In a world brimming with financial complexities, the simple act of budgeting stands as a beacon of clarity and control. Often misunderstood as a restrictive chore, budgeting is, in fact, the most powerful tool for achieving financial freedom, stability, and peace of mind. It’s not about depriving yourself; it’s about empowering yourself to make conscious choices about your money, aligning your spending with your values and long-term aspirations.

This guide will demystify the budgeting process, transforming it from a daunting task into an accessible and empowering habit. We’ll explore the fundamental “why,” delve into various methodologies, walk through practical implementation steps, and discuss how to sustain your budgeting efforts for lasting success. Whether you’re drowning in debt, saving for a major purchase, or simply seeking greater financial clarity, mastering the art of budgeting is your first, most crucial step.

Understanding the ‘Why’ Behind Budgeting

Before diving into the mechanics, it’s essential to grasp the profound impact budgeting can have on your life. Without a clear understanding of your financial inflows and outflows, you’re essentially navigating a ship without a compass – drifting without direction. Budgeting provides that compass, charting your course towards desired financial destinations.

The Pillars of Financial Stability

Budgeting is the bedrock upon which all other financial goals are built. It allows you to:

- Track Your Money: Gain a clear picture of where every dollar comes from and where it goes. This visibility is often eye-opening, revealing hidden spending patterns.

- Prevent Overspending: By setting limits and allocating funds, you avoid the trap of impulse purchases and living beyond your means, which is a common precursor to debt.

- Save for Goals: Whether it’s a down payment on a house, retirement, a child’s education, or a dream vacation, budgeting provides the framework to systematically set aside funds for these aspirations.

- Reduce Financial Stress: Knowing you have a plan and that your finances are under control significantly alleviates anxiety related to money, fostering greater peace of mind.

- Build an Emergency Fund: Life is unpredictable. A well-structured budget prioritizes saving for an emergency fund, acting as a crucial safety net for unexpected expenses like medical bills or job loss.

- Pay Down Debt: For those grappling with credit card debt or loans, budgeting is instrumental in allocating dedicated funds towards accelerated repayment, saving you thousands in interest.

Overcoming Common Budgeting Misconceptions

Many shy away from budgeting due to prevalent myths:

- “Budgeting is too restrictive.” While it involves setting limits, it’s more about intentional spending than deprivation. It frees up money for what truly matters to you.

- “I don’t earn enough to budget.” Budgeting is even more critical for those with limited income, as it ensures every dollar is maximized and directed efficiently.

- “Budgeting is complicated and time-consuming.” While there’s an initial setup, modern tools and simplified methods make ongoing management quick and straightforward.

- “I’m not good with numbers.” Budgeting doesn’t require advanced math skills; it primarily requires honesty and consistency.

Identifying Your Financial Goals

The most effective budgets are those driven by clear, compelling goals. Before you start crunching numbers, take time to define what you want your money to do for you. Are you aiming for:

- Becoming debt-free by a certain date?

- Saving a specific amount for an emergency fund?

- Making a down payment on a home within five years?

- Funding a significant travel experience?

- Investing for early retirement?

- Building a nest egg for your children?

Write these goals down. Make them SMART (Specific, Measurable, Achievable, Relevant, Time-bound). These goals will serve as your motivation and the guiding principles for every financial decision within your budget.

The Core Mechanics: Choosing Your Budgeting Method

There isn’t a one-size-fits-all approach to budgeting. The best method is the one you can stick with consistently. Explore these popular frameworks to find your ideal fit.

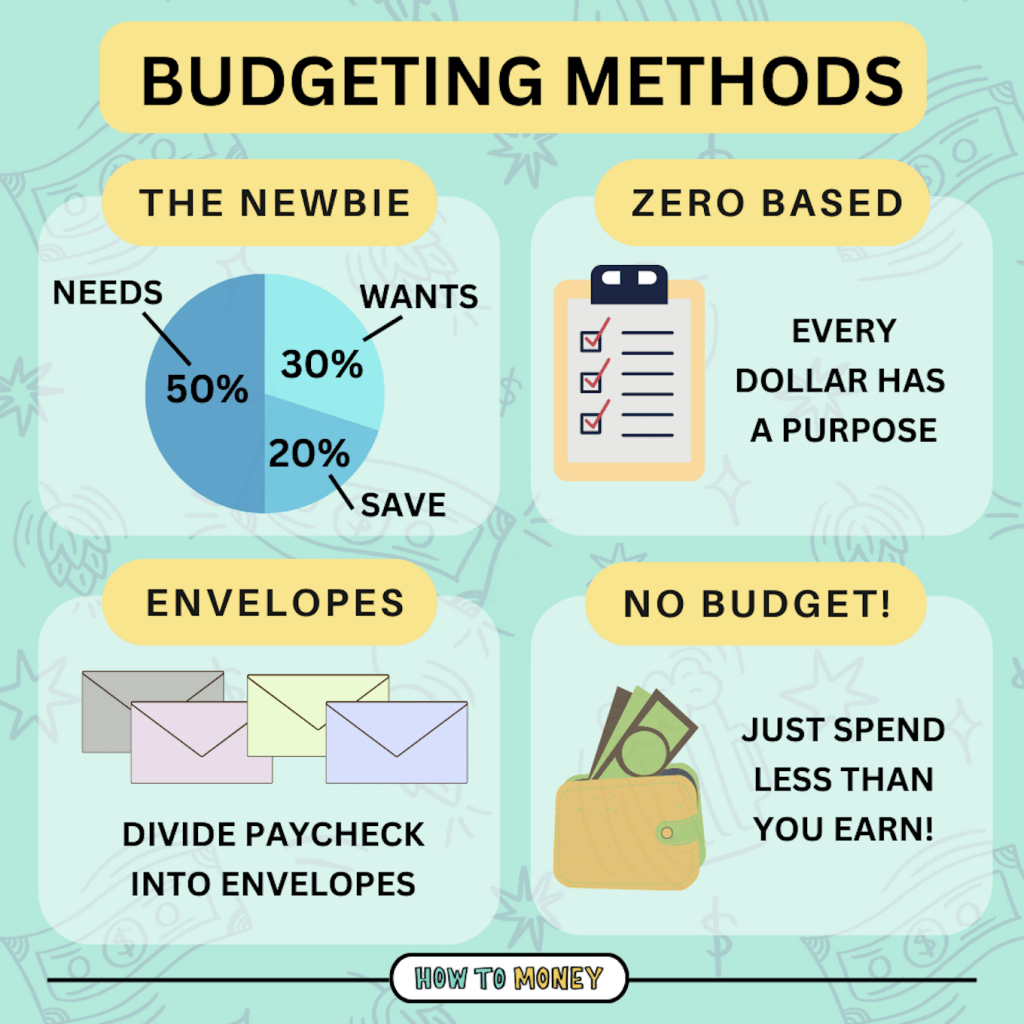

The 50/30/20 Rule: A Simple Framework

Popularized by Senator Elizabeth Warren, this method offers a straightforward guideline for allocating your after-tax income:

- 50% for Needs: Essential expenses like housing (rent/mortgage), utilities, groceries, transportation, insurance, and minimum loan payments.

- 30% for Wants: Discretionary spending such as dining out, entertainment, hobbies, travel, shopping, and subscriptions.

- 20% for Savings & Debt Repayment: Contributions to an emergency fund, retirement accounts, investments, and any debt payments above the minimum (e.g., student loans, credit cards).

This method is excellent for beginners due to its simplicity and flexibility.

Zero-Based Budgeting: Every Dollar Has a Job

With zero-based budgeting, you allocate every dollar of your income to a specific category – expenses, savings, or debt repayment – until your income minus your expenses equals zero. It doesn’t mean your bank account reaches zero, but rather that every dollar has been assigned a purpose on paper.

