Purchasing a vehicle is often the second most significant financial commitment an individual makes, trailing only the purchase of a home. While most consumers focus heavily on the “sticker price” or the monthly payment amount, the true cost of owning a vehicle is often hidden within the nuances of the loan’s interest. Understanding how to calculate interest on a car loan is not merely an academic exercise in mathematics; it is a vital financial skill that empowers you to negotiate better terms, choose the right lending product, and potentially save thousands of dollars over the life of your debt.

To truly master your personal finances, you must look beyond the monthly bill and understand the mechanics of amortization, the difference between various interest types, and how your financial profile dictates the rates you are offered. This guide provides a deep dive into the calculations and strategic considerations of auto financing.

Understanding the Fundamentals: The Components of an Auto Loan

Before diving into complex formulas, it is essential to define the variables that dictate how much you will pay for the privilege of borrowing money. In the world of personal finance, three primary factors interact to determine the cost of your car loan.

Principal Amount and Down Payments

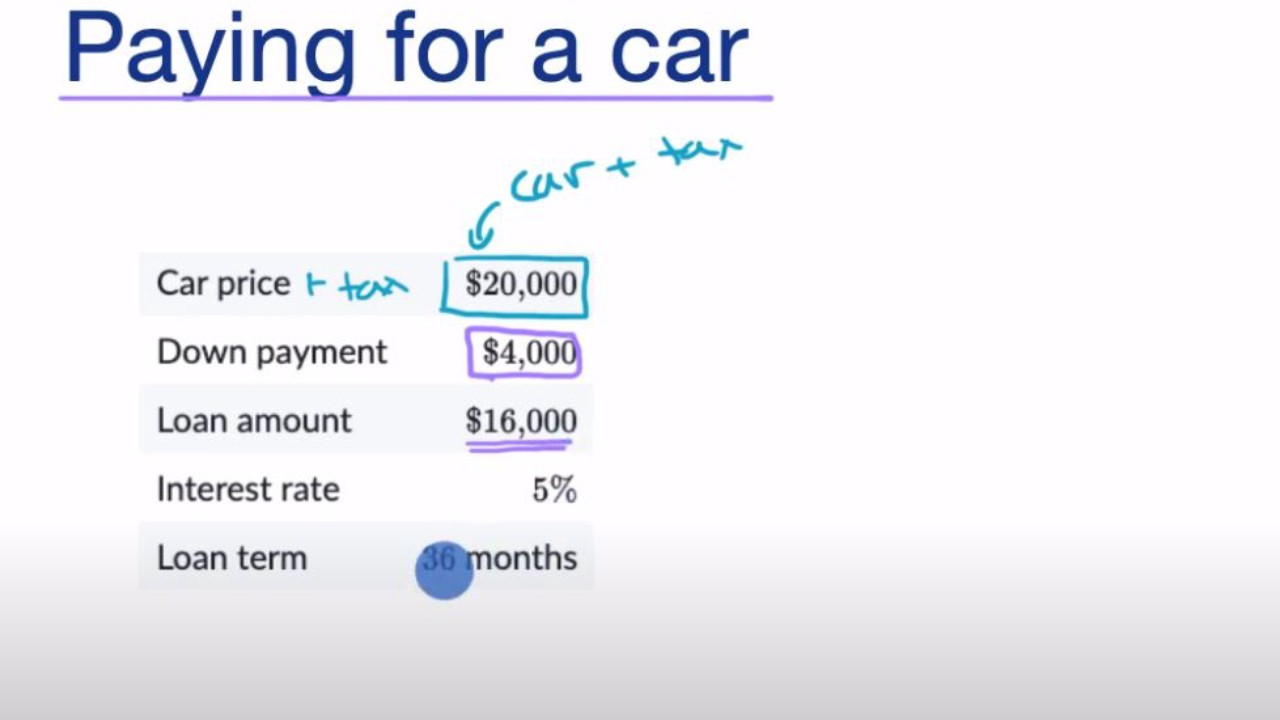

The principal is the total amount of money you borrow from a lender to purchase the vehicle. This is not necessarily the price of the car. The principal is calculated by taking the purchase price, adding taxes, registration fees, and any “add-ons” (like extended warranties), and then subtracting your down payment or the trade-in value of your old vehicle.

From a financial health perspective, the principal is the most dangerous component of the loan because it is the “seed” from which interest grows. A larger down payment reduces the principal, which in turn reduces the base upon which interest is calculated, leading to exponential savings over time.

Annual Percentage Rate (APR) vs. Interest Rate

It is a common mistake to use the terms “interest rate” and “APR” interchangeably. The interest rate is the percentage of the principal that the lender charges you annually to borrow the money. The APR, however, is a more inclusive figure. It includes the interest rate plus any additional fees or costs associated with the loan, such as origination fees or documentation charges. When calculating the total cost of a loan, the APR provides the most accurate reflection of the true annual cost.

The Loan Term and Amortization

The loan term is the duration you have to pay back the loan, typically expressed in months (e.g., 36, 48, 60, or 72 months). While longer terms result in lower monthly payments—making them attractive to budget-conscious buyers—they significantly increase the total interest paid. Auto loans are generally “amortized,” meaning your monthly payment stays the same, but the ratio of the payment going toward interest versus principal shifts over time. In the early stages of the loan, a larger portion of your payment goes toward interest.

