Investing in the stock market can seem daunting, a complex landscape of volatile stocks, bewildering terminology, and endless choices. For many, the idea of picking individual winners feels like a gamble best left to seasoned professionals. Yet, for those seeking a straightforward, diversified, and cost-effective path to long-term wealth creation, the S&P 500 index fund stands out as a beacon of simplicity and efficacy.

An S&P 500 index fund offers an elegant solution: rather than trying to beat the market, you effectively become the market. By investing in such a fund, you gain exposure to the performance of 500 of the largest and most established U.S. companies, spanning various sectors. This inherent diversification significantly reduces the risk associated with investing in single stocks, while historically delivering robust returns over extended periods.

This guide will demystify the process, walking you through everything you need to know about S&P 500 index funds – from understanding what they are and why they’re so popular, to the practical steps of purchasing one, and crucial considerations for managing your investment. Whether you’re a novice investor taking your first steps or looking to refine your portfolio, understanding how to buy an S&P 500 index fund is a foundational skill for financial success.

Understanding the S&P 500 Index Fund

Before diving into the mechanics of buying, it’s essential to grasp what an S&P 500 index fund truly represents and its underlying philosophy. This knowledge forms the bedrock of a confident investment strategy.

What is the S&P 500?

The S&P 500, or Standard & Poor’s 500, is a stock market index that represents the performance of 500 of the largest publicly traded companies in the United States. It’s a “market-capitalization-weighted” index, meaning companies with larger market values have a greater impact on the index’s movement. These companies are selected by a committee based on criteria such as market size, liquidity, and sector representation, making the S&P 500 a robust barometer of the overall U.S. stock market and, by extension, the broader U.S. economy. Iconic names like Apple, Microsoft, Amazon, Google (Alphabet), and Tesla are among its constituents, covering diverse sectors from technology and finance to healthcare and consumer staples.

How Index Funds Work

An index fund is a type of mutual fund or Exchange Traded Fund (ETF) with a portfolio constructed to match or track the components of a market index, such as the S&P 500. Instead of actively picking stocks, the fund manager’s job is simply to replicate the index’s performance. If the S&P 500 goes up by 1%, the index fund tracking it aims to go up by roughly 1% (minus a minuscule fee). This passive management approach is a stark contrast to actively managed funds, where managers attempt to outperform the market through strategic buying and selling of securities. The beauty of index funds lies in their simplicity and the fact that most actively managed funds struggle to consistently beat their benchmark index over the long term, especially after accounting for higher fees.

Why Invest in an S&P 500 Index Fund?

Investing in an S&P 500 index fund offers several compelling advantages for both novice and experienced investors:

- Broad Diversification: With exposure to 500 companies across 11 major sectors, your investment is inherently diversified. This reduces the risk associated with a single company performing poorly or an entire industry experiencing a downturn. You’re not putting all your eggs in one basket.

- Low Costs: Due to their passive management style, index funds typically have significantly lower expense ratios (annual fees) compared to actively managed funds. These small differences in fees can translate into substantial savings and higher returns over decades.

- Passive Investing (Set It and Forget It): Once you’ve invested, there’s no need to constantly monitor individual stock performance or make frequent trading decisions. This makes it an ideal choice for long-term investors who prefer a hands-off approach.

- Historical Performance: Historically, the S&P 500 has delivered average annual returns of around 10-12% over long periods, making it a powerful engine for wealth accumulation when combined with the magic of compound interest. While past performance is no guarantee of future results, it provides a strong foundation for long-term growth.

- Transparency: You always know what you own – a slice of the 500 largest U.S. companies, publicly listed and easily verifiable.

Types of S&P 500 Index Funds

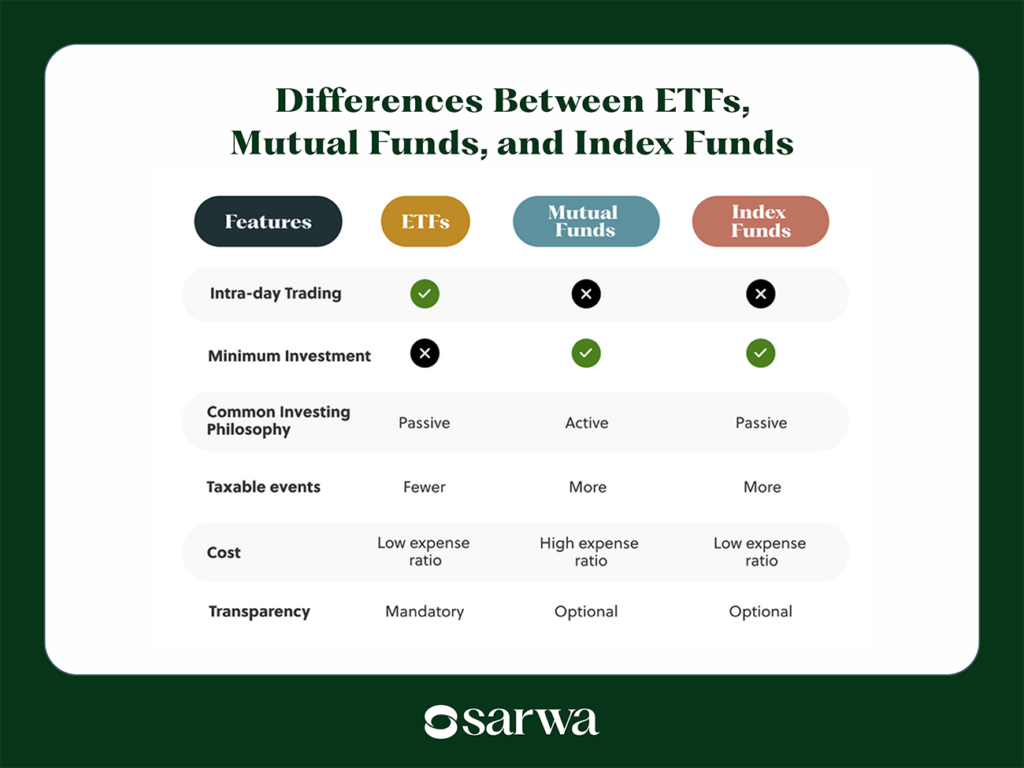

When you decide to invest in an S&P 500 index fund, you’ll generally encounter two primary structures: Exchange-Traded Funds (ETFs) and mutual funds. While both achieve the goal of tracking the S&P 500, they have distinct characteristics that might suit different investor preferences.

Exchange-Traded Funds (ETFs)

ETFs are funds that hold a collection of assets, like stocks, but trade on stock exchanges much like individual stocks. You can buy and sell ETF shares throughout the trading day at market prices. For an S&P 500 ETF, this means you can place an order for a specific number of shares at any point during market hours, and the price will fluctuate based on supply and demand, similar to a stock. Popular S&P 500 ETFs include SPY (SPDR S&P 500 ETF Trust), IVV (iShares Core S&P 500), and VOO (Vanguard S&P 500 ETF).

Mutual Funds

Mutual funds are professionally managed investment funds that pool money from many investors to purchase securities. When you invest in an S&P 500 mutual fund, you’re buying “units” or “shares” of the fund directly from the fund company. Mutual fund shares are typically priced once a day, after the market closes, based on their Net Asset Value (NAV). This means you place an order, and it’s executed at that end-of-day price. Vanguard 500 Index Fund (VFIAX) and Fidelity 500 Index Fund (FXAIX) are well-known examples of S&P 500 index mutual funds.

Key Differences and Considerations

Choosing between an S&P 500 ETF and a mutual fund often comes down to trading flexibility, minimum investment amounts, and how you prefer to invest.

- Trading Flexibility: ETFs offer intra-day trading flexibility, allowing you to buy or sell at any moment the market is open. Mutual funds only trade once a day at the closing NAV. For long-term investors, this difference is often negligible.

- Minimum Investment: ETFs typically have no minimum investment beyond the price of a single share (though some brokers allow fractional shares), making them accessible even with small amounts. Mutual funds often have minimum initial investment requirements, which can range from $1,000 to $3,000 or more, though some brokerage firms offer no-minimum funds.

- Cost Structure: Both ETFs and index mutual funds tracking the S&P 500 typically have very low expense ratios. However, ETFs may incur trading commissions (though many brokers now offer commission-free ETF trading), whereas mutual funds might have transaction fees or loads (sales charges) if not purchased directly or through certain platforms. Always opt for no-load, low-expense ratio funds.

- Automatic Investing: Mutual funds often facilitate automatic, recurring investments (e.g., $100 every month) more seamlessly than ETFs, though many brokerage platforms now support automated investing into ETFs as well.

For most long-term investors, either an ETF or a mutual fund tracking the S&P 500 will serve the purpose admirably. The best choice depends on your specific brokerage’s offerings and your preference for how you place orders.

Steps to Buying an S&P 500 Index Fund

Purchasing an S&P 500 index fund is a straightforward process once you understand the steps involved. It typically requires setting up an investment account and then selecting and funding your chosen fund.

Open a Brokerage Account

The first step is to open an investment account with a reputable brokerage firm. This will be the account where you hold your index fund shares. Popular options include Vanguard, Fidelity, Charles Schwab, E*TRADE, and Merrill Edge. When choosing a brokerage, consider factors like:

- Fees and Commissions: Look for commission-free ETF trading and no-transaction-fee mutual funds.

- Investment Options: Ensure they offer the specific S&P 500 index funds or ETFs you’re interested in.

- User Interface and Tools: A user-friendly platform is crucial, especially for beginners.

- Customer Service: Good support can be invaluable if you encounter issues.

- Account Types: Decide what type of account is best for your goals. Common options include:

- Taxable Brokerage Account: A standard investment account with no contribution limits, but earnings are subject to capital gains tax.

- Roth IRA: Contributions are made with after-tax money, and qualified withdrawals in retirement are tax-free.

- Traditional IRA: Contributions may be tax-deductible, but withdrawals in retirement are taxed as ordinary income.

- 401(k) or 403(b): Employer-sponsored retirement plans that often offer S&P 500 index funds as an investment option.

The application process typically involves providing personal information (name, address, Social Security number), employment details, and financial information. It usually takes a few minutes to complete online.

Fund Your Account

Once your brokerage account is open, you’ll need to transfer money into it. Common funding methods include:

- Electronic Funds Transfer (EFT): Linking your bank account to your brokerage account for direct transfers, usually taking 1-3 business days.

- Wire Transfer: Faster but often incurs fees.

- Check Deposit: Slower processing time.

- Rollover: Transferring funds from an old 401(k) or IRA.

Ensure you fund your account with enough money to meet any minimum investment requirements for the fund you choose (especially for mutual funds) or to purchase at least one share of your chosen ETF.

Research and Select Your Fund

With funds in your account, it’s time to choose your specific S&P 500 index fund. Key metrics to compare include:

- Expense Ratio: This is the annual fee charged as a percentage of your investment. Aim for the lowest possible, ideally below 0.10% for S&P 500 index funds. For instance, Vanguard’s VOO, Fidelity’s FXAIX, and Schwab’s SWPPX all boast expense ratios under 0.05%.

- Tracking Error: How closely the fund tracks its underlying index. Lower is better.

- AUM (Assets Under Management): Larger funds tend to be more stable and liquid.

- Fund Provider: Stick with reputable providers like Vanguard, Fidelity, iShares (BlackRock), and Charles Schwab.

For ETFs, look for tickers like SPY, IVV, or VOO. For mutual funds, look for VFIAX or FXAIX, among others. Most brokerages will have their own proprietary S&P 500 index fund with very competitive fees.

Place Your Buy Order

Finally, execute your purchase.

- For ETFs:

- Search for the ETF by its ticker symbol (e.g., VOO).

- Select “Buy.”

- Enter the number of shares you want to purchase.

- Choose your order type (market order for immediate execution at the current market price, or limit order to set a specific price you’re willing to pay). For long-term investors, a market order is often acceptable for ETFs with high trading volume.

- Review and confirm your order.

- For Mutual Funds:

- Search for the mutual fund by its ticker symbol (e.g., VFIAX).

- Select “Buy.”

- Enter the dollar amount you want to invest.

- Review and confirm your order. Your purchase will be executed at the fund’s NAV after the market closes.

Congratulations! You’ve successfully purchased your S&P 500 index fund.

Important Considerations Before Investing

While buying an S&P 500 index fund is generally a sound strategy, a few critical financial principles and considerations should guide your decision-making to ensure it aligns with your broader financial goals.

Expense Ratios and Fees

Reiterating this point is crucial: small fees can have a massive impact over decades. A fund with a 0.50% expense ratio versus one with a 0.03% expense ratio might seem insignificant, but the difference compounded over 30-40 years can amount to tens or even hundreds of thousands of dollars in lost earnings. Always prioritize funds with the lowest possible expense ratios for broad market index tracking. Be wary of hidden transaction fees or sales loads (commissions) associated with certain mutual funds.

Capital Gains Tax and Dividends

Understanding the tax implications of your investments is vital, especially in a taxable brokerage account.

- Dividends: S&P 500 companies pay dividends, which the index fund collects and then distributes to its shareholders (you). These dividends are typically taxable as ordinary income or qualified dividends in the year they are received, even if you reinvest them.

- Capital Gains: When you eventually sell your fund shares for a profit, you’ll incur capital gains taxes. Short-term capital gains (assets held for one year or less) are taxed at your ordinary income tax rate, while long-term capital gains (assets held for more than one year) benefit from preferential lower tax rates. Index funds tend to be tax-efficient because their passive nature means less frequent selling of underlying securities, reducing capital gains distributions within the fund itself. However, if you sell your shares, that’s a taxable event.

- Tax-Advantaged Accounts: Investing in an S&P 500 index fund within a Roth IRA or Traditional IRA offers significant tax benefits, either tax-free growth and withdrawals (Roth) or tax-deferred growth (Traditional). Maxing out these accounts before investing heavily in taxable brokerage accounts is often a smart move.

Dollar-Cost Averaging

Dollar-cost averaging is an investment strategy where you invest a fixed amount of money at regular intervals (e.g., $100 every month), regardless of the market’s current price. This strategy helps mitigate risk by preventing you from investing a large sum at a market peak. When prices are high, your fixed amount buys fewer shares; when prices are low, it buys more shares. Over time, this averages out your purchase price, reducing the emotional temptation to time the market. It’s a particularly effective strategy for long-term S&P 500 index fund investors.

Long-Term vs. Short-Term Goals

S&P 500 index funds are best suited for long-term investment goals, typically those with a time horizon of 5-10 years or more. While they offer diversification, they are still exposed to stock market volatility. Short-term market fluctuations can lead to temporary losses. If you need the money within a few years (e.g., for a down payment on a house), it might be better kept in less volatile assets like high-yield savings accounts or short-term bonds. Patience and a long-term perspective are crucial for seeing significant returns from the S&P 500.

Risk Tolerance and Portfolio Allocation

While S&P 500 index funds are diversified, they represent a 100% equity (stock) investment and thus carry inherent market risk. The value of your investment can go down, and you could lose money. Assess your personal risk tolerance. If you’re particularly risk-averse, you might consider a more diversified portfolio that includes bonds or other asset classes to reduce overall volatility. An S&P 500 fund might form the core of your equity allocation, but it’s important to understand how it fits into your overall financial plan and risk profile.

Managing Your S&P 500 Investment

Once you’ve purchased your S&P 500 index fund, the management aspect is refreshingly minimal, reinforcing its appeal as a passive investment strategy.

Rebalancing (If Applicable)

If your S&P 500 index fund is part of a broader, more diversified portfolio (e.g., 60% stocks, 40% bonds), you may need to rebalance periodically. Rebalancing means adjusting your portfolio back to your target asset allocation. For example, if your stocks have performed exceptionally well, they might now represent 70% of your portfolio. Rebalancing would involve selling some of your S&P 500 fund shares (or stopping new contributions to it and directing them elsewhere) and buying more bonds to return to your 60/40 target. For an investor whose entire equity allocation is the S&P 500 fund, rebalancing within that specific fund isn’t necessary, as the fund itself is always rebalancing its underlying holdings to match the index.

Staying the Course

Perhaps the most challenging but crucial aspect of managing an S&P 500 investment is resisting the urge to react to short-term market fluctuations. The market will inevitably experience downturns, sometimes severe ones. During these times, it’s easy to panic and sell. However, history repeatedly shows that market timing is a fool’s errand, and those who remain invested through downturns are typically rewarded when the market recovers. Trust in the long-term growth potential of the S&P 500, continue your regular contributions (dollar-cost averaging), and avoid emotional decisions.

When to Sell (Rarely, But Possible)

For a long-term, passive investor, the ideal scenario is to rarely sell your S&P 500 index fund shares. You typically sell when:

- You need the money: For retirement, a major planned expense years down the line, or an emergency (though you should have a separate emergency fund).

- Your financial goals or risk tolerance have significantly changed: Your investment strategy needs to evolve with your life stages.

- You’re rebalancing a highly diversified portfolio: As mentioned above, to maintain your target asset allocation.

Selling purely out of fear during a market crash is almost always detrimental to long-term wealth.

Conclusion

Investing in an S&P 500 index fund is a powerful and accessible strategy for building long-term wealth. It offers unparalleled diversification, low costs, and the simplicity of passively tracking the performance of 500 of America’s leading companies. By understanding the fundamentals of what these funds are, choosing between ETFs and mutual funds, meticulously following the steps to open an account and make a purchase, and adhering to sound investment principles like minimizing fees and practicing dollar-cost averaging, you can harness the formidable power of the stock market.

Remember, patience and a long-term perspective are your greatest allies. The journey to financial independence is a marathon, not a sprint, and an S&P 500 index fund provides a sturdy, reliable vehicle to help you reach your destination. By taking action today, you’re not just buying a fund; you’re investing in your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.