Compound interest is often referred to as the “eighth wonder of the world” by financial experts and enthusiasts alike. Its power lies in its ability to turn modest, consistent savings into substantial wealth over time. Unlike simple interest, which is calculated only on the initial amount of money deposited, compound interest is calculated on the initial principal and also on the accumulated interest of previous periods. Understanding how to calculate and leverage this mathematical phenomenon is perhaps the most critical skill in personal finance and long-term investing.

Understanding the Fundamentals of Compound Interest

Before diving into the complex formulas, it is essential to grasp the conceptual framework of how compounding works. At its core, compounding is the process where the value of an investment increases because the earnings on an investment, both capital gains and interest, earn interest as time passes.

Simple vs. Compound Interest: What’s the Difference?

To appreciate compound interest, one must first understand simple interest. Simple interest is calculated solely on the principal amount. For example, if you invest $1,000 at a 5% simple interest rate per year, you will earn $50 every year. After ten years, you would have $1,500.

In contrast, compound interest applies the interest rate to the new balance at the end of each period. Using the same $1,000 at a 5% interest rate compounded annually, you would earn $50 in the first year. However, in the second year, the 5% is calculated on $1,050, resulting in $52.50 of interest. While the difference seems negligible in the first few years, the gap between simple and compound interest widens exponentially over decades.

The “Magic” of the Snowball Effect

Financial advisors often use the analogy of a snowball rolling down a hill. Initially, the snowball is small and picks up very little snow. However, as it moves further down the hill, its surface area increases, allowing it to pick up more snow with every rotation. By the time it reaches the bottom, it has grown into a massive boulder. This is exactly how your money behaves in a compounding environment. The “snow” is your interest, and the “hill” is the time horizon of your investment.

