For millions of retirees and beneficiaries, Social Security represents a vital component of their financial well-being. However, a common misconception is that these benefits are entirely tax-free. In reality, a portion of Social Security benefits can be subject to federal income tax, and in some cases, state income tax, depending on your total income and filing status. Understanding how to calculate this taxable amount is crucial for effective retirement planning and avoiding unexpected tax liabilities. This guide will demystify the process, providing a clear, step-by-step approach to determining if and how much of your Social Security income Uncle Sam claims.

Understanding the Basics of Social Security Taxation

The taxation of Social Security benefits was introduced in 1983 and expanded in 1993, primarily affecting higher-income beneficiaries. The intent was to ensure the long-term solvency of the Social Security system by having those with greater financial capacity contribute more. It’s not a simple flat tax; rather, it’s a tiered system based on what the Internal Revenue Service (IRS) refers to as “provisional income.”

Who Pays Taxes on Benefits? The Provisional Income Threshold

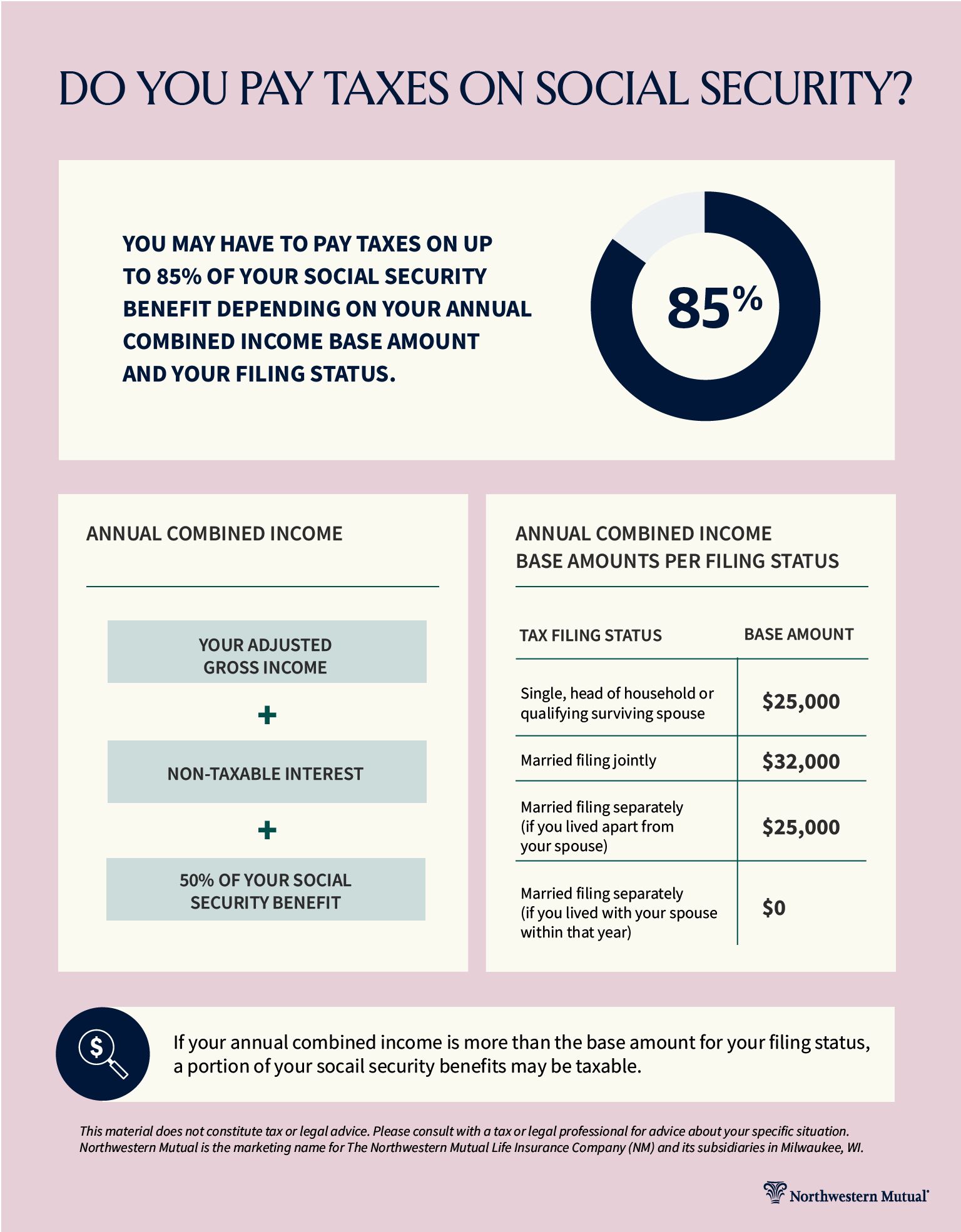

The key determinant for whether your Social Security benefits are taxable is your “provisional income.” This isn’t your Adjusted Gross Income (AGI) in the traditional sense, but a specific calculation used only for Social Security taxation. Provisional income is calculated as the sum of:

- Your adjusted gross income (AGI) from all other sources (excluding Social Security benefits).

- Any tax-exempt interest (e.g., from municipal bonds).

- One-half (50%) of your annual Social Security benefits.

It’s important to note that all Social Security benefits received, including those for spouses or children based on your record, are included in this calculation. Once you have this provisional income figure, you compare it against specific thresholds to determine the taxable portion.

The Two-Tiered Taxation System (50% or 85%)

The taxation of Social Security benefits operates on a progressive, two-tiered system based on your provisional income thresholds and filing status:

- First Tier (Up to 50% Taxable): If your provisional income falls between a lower and upper threshold, up to 50% of your Social Security benefits may be subject to federal income tax.

- Second Tier (Up to 85% Taxable): If your provisional income exceeds the upper threshold, up to 85% of your Social Security benefits may be subject to federal income tax.

These thresholds vary based on your tax filing status:

- Single, Head of Household, or Qualifying Widow(er):

- Provisional income between $25,000 and $34,000: Up to 50% of benefits are taxable.

- Provisional income above $34,000: Up to 85% of benefits are taxable.

- Married Filing Jointly:

- Provisional income between $32,000 and $44,000: Up to 50% of benefits are taxable.

