In the modern economic landscape, financial literacy is no longer a luxury—it is a survival skill. At the heart of financial literacy lies a single, often misunderstood practice: budgeting. While many perceive a budget as a restrictive tool designed to limit enjoyment, the reality is quite the opposite. A well-constructed budget is a roadmap to freedom. It provides the clarity needed to make informed decisions, the discipline to avoid debt, and the strategic framework required to build long-term wealth.

Budgeting is not merely about tracking pennies; it is about aligning your spending with your values. It is the process of intentionally allocating your resources so that your money works for you, rather than you working indefinitely for your money. This guide explores the multi-faceted world of personal finance management, offering a deep dive into the methodologies and psychological shifts necessary to master your cash flow.

The Foundation of Financial Literacy: Mindset and Principles

Before crunching numbers, one must address the psychological framework of spending. Most financial failures do not stem from a lack of income, but from a lack of intentionality.

Defining Your Financial “Why”

A budget without a purpose is rarely sustainable. To succeed, you must identify your core motivations. Are you budgeting to escape the crushing weight of student loans? Are you looking to achieve FIRE (Financial Independence, Retire Early)? Or is your goal to provide a legacy for your children? By attaching emotional weight to your financial targets, the act of “cutting back” transforms into an act of “investing in the future.” This shift in perspective is what differentiates a temporary diet from a lifestyle change.

Distinguishing Between Needs, Wants, and Obligations

The fundamental building block of any budget is the ability to categorize expenses accurately.

- Needs are the non-negotiables: housing, utilities, basic groceries, and insurance.

- Wants are the lifestyle choices: dining out, subscription services, and hobbies.

- Obligations are the commitments you’ve already made, primarily debt repayments.

The danger in modern personal finance is “lifestyle creep,” where wants are slowly rebranded as needs. A rigorous audit of your spending habits usually reveals that a significant portion of “essential” spending is actually discretionary.

Selecting Your Budgeting Methodology

There is no one-size-fits-all approach to money management. The best budget is the one you can stick to consistently. Depending on your personality and financial complexity, several proven frameworks can serve as your blueprint.

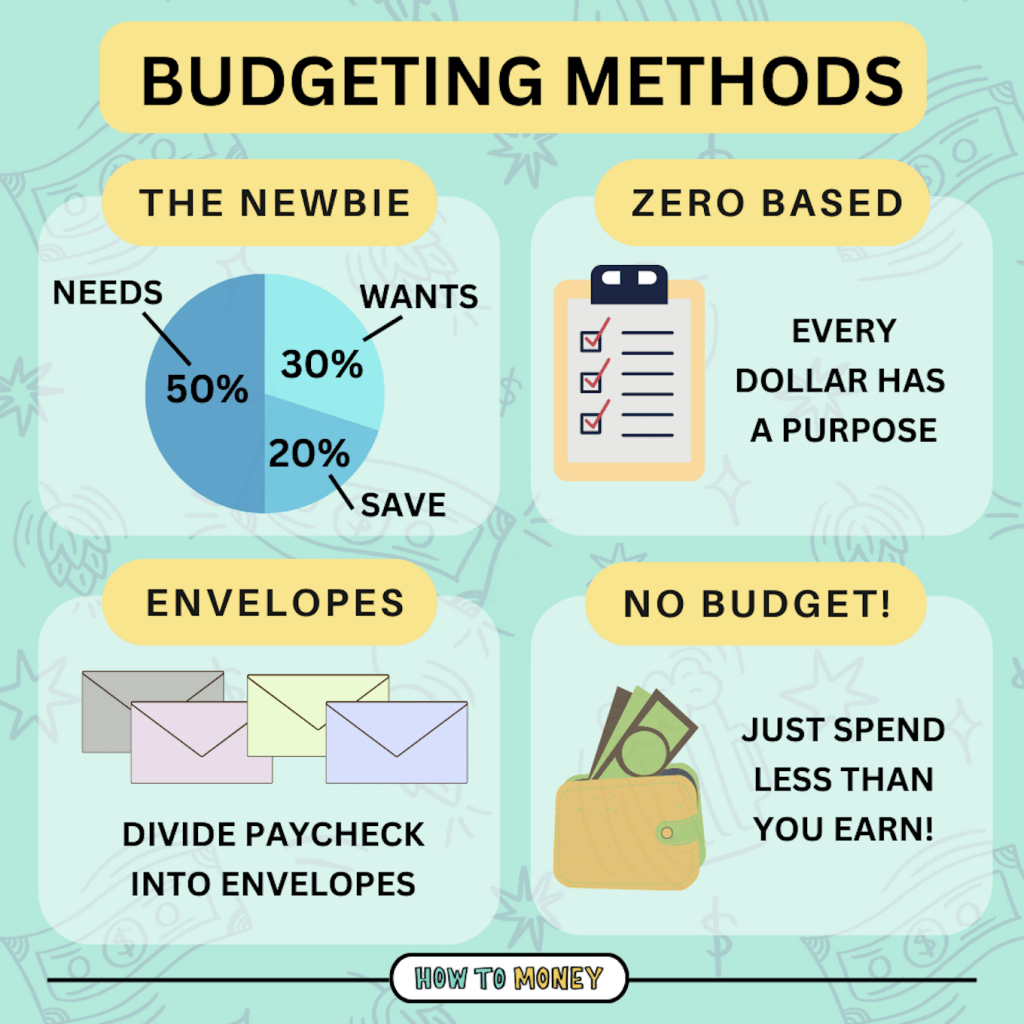

The 50/30/20 Rule

Popularized by Senator Elizabeth Warren, this is the gold standard for those who prefer simplicity. Under this model, 50% of your after-tax income goes toward Needs, 30% toward Wants, and 20% toward Savings and Debt Repayment. This framework provides a clear boundary for lifestyle spending while ensuring that a fifth of every dollar earned goes toward building your net worth. It is particularly effective for those new to budgeting who need high-level guardrails rather than granular tracking.

