In the realm of high-stakes finance, personal wealth management, and corporate strategy, numbers are the universal language. However, raw data often fails to tell the complete story. To understand growth, assess risk, and compare disparate assets, one must master the most fundamental tool in the financial arsenal: the percentage. Whether you are analyzing a stock’s year-to-date performance, determining the impact of inflation on your purchasing power, or calculating the gross margin of a startup, knowing how to calculate percentage accurately is the bridge between raw data and actionable intelligence.

This guide provides a comprehensive deep dive into percentage calculations through the lens of money, investing, and business finance, ensuring you can navigate the complexities of the modern economy with precision.

1. The Fundamentals of Financial Percentages

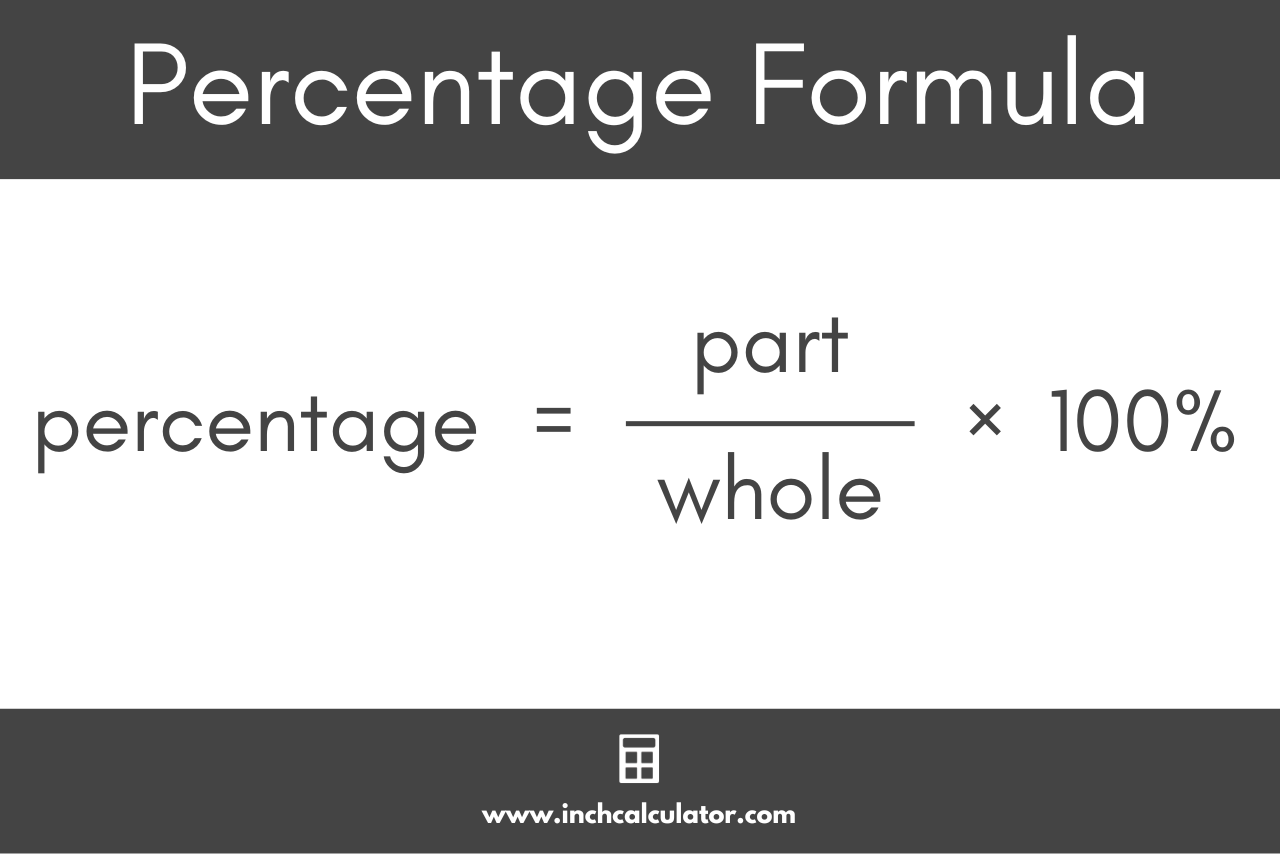

At its core, a percentage is a ratio that represents a fraction of 100. In finance, this simple mathematical concept allows for a standardized comparison between different scales of investment. Without percentages, it would be impossible to compare the performance of a $1,000 retail account against a $1 billion hedge fund.

The Core Formula: Converting Values to Ratios

The basic formula for finding a percentage is:

** (Part / Whole) × 100 = Percentage **

In a financial context, this is often used to determine portfolio allocation. For example, if you have $25,000 invested in gold within a total portfolio of $100,000, the calculation is ($25,000 / $100,000) × 100, resulting in a 25% allocation. Mastering this allows investors to maintain a balanced risk profile, ensuring they are not over-leveraged in a single asset class.