- Provisional income above $44,000: Up to 85% of benefits are taxable.

- Married Filing Separately (and lived with your spouse at any time during the year):

- If you lived with your spouse at any point during the tax year and file separately, your Social Security benefits are generally 85% taxable, regardless of income. This is a punitive rule designed to prevent couples from artificially lowering their provisional income by filing separately.

- Married Filing Separately (and did NOT live with your spouse at any time during the year):

- Use the “Single” thresholds for calculating taxation.

Why Social Security Benefits Are Taxed

The taxation of Social Security benefits serves multiple purposes. Primarily, it’s a mechanism to help fund the Social Security trust funds. When the system was established, life expectancies were lower, and the ratio of workers to beneficiaries was much higher. As demographics have shifted, and people live longer, the financial strain on the system has increased. Taxing benefits from those with higher incomes helps to maintain the program’s solvency, ensuring it can continue to pay benefits to future generations. Furthermore, it aligns with a progressive tax system, where individuals with greater financial resources contribute proportionally more.

Step-by-Step Guide to Calculating Taxable Benefits

Calculating the exact taxable portion of your Social Security benefits can seem daunting, but by breaking it down into manageable steps, it becomes much clearer.

Step 1: Determine Your Provisional Income

As discussed, provisional income is the linchpin of this calculation. Gather all your income statements for the tax year:

- Line 1: Your Adjusted Gross Income (AGI) from sources other than Social Security. This includes wages, pensions, annuities, taxable interest, dividends, capital gains, required minimum distributions (RMDs) from traditional IRAs, etc.

- Line 2: Add any tax-exempt interest income (e.g., from municipal bonds).

- Line 3: Add 50% of your total Social Security benefits received for the year. (You’ll receive Form SSA-1099, which shows your total benefits in Box 5).

Provisional Income = (AGI excluding Social Security) + (Tax-exempt Interest) + (50% of Social Security Benefits)

Step 2: Compare Provisional Income to Thresholds

Once you have your provisional income, compare it against the thresholds for your specific filing status.

- Single, Head of Household, or Qualifying Widow(er): $25,000 and $34,000.

- Married Filing Jointly: $32,000 and $44,000.

- Married Filing Separately (and lived with spouse): Usually 85% taxable.

- Married Filing Separately (did not live with spouse): Use single thresholds.

Step 3: Calculate Taxable Portion (50% Rule)

If your provisional income is between the lower and upper thresholds:

- The taxable amount is the lesser of:

- 50% of your Social Security benefits.