Zero-Based Budgeting

For the detail-oriented individual, Zero-Based Budgeting (ZBB) is the most powerful tool available. The philosophy is simple: Income minus Expenses equals Zero. Every single dollar you earn is assigned a specific “job” before the month begins. If you have $500 left over after covering bills and groceries, you don’t leave it in the checking account to be spent mindlessly; you assign it to a “Vacation Fund,” “Extra Principle on Mortgage,” or “Roth IRA.” This method eliminates “leakage”—those small, untracked expenses that quietly drain a bank account.

The “Pay Yourself First” Model

Also known as reverse budgeting, this method prioritizes long-term goals over short-term consumption. The moment your paycheck hits your account, a predetermined amount is automatically transferred to savings, investments, and debt payments. You are then free to spend the remainder of the money however you choose. This is ideal for high-earners or those who find traditional tracking too tedious but still want to guarantee their financial growth.

Managing Debt and Building Safety Nets

A budget is a defensive tool as much as an offensive one. You cannot build wealth effectively while being dragged down by high-interest liabilities or the constant threat of an unexpected emergency.

The Debt Snowball vs. The Debt Avalanche

When your budget reveals a surplus, it should be directed toward debt elimination. Two primary strategies exist:

- The Debt Snowball: Focus on paying off the smallest balance first while maintaining minimum payments on others. The psychological “win” of eliminating a debt quickly builds momentum.

- The Debt Avalanche: Focus on the debt with the highest interest rate. Mathematically, this saves the most money over time and leads to a faster exit from debt.

Your choice between these two should depend on whether you are motivated more by psychological victories or mathematical efficiency.

The Vital Role of the Emergency Fund

Financial volatility is a certainty, not a possibility. A robust budget must include a line item for an emergency fund. The standard recommendation is three to six months of essential living expenses. This fund acts as your financial “buffer,” preventing you from resorting to high-interest credit cards when a car breaks down or a medical bill arrives. Without this safety net, a single stroke of bad luck can dismantle years of disciplined budgeting.

Advanced Wealth Management through Budgeting

Once you have mastered the basics of cash flow and debt management, the budget evolves into a tool for optimization and wealth acceleration.

Managing Sinking Funds

One of the primary reasons budgets fail is the “unexpected” expense that was actually predictable—annual car registrations, holiday gifts, or home maintenance. Sinking funds solve this. By calculating the annual cost of these items and dividing by twelve, you can include them as a monthly “expense” in your budget. When the bill finally arrives, the money is already sitting in a dedicated account, turning a potential financial crisis into a non-event.

Automating Your Wealth

The ultimate goal of a sophisticated budget is to remove human error and emotion from the equation. High-level budgeters use automation to route their income into various “buckets” (Taxable brokerage accounts, 401ks, High-Yield Savings Accounts). By the time you look at your “available balance,” your future self has already been taken care of. This turns wealth building from an act of willpower into a default setting.

Sustaining Your Financial Momentum

The greatest challenge of budgeting is not the initial setup; it is the long-term maintenance. As your life changes, your financial plan must adapt accordingly.

Dealing with Lifestyle Creep

As your career progresses and your income increases, the natural tendency is to increase your spending proportionally. This is “lifestyle creep,” and it is the enemy of financial independence. To combat this, implement a “Percentage Split” for every raise. For every dollar of increased income, commit 50% to your future (investing/debt) and 50% to your present (lifestyle upgrades). This allows you to enjoy your success while simultaneously accelerating your path to wealth.

The Power of the Monthly Review

A budget is a living document. At the end of every month, you must perform a “reconciliation.” Compare your planned spending with your actual spending. This is not an exercise in self-guilt, but a data-gathering mission. If you consistently overspend in the “Groceries” category, your budget isn’t failing—it’s unrealistic. Adjust the numbers for the following month to reflect reality. This iterative process ensures that your budget remains a relevant and useful tool rather than a source of frustration.

Conclusion: The Freedom of the Constraint

In conclusion, learning how to budget is the most significant step an individual can take toward personal empowerment. By imposing intentional constraints on your spending, you grant yourself the freedom to live without financial anxiety. You shift from a reactive state—always wondering where the money went—to a proactive state—telling your money exactly where to go.

Whether you utilize the 50/30/20 rule for its simplicity or Zero-Based Budgeting for its precision, the result is the same: a life built on a foundation of stability and a future defined by opportunity. Financial success is rarely the result of a single windfall; it is the cumulative result of a thousand small, disciplined decisions made every month within the framework of a strategic budget. Start today, refine tomorrow, and watch as your financial goals transition from distant dreams into inevitable realities.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.