In the realm of personal finance and global economics, few acronyms carry as much weight as CPI. The Consumer Price Index is more than just a dry statistical figure released by government agencies; it is the primary thermometer used to measure the heat of inflation. For the individual investor, the business owner, or the household budgeter, understanding how to calculate CPI—and interpreting what those numbers signify—is essential for maintaining financial health.

When the CPI rises, your dollar buys less. When it stabilizes, your financial planning becomes more predictable. This guide provides an in-depth exploration of the mechanics behind the Consumer Price Index, the mathematical formulas required to calculate it, and how you can use this data to make informed decisions about your money.

Understanding the Fundamentals of the Consumer Price Index

Before diving into the mathematics, it is crucial to define what the Consumer Price Index actually represents. At its core, the CPI measures the average change over time in the prices paid by urban consumers for a representative “market basket” of consumer goods and services.

What is the “Market Basket”?

The “market basket” is a metaphorical collection of products and services that an average household purchases. To ensure the CPI is accurate, economists categorize these items into groups such as food and beverages, housing, apparel, transportation, medical care, recreation, and education. By tracking the price of this specific basket month after month, year after year, we can see exactly how much more (or less) expensive it is to maintain a standard of living.

Why CPI Matters for Your Wallet

For the average person, the CPI is the most visible indicator of inflation. It dictates the “real” value of your savings. If your bank account earns 2% interest but the CPI indicates inflation is at 5%, you are effectively losing 3% of your purchasing power annually. Furthermore, the CPI often determines Cost of Living Adjustments (COLA) for Social Security recipients and affects the interest rates set by central banks, which in turn influences your mortgage and credit card rates.

The Step-by-Step Formula for Calculating CPI

Calculating the CPI involves comparing the cost of a fixed set of goods in a given year to the cost of that same set of goods in a designated “base year.” This comparison allows us to see price movements relative to a stable point in time.

Step 1: Selecting the Market Basket and Finding Prices

The first step is identifying the items to be included. For a simplified personal calculation, you might choose ten items you buy every week. For the official government CPI, thousands of items are tracked. Once the basket is set, you must find the total cost of these items for two periods: the base period and the current period.

Step 2: Identifying the Base Year

The base year serves as the benchmark. In index calculations, the base year is always assigned a value of 100. This makes it easy to see percentage changes. If the current year’s index is 110, it means prices have risen 10% since the base year.

Step 3: The Mathematical Formula

The standard formula for calculating the Consumer Price Index is:

CPI = (Cost of Market Basket in Current Year / Cost of Market Basket in Base Year) × 100

For example, if the cost of a basket of goods in the base year (2020) was $500, and the cost of that same basket in the current year (2024) is $575, the calculation would look like this:

- CPI = ($575 / $500) × 100

- CPI = 1.15 × 100

- CPI = 115

This result tells us that there has been a 15% increase in the price level since the base year.

