Understanding how Social Security credits work is not merely an administrative task; it’s a fundamental pillar of personal financial planning. For millions of Americans, Social Security benefits form a crucial part of their retirement income, disability protection, and survivor support for their families. However, eligibility for these vital benefits hinges entirely on earning enough Social Security credits throughout one’s working life. Demystifying this system is the first step toward securing your financial future and ensuring you and your loved ones are protected.

This guide will delve into the mechanics of Social Security credits, explaining what they are, how they are earned, why they are so important, and how you can track your progress. By the end, you’ll have a clear understanding of this essential component of America’s social safety net and be better equipped to plan for a secure financial tomorrow.

Understanding Social Security Credits: The Foundation of Your Future Benefits

Social Security credits, sometimes referred to as “quarters of coverage,” are the building blocks that determine your eligibility for Social Security benefits. Think of them as points you accumulate through your work history, much like earning stars for loyalty programs. The more you work and earn, the more credits you gain, up to a maximum each year.

What Exactly Are Social Security Credits?

The Social Security Administration (SSA) assigns credits based on your annual earnings. In simple terms, for every specific amount of money you earn from wages or self-employment income that is subject to Social Security taxes, you earn one credit. This system ensures that those who contribute to the system through their payroll taxes are the ones who ultimately benefit from it. The specific earnings amount required to earn a credit typically increases each year to keep pace with average wage growth. This adjustment is crucial for maintaining the relevance and fairness of the system over time.

These credits are not just for retirement. They are the universal metric used by the SSA to determine eligibility across the spectrum of benefits offered, including disability and survivor benefits. Without sufficient credits, you cannot claim any of these protections, regardless of how many years you’ve worked or paid taxes.

Why Credits Are Essential for Eligibility

The primary reason Social Security credits are essential is that they serve as the gateway to all Social Security benefits. Without meeting specific credit thresholds, you simply cannot receive payments. This system is designed to ensure that benefits are paid to individuals who have demonstrated a sustained commitment to the workforce and, by extension, to contributing to the Social Security trust funds.

For retirement benefits, the most common type, a specific number of credits is required to be “fully insured.” This full insurance status is your ticket to receiving benefits once you reach retirement age. Similarly, to qualify for disability benefits, you need to be “disability insured,” which requires a different, often more recent, credit threshold depending on your age at the onset of disability. And in the unfortunate event of your passing, your loved ones can receive “survivor benefits” if you were adequately insured through your work credits. The credit system is the backbone of the entire program, ensuring fairness and sustainability.

The Mechanics of Earning Credits: Annual Thresholds and Limits

Earning Social Security credits is a straightforward process tied directly to your income. However, understanding the annual thresholds and limits is key to accurately calculating your progress and ensuring you’re on track.

How Much Earnings Equal One Credit?