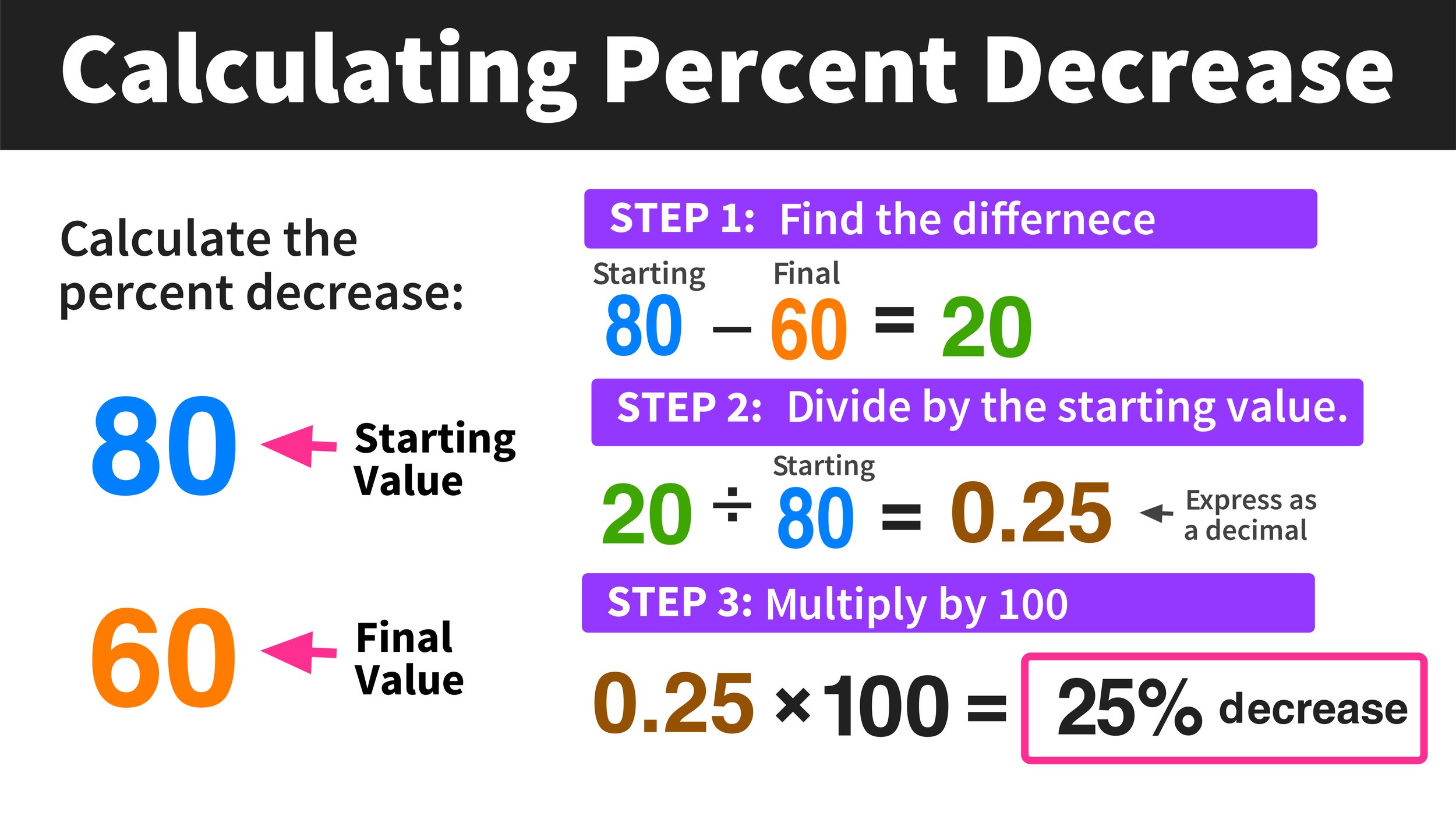

Percentage Increase vs. Decrease in Market Trends

Volatility is an inherent part of the financial markets. Understanding the “Percentage Change” formula is critical for tracking gains and losses over time. The formula is:

** [(New Value – Old Value) / Old Value] × 100 **

If a stock price moves from $150 to $180, the increase is 20%. Conversely, if it drops from $150 to $120, the decrease is 20%. However, a vital lesson for every investor is the “Asymmetry of Loss.” If an asset drops by 50%, it requires a 100% gain just to return to the original break-even point. This mathematical reality is why risk management and stop-loss orders are foundational to wealth preservation.

2. Calculating Returns on Investment (ROI)

For the serious investor, the primary objective is the efficient allocation of capital to generate maximum returns. Return on Investment (ROI) is the ultimate metric for evaluating the efficiency of an investment or comparing the efficiencies of several different investments.

Real Estate and Dividend Yields

In real estate and dividend investing, percentages are used to calculate “Yield.” For a rental property, the “Cap Rate” (Capitalization Rate) is a percentage calculated by dividing the Net Operating Income (NOI) by the current market value.