The Mechanics of Interest: Simple vs. Compound Calculations

Most modern car loans utilize “simple interest.” This is a borrower-friendly structure compared to the compound interest found in credit cards. However, understanding how these calculations function is key to managing your debt effectively.

Why Most Car Loans Use Simple Interest

Simple interest is calculated based on the principal balance on the day the payment is due. Because your principal decreases every time you make a payment, the amount of interest you owe also decreases over time. This structure rewards borrowers who make extra payments or pay more than the minimum, as reducing the principal faster directly lowers the interest accrued in the following months.

The Dangers of Precomputed Interest

While rare in prime lending, some subprime or “buy-here-pay-here” lots use precomputed interest. In this scenario, the total interest for the entire life of the loan is calculated at the beginning and added to the principal. Unlike simple interest, paying off a precomputed loan early does not necessarily save you money on interest because the total interest amount was locked in at the start. Always confirm that your loan is a simple interest contract before signing.

Daily Interest Accrual

Under a simple interest model, interest usually accrues daily. To find your daily interest rate, you divide your APR by 365. This small number is then multiplied by your current principal balance. This is why the timing of your payment matters; if you pay a few days early, less interest has accrued, and more of your money goes toward the principal.

Step-by-Step Guide: How to Manually Calculate Your Interest

While online calculators are convenient, knowing how to run the numbers manually allows you to verify lender disclosures and compare offers on the fly.

The Monthly Interest Formula

To calculate the interest portion of your first monthly payment, follow this standard financial formula:

- Divide your APR by 12 to get your monthly interest rate. (e.g., 0.06 / 12 = 0.005).

- Multiply that decimal by your remaining principal balance. (e.g., 0.005 x $30,000 = $150).

In this example, $150 of your first payment goes straight to the lender as interest. If your total monthly payment is $550, the remaining $400 is applied to reduce your principal to $29,600. For the second month, you would repeat the calculation using $29,600 as the base.

Calculating Total Interest Over the Life of the Loan

To understand the total financial impact of the loan, you can use the following steps:

- Determine your monthly payment (using an amortization formula or a provider’s quote).

- Multiply the monthly payment by the total number of months in the term.

- Subtract the original principal from that total.

For example, if you pay $500 a month for 60 months on a $25,000 loan:

- $500 x 60 = $30,000 (Total Paid)

- $30,000 – $25,000 = $5,000 (Total Interest)

The Impact of Amortization Schedules

An amortization schedule is a table that lists every payment of the loan. Each entry shows how much of the payment is interest and how much is principal. Reviewing this schedule is an eye-opening experience for many investors; it highlights how slowly equity is built in the first half of a loan term, which is particularly relevant if you plan to sell or trade in the vehicle before the loan is fully paid.

Factors That Influence Your Car Loan Interest Rates

Understanding the math is only half the battle; the other half is understanding the “why” behind the rate you are offered. Interest rates are essentially a price tag on risk.

Credit Score and Financial History

Your credit score is the primary determinant of your interest rate. Lenders categorize borrowers into “tiers” (e.g., Super Prime, Prime, Non-prime, Subprime). A borrower with a 780 score might be offered a 4% APR, while a borrower with a 600 score might face a 15% APR or higher. On a $30,000 loan, this difference in “personal financial health” can translate to over $10,000 in additional interest costs.

Loan-to-Value (LTV) Ratio

Lenders look at the value of the car versus the amount you are borrowing. If you borrow more than the car is worth (often due to rolling over debt from a previous vehicle or having a zero-down payment), you have a high LTV. High LTV loans are riskier for lenders, which often leads to higher interest rates. Keeping your LTV below 80% is a benchmark for securing more competitive financing.

Market Trends and Federal Policy

The macro-economic environment plays a significant role. When the Federal Reserve adjusts the federal funds rate, the cost for banks to borrow money changes. This trickles down to consumer products like auto loans. In a high-inflation environment, interest rates across the board will rise, making it even more critical to optimize the factors within your control, such as your credit score and down payment size.

Strategies to Minimize Interest Costs and Optimize Your Finances

Once you understand how interest is calculated, you can move from a passive borrower to an active financial manager. Use these strategies to ensure you pay as little interest as possible.

The Power of Extra Principal Payments

Since most car loans use simple interest calculated on the remaining balance, any extra payment you make goes directly toward the principal (provided you specify this with your lender). By reducing the principal faster than the schedule dictates, you “starve” the interest calculation. Even an extra $50 a month can shave months off your loan and save hundreds in interest.

Short-Term Loan Selection

While a 72-month or 84-month loan makes a luxury vehicle seem “affordable,” it is a poor financial move. Not only are the interest rates typically higher for longer terms, but the total interest paid skyrockets. Aim for a term of 48 to 60 months. This ensures you build equity in the vehicle faster than it depreciates, preventing you from becoming “upside down” on the loan.

Refinancing Opportunities

Your financial situation is not static. If you took out a loan during a period of poor credit but have spent the last 18 months improving your score, you may be eligible for refinancing. Refinancing involves taking out a new loan at a lower interest rate to pay off the old one. In the world of personal finance, this is one of the most effective ways to “correct” a past high-interest mistake.

By mastering the calculation of car loan interest, you transition from a consumer who “buys a payment” to a savvy investor who “manages a debt.” Armed with the formulas and strategic insights provided here, you can approach the dealership or the bank with confidence, knowing exactly what your money is doing and how to keep more of it in your pocket.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.