Understanding how to calculate interest on a bank account is more than just a mathematical exercise; it is a fundamental pillar of financial literacy. In an era of fluctuating inflation and shifting central bank policies, knowing exactly how your money grows—or why it might be stagnating—is essential for anyone looking to build long-term wealth. Interest is essentially the “rent” a bank pays you to use your money. While the concept seems simple, the mechanics of compounding, the distinction between various interest rates, and the impact of external economic factors can make the reality quite complex.

This guide explores the intricate details of interest calculation, the variables that influence your earnings, and the strategic choices you can make to ensure your capital is working as hard as possible for you.

1. Understanding the Fundamentals: Simple vs. Compound Interest

Before diving into complex formulas, it is vital to distinguish between the two primary ways interest is calculated. The difference between these two methods can result in a discrepancy of thousands of dollars over a long-term savings horizon.

Simple Interest: The Basics

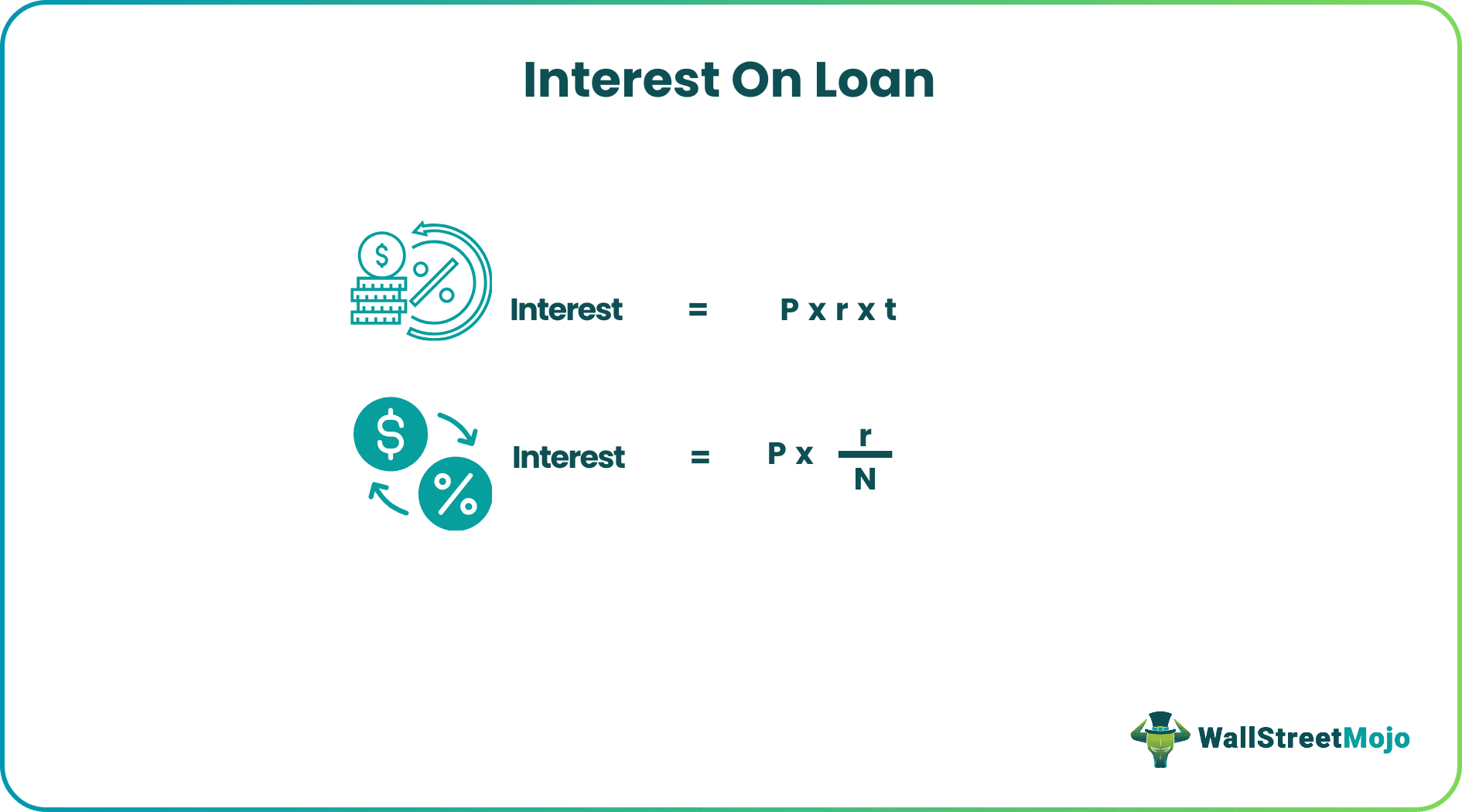

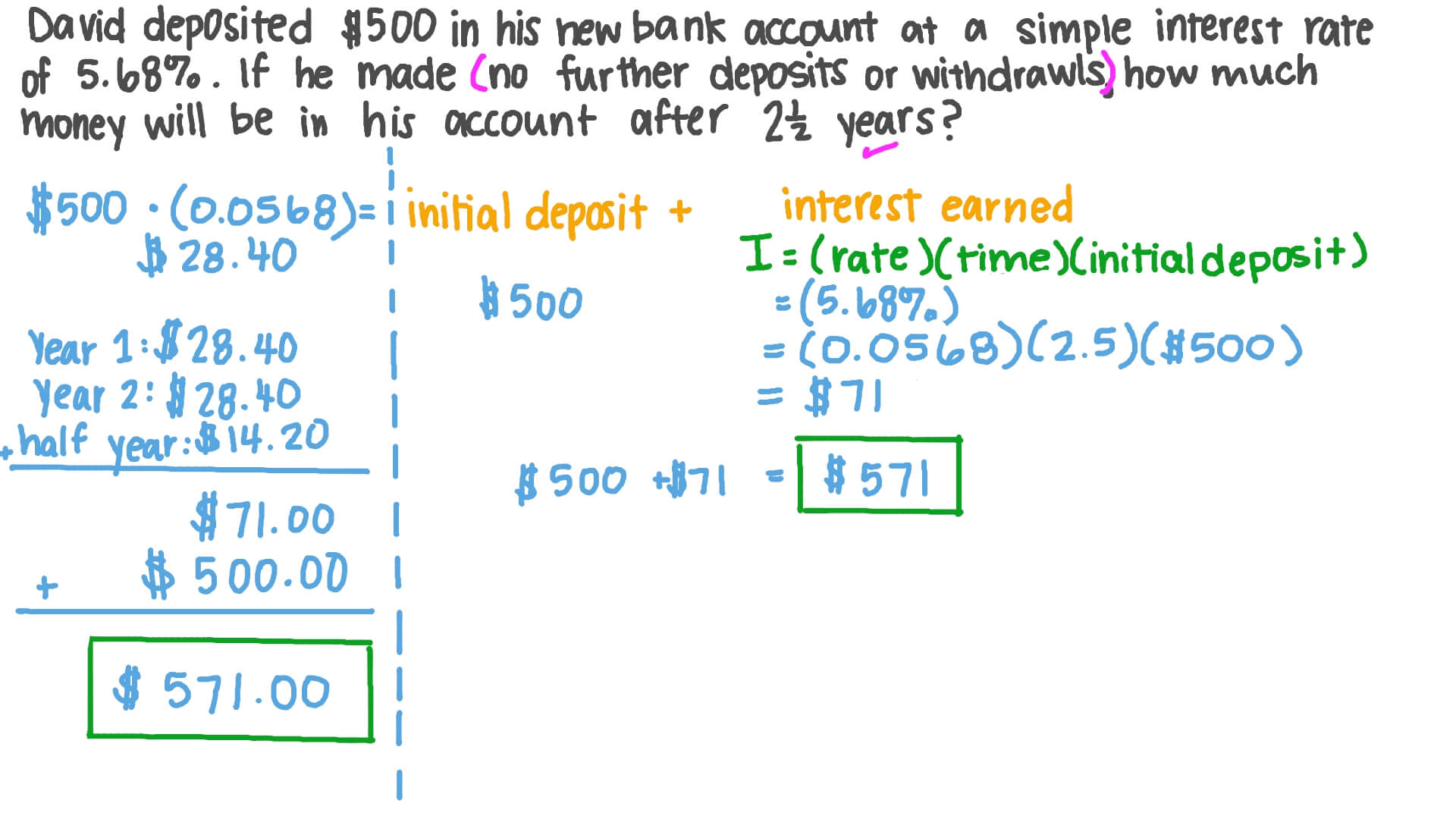

Simple interest is the most straightforward way to calculate earnings. It is determined by multiplying the daily interest rate by the principal (the amount of money in the account) by the number of days that elapse between payments.

The formula is: Interest = Principal × Rate × Time.

In a simple interest scenario, you only earn money on the initial deposit you made. While this is rare for modern savings accounts—which almost exclusively use compounding—it is still a common calculation for certain types of short-term loans or basic certificates of deposit (CDs).

Compound Interest: The Engine of Wealth

Compound interest is often referred to as “interest on interest.” It occurs when the interest you earn is added back into your principal balance, and then the next round of interest is calculated based on that new, higher total.

The formula for compound interest is: A = P (1 + r/n)^(nt)

- A = the future value of the investment/loan, including interest.

- P = the principal investment amount.

- r = the annual interest rate (decimal).

- n = the number of times that interest is compounded per unit t.

- t = the time the money is invested for.

The more frequently interest compounds—whether daily, monthly, or quarterly—the faster your balance grows. Most modern high-yield savings accounts compound interest daily and credit it to your account monthly.

APY vs. APR: Knowing the Difference

When browsing bank websites, you will encounter two acronyms: APR (Annual Percentage Rate) and APY (Annual Percentage Yield).

- APR represents the simple interest rate over a year without taking compounding into account.

- APY reflects the total amount of interest you will earn in one year, including the effect of compounding.

For a saver, the APY is the most accurate representation of your potential earnings. If a bank advertises a 5.00% APR with daily compounding, the APY will actually be slightly higher (approximately 5.13%). Always use the APY when comparing different financial institutions.

2. The Mathematics of Interest Calculation: A Step-by-Step Approach

To truly master your personal finances, you should be able to manually verify the interest credited to your account. This ensures that you are not losing money to hidden fees or calculation errors.