- 50% of the amount by which your provisional income exceeds the lower threshold.

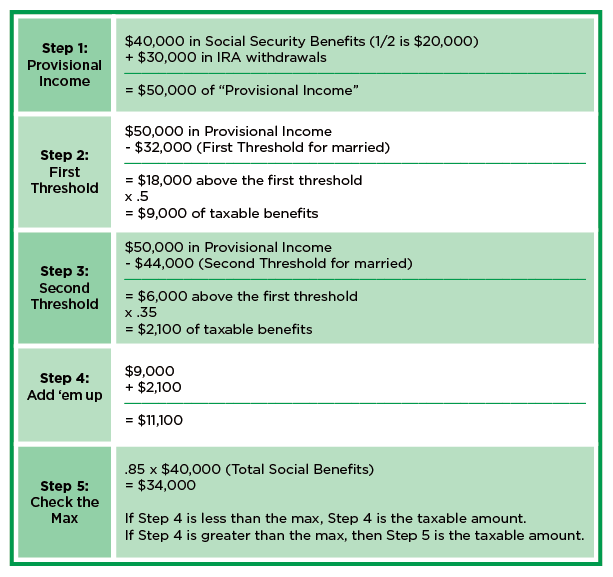

Example (Single): If provisional income is $30,000 and Social Security benefits are $12,000.

- 50% of Social Security benefits = 0.50 * $12,000 = $6,000.

- 50% of (Provisional Income – Lower Threshold) = 0.50 * ($30,000 – $25,000) = 0.50 * $5,000 = $2,500.

In this case, $2,500 is the lesser amount, so $2,500 of the Social Security benefits would be taxable.

Step 4: Calculate Taxable Portion (85% Rule)

If your provisional income is above the upper threshold:

- The taxable amount is the lesser of:

- 85% of your Social Security benefits.

- The sum of:

- The maximum amount taxable under the 50% rule for your filing status, PLUS

- 85% of the amount by which your provisional income exceeds the upper threshold.

Example (Single): If provisional income is $40,000 and Social Security benefits are $12,000.

First, calculate the maximum amount taxable under the 50% rule:

- 50% of the first $9,000 above the lower threshold ($34,000 – $25,000 = $9,000) is $4,500. (This is the maximum under the 50% rule for single filers: 50% of the maximum $9,000 range, or 50% of max benefits, whichever is less)

Now, calculate for the 85% rule:

- 85% of Social Security benefits = 0.85 * $12,000 = $10,200.

- (Maximum from 50% tier) + 85% of (Provisional Income – Upper Threshold)

= $4,500 + 0.85 * ($40,000 – $34,000)

= $4,500 + 0.85 * $6,000

= $4,500 + $5,100 = $9,600.

In this case, $9,600 is the lesser amount, so $9,600 of the Social Security benefits would be taxable.

This calculation can be complex, and often tax software or a tax professional will handle these intricacies. The IRS provides detailed worksheets in Publication 915.

Factors Influencing Social Security Taxation

Beyond provisional income and filing status, several other elements can play a significant role in how much of your Social Security benefits are subject to tax.

Other Sources of Income

The most significant factor influencing Social Security taxation is the presence and amount of other income. This includes traditional pension payments, distributions from 401(k)s and traditional IRAs (including required minimum distributions), wages from part-time work, taxable interest, and dividends. The more income you have from these sources, the higher your provisional income will be, and the greater the likelihood that a larger portion (up to 85%) of your Social Security benefits will become taxable. This highlights the importance of strategically managing all income streams in retirement.

Filing Status Matters

As demonstrated in the calculation steps, your tax filing status — Single, Married Filing Jointly, Head of Household, Qualifying Widow(er), or Married Filing Separately — directly impacts the provisional income thresholds. Married couples filing jointly have higher thresholds than single filers. Crucially, married couples filing separately and living together are often penalized, with 85% of their benefits automatically becoming taxable regardless of income levels, unless specific conditions are met (e.g., legally separated with a court decree). Choosing the correct filing status is a foundational element of tax planning for retirees.

