In the increasingly digitized landscape of personal finance, platforms like Venmo have revolutionized how we send and receive money. From splitting dinner bills to paying for freelance services, these apps offer unparalleled convenience. However, with this ease comes a critical need to understand the tax implications of these transactions. The phrase “Venmo tax” often circulates with a sense of unease and misunderstanding. This article aims to demystify the IRS reporting requirements for transactions conducted through third-party payment networks like Venmo, providing a professional and insightful guide to ensure compliance and smart financial management.

Demystifying the “Venmo Tax”: Understanding IRS Reporting Thresholds

The idea of a blanket “Venmo tax” is a common misconception. The IRS doesn’t tax the act of using Venmo itself; rather, it taxes certain types of income, regardless of how they are received. The “Venmo tax” discussion primarