In the realm of finance, numbers are more than just digits on a screen; they are the narrative of progress, the heartbeat of an investment, and the ultimate indicator of success. Whether you are tracking the growth of a retirement portfolio, evaluating the scalability of a startup, or negotiating a salary raise, understanding how to calculate percent increase is a fundamental skill. It transforms raw data into actionable insights, allowing you to compare performance across different asset classes and timeframes.

This guide provides a comprehensive deep dive into the mechanics of percentage growth within the “Money” niche, covering everything from basic formulas to advanced applications in wealth management and corporate finance.

1. The Core Formula and Financial Fundamentals

At its simplest level, calculating a percent increase allows you to quantify how much a value has grown relative to its starting point. In finance, this is often referred to as a “rate of return” or “growth rate.” Without this calculation, it is impossible to determine if a $5,000 gain is impressive or negligible.

The Basic Mathematical Equation

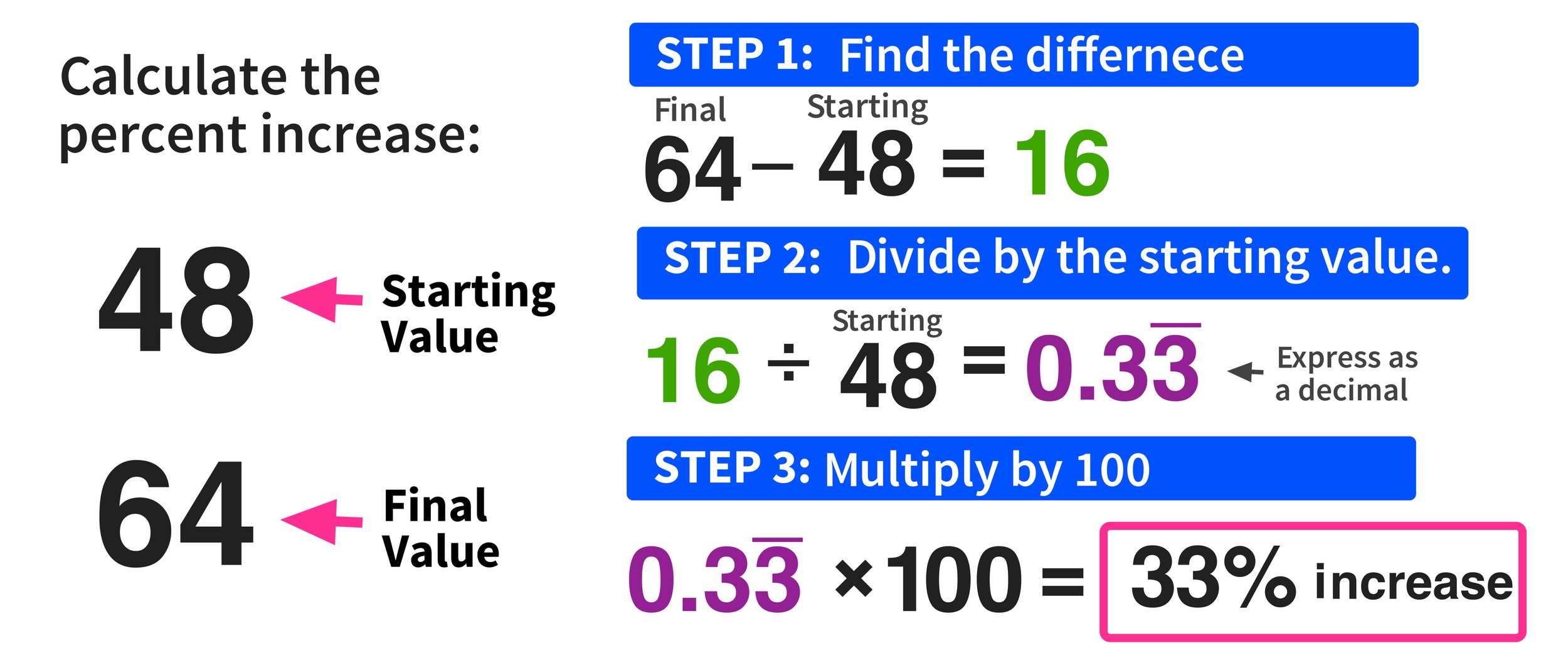

To find the percent increase, you follow a three-step logical process. First, subtract the original value from the new value to find the “increase amount.” Second, divide that increase by the original value. Finally, multiply the result by 100 to convert the decimal into a percentage.

The formula is expressed as:

((New Value – Original Value) / Original Value) × 100 = Percent Increase

For example, if you purchased a share of a tech conglomerate for $150 and its current market price is $195, the calculation would be:

- $195 – $150 = $45 (The absolute gain)

- $45 / $150 = 0.3

- 0.3 × 100 = 30%

Why Context Matters in Finance

While the math remains constant, the interpretation of the percentage changes based on the financial context. In personal finance, a 5% increase in your savings account yield is a victory. In the world of high-risk venture capital, a 5% year-over-year growth rate might be seen as a failure. Understanding the “denominator”—the original value—is crucial. A 100% increase on a $1 investment results in only $2, whereas a 1% increase on a $1,000,000 portfolio results in $10,000. Real wealth is built by maximizing both the percentage and the principal.

2. Measuring Investment Performance and Wealth Accumulation

For investors, the percent increase is the primary metric for evaluating the efficiency of capital allocation. It allows an “apples-to-apples” comparison between disparate investments, such as real estate, stocks, and cryptocurrencies.

Evaluating Portfolio Gains and ROI

Return on Investment (ROI) is perhaps the most common application of the percent increase formula. When you look at your brokerage statement, the “Total Return” is essentially the percent increase of your initial capital plus any dividends reinvested.

However, investors must distinguish between “nominal” and “real” percent increases. If your portfolio grew by 8% this year, but inflation was 4%, your “real” percent increase in purchasing power is only 4%. Professional wealth managers use these calculations to determine if an asset is actually building wealth or merely keeping pace with the devaluing currency.

Compound Growth vs. Simple Percent Increase

While a simple percent increase measures growth over a single period, financial mastery requires understanding how these increases stack over time. This is known as the Compound Annual Growth Rate (CAGR). If an investment increases by 10% one year and 10% the next, the total increase isn’t 20%—it’s 21%, because the second year’s growth applies to the new, larger base. Calculating the percent increase annually allows you to see the “snowball effect” of compound interest, which is the cornerstone of long-term wealth building.

3. Business Finance and Revenue Scaling

In a corporate or entrepreneurial setting, calculating percent increase is the standard method for reporting financial health to stakeholders. It moves the conversation beyond “how much did we make?” to “how fast are we growing?”

Year-over-Year (YoY) and Month-over-Month (MoM) Growth

Businesses use percent increase to track seasonal trends and growth trajectories. Year-over-Year (YoY) calculations compare a specific timeframe (like Q3 2023) against the same timeframe in the previous year (Q3 2022). This eliminates “noise” from seasonal fluctuations.

For instance, a retail business might see a 50% increase in sales in December compared to November. While that sounds impressive, a YoY calculation might reveal that sales are actually 5% lower than last December, signaling a potential decline in market share or consumer demand.

Analyzing Profit Margins and Cost Escalation

Revenue growth is only one side of the coin. A savvy business owner also calculates the percent increase in operating expenses. If your revenue increases by 20% but your costs increase by 30%, your profit margin is shrinking despite the higher sales volume.

By applying the percent increase formula to “Cost of Goods Sold” (COGS) and overhead, businesses can identify “bracket creep”—the subtle increase in expenses that eats away at the bottom line. Calculating the percent increase in “Net Profit” is the ultimate test of a business’s operational efficiency.

4. Personal Budgeting and the Impact of Inflation

On a microeconomic level, your personal financial success depends on your ability to ensure your income’s percent increase outpaces the percent increase of your expenses.

Tracking Income Growth and Salary Negotiations

When preparing for a performance review, you should never walk into the room without knowing your numbers. If you received a $5,000 raise on a $50,000 salary, that is a 10% increase. If your workload or responsibilities increased by an estimated 30%, you have a mathematical basis to argue for a higher adjustment. Understanding your personal “income growth rate” helps you determine if you are moving toward your financial goals or if your career has plateaued.

Measuring the Real Value of Money Against Inflation

Inflation is essentially a percent increase in the Consumer Price Index (CPI). If the cost of living increases by 6% annually, and you do not receive a raise, you have effectively taken a 6% pay cut in terms of purchasing power.

By calculating the percent increase in your recurring bills—rent, groceries, utilities—you can adjust your budget proactively. If your grocery bill has seen a 15% increase over twelve months, it may be time to reallocate funds from discretionary spending (like entertainment) to maintain your savings rate.

5. Advanced Financial Tools and Avoiding Mathematical Pitfalls

While the formula is straightforward, the application of percent increase in complex financial models requires precision and the right tools.

Using Excel and Google Sheets for Real-Time Tracking

In the modern financial landscape, manual calculations are often replaced by automation. In spreadsheet software, calculating percent increase is simplified. If your original value is in cell A1 and your new value is in B1, the formula is:

=(B1-A1)/A1

By formatting the cell as a percentage, you gain an instant view of performance. This is particularly useful for tracking “Trailing Twelve Months” (TTM) performance or monitoring volatile assets like individual stocks.

The Asymmetry of Percentage Gains and Losses

One of the most critical lessons in business finance is the “Asymmetry of Loss.” A common pitfall is assuming that a 50% loss can be recovered by a 50% gain. It cannot.

If you have $100 and it drops by 50%, you have $50. To get back to $100, that $50 must increase by $50, which is a 100% increase. Understanding this mathematical reality changes how an investor views risk. It highlights the importance of capital preservation: the larger the percent decrease, the exponentially larger the percent increase required just to break even.

Conclusion

Mastering the calculation of percent increase is not merely an exercise in arithmetic; it is an essential component of financial literacy. It provides the clarity needed to navigate the complexities of the stock market, the nuances of corporate balance sheets, and the day-to-day realities of personal budgeting. By consistently applying this formula, you can strip away the emotional bias of raw numbers and see your financial journey for what it truly is—a series of growth rates that, if managed correctly, lead to long-term prosperity and security.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.