Understanding how to calculate interest for a month is a fundamental skill that empowers individuals and businesses to make informed financial decisions. Whether you’re managing personal savings, grappling with credit card debt, assessing a loan payment, or planning investments, a clear grasp of monthly interest calculations is indispensable. Interest, in its simplest form, is the cost of borrowing money or the reward for lending it. It’s the engine behind growth in savings and the silent force behind accumulating debt. This guide will demystify the process, breaking down the essential concepts and providing practical methods to calculate monthly interest across various financial scenarios.

Understanding the Fundamentals of Interest

Before diving into calculations, it’s crucial to establish a solid understanding of what interest is and the key terms associated with it. This foundation will enable you to approach any financial product with confidence and clarity.

What is Interest?

At its core, interest is a charge for the privilege of borrowing money, typically expressed as a percentage of the principal amount. From the perspective of a borrower, interest is the cost they pay for using someone else’s money. For a lender or saver, interest is the income earned for allowing someone else to use their money or for depositing funds in an interest-bearing account. This dynamic makes interest a critical component of virtually every financial transaction, from simple bank accounts to complex investment vehicles.

Key Terms in Interest Calculation

To accurately calculate interest, several key terms must be understood:

- Principal (P): This is the initial amount of money borrowed or invested. For example, if you take out a $10,000 loan, your principal is $10,000. If you deposit $5,000 into a savings account, your principal is $5,000.

- Interest Rate (R): The percentage charged on the principal over a specific period, usually expressed annually. For instance, an annual interest rate of 5% means you’ll pay or earn 5% of the principal over a year. It’s crucial to convert this percentage to a decimal for calculations (e.g., 5% becomes 0.05).

- Time (T): The duration for which the money is borrowed or invested. This is typically expressed in years for annual rates. When calculating monthly interest, time will often be represented as a fraction of a year (e.g., 1/12 for one month).

- Compounding Frequency: This refers to how often the interest is calculated and added to the principal. Common compounding frequencies include annually, semi-annually, quarterly, monthly, daily, or even continuously. The more frequently interest compounds, the faster your money grows (or your debt increases).

- Annual Percentage Rate (APR) vs. Annual Percentage Yield (APY):

- APR is the annual rate charged for borrowing or earned by an investment, expressed as a simple percentage. It typically does not factor in compounding. It’s commonly used for loans, credit cards, and mortgages.

- APY, also known as the effective annual rate, is the real rate of return earned on an investment, taking into account the effect of compounding interest. APY is typically higher than APR when compounding occurs more frequently than annually, as it reflects the “interest on interest” effect. It’s commonly used for savings accounts and certificates of deposit (CDs). Understanding the difference is vital for comparing financial products effectively.

Calculating Simple Monthly Interest

Simple interest is the most straightforward method of calculating interest, where the interest is only calculated on the original principal amount. It does not compound, meaning you don’t earn interest on previously accrued interest. While less common for long-term investments, simple interest is often used for short-term loans or specific types of credit.

The Simple Interest Formula

The formula for calculating simple interest is:

I = P × R × T

Where:

- I = Interest amount

- P = Principal amount

- R = Annual interest rate (as a decimal)

- T = Time (in years)

To calculate simple interest for a single month, you need to adjust the “Time” (T) variable accordingly. Since there are 12 months in a year, one month would be represented as 1/12 of a year.

Let’s illustrate with a couple of examples:

Example 1: Calculating Monthly Simple Interest on a Loan

Suppose you take out a short-term personal loan of $5,000 at an annual simple interest rate of 8%. You want to calculate the interest accrued for one month.

- P = $5,000

- R = 8% = 0.08

- T = 1 month = 1/12 year

I = $5,000 × 0.08 × (1/12)

I = $400 × (1/12)

I = $33.33

So, the simple interest for that month would be $33.33.

Example 2: Calculating Monthly Simple Interest on Savings (Hypothetical)

While most savings accounts use compound interest, for illustrative purposes, imagine a savings bond with a principal of $1,000 and an annual simple interest rate of 2%.

- P = $1,000

- R = 2% = 0.02

- T = 1 month = 1/12 year

I = $1,000 × 0.02 × (1/12)

I = $20 × (1/12)

I = $1.67

The simple interest earned for one month would be $1.67.

Step-by-Step Guide for Simple Monthly Interest

- Identify the Principal (P): Determine the initial amount of money involved.

- Determine the Annual Interest Rate (R): Find the annual percentage rate and convert it to a decimal (divide by 100).

- Set the Time (T): For a single month, this will always be 1/12 (or approximately 0.0833). If calculating for multiple months, it would be

number of months / 12. - Apply the Formula: Multiply P, R, and T together.

- Interpret the Result: The calculated value is the interest amount for the specified month(s).

Simple interest is straightforward, but it’s important to confirm whether a financial product uses simple or compound interest, as the latter can significantly alter the total interest paid or earned over time.

Calculating Compound Monthly Interest

Compound interest is often referred to as “interest on interest” and is a powerful force in finance. Unlike simple interest, compound interest is calculated on the initial principal and also on all the accumulated interest from previous periods. This means your money grows faster (or your debt increases faster) over time, as the base for the interest calculation keeps expanding.

The Power of Compounding

The magic of compounding lies in its ability to accelerate wealth accumulation or debt growth. For investments, the more frequently interest is compounded, the faster your money grows. For loans and credit cards, the opposite is true: frequent compounding can quickly inflate your outstanding balance if not managed responsibly. Most long-term savings accounts, investments, and loans (like mortgages or car loans) utilize compound interest.

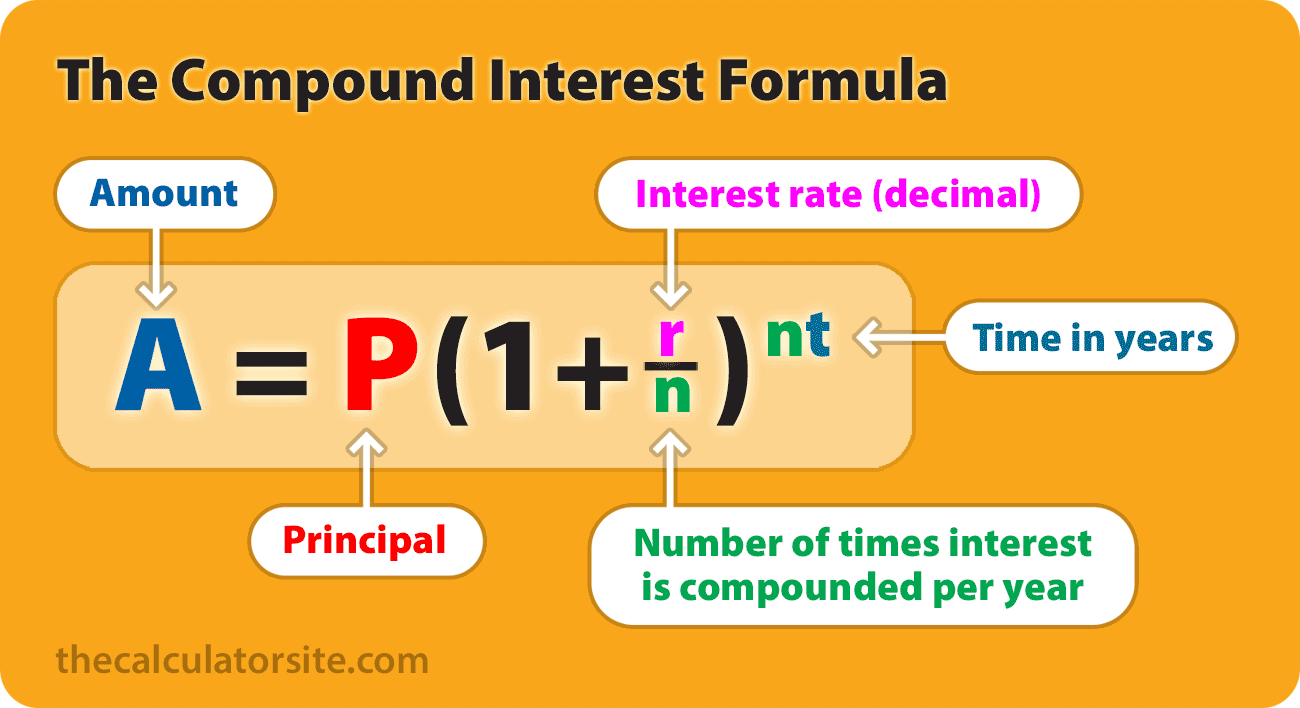

The general formula for compound interest is:

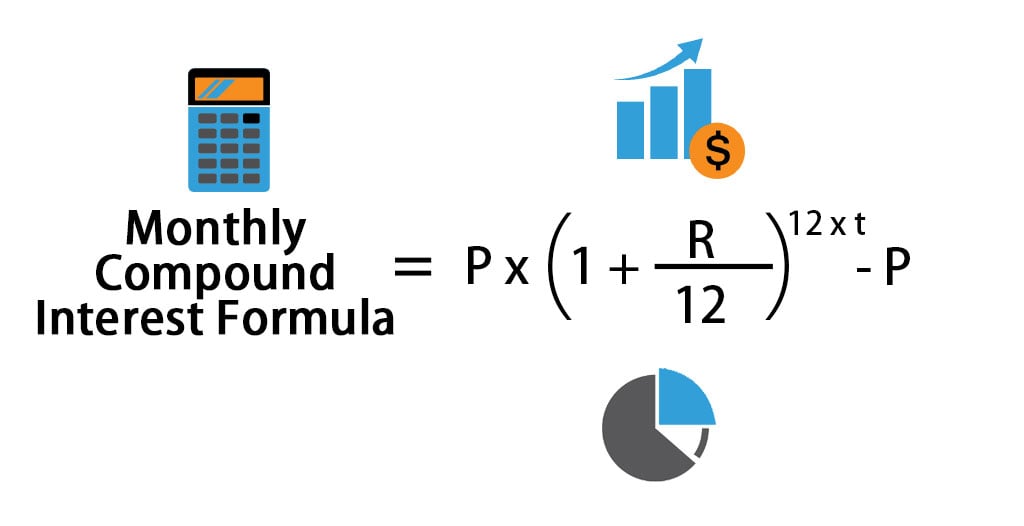

A = P (1 + r/n)^(nt)

Where:

- A = The future value of the investment/loan, including interest

- P = The principal investment amount (the initial deposit or loan amount)

- r = The annual interest rate (as a decimal)

- n = The number of times that interest is compounded per year

- t = The number of years the money is invested or borrowed for

Monthly Compounding Scenarios

When interest is compounded monthly, n in the formula becomes 12. This means that every month, interest is calculated and added to the principal, and the next month’s interest is calculated on this new, larger principal.

1. Savings Accounts (Compounded Monthly):

Most high-yield savings accounts compound interest monthly. To find the interest earned for a single month, you can calculate the balance at the start of the month and then again at the end of the month, subtracting the two.

Alternatively, a simpler way to find the interest earned for a single month on the current balance is:

Monthly Interest = (Current Principal Balance) × (Annual Interest Rate / 12)

Let’s say you have $10,000 in a savings account with an annual interest rate of 3%, compounded monthly.

- Current Principal Balance (P) = $10,000

- Annual Interest Rate (r) = 3% = 0.03

- Number of Compounding Periods per Year (n) = 12

Monthly Interest Rate = 0.03 / 12 = 0.0025

Interest for the month = $10,000 × 0.0025 = $25.00

So, for that month, you would earn $25.00 in interest. Your new principal for the next month would be $10,025.00.

2. Credit Cards:

Credit card interest is often calculated on an “average daily balance” and usually compounded daily or monthly. To find the interest for a billing cycle (typically a month), the card issuer will usually take your average daily balance and multiply it by your daily periodic rate (APR divided by 365, or sometimes 360) for each day in the billing cycle.

- Assume an average daily balance of $1,500 for a month.

- APR = 18% = 0.18

- Number of days in the billing cycle = 30

Daily Periodic Rate = 0.18 / 365 = 0.00049315 (approximately)

Interest for the month = $1,500 (average daily balance) × 0.00049315 × 30 days

Interest for the month = $22.19

This calculation shows why even small credit card balances can accumulate interest quickly if not paid off.

3. Loans (e.g., Mortgages, Car Loans):

For amortizing loans, where you make regular payments that cover both principal and interest, calculating the interest for a single month involves a slightly different approach. The interest portion of your monthly payment is calculated based on the outstanding principal balance at the beginning of that month.

Let’s consider a car loan:

- Outstanding Principal Balance at the start of the month = $15,000

- Annual Interest Rate (APR) = 6% = 0.06

Monthly Interest Rate = 0.06 / 12 = 0.005

Interest portion of payment for the month = $15,000 × 0.005 = $75.00

This $75 is the amount of your monthly payment that goes towards interest. The remainder of your payment (minus any fees) goes towards reducing the principal. As the principal reduces with each payment, the interest portion of future payments will also decrease.

Step-by-Step for Compound Monthly Interest (for a single month)

- Identify the Current Principal Balance (P): This is the balance at the beginning of the month for which you want to calculate interest.

- Determine the Annual Interest Rate (r): Convert the annual percentage rate to a decimal.

- Calculate the Monthly Interest Rate: Divide the annual interest rate (r) by 12 (since interest is compounded monthly).

- Multiply: Multiply the Current Principal Balance by the Monthly Interest Rate.

- Result: This gives you the interest amount accrued for that specific month. Add this to your principal to find the new balance for the next month if no payments or withdrawals occur.

For calculating the total amount over multiple compounding periods, you would use the full compound interest formula A = P (1 + r/n)^(nt). For example, to find out how much $10,000 would grow to in 5 years at 3% annual interest compounded monthly:

A = 10,000 * (1 + 0.03/12)^(12*5)

A = 10,000 * (1.0025)^60

A = 10,000 * 1.161616...

A = $11,616.17

The total interest earned over 5 years would be $1,616.17.

Practical Applications and Tools for Monthly Interest Calculations

The ability to accurately calculate monthly interest extends beyond academic understanding; it has direct and significant implications for your financial well-being. From managing debt to maximizing savings, practical application of these calculations is key.

Why Accuracy Matters

- Budgeting and Debt Management: Knowing how much interest you’ll pay each month allows you to create realistic budgets, prioritize high-interest debts, and understand the true cost of borrowing. It can motivate you to pay down credit card balances faster or make extra loan payments to save on interest over the long term.

- Investment and Savings Planning: For savers, understanding monthly interest helps in projecting growth and comparing different savings products. Knowing the precise monthly accumulation helps in setting financial goals, such as saving for a down payment or retirement, with greater accuracy.

- Avoiding Surprises: Unexpected interest charges can derail financial plans. By proactively calculating and understanding your monthly interest obligations or earnings, you can avoid unwelcome surprises and maintain better control over your money.

- Informed Decision-Making: Whether taking out a loan, opening a savings account, or making an investment, an accurate understanding of interest allows you to compare options effectively and choose the financial products that best align with your goals.

Online Calculators and Financial Software

While manual calculations are excellent for understanding the mechanics, a plethora of tools are available to assist with complex or repetitive interest calculations:

- Online Loan Calculators: These tools can quickly determine monthly payments, total interest paid over the life of a loan, and amortization schedules, which show how much principal and interest you pay each month.

- Savings Calculators: Ideal for projecting the growth of your investments over time, considering various interest rates, compounding frequencies, and additional contributions.

- Credit Card Interest Calculators: These help you understand how quickly interest can accumulate on outstanding balances and the impact of minimum payments versus paying more.

- Spreadsheet Software (Excel, Google Sheets): Offers powerful functions like

PMT(for loan payments),FV(future value of an investment), andIPMT(interest portion of a payment) that automate complex calculations and allow for scenario analysis. These are invaluable for creating personalized financial models. - Financial Planning Apps: Many personal finance apps now include built-in calculators or integrate with financial tools that can help you visualize the impact of interest on your finances.

Key Considerations and Tips

- Always Check the Compounding Frequency: This is perhaps the most critical factor. Daily, monthly, quarterly, or annually can drastically change the total interest. Don’t assume; always confirm.

- Understand APR vs. APY: Remember that APY (for savings) reflects the true annual return considering compounding, making it a better metric for comparison than APR (for loans) which usually represents the simple annual rate.

- Consider Fees: Interest is not the only cost associated with financial products. Account maintenance fees, late payment fees, origination fees, and other charges can impact the overall cost or return. Factor these into your financial planning.

- The Impact of Payments/Withdrawals: For loans, making payments reduces the principal, thereby reducing the interest calculated for subsequent periods. For savings, withdrawals decrease the principal, lowering future interest earnings. Your interest calculations should always be based on the current outstanding principal.

- Read the Fine Print: Financial agreements can be complex. Always take the time to read and understand the terms and conditions, especially regarding interest rates, compounding methods, and any penalties or bonuses.

Conclusion

Calculating interest for a month is a fundamental financial literacy skill that empowers you to gain control over your money. Whether you’re trying to escape debt, grow your savings, or make a significant purchase, understanding how simple and compound interest works on a monthly basis is non-negotiable.

By familiarizing yourself with the key terms, mastering the simple and compound interest formulas, and utilizing available financial tools, you can accurately forecast your financial future. This knowledge transforms you from a passive participant in financial transactions to an active, informed decision-maker. Take the time to apply these calculations to your own financial situation – it’s an investment in your financial health that will pay dividends for years to come.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.