This method ensures maximum intentionality with your money and can be highly effective for those who want tight control over their finances. It requires diligent tracking but prevents “mystery spending.”

Envelope System: A Tangible Approach

This traditional method involves withdrawing cash for variable spending categories (like groceries, entertainment, personal care) and placing it into separate physical envelopes. Once an envelope is empty, you stop spending in that category until the next pay period.

The envelope system is particularly powerful for visual learners or those who struggle with overspending on credit cards, as it provides a tangible limit and reinforces the feeling of “spending real money.”

Digital Tools and Budgeting Apps

For the modern budgeter, numerous digital solutions streamline the process:

- Spreadsheets (Excel, Google Sheets): Customizable and free, allowing for detailed tracking and analysis.

- Budgeting Apps (You Need A Budget – YNAB, Mint, Personal Capital, Simplifi): These apps often link to your bank accounts and credit cards, automatically categorizing transactions and providing real-time insights, alerts, and goal tracking. Many offer reporting features to visualize your spending trends.

- Bank-Specific Tools: Many financial institutions now offer integrated budgeting tools within their online banking platforms.

These tools reduce manual effort and provide a dynamic view of your financial health, making it easier to stay on track.

Practical Steps to Building Your Budget

Once you’ve chosen a method, it’s time to roll up your sleeves and construct your budget. This process requires honesty and attention to detail.

Tracking Your Income: The Foundation

Start by listing all sources of income for a typical month after taxes (your net income). This includes your salary, freelance earnings, passive income, and any other regular inflows. If your income varies, use an average or a conservative estimate. This total figure will be the foundation of your budget.

Categorizing Your Expenses: Fixed vs. Variable

This is where many people get stuck. Gather your bank statements, credit card bills, and receipts from the past 1-3 months. Categorize every single expense.

- Fixed Expenses: These are predictable and generally remain the same each month. Examples: rent/mortgage, loan payments, insurance premiums, subscriptions.

- Variable Expenses: These fluctuate month-to-month and are often areas where you have the most control. Examples: groceries, dining out, entertainment, utilities (can vary), transportation (gas, public transit), clothing, personal care.

Don’t forget irregular expenses that might occur annually or quarterly (e.g., car registration, holiday gifts). Allocate a monthly amount for these by dividing the total annual cost by 12.

Identifying Areas for Optimization and Savings

Once you see your actual spending laid out, you’ll likely identify “money leaks.”

- Are you spending too much on dining out or impulse purchases?

- Are there subscriptions you no longer use?

- Can you negotiate lower insurance rates or bundle services?

- Are there cheaper alternatives for utilities or groceries?

This step is crucial for finding funds to reallocate towards your financial goals. Be honest but not overly critical. The goal is improvement, not perfection.

Allocating Funds to Your Financial Goals

Now, revisit your financial goals. Based on your income and optimized expenses, dedicate specific amounts to savings, debt repayment, and investments. Treat these allocations as non-negotiable “expenses.” For example, if your goal is to save $500/month for a down payment, that $500 needs a home in your budget just like your rent does. This ensures your money is actively working towards your future.

Maintaining and Adapting Your Budget Over Time

A budget is not a static document; it’s a living, breathing financial roadmap that requires ongoing attention and flexibility.

Regular Review and Adjustment

Set aside time at least once a month (or even weekly for the first few months) to review your budget.

- Compare Actual Spending to Budgeted Amounts: Where did you overspend? Where did you underspend?

- Analyze Variances: Understand why there were differences. Did an unexpected expense come up? Did you consciously choose to spend more in one category?

- Make Adjustments: If you consistently go over budget in a certain category, adjust your allocation, or find ways to reduce spending in that area. If you consistently underspend, you might reallocate those funds to savings or another goal.

- Update Income/Expenses: If your income changes, or if you incur new recurring expenses (e.g., a new subscription), update your budget immediately.