State Income Taxes on Social Security

While federal taxation of Social Security benefits is widespread, it’s also essential to consider state income taxes. The good news is that most states do not tax Social Security benefits. However, a handful of states do, and their rules vary. As of recent updates, states like Colorado, Connecticut, Kansas, Minnesota, Missouri, Montana, Nebraska, New Mexico, Rhode Island, Utah, Vermont, and West Virginia may tax a portion of Social Security benefits, often with their own income thresholds and exemptions. It’s vital to check your specific state’s tax laws to get a complete picture of your total tax liability on these benefits. Moving to a state that doesn’t tax Social Security benefits is a common strategy for some retirees.

Strategies to Potentially Reduce Your Social Security Tax Burden

While you can’t eliminate the provisional income calculation, several financial planning strategies can help manage and potentially reduce the taxable portion of your Social Security benefits.

Tax-Advantaged Retirement Accounts (Roth vs. Traditional)

The type of retirement accounts you draw from in retirement can significantly impact your provisional income.

- Traditional IRAs/401(k)s: Distributions from these accounts are generally taxed as ordinary income and directly increase your AGI, thereby increasing your provisional income and potentially making more of your Social Security benefits taxable.

- Roth IRAs/401(k)s: Qualified distributions from Roth accounts are tax-free. This means they do not contribute to your AGI or provisional income, making them an excellent tool for managing the taxation of Social Security benefits. By strategically drawing from Roth accounts, you can keep your AGI lower, potentially preventing your provisional income from crossing the thresholds where Social Security benefits become taxable at 50% or 85%.

Qualified Charitable Distributions (QCDs)

For those aged 70 ½ or older who are charitably inclined, a Qualified Charitable Distribution (QCD) can be a powerful tax-planning tool. A QCD allows you to donate money directly from your IRA to an eligible charity. The amount donated counts towards your Required Minimum Distribution (RMD) but is not included in your AGI. By reducing your AGI, QCDs can effectively lower your provisional income, which in turn can reduce the taxable portion of your Social Security benefits.

Tax-Loss Harvesting and Income Management

Tax-loss harvesting involves selling investments at a loss to offset capital gains and, potentially, a limited amount of ordinary income. By strategically managing capital gains and losses, you can reduce your taxable income, which flows through to a lower AGI and, consequently, a lower provisional income. Similarly, being mindful of when you take distributions from taxable accounts or realizing other income can help you stay below the critical provisional income thresholds. This might involve spreading out large income events over several years if possible.

Deferring Social Security Benefits

While not directly a method to reduce tax on benefits once received, deferring when you start taking Social Security benefits can indirectly impact your overall tax picture. Delaying benefits beyond your Full Retirement Age (FRA) can lead to higher monthly payments. If your other retirement income sources are sufficient in your early retirement years, you might delay taking Social Security until your provisional income is lower (e.g., after RMDs start later in life or if you reduce other income). This strategy might not always reduce the percentage of benefits taxed but could allow you to receive higher benefits overall, which, even if partially taxed, provides greater net income.

Essential Tools and Resources for Tax Planning

Navigating the complexities of Social Security taxation requires accurate information and, often, professional guidance.

IRS Publication 915

The definitive guide for understanding Social Security and equivalent railroad retirement benefits taxation is IRS Publication 915, “Social Security and Equivalent Railroad Retirement Benefits.” This publication provides detailed explanations, worksheets, and examples that mirror the calculations tax professionals use. It’s updated annually and is an invaluable resource for anyone seeking a comprehensive understanding or attempting to calculate their taxable benefits manually. The worksheets found within it are the official method used by the IRS.

Tax Software and Professional Advice

For most individuals, using reputable tax preparation software (e.g., TurboTax, H&R Block) is the most straightforward way to calculate taxable Social Security benefits. These programs integrate the IRS rules and automatically perform the provisional income calculation, ensuring accuracy based on your entered income data. However, for those with complex financial situations, multiple income streams, or significant assets, consulting a qualified tax professional (e.g., a Certified Public Accountant – CPA, or an Enrolled Agent – EA) is highly recommended. A professional can offer personalized advice, identify additional deductions or strategies, and ensure compliance with all tax laws.

The Importance of Proactive Planning

Understanding how your Social Security benefits are taxed isn’t just about filing your annual return; it’s a critical component of holistic retirement planning. By projecting your income sources and provisional income levels in advance, you can make informed decisions about when to take Social Security benefits, how to structure your retirement account withdrawals, and implement tax-efficient strategies. Proactive planning allows you to optimize your net retirement income, minimize unexpected tax burdens, and secure a more financially stable future. Engaging with a financial advisor who understands tax implications can provide significant value in this long-term planning process.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.