In the realm of personal and professional finance, the ability to perform mental mathematics is more than just a convenient party trick; it is a vital skill for real-time decision-making. Among all mathematical operations, calculating 10 percent of a number stands as the most critical “anchor” calculation. Whether you are at a restaurant calculating a tip, in a boardroom evaluating a profit margin, or looking at a brokerage account to assess a market dip, the “10 percent rule” provides an immediate framework for understanding value.

While a calculator is always within reach in our digital age, the cognitive ability to grasp percentages intuitively allows for a deeper connection with your money. This guide explores the mechanics of calculating 10 percent and, more importantly, how to apply this foundational math to achieve financial literacy and long-term wealth.

The Mechanics of the 10% Calculation in Personal Finance

The beauty of the number ten lies in our base-10 numeral system. Because our entire financial structure is built on tens, hundreds, and thousands, finding 10 percent is mathematically the simplest percentage to derive. Understanding the “how” is the first step toward utilizing this tool in high-pressure financial environments.

The “Decimal Shift” Method

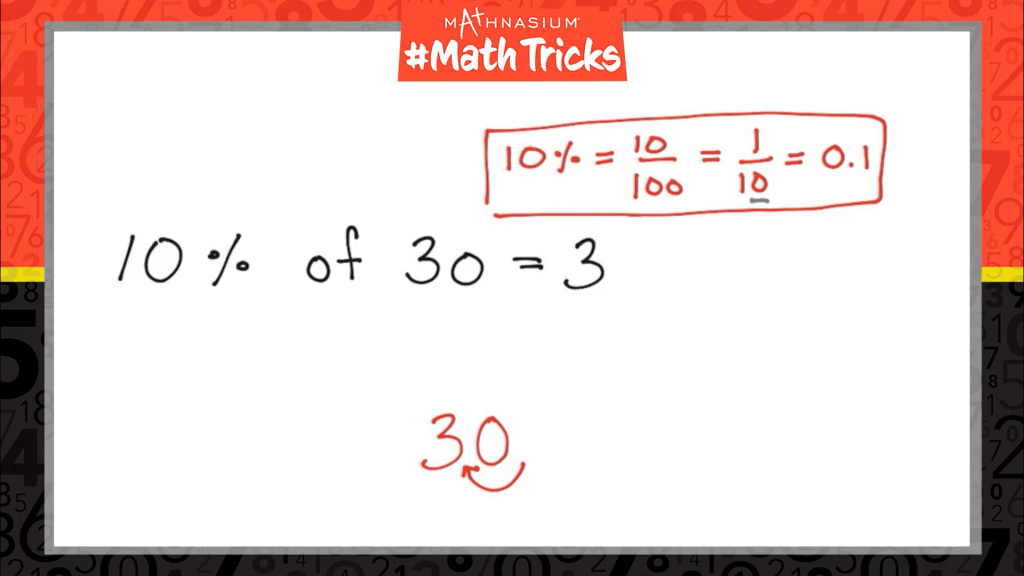

The most efficient way to calculate 10 percent of any number is the decimal shift method. Since 10 percent is equivalent to the fraction 1/10 or the decimal 0.10, calculating it simply requires moving the decimal point one position to the left.

For example, if you are looking at a business invoice for $1,550.00, finding 10 percent involves moving the decimal point once to the left, resulting in $155.00. If the number is a single digit or does not have a visible decimal, such as 5, you treat it as 5.0, move the decimal, and arrive at 0.5. This mental shortcut eliminates the need for long division or multiplication, allowing for instantaneous financial assessments during negotiations or budgeting sessions.

Why 10% is the Anchor of Financial Literacy

In finance, 10 percent serves as a “benchmark.” Once you have identified 10 percent of a figure, you can quickly derive other common percentages. If you need to find 5 percent, you simply take half of your 10 percent figure. If you need 20 percent, you double it.

This creates a mental “financial map.” If you are evaluating a credit card with an 18 percent APR, you can quickly calculate 10 percent, double it to get 20 percent, and realize the interest is slightly less than that double-figure. This level of numeracy prevents consumers from falling into debt traps where the actual cost of borrowing is obscured by abstract percentage points.

Applying the 10% Rule to Budgeting and Savings

In the world of money management, 10 percent is often cited as the “golden ratio” for sustainable growth. From the ancient practice of tithing to modern 401(k) contributions, the 10 percent figure represents a balance between living for today and securing tomorrow.