Calculating Your Daily Interest Rate

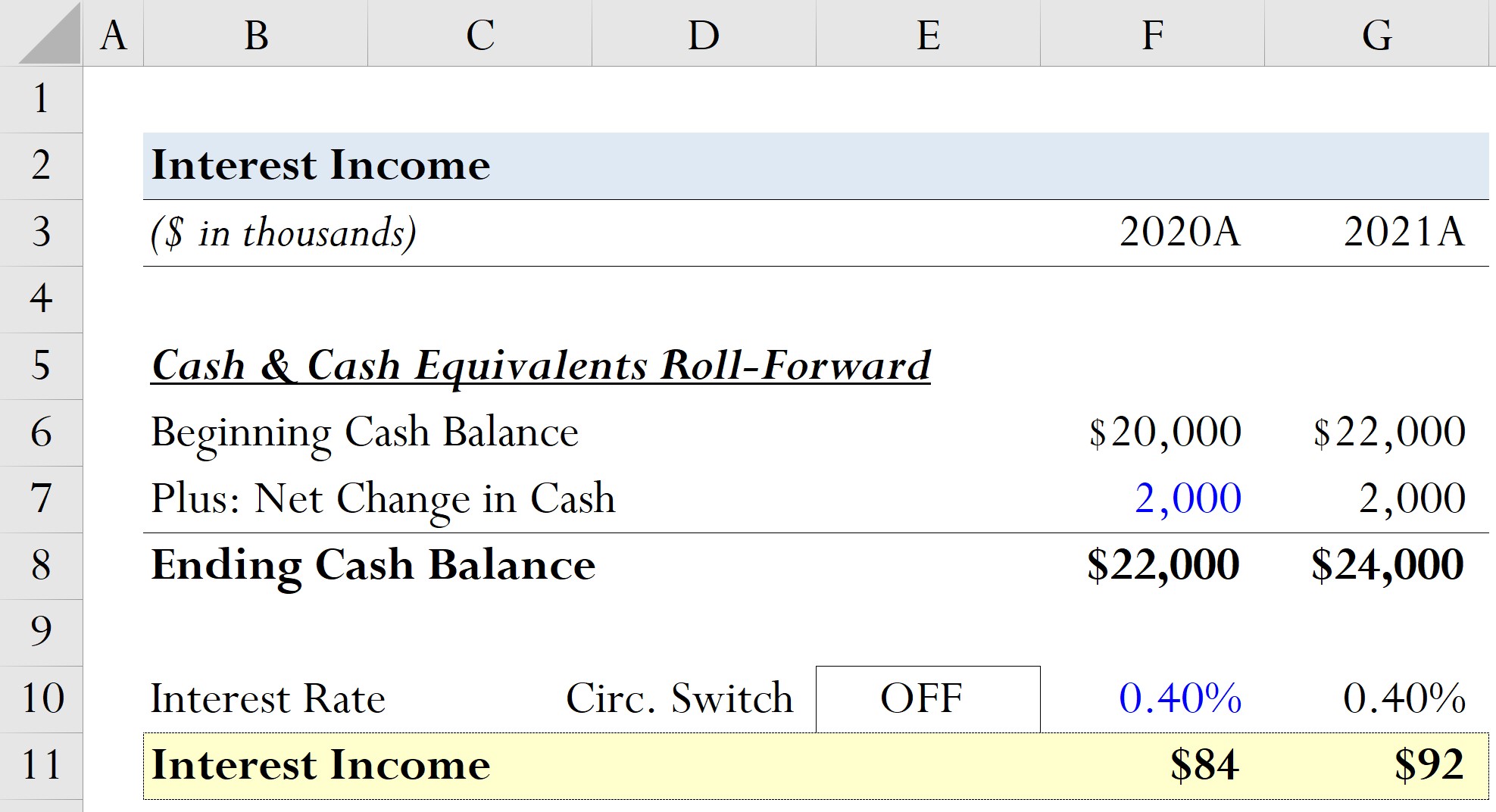

Banks typically quote interest rates as an annual figure. To find out how much you are earning on a daily basis, you must divide the annual rate by the number of days in the year.

For example, if you have a 4% annual interest rate:

0.04 (interest rate) ÷ 365 (days) = 0.000109589.

This small decimal is your daily periodic rate. When applied to a $10,000 balance, you would earn roughly $1.10 per day.

The Impact of Compounding Frequency

The frequency of compounding is the “secret sauce” of growth. Consider a $10,000 deposit at a 5% interest rate:

- Annual Compounding: After one year, you have $10,500.

- Monthly Compounding: After one year, you have $10,511.62.

- Daily Compounding: After one year, you have $10,512.67.

While the difference between monthly and daily compounding might seem negligible in the short term, over twenty or thirty years, those extra dollars compound upon themselves, creating a significant “snowball effect.”

The Rule of 72: A Quick Mental Shortcut

If you want to know how long it will take to double your money at a specific interest rate, use the “Rule of 72.” Simply divide 72 by your interest rate.