Handling Unexpected Expenses and Income Changes

Life happens. A tire blows out, a medical bill arrives, or you get a bonus at work.

- Emergency Fund: This is precisely why you budget for an emergency fund. Dip into it for true emergencies, and then prioritize replenishing it.

- Budget Flex: For smaller, unexpected costs, see if you can temporarily cut back in a variable spending category (e.g., dining out less) to absorb the cost without derailing your budget.

- Income Windfalls: If you receive a bonus or tax refund, resist the urge to splurge entirely. Allocate a significant portion towards debt repayment, savings, or investments, and perhaps a smaller portion for a planned treat.

Celebrating Milestones and Staying Motivated

Budgeting can be a marathon, not a sprint. Acknowledge your progress to stay motivated:

- Small Rewards: Hit a debt repayment milestone? Treat yourself to a modest, pre-budgeted reward.

- Visual Progress: Use charts or trackers to visualize your debt reduction or savings growth.

- Share Your Success: Talk to a trusted friend or partner about your achievements.

Maintaining momentum is key. Remind yourself of your goals and how each budget decision brings you closer to them.

Budgeting as a Lifelong Skill

Think of budgeting not as a temporary fix but as an essential life skill. Just like learning to cook or drive, it improves with practice. The more you engage with your money, the more intuitive and effective your budgeting becomes. It transforms from a chore into a powerful habit that underpins all your financial success.

Beyond the Basics: Advanced Budgeting Strategies

Once you’ve mastered the fundamentals, you can integrate more sophisticated financial strategies into your budget.

Integrating Debt Management into Your Budget

If you have high-interest debt, your budget should be its fiercest enemy.

- Debt Snowball/Avalanche: Dedicate extra funds (found through optimization) to aggressively pay down debt. The snowball method tackles the smallest balance first for psychological wins, while the avalanche method targets the highest interest rate first to save the most money.

- Consolidation/Refinancing: Explore options to lower your interest rates, freeing up more money within your budget for principal payments.

- Minimum Payments as Needs: Ensure all minimum payments are allocated in your “needs” category to avoid penalties and credit score damage.

Budgeting for Investments and Wealth Building

As your financial situation strengthens, your budget can pivot from primarily debt reduction and basic savings to wealth accumulation.

- Automate Investments: Treat investment contributions (e.g., 401k, IRA, brokerage accounts) as fixed expenses within your budget and set up automatic transfers.

- Diversify: As your investment budget grows, explore different asset classes to build a robust portfolio.

- Financial Advisor: Consider consulting a fee-only financial advisor to help you optimize your investment strategy within your budget framework.

The Role of Emergency Funds

An emergency fund is paramount. Your budget should prioritize building this fund until it covers 3-6 months of essential living expenses. This fund acts as a buffer, preventing you from going into debt when unforeseen circumstances arise. Keep it in an easily accessible, high-yield savings account separate from your everyday checking.

Family Budgeting and Financial Planning

For couples and families, budgeting becomes a collaborative effort.

- Open Communication: Regular financial discussions are crucial to align goals, understand spending habits, and make joint decisions.

- Shared vs. Separate Accounts: Decide on an approach that works for you – completely joint, completely separate, or a hybrid model.

- Involve Children (Age-Appropriate): Teach children about money, saving, and responsible spending as they grow, integrating them into simple budgeting concepts.

- Long-Term Planning: Extend your budgeting horizon to include major life events like college savings, retirement planning, and estate planning, ensuring your current budget supports these future goals.

In conclusion, budgeting is not a constraint but a catalyst. It’s the disciplined act of financial self-awareness that unlocks the door to greater choice, reduced stress, and ultimately, true financial freedom. By committing to understanding your money, choosing a method that works for you, and consistently adapting your approach, you will build a robust financial foundation that supports your aspirations, both immediate and long-term. Start today, and empower yourself to write your own financial story.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.