- Formula: (Annual Net Income / Property Price) × 100

A property purchased for $500,000 that generates $30,000 in annual profit has a 6% cap rate. Similarly, dividend yield is calculated by dividing the annual dividend per share by the share price. These percentages allow investors to treat real estate or equities like “yield-bearing instruments,” comparing them directly against the “risk-free rate” offered by government bonds.

Compounding Interest: The Rule of Percentage Over Time

Perhaps the most powerful force in finance is compound interest—the process where the value of an investment grows based on both the initial principal and the accumulated interest from previous periods. The “Annual Percentage Yield” (APY) reflects the real rate of return on an investment, taking into account the effect of compounding.

When calculating compound interest, the frequency of the percentage application (monthly, quarterly, annually) drastically changes the outcome. Professional investors use the “Rule of 72” as a quick mental percentage calculation: divide 72 by your annual interest rate to find out approximately how many years it will take for your money to double.

3. Business Finance and Profit Margin Analysis

For entrepreneurs and corporate executives, percentages are the primary indicators of a company’s health. While “revenue is vanity,” “profit is sanity,” and profit is almost always measured in percentages.

Gross vs. Net Profit Margins

A company might generate millions in sales, but if its margins are thin, it remains a high-risk venture.

- Gross Profit Margin: This percentage reveals how efficiently a company produces its goods. Calculated as [(Revenue – Cost of Goods Sold) / Revenue] × 100.

- Net Profit Margin: This is the “bottom line.” It accounts for all expenses, including taxes and interest.

A high net profit margin suggests a company has significant “moat” or competitive advantage, allowing it to keep more cents of every dollar earned. Investors often look for expanding margins as a sign of operational excellence and scaling efficiency.

Markup vs. Margin: Avoiding the Common Entrepreneurial Trap

One of the most frequent financial errors in business is confusing “markup” with “margin.”

- Markup is the percentage added to the cost to reach a selling price.

- Margin is the percentage of the selling price that is profit.

If an item costs $80 and you sell it for $100, your markup is 25% ($20 is 25% of $80). However, your profit margin is only 20% ($20 is 20% of $100). Miscalculating this can lead to disastrous pricing strategies where overhead costs exceed the actual margin, leading to a business that loses money despite high sales volume.

4. Personal Finance and Debt Management

On an individual level, percentages dictate the cost of our lifestyles. From the interest we pay on debt to the way we structure our monthly spending, the ability to calculate and manipulate these figures is the definition of financial literacy.

Calculating APR and Credit Card Interest

Annual Percentage Rate (APR) represents the yearly cost of borrowing money. However, most credit cards calculate interest daily. To understand the true cost of debt, you must divide the APR by 365 to find the “Daily Periodic Rate.”

If you carry a balance of $5,000 on a card with a 24% APR, you are accruing roughly $3.28 in interest every single day. Seeing debt as a daily percentage cost often provides the necessary psychological shift for individuals to prioritize debt repayment over discretionary spending.

The 50/30/20 Rule: Percentage-Based Budgeting

Financial planners often recommend a percentage-based approach to budgeting to ensure long-term stability. The 50/30/20 rule suggests:

- 50% of income to Needs (housing, utilities, groceries).

- 30% of income to Wants (entertainment, dining out).

- 20% of income to Savings and Debt Repayment.

By viewing a budget through percentages rather than fixed dollar amounts, your financial plan becomes “scalable.” As your income increases, your lifestyle doesn’t simply inflate to match it; instead, your savings and investments grow proportionally.

5. Practical Tools for Financial Precision

While mental math is a valuable skill, professional financial management requires precision. In a world of digital tools, the “how” of percentage calculation often moves into the realm of software and specialized metrics.

Using Spreadsheet Functions for Automated Calculations

In platforms like Microsoft Excel or Google Sheets, calculating percentages is automated, but the logic remains the same. To calculate a percentage change across a thousand-line spreadsheet, one uses the cell formula =(New_Cell - Old_Cell)/Old_Cell and then formats the column as a percentage.

Advanced users utilize “Weighted Averages,” where different percentages are given different “weights” based on their importance—a critical technique for calculating the performance of a diversified investment portfolio where the positions are of unequal size.

Tax Obligations and Effective Tax Rates

Finally, understanding percentages is vital for tax planning. Many people confuse their “Tax Bracket” (Marginal Tax Rate) with their “Effective Tax Rate.”

The Marginal Rate is the percentage paid only on the last dollar earned, while the Effective Rate is the actual percentage of your total income that goes to the government (Total Tax / Total Taxable Income). Understanding this percentage allows for better “tax-loss harvesting” and retirement planning, ensuring that you keep a larger percentage of your hard-earned wealth.

Conclusion

Mastering the calculation of percentages is more than just a mathematical exercise; it is a fundamental requirement for financial freedom. From the micro-calculations of daily interest to the macro-analysis of corporate profit margins, percentages provide the clarity needed to make informed decisions. By looking at your money through the lens of percentages, you move away from emotional reactions and toward a disciplined, data-driven approach to wealth creation. Whether you are an investor, an entrepreneur, or simply someone looking to master their personal budget, the humble percentage is your most powerful ally in the pursuit of prosperity.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.