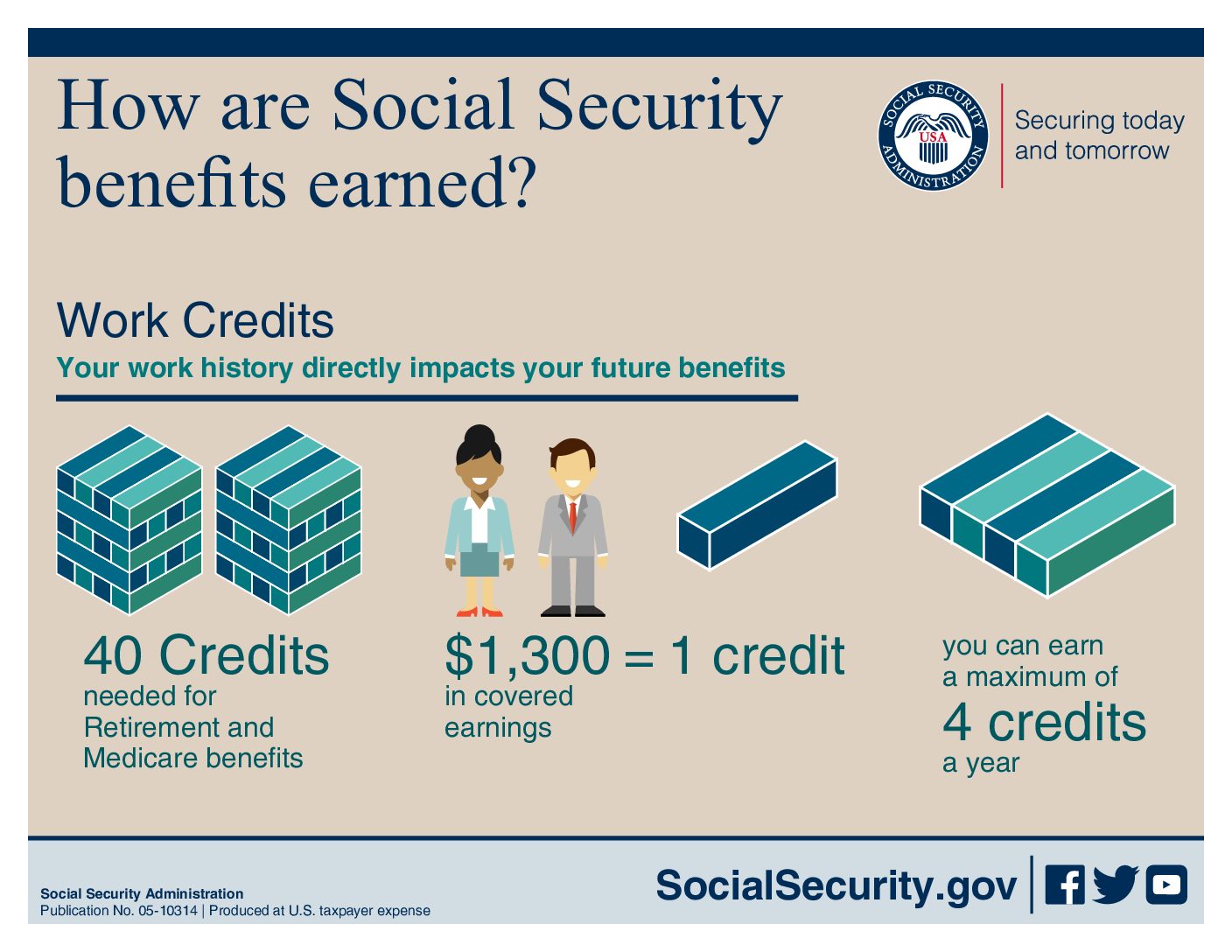

The amount of earnings required for one Social Security credit changes annually to reflect changes in national average wages. For instance, in 2024, you earn one Social Security credit for every $1,730 in earnings. This means that if you earn $1,730, you get one credit; if you earn $3,460, you get two credits, and so on. These earnings can come from wages (if you’re an employee) or from net earnings from self-employment. It’s important to note that these are cumulative earnings throughout the year, not per pay period. Your annual gross income is what determines your credit accumulation.

This threshold is a crucial piece of information for anyone planning their financial future, especially those who may work part-time, seasonally, or are self-employed. Keeping track of this figure each year helps you gauge how much income you need to earn to meet your credit goals.

The Maximum Credits You Can Earn Annually

There’s a cap on how many credits you can earn in a single year: a maximum of four credits. This means that even if you earn significantly more than four times the annual credit threshold, you will only receive four credits for that year. For example, in 2024, earning $6,920 (4 x $1,730) or more in the year would grant you the maximum four credits. Earning $100,000 would still only give you four credits for that year.

This annual maximum simplifies the system and ensures that individuals don’t disproportionately accumulate credits based on extraordinarily high earnings in a short period. It emphasizes consistent participation in the workforce over many years rather than sporadic high-income periods. The system is designed for long-term contributions.

The 40-Credit Rule: Your Key to Retirement Benefits

For most people, the magic number for Social Security retirement benefits is 40 credits. To be “fully insured” and eligible to receive retirement benefits when you reach your specific retirement age, you typically need to accumulate 40 credits. Since you can only earn a maximum of four credits per year, this translates to roughly 10 years of work (40 credits / 4 credits per year = 10 years).

It’s important to understand that these 10 years do not have to be consecutive. You can work for a few years, take time off, and then return to work, picking up where you left off. The SSA keeps a running tally of all the credits you earn throughout your entire working life. Once you hit the 40-credit mark, you are permanently fully insured for retirement benefits, regardless of any future breaks in employment. This rule provides immense flexibility and reassurance for individuals who may experience career changes, family leave, or periods of unemployment.

Beyond Retirement: The Broad Impact of Social Security Credits

While retirement benefits are often the first thing that comes to mind with Social Security, your earned credits extend their protective reach far beyond your golden years. They are crucial for securing a comprehensive financial safety net for you and your loved ones in various life circumstances.

