

- Request that Credit One send you a formal letter or email confirming the account closure. Keep this document with your important financial papers. This provides irrefutable proof that you requested the closure and when.

This meticulous record-keeping acts as your safety net against any future billing errors or discrepancies related to the closed account.

Physically Destroying the Card

Once the account is confirmed closed and you have your documentation, the physical card becomes a security risk and an unnecessary piece of plastic. Cut up the card, ensuring you cut through the magnetic stripe, chip, and account number. Dispose of the pieces in separate bins if possible, to prevent anyone from reconstructing the card details. This small but important step protects you from identity theft or unauthorized use of the defunct card. It’s the final, tangible act in the cancellation process, symbolizing the end of that financial relationship.

Post-Cancellation Vigilance: Protecting Your Financial Health

The cancellation process doesn’t end when you hang up the phone. Vigilance in the months that follow is paramount to ensure the account is properly closed, your credit score is unaffected (or affected as expected), and your overall financial health remains intact.

Monitoring Your Credit Report

For at least the next 3-6 months, closely monitor your credit reports from all three major bureaus (Equifax, Experian, and TransUnion). You can obtain free copies annually at AnnualCreditReport.com. Look for the following:

- Account Status: Ensure the Credit One account is listed as “closed by grantor” or “closed by consumer” with a zero balance. If it still shows as open or has an outstanding balance, contact Credit One immediately with your documentation.

- Unexpected Charges: Although rare for a closed account, meticulously check for any new activity or charges.

- Credit Score Impact: Observe how your credit score reacts. While a temporary dip is possible due to changes in credit utilization or average age of accounts, it should stabilize over time if you manage your other credit responsibly. Any drastic or prolonged negative changes not attributable to other factors warrant investigation.

This proactive monitoring helps catch and rectify any errors quickly, preventing potential long-term damage to your credit profile.

Confirming Account Closure

Beyond checking your credit report, you should also confirm closure through your statements. Credit One might send one final statement after closure, showing a zero balance and indicating the account is closed. If you requested a formal closure letter, ensure you receive it and keep it for your records. If you don’t receive confirmation within a reasonable timeframe (2-4 weeks), follow up with Credit One using your documented details from the cancellation call. Timely confirmation brings peace of mind and verifies that the process was completed correctly by the bank.

Managing Your Credit Utilization Ratio

As discussed, cancelling a card reduces your total available credit, which can increase your credit utilization ratio if you carry balances on other cards. To mitigate this, consider paying down balances on your remaining credit cards to keep your utilization ratio low (ideally below 30%). This is a crucial aspect of responsible personal finance. If you have a zero balance across all your cards, the impact will be minimal. However, if you often use a significant portion of your available credit, strategizing how you manage your other accounts becomes even more important after a cancellation.

Future Financial Planning

Cancelling a Credit One card could be a stepping stone to a healthier financial future. Use this opportunity to re-evaluate your overall financial plan.

- Alternative Cards: If you cancelled due to high fees or poor rewards, research and consider applying for a new card that better fits your needs (e.g., a card with better rewards, lower APR, or no annual fee) once your credit score has stabilized.

- Budgeting Strategies: Reassess your budgeting. If you cancelled the card to reduce spending, reinforce those habits with a robust budget.

- Emergency Fund: Ensure you have a strong emergency fund so you’re not solely reliant on credit cards for unexpected expenses.

- Debt Management: If the cancellation was part of a larger debt management strategy, stick to your plan for paying down other debts.

Ultimately, cancelling your Credit One credit card, when executed thoughtfully and strategically, can be a positive step toward better financial health and a more optimized credit portfolio. It’s a decision rooted in sound personal finance principles, demanding preparation, precise execution, and ongoing vigilance to secure your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.