Tithing to Your Future Self: The 10% Savings Rule

One of the most enduring pieces of financial advice is to “pay yourself first” by saving at least 10 percent of your gross income. This is often the baseline for financial stability. When you calculate 10 percent of your monthly paycheck immediately upon receipt, you set a boundary for your lifestyle.

If you earn $5,000 a month, your 10 percent calculation—$500—becomes a non-negotiable expense. By automating this $500 transfer to a high-yield savings account or an index fund, you ensure that your net worth grows proportionally with your income. The simplicity of the 10 percent calculation makes it easy to adjust your savings goals as you receive raises or take on side hustles, ensuring that “lifestyle creep” does not erode your financial future.

Managing Variable Expenses and Tipping Culture

On the micro-economic level, calculating 10 percent is a daily necessity for managing variable expenses, particularly in service industries. While 15 to 20 percent has become the standard for gratuity in many regions, 10 percent remains the mental starting point.

Being able to calculate 10 percent of a $78.40 dinner bill ($7.84) allows you to quickly double it for a 20 percent tip ($15.68) or add half of the 10 percent to reach 15 percent ($7.84 + $3.92 = $11.76). This speed ensures that you remain in control of your daily outgoings without the friction of fumbling with a smartphone app, maintaining a professional and confident presence in social financial settings.

Strategic Investing and Risk Management

Beyond simple savings, the 10 percent figure plays a sophisticated role in investment strategy and risk mitigation. Professional investors use this percentage to gauge market health and portfolio balance.

The 10% Threshold for Portfolio Rebalancing

In an investment portfolio, asset allocation is key to long-term success. Many financial advisors suggest rebalancing a portfolio if a specific asset class grows or shrinks by 10 percent relative to its target weight. For instance, if your strategy dictates that 50 percent of your wealth should be in equities, but a market rally pushes that figure to 55 percent, you have experienced a 10 percent relative shift (5% is 10% of 50%).

Calculating this 10 percent deviation is crucial for risk management. It signals that it is time to sell some winners and buy underperforming assets to maintain your desired risk profile. Without the ability to quickly recognize these 10 percent shifts, an investor may find themselves “over-leveraged” in a volatile market, leading to significant losses during a correction.

Evaluating Annualized Returns and Dividends

The S&P 500 has historically provided an average annual return of approximately 10 percent before inflation. This makes the 10 percent calculation the standard against which all other investments are measured. When an investment opportunity promises a 4 percent return, you know it is less than half of the historical market average. Conversely, if an “online income” scheme promises 10 percent returns per month, your mathematical intuition should immediately signal high risk, as that would vastly outperform the 10 percent per year gold standard.

Business Finance: Utilizing 10% for Growth and Taxation

For entrepreneurs and small business owners, 10 percent is more than a number—it is a metric for health and a buffer for survival. In the corporate world, margins and tax liabilities are often viewed through this lens.

Setting Aside 10% for Tax Liabilities

One of the most common reasons small businesses fail is the inability to pay quarterly or end-of-year taxes. A prudent financial strategy is to calculate 10 percent of every dollar of revenue and move it into a dedicated tax holding account. While the actual tax rate may be higher or lower depending on the jurisdiction and business structure, the 10 percent rule provides an immediate, easy-to-calculate liquidity buffer.

By calculating 10 percent on a $10,000 contract ($1,000) and sequestering it, the business owner ensures that they are never caught off guard by the IRS or local tax authorities. This discipline transforms the 10 percent calculation from a math problem into a sophisticated risk-mitigation strategy.

The 10% Profit Margin Benchmark

In many industries, a 10 percent net profit margin is considered the threshold for a “healthy” business. By constantly calculating 10 percent of gross sales and comparing it to net income, owners can quickly assess operational efficiency. If a company generates $1,000,000 in revenue but produces only $50,000 in profit, the owner can use the 10 percent benchmark ($100,000) to realize they are performing at only half the desired efficiency. This realization often prompts a deep dive into overhead costs, labor expenses, and pricing strategies.

Conclusion: The Power of the Decimal

Mastering the calculation of 10 percent is the first step toward total financial command. It is a deceptively simple tool that facilitates complex financial behaviors: saving for retirement, managing investment risk, and ensuring business solvency.

When you look at a number—any number—and can instantly see its tenth part, you are no longer a passive observer of your financial life. You become an active manager, capable of assessing discounts, calculating taxes, and evaluating market trends in the blink of an eye. In the pursuit of wealth, the decimal point is your most powerful lever; moving it one space to the left is the simplest way to move your financial future ten steps forward.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.