Eligibility for Disability Benefits

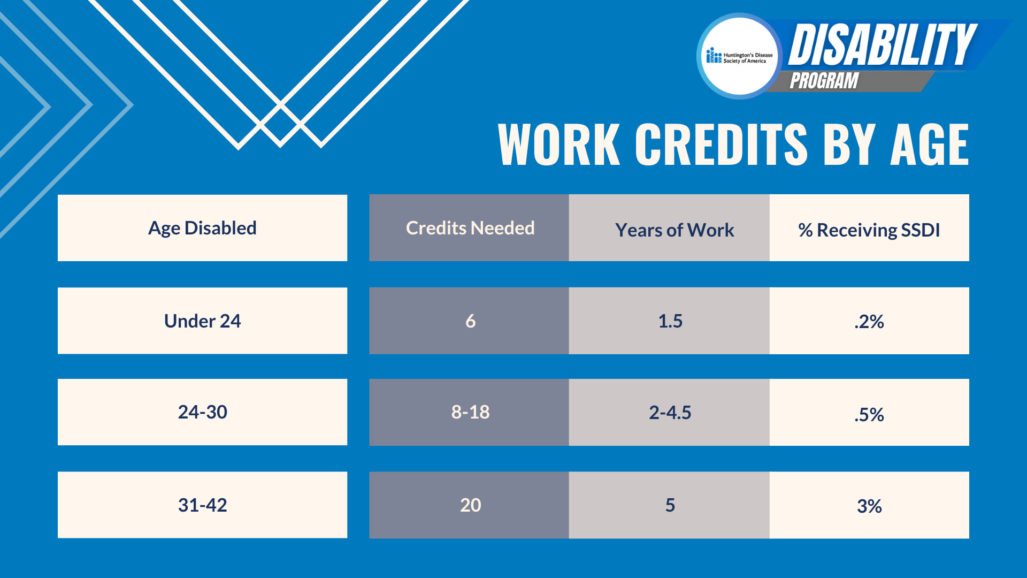

Should you become unable to work due to a severe physical or mental condition, Social Security Disability Insurance (SSDI) can provide a vital income stream. However, eligibility for SSDI is also contingent upon earning sufficient Social Security credits. The number of credits required depends on your age when your disability begins. Younger workers typically need fewer credits than older workers because they haven’t had as much time in the workforce.

For example, if you become disabled at age 31 or older, you generally need 20 credits earned in the 10 years immediately before your disability. For younger individuals, the requirements are less stringent, acknowledging that they have had less time to accumulate a long work history. For instance, if you become disabled before age 24, you might only need 6 credits earned in the 3 years before your disability. These “recency of work” rules are critical to understand, as falling short could leave you without vital income protection during a time of great need.

Survivor Benefits for Your Loved Ones

In the unfortunate event of your death, your Social Security credits can provide crucial financial support to your surviving family members, including your spouse, minor children, and dependent parents. These “survivor benefits” act as a form of life insurance, offering a safety net during a difficult time. The amount of credits you need for your family to be eligible for survivor benefits also varies.

Generally, you need 40 credits to be fully insured for survivor benefits, similar to retirement. However, a special rule called “currently insured” status allows benefits to be paid if you have earned 6 credits in the 3 years immediately before your death. This provision ensures that even younger workers or those with shorter work histories provide some level of protection for their families. Understanding these provisions is a critical component of estate planning and ensuring your loved ones are cared for.

Medicare Eligibility Considerations

While Medicare is a separate federal program providing health insurance for Americans aged 65 or older, and for certain younger people with disabilities, its eligibility is closely linked to Social Security. If you are eligible for Social Security retirement benefits (meaning you have 40 credits), you are automatically eligible for premium-free Part A of Medicare (hospital insurance) when you turn 65.

Even if you don’t collect Social Security retirement benefits at 65 (perhaps because you’re delaying for higher payments), your eligibility for Social Security credits grants you access to Medicare. If you have fewer than 40 credits, you may still qualify for Medicare Part A, but you might have to pay a monthly premium. This connection highlights the broad, integrated impact of your Social Security work history on your overall financial and health security in retirement.

Tracking Your Progress: Tools and Strategies for Monitoring Your Credits

Knowing how credits work is one thing; actually keeping tabs on your accumulated credits is another. Fortunately, the Social Security Administration provides robust tools and resources to help you monitor your progress and ensure your records are accurate. Proactive monitoring is a cornerstone of sound financial planning.

The Social Security Administration (SSA) Online Account

The single most important tool for tracking your Social Security credits is your personal “my Social Security” online account. Creating an account is free, secure, and provides immediate access to your earnings record. Through this portal, you can:

- View your complete earnings history, year by year.

- See how many Social Security credits you’ve accumulated.

- Get estimates of your future retirement, disability, and survivor benefits.

- Request a replacement Social Security card.

- Manage your direct deposit information if you’re already receiving benefits.

