Compounding is often hailed as the “eighth wonder of the world” by Albert Einstein, and for good reason. It’s the process by which an asset’s earnings, from either capital gains or interest, are reinvested to generate additional earnings over time. This concept is fundamental to personal finance, investing, and wealth creation, allowing your money to grow exponentially. Understanding how to calculate compounding is not just an academic exercise; it’s a critical skill for anyone looking to build financial security, plan for retirement, or grow their investments effectively. This article will demystify the mechanics of compounding, offering practical methods and insights into harnessing its immense power.

Understanding the Basics of Compounding

Before diving into calculations, it’s crucial to grasp the core principles that make compounding so potent. At its heart, compounding is about earning returns on your initial investment and on the accumulated returns from previous periods.

What is Compound Interest? Simple vs. Compound

The simplest form of interest is simple interest, where interest is calculated only on the principal amount. For example, if you invest $1,000 at 5% simple interest, you earn $50 each year, and after 10 years, you’ll have earned $500 in interest ($1,000 + $500 = $1,500).

Compound interest, however, takes this a step further. It calculates interest on the principal plus any accumulated interest from previous periods. Using the same example: if you invest $1,000 at 5% compound interest annually, in year one you earn $50. In year two, you earn 5% on $1,050 (your principal plus first-year interest), which is $52.50. This seemingly small difference quickly snowballs, making a profound impact over time. The key differentiator is that your base for interest calculation grows with each compounding period.

The Power of Time and Interest Rate

Two primary variables amplify the effects of compounding: time and the interest rate. The longer your money is invested, the more periods it has to compound, and thus, the greater the exponential growth. Even a modest interest rate, when given sufficient time, can lead to substantial wealth accumulation. Conversely, a higher interest rate can accelerate growth significantly, even over shorter periods. This dynamic interplay underscores the importance of starting to invest early and seeking reasonable, consistent returns. Early investment means your money has more time to “work for you,” leveraging compounding to its fullest potential.

Key Variables in Compounding

To calculate compounding accurately, you need to identify several key variables:

- Principal (P): The initial amount of money invested or loaned.

- Interest Rate (r): The annual rate of interest, expressed as a decimal (e.g., 5% is 0.05).

- Number of Compounding Periods per Year (n): How frequently the interest is calculated and added to the principal (e.g., annually n=1, semi-annually n=2, quarterly n=4, monthly n=12, daily n=365).

- Time (t): The number of years the money is invested or borrowed for.

- Future Value (A): The total amount of money after a specified period, including both principal and accumulated interest. This is what we typically aim to calculate.

These variables form the bedrock of all compounding calculations, from simple estimations to complex financial models.

Simple Methods for Calculating Compounding

While the formal compound interest formula can look intimidating, there are several straightforward ways to understand and estimate the power of compounding. These methods are particularly useful for quick mental calculations or for gaining an intuitive feel for how your money grows.

Manual Calculation: Step-by-Step Approach

For shorter periods or to truly grasp the mechanics, a step-by-step manual calculation can be incredibly insightful. Let’s say you invest $1,000 at an annual compound interest rate of 7% for three years.

- Year 1:

- Starting Balance: $1,000

- Interest Earned: $1,000 * 0.07 = $70

- Ending Balance: $1,000 + $70 = $1,070

- Year 2:

- Starting Balance: $1,070

- Interest Earned: $1,070 * 0.07 = $74.90

- Ending Balance: $1,070 + $74.90 = $1,144.90

- Year 3:

- Starting Balance: $1,144.90

- Interest Earned: $1,144.90 * 0.07 = $80.14

- Ending Balance: $1,144.90 + $80.14 = $1,225.04

After three years, your initial $1,000 has grown to $1,225.04. This manual process clearly illustrates how the interest earned in one period becomes part of the principal for the next, driving exponential growth. While effective for short periods, this method quickly becomes cumbersome for longer investment horizons or frequent compounding periods.

The Rule of 72: A Quick Estimation Tool

The Rule of 72 is a simple and powerful mental math trick used to estimate the number of years required to double an investment at a fixed annual rate of return. It’s an approximation, but it provides a surprisingly accurate benchmark for financial planning.

The rule states:

Years to Double = 72 / Annual Interest Rate (as a percentage)

For instance, if your investment earns 6% annually:

Years to Double = 72 / 6 = 12 years.