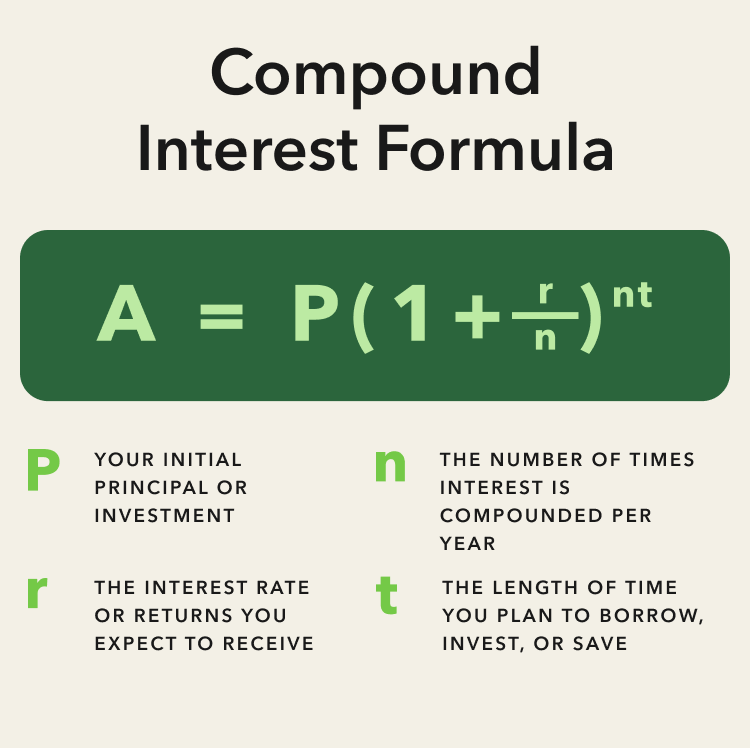

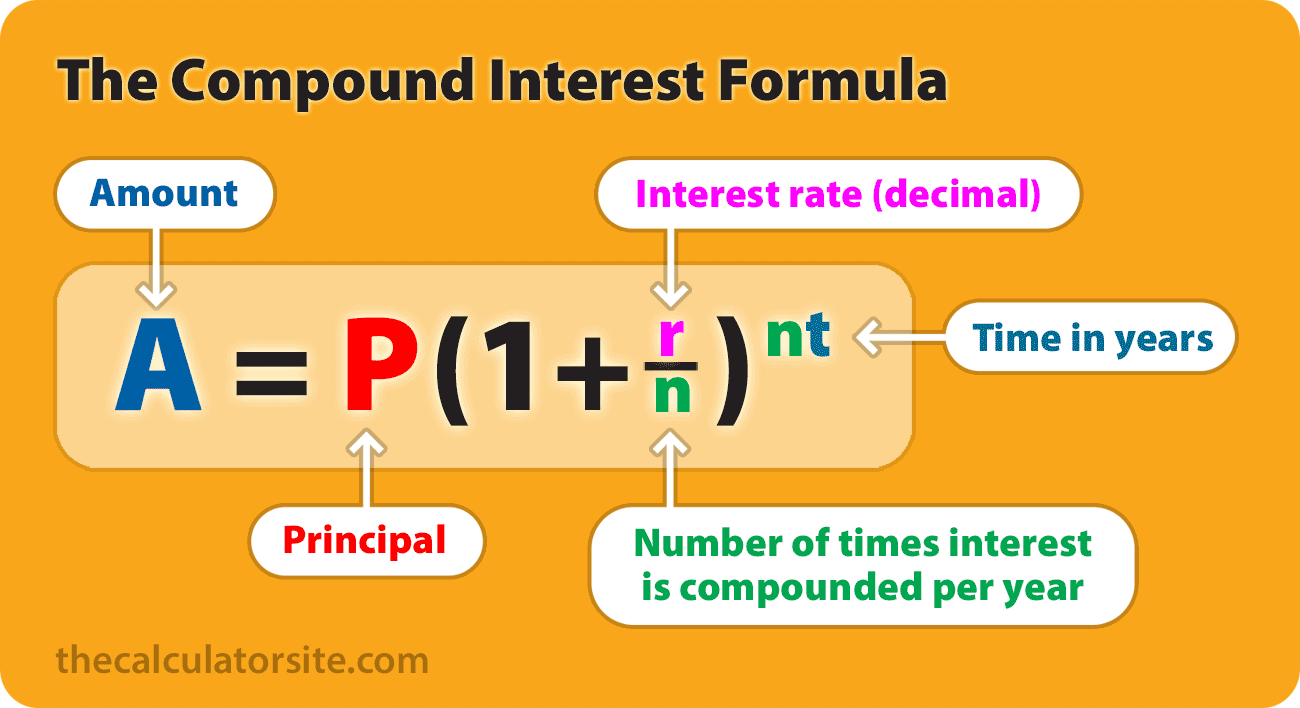

The Mathematics Behind the Growth: Breaking Down the Formula

While online calculators are readily available, knowing how to perform the calculation manually provides a deeper insight into how different variables affect your financial outcome. The standard formula for compound interest is:

A = P (1 + r/n)^(nt)

Identifying the Key Variables

To use the formula effectively, you must understand what each letter represents:

- A (Total Amount): This is the final amount of money you will have after the interest has been compounded over the specified time.

- P (Principal): This is the initial sum of money you start with—your seed capital.

- r (Annual Interest Rate): This is the interest rate expressed as a decimal (e.g., 5% becomes 0.05).

- n (Compounding Frequency): This represents how many times the interest is compounded per year (e.g., 12 for monthly, 4 for quarterly).

- t (Time): This is the number of years the money is left to grow.

Step-by-Step Calculation Examples

Let’s look at a practical scenario. Suppose you invest $5,000 in a high-yield savings account with an annual interest rate of 4%, and the interest is compounded monthly for 10 years.

- Identify variables: P = 5,000; r = 0.04; n = 12; t = 10.

- Plug into the formula: A = 5,000 (1 + 0.04/12)^(12*10).

- Solve the parenthesis: 0.04 divided by 12 is approximately 0.00333. Adding 1 gives 1.00333.

- Calculate the exponent: 12 times 10 is 120.

- Calculate the power: (1.00333)^120 is approximately 1.4908.

- Multiply by the principal: 5,000 * 1.4908 = $7,454.

In this scenario, your $5,000 grew to $7,454, earning you $2,454 in interest without you ever adding another penny.

The Rule of 72: A Shortcut for Estimates

For those who want a quick mental estimate without a calculator, the “Rule of 72” is an invaluable tool. By dividing 72 by your annual interest rate, you can determine approximately how many years it will take for your investment to double. For instance, if you have an 8% return, 72/8 = 9. It will take roughly nine years for your money to double.