Setting up this account is highly recommended for anyone who has worked and paid into the system. It offers transparent, real-time access to the information that directly impacts your future financial security.

Reviewing Your Social Security Statement

Even if you don’t have an online account, the SSA periodically mails a paper Social Security Statement to workers aged 60 and over who are not yet receiving benefits. For younger workers, the statement is typically available online only. This statement provides a comprehensive summary of your earnings record, estimated benefits, and the number of credits you’ve earned.

It’s crucial to review this statement carefully each time you receive it. Check your earnings history against your own records (such as W-2s or tax returns) to ensure accuracy. Mistakes can happen, and they are easier to correct when caught early. Any discrepancies in your reported earnings could impact your future benefits, potentially reducing them.

What to Do If There Are Discrepancies

If you identify any discrepancies in your earnings record – for instance, if a year’s income is missing or incorrect – it’s vital to act quickly. Contact the Social Security Administration immediately to report the error. You will likely need to provide documentation, such as W-2 forms, tax returns, or pay stubs, to prove your correct earnings.

The SSA has a process for correcting earnings records, but it often requires clear evidence. Keeping meticulous records of your employment history and income is not just good practice for tax purposes, but also for safeguarding your Social Security benefits. Resolving these issues early ensures that your credit count and future benefit calculations are accurate, protecting your financial future.

Strategic Financial Planning with Social Security Credits

Understanding and tracking your Social Security credits is not an isolated task; it’s an integral part of a broader financial strategy. By strategically integrating your knowledge of credits, you can make more informed decisions about your retirement, savings, and overall financial well-being.

Integrating Credits into Your Retirement Strategy

Your Social Security credits dictate your eligibility, but your overall retirement strategy needs to consider how those benefits will complement your other income sources. Knowing you have 40 credits means you’re “in,” but it doesn’t tell you how much you’ll receive. Your benefit amount is calculated based on your highest 35 years of indexed earnings. Therefore, working longer, especially during your peak earning years, can significantly increase your monthly benefit.

Consider Social Security as one leg of a three-legged stool for retirement income, alongside personal savings (401(k)s, IRAs) and pensions. Understanding your projected Social Security income allows you to determine how much more you need to save to meet your retirement goals. It also influences decisions like when to stop working, when to claim benefits, and how to structure your withdrawals from other retirement accounts.

Understanding Your Full Retirement Age (FRA)

Your “full retirement age” (FRA) is the age at which you are entitled to receive 100% of your Social Security retirement benefits. This age varies depending on your birth year. For those born between 1943 and 1954, it’s 66. For those born in 1960 or later, it’s 67. Understanding your FRA is critical because it dictates the impact of claiming benefits earlier or later.

Claiming benefits before your FRA (as early as age 62) results in a permanent reduction in your monthly payment. Conversely, delaying beyond your FRA (up to age 70) results in a significant increase in your monthly payment due to “delayed retirement credits.” Knowing your FRA and your credit status allows you to calculate the financial implications of these claiming decisions, optimizing your lifetime benefits.

The Value of Early and Delayed Claiming

The decision of when to start collecting Social Security benefits is one of the most significant financial choices many people face. It’s not just about when you become eligible with your credits, but also about maximizing your overall financial health.

- Early Claiming (as early as age 62): While your monthly benefit will be permanently reduced, early claiming can provide much-needed income if you are no longer able to work, face health challenges, or simply want to retire sooner. It also means you receive payments for a longer duration.

- Delayed Claiming (up to age 70): Delaying benefits past your FRA can increase your monthly payment by 8% per year for each year you delay, up to age 70. This can result in a significantly higher monthly check for the rest of your life, which is particularly advantageous if you anticipate a long lifespan or have other income sources to bridge the gap until 70.

The optimal claiming strategy depends on a multitude of factors, including your health, other retirement savings, spousal benefits, and life expectancy. Your Social Security credits ensure you can claim; strategic planning around your FRA helps you decide when and how to maximize those claims for your specific circumstances.

Conclusion

Social Security credits are more than just an abstract accounting measure; they are the bedrock of your eligibility for critical financial protection in retirement, during disability, and for your family in the event of your passing. Understanding how to calculate and track these credits is a fundamental step in responsible personal financial planning.

By diligently monitoring your earnings history through your “my Social Security” account, reviewing your annual statements, and acting swiftly on any discrepancies, you empower yourself to navigate this essential system with confidence. Integrate this knowledge into your broader retirement strategy, mindful of your full retirement age and the implications of early or delayed claiming, and you will be well on your way to securing a stable and predictable financial future. Your Social Security benefits are a hard-earned right; make sure you understand how to claim them fully and strategically.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.