So, an investment at 6% interest will roughly double in 12 years.

If you want to know what interest rate you need to double your money in a certain number of years, you can rearrange the formula:

Interest Rate = 72 / Years to Double

If you want to double your money in 8 years:

Interest Rate = 72 / 8 = 9%.

You would need an annual return of approximately 9% to double your investment in 8 years.

The Rule of 72 is invaluable for quick comparisons and understanding the long-term implications of different investment returns without needing a calculator. It highlights the significant impact of even small differences in interest rates over time.

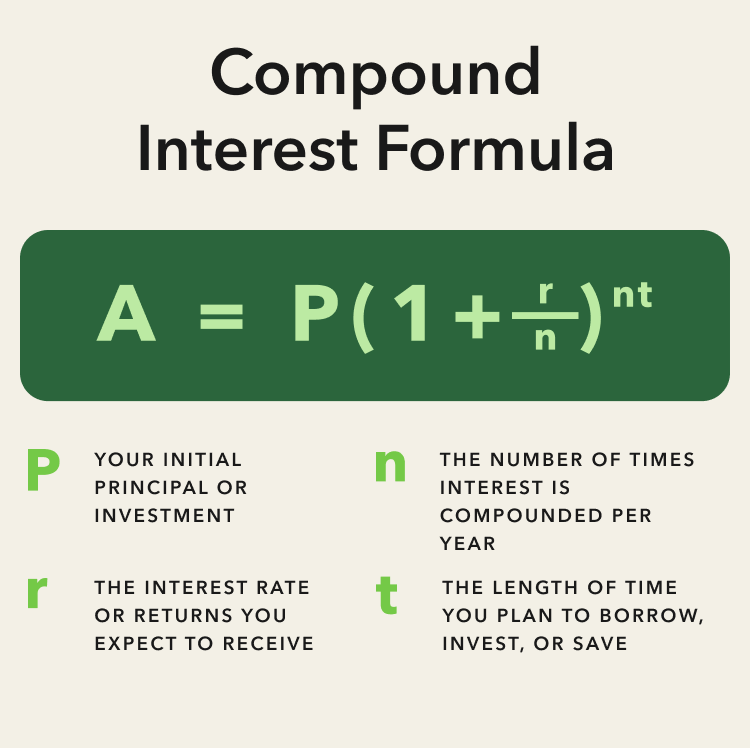

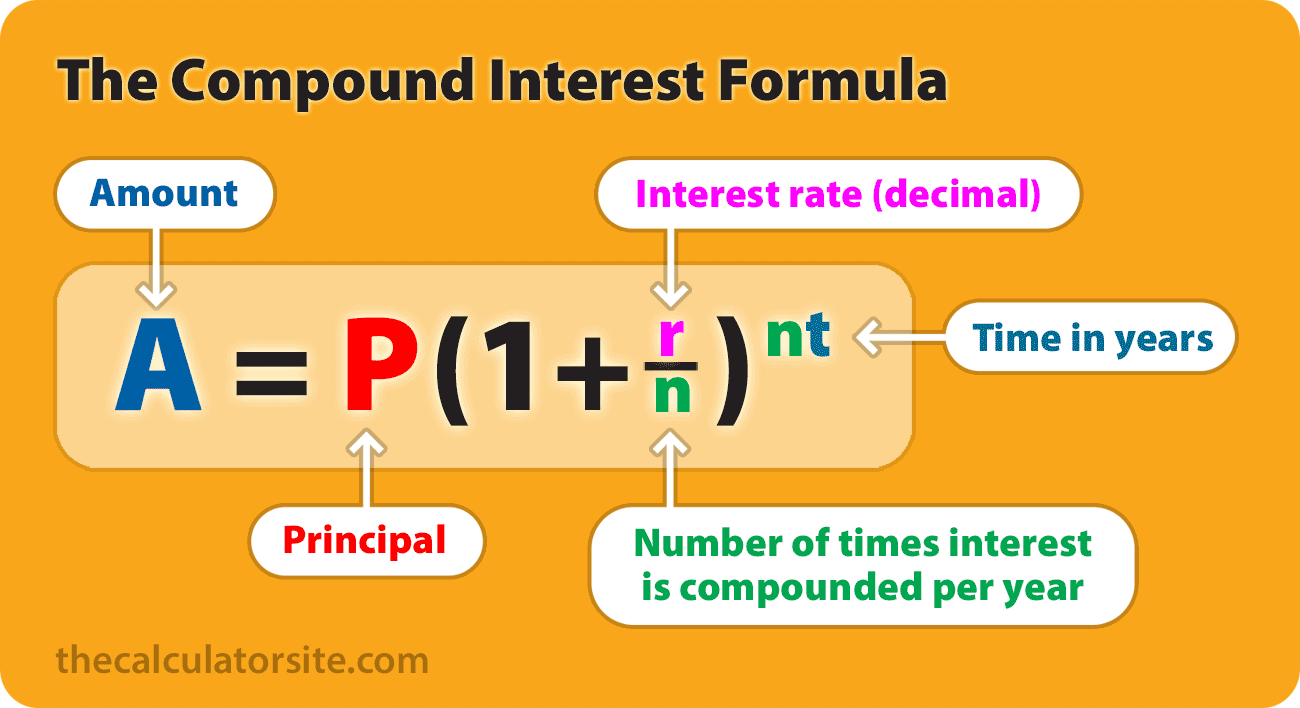

The Compound Interest Formula Explained

For precise calculations, especially for varying compounding frequencies and longer durations, the standard compound interest formula is indispensable. This formula provides the future value of an investment, taking into account all the variables discussed earlier.

Deconstructing the Formula

The formula for calculating compound interest is:

A = P(1 + r/n)^(nt)

Where:

- A = The future value of the investment/loan, including interest

- P = The principal investment amount (the initial deposit or loan amount)

- r = The annual interest rate (as a decimal)

- n = The number of times that interest is compounded per year

- t = The number of years the money is invested or borrowed for

Let’s break down each part of the formula:

- (1 + r/n): This represents the growth factor for a single compounding period.

r/ncalculates the interest rate per compounding period. Adding1accounts for the original principal. - ^(nt): This exponent represents the total number of compounding periods over the entire investment horizon.

n(periods per year) multiplied byt(total years) gives you the total count.

Understanding each component helps in not just plugging in numbers but also comprehending the underlying financial mechanics.

Practical Application with an Example

Let’s apply the formula to a real-world scenario. Suppose you invest $5,000 at an annual interest rate of 8%, compounded quarterly, for 10 years.

- P = $5,000

- r = 0.08 (8%)

- n = 4 (compounded quarterly)

- t = 10 years

Now, plug these values into the formula:

A = $5,000 * (1 + 0.08/4)^(4*10)

A = $5,000 * (1 + 0.02)^(40)

A = $5,000 * (1.02)^(40)

To solve (1.02)^40, you’ll typically use a calculator:

(1.02)^40 ≈ 2.20804

A = $5,000 * 2.20804

A ≈ $11,040.20

So, after 10 years, your initial $5,000 investment would grow to approximately $11,040.20 with quarterly compounding. The total interest earned is $11,040.20 – $5,000 = $6,040.20.

Understanding Frequency of Compounding

The frequency of compounding (n) significantly impacts the final amount. The more frequently interest is compounded, the greater the effect, as interest starts earning interest sooner.

- Annually (n=1): Interest is calculated once a year.

- Semi-annually (n=2): Interest is calculated twice a year.

- Quarterly (n=4): Interest is calculated four times a year.

- Monthly (n=12): Interest is calculated twelve times a year.

- Daily (n=365): Interest is calculated daily.

While increasing compounding frequency boosts returns, the difference becomes less dramatic as n gets very large. For example, the difference between monthly and daily compounding is often negligible for most practical purposes compared to the difference between annual and monthly. Nevertheless, for large sums and long periods, even minor differences in compounding frequency can accumulate into substantial amounts.

Leveraging Financial Tools for Compounding Calculations

While understanding the formula and manual steps is essential, modern financial tools make calculating compounding simple and efficient. These tools eliminate human error and allow for rapid scenario analysis.

Online Compound Interest Calculators

A plethora of free online compound interest calculators are available from financial institutions, investment websites, and educational platforms. These tools typically require you to input the principal, interest rate, compounding frequency, and time period, then instantly provide the future value and total interest earned. Many also offer advanced features, such as factoring in additional periodic contributions (e.g., monthly deposits), allowing you to project the growth of your savings with ongoing contributions. They are excellent for quick calculations and exploring various investment scenarios without needing to manually input formulas.