Factors That Influence Your Financial Gains

Several variables can drastically change the trajectory of your wealth. Understanding these factors allows you to optimize your savings strategy.

The Impact of Compounding Frequency

The value of “n” in our formula is more significant than many realize. The more frequently interest is compounded, the higher the final amount. Interest can be compounded annually, semi-annually, quarterly, monthly, or even daily.

If you have $10,000 at 10% interest:

- Compounded Annually: You have $11,000 after one year.

- Compounded Daily: You have approximately $11,051.71 after one year.

While the $51.71 difference seems small, when applied to hundreds of thousands of dollars over thirty years, the frequency of compounding can result in a difference of tens of thousands of dollars.

The Critical Role of Time and Consistency

Time is the most potent ingredient in the compound interest recipe. This is why financial experts emphasize starting early. Consider two investors: Investor A starts at age 20 and invests $200 a month for 10 years, then stops. Investor B starts at age 30 and invests $200 a month for the next 30 years. Despite Investor B contributing much more total capital, Investor A will likely end up with more money at retirement because their initial contributions had an extra decade to compound.

Considering Inflation and Taxes

When calculating your future wealth, it is vital to account for “real” returns. Inflation erodes the purchasing power of your money. If your investment grows at 7% but inflation is 3%, your real rate of return is 4%. Additionally, unless your money is in a tax-advantaged account like a Roth IRA, you will owe taxes on your gains, which can slow down the compounding process.

Leveraging Compound Interest in Your Personal Finance Strategy

Knowing the math is one thing; applying it to your life is another. To truly benefit from compound interest, you must choose the right financial vehicles.

High-Yield Savings Accounts and CDs

For short-to-medium-term goals, High-Yield Savings Accounts (HYSAs) and Certificates of Deposit (CDs) are excellent entry points. These accounts offer higher interest rates than standard checking accounts and often compound interest daily or monthly, ensuring your “n” value is working in your favor.

Dividend Reinvestment Plans (DRIPs)

For stock market investors, dividends offer a unique way to compound. A Dividend Reinvestment Plan (DRIP) automatically uses the dividends paid out by a company to purchase more shares of that company. Instead of taking the cash, you increase your principal (P), which in turn generates more dividends in the next cycle. This creates a powerful feedback loop of growth.

Retirement Accounts: 401(k)s and IRAs

Retirement accounts are designed specifically to maximize compounding. Because these accounts are tax-deferred (Traditional) or tax-free (Roth), the interest that would normally go to the government stays in your account, compounding alongside your principal. Furthermore, many employers offer a “match” on 401(k) contributions, which essentially doubles your principal before the compounding even begins.

Avoiding the Reverse Effect: Compound Interest on Debt

While compound interest is a friend to the saver, it is a formidable enemy to the debtor. The same mathematics that grows your wealth can also accelerate your financial ruin if you are carrying high-interest debt.

The Danger of Credit Card Balances

Credit cards are the most common example of compound interest working against the consumer. Most credit card companies compound interest daily. If you carry a balance of $5,000 at a 20% APR, the interest added today will itself begin accruing interest tomorrow. This is why many people feel they are “treading water” even when making the minimum payments; they are only covering the newly compounded interest rather than touching the principal.

Strategies to Mitigate Interest Accumulation

To stop the negative effects of compounding debt, financial experts suggest several strategies:

- The Debt Avalanche: Focus on paying off the debt with the highest interest rate first, effectively removing the most aggressive “compounding” threat to your net worth.

- Balance Transfers: Moving high-interest debt to a 0% APR introductory card can pause the compounding process, allowing every dollar you pay to go directly toward the principal.

- Increased Payment Frequency: Making bi-weekly payments instead of monthly payments can slightly reduce the amount of interest that has time to accrue and compound.

In conclusion, compound interest is a neutral mathematical force. Whether it builds a mountain of wealth or a mountain of debt depends entirely on your financial habits and your understanding of the formula. By starting early, choosing high compounding frequencies, and remaining consistent, you can ensure that the “magic” of compounding works for you, securing your financial future and paving the way for long-term prosperity.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.