For example, if your bank account offers a 4% interest rate, it will take approximately 18 years (72 ÷ 4 = 18) for your money to double without any additional deposits. This tool is invaluable for quick comparisons when deciding between different investment or savings vehicles.

3. Factors That Influence Your Interest Earnings

Calculating interest isn’t just about the formula; it’s about the variables that go into it. Several external and internal factors can fluctuate, affecting your bottom line.

Federal Reserve Policy and Market Trends

In many countries, bank interest rates are heavily influenced by the central bank’s “benchmark rate” (such as the Federal Funds Rate in the U.S.). When the central bank raises rates to combat inflation, commercial banks usually follow suit by increasing the interest they pay on savings accounts. Conversely, in a low-rate environment, your bank interest might struggle to keep pace with the cost of living. Understanding this relationship helps you time your moves, such as locking in a high rate with a CD before the Fed cuts rates.

Minimum Balance Requirements and Tiered Interest

Many financial institutions use “tiered” interest structures. For instance, a bank might offer 4.5% interest on the first $25,000 in your account, but only 1.0% on any amount exceeding that threshold. Alternatively, some accounts require a minimum daily balance to earn any interest at all. If your balance dips below that minimum for even one day, the bank may waive interest for the entire month and potentially charge a maintenance fee, effectively giving you a negative return.

The Hidden Impact of Taxes and Inflation

It is a common mistake to view interest earnings in a vacuum. In reality, two forces “tax” your interest:

- Income Tax: In most jurisdictions, interest earned is considered taxable income. At the end of the year, your bank will issue a form (like a 1099-INT) reporting your earnings to the tax authorities.

- Inflation: If your bank account earns 3% interest but inflation is at 4%, your “real” interest rate is -1%. While your numerical balance is increasing, your purchasing power is actually decreasing. To truly grow wealth, your goal should be to find interest rates that exceed the current rate of inflation.

4. Practical Strategies to Maximize Your Returns

Knowing how to calculate interest is the first step; the second is applying that knowledge to maximize your personal wealth.

Utilizing High-Yield Savings Accounts (HYSA)

The most effective way to boost your interest earnings without taking on market risk is to move funds from a traditional “brick-and-mortar” bank to an online High-Yield Savings Account. Because online banks have lower overhead costs, they can offer interest rates that are often 10 to 20 times higher than the national average. By using the calculation methods mentioned earlier, you can see that moving $20,000 from a 0.01% account to a 4.5% account results in an extra $898 in interest over a single year.

Implementing a CD Ladder

Certificates of Deposit (CDs) usually offer higher interest rates than standard savings accounts in exchange for “locking up” your money for a set period. To maintain liquidity while still capturing high rates, many investors use a “CD Ladder.”

By dividing your total savings into five equal parts and opening 1-year, 2-year, 3-year, 4-year, and 5-year CDs, you ensure that one-fifth of your money becomes available every year. This allows you to reinvest at higher rates if interest rates are rising, while still benefiting from the higher yields of long-term deposits.

Monitoring Digital Tools and Calculators

While manual calculation is a great skill, digital tools can help you model complex scenarios involving monthly contributions. Many personal finance apps allow you to input your current balance, interest rate, and monthly “top-off” amount to project your savings 10 or 20 years into the future. This visualization is a powerful psychological motivator for consistent saving.

Conclusion: The Path to Financial Empowerment

Calculating interest on your bank account is more than just checking a box on a monthly statement; it is the process of monitoring your financial health. By understanding the difference between APY and APR, recognizing the power of daily compounding, and staying aware of how inflation and taxes erode your gains, you transition from a passive saver to an active manager of your wealth.

In the world of finance, knowledge is the ultimate multiplier. When you understand exactly how your money grows, you are better equipped to make the strategic decisions—like switching to a high-yield account or laddering CDs—that lead to long-term financial independence. Remember, every decimal point in an interest rate represents your hard-earned money; ensure you are capturing every cent possible.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.