Spreadsheet Software (Excel/Google Sheets)

Spreadsheet programs like Microsoft Excel or Google Sheets are incredibly powerful for more detailed and customized compounding calculations. They allow you to build models, compare different investment strategies side-by-side, and visualize growth over time.

The primary function used is FV (Future Value):

=FV(rate, nper, pmt, [pv], [type])

rate: The interest rate per period (e.g., annual rate / n).nper: The total number of payment periods in an annuity (t * n).pmt: The payment made each period (for regular contributions; use 0 if none).pv: The present value, or the principal (enter as a negative number for an investment).type: Optional, specifies when payments are due (0 for end of period, 1 for beginning).

For a simple compound interest calculation with no additional payments:

=FV(annual_rate/n, n*years, 0, -principal)

Using a spreadsheet gives you the flexibility to adjust variables easily, create charts, and integrate these calculations into broader financial plans. It’s an indispensable tool for serious financial planning.

Financial Calculators and Apps

Dedicated financial calculators (like the HP 12c or Texas Instruments BA II Plus) are staples for finance professionals, offering specialized functions for time value of money calculations, including compound interest. These devices are robust and don’t require an internet connection, making them reliable for on-the-go calculations.

Furthermore, many personal finance apps available on smartphones now include integrated compound interest calculators, often with user-friendly interfaces and visualization tools. These apps can sync with your investment accounts, providing a holistic view of your financial growth and the impact of compounding on your portfolio.

Strategic Implications of Compounding for Financial Growth

Understanding how to calculate compounding is only the first step; applying this knowledge strategically is where true financial advantage is gained. Compounding is more than just a mathematical formula; it’s a powerful principle that underpins long-term wealth creation.

The Importance of Early Investment

The single most significant strategic implication of compounding is the paramount importance of starting early. Because time is a crucial multiplier in the compound interest formula, even small investments made early in life can grow into substantial sums over decades. A person who starts investing $200 per month at age 25 for 10 years (then stops, letting it compound) will likely accumulate more wealth by retirement than someone who starts investing $200 per month at age 35 and continues for 30 years, assuming the same rate of return. The initial investor’s money simply has more years to compound, illustrating the concept of “time in the market” being more important than “timing the market.” This highlights the lost opportunity cost of delaying investment.

Reinvesting Returns for Maximum Impact

For compounding to work its magic fully, the returns generated must be reinvested. If you consistently withdraw the interest or dividends your investments earn, you negate the compounding effect. Reinvesting means that your earnings become part of your principal, which then earns its own returns, creating an ever-expanding base for future growth. This strategy is particularly effective in long-term investment vehicles like retirement accounts (401k, IRA) and growth-oriented mutual funds or ETFs, where dividends and capital gains are often automatically reinvested, allowing for seamless compound growth.

Compounding Beyond Interest: Skills and Habits

The principle of compounding isn’t limited to financial interest alone. It can be applied metaphorically to other areas of life that contribute to financial well-being.

- Compounding Knowledge: Continuously learning new skills or deepening existing ones builds expertise over time, leading to greater career opportunities and earning potential. Each new piece of knowledge adds to your existing base, amplifying your capabilities.

- Compounding Habits: Small, positive daily habits, whether in saving, budgeting, or health, accumulate over time to create significant long-term benefits. Consistently saving a small amount, even if it seems insignificant, builds up substantial savings over years. Similarly, consistent healthy choices compound into better long-term health, which can reduce future medical expenses.

- Compounding Networks: Nurturing relationships and building a professional network consistently can lead to unforeseen opportunities, collaborations, and career advancement, with each connection potentially opening doors to many more.

By applying the compounding mindset to various aspects of life, individuals can foster growth not just in their investment portfolios but also in their personal and professional development, ultimately contributing to a richer and more secure financial future.

Conclusion

Compounding is undeniably one of the most powerful forces in finance, transforming modest investments into significant wealth given enough time and a consistent rate of return. From manual step-by-step calculations and the quick estimation of the Rule of 72 to the precision of the compound interest formula and the efficiency of financial tools, the methods for calculating compounding are accessible to everyone. More importantly, understanding and strategically applying the principles of compounding – particularly through early investment and reinvesting returns – is paramount for achieving long-term financial goals. Embrace the magic of compounding, make it a cornerstone of your financial strategy, and watch your wealth grow exponentially over time.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.