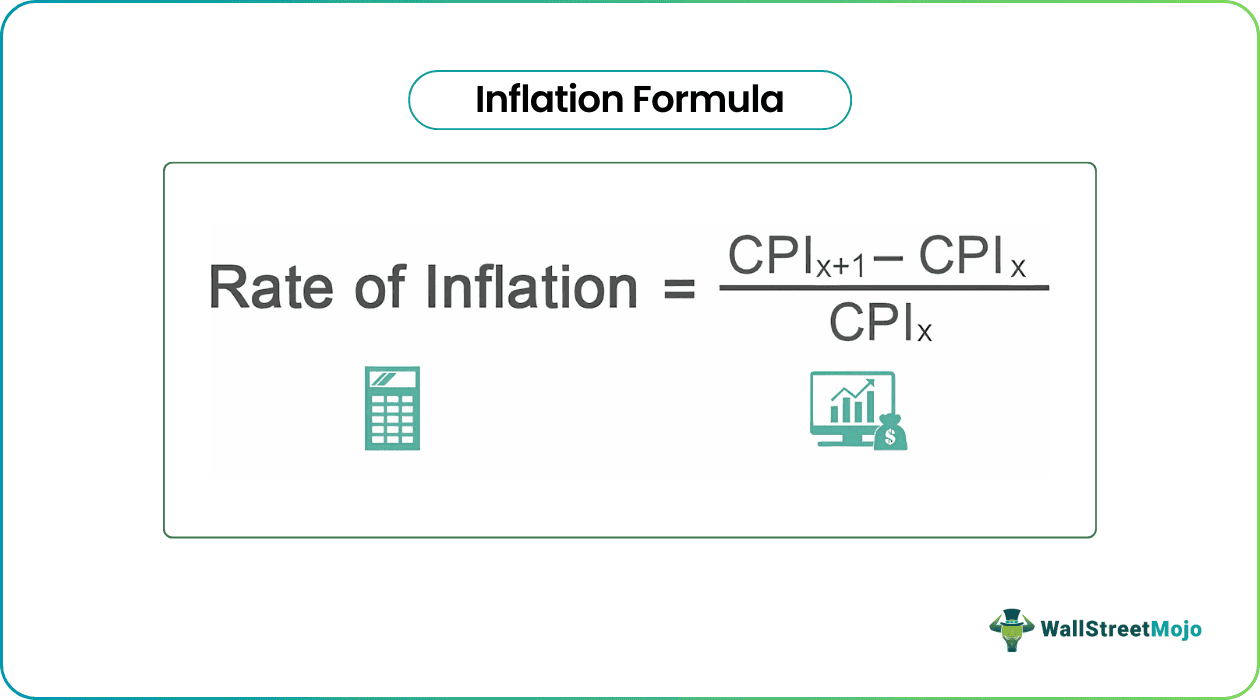

Calculating the Inflation Rate

While the CPI itself is an index number, the “Inflation Rate” is the percentage change between two specific points in time. To find the inflation rate between two years, use this formula:

Inflation Rate = [(CPI in Year 2 – CPI in Year 1) / CPI in Year 1] × 100

If the CPI last year was 110 and this year it is 115, the inflation rate is approximately 4.54%.

Analyzing Real-World Implications of CPI Changes

Understanding the calculation is only half the battle; the true value lies in interpreting the data to safeguard your personal finances.

CPI vs. Your Personal Inflation Rate

It is important to note that the official CPI is an average. It may not perfectly reflect your personal financial reality. For instance, if the CPI rises primarily due to an increase in the cost of gasoline, but you live in a city and use public transportation, your “personal inflation rate” may be lower than the national average. Conversely, if you have high medical expenses and healthcare costs are skyrocketing faster than the general index, your personal cost of living is rising faster than the headline number suggests.

How the Federal Reserve Uses CPI

In the United States, the Federal Reserve monitors the CPI (and the related Personal Consumption Expenditures price index) to decide on monetary policy. When CPI readings are too high, the Fed often raises interest rates to “cool down” the economy and curb inflation. For you, this means higher borrowing costs but potentially better returns on high-yield savings accounts and Certificates of Deposit (CDs). Monitoring the CPI can help you anticipate whether interest rates are likely to rise or fall in the coming months.

How CPI Influences Your Investment and Savings Strategy

For those focused on building wealth, the CPI is a critical metric for determining “real” versus “nominal” returns.

Protecting Wealth from Inflation

When inflation is high (as indicated by a rising CPI), holding large amounts of cash is generally a losing strategy. The purchasing power of that cash evaporates over time. Investors often look toward “inflation hedges”—assets that historically maintain or increase their value when the CPI rises. These may include:

- Real Estate: Property values and rents often climb alongside inflation.

- Commodities: Prices for raw materials like gold, oil, and agricultural products frequently rise when the currency devalues.

- TIPS (Treasury Inflation-Protected Securities): These are government bonds specifically designed to increase in value in line with the CPI.

Calculating Inflation-Adjusted Returns

To know if your investments are actually growing, you must subtract the inflation rate from your nominal return. This is known as the Real Rate of Return.

Real Return = Nominal Return – Inflation Rate

If your stock portfolio gained 8% this year, but the CPI showed an inflation rate of 6%, your real gain is only 2%. Professional investors use this calculation to ensure they aren’t just running in place while the cost of living moves forward.

Limitations and Nuances of the CPI Model

While the CPI is a powerful tool, it is not without its flaws. Understanding these limitations prevents you from over-relying on a single number for your entire financial strategy.

Substitution Bias

The CPI calculation often assumes that the “market basket” remains fixed. However, in the real world, consumers are rational. If the price of beef rises significantly, many consumers will substitute it with chicken. Traditional CPI formulas may overstate inflation because they don’t always account for these consumer shifts toward cheaper alternatives.

Quality Changes and New Products

A smartphone today costs more than a basic flip phone did fifteen years ago, but the smartphone provides significantly more value and utility. If the price of a product rises because the quality has improved, is that truly “inflation”? Economists use “hedonic adjustment” to try to account for this, but it remains a subjective and complicated part of the calculation.

Furthermore, the CPI can be slow to include new technology or services (like streaming platforms or ridesharing) that may eventually lower the overall cost of living by replacing more expensive traditional services.

Conclusion: Mastering the Math of Money

Calculating the CPI is a fundamental skill for anyone serious about mastering their financial future. By understanding the relationship between the cost of a market basket and the resulting index number, you gain a clearer view of the economic forces at play.

Whether you are negotiating a salary raise, choosing between investment vehicles, or simply trying to understand why your grocery bill has climbed, the CPI provides the objective data necessary to navigate an inflationary environment. While the headline figures provide the “big picture,” applying these calculations to your own spending habits will allow you to protect your purchasing power and ensure that your money continues to work as hard for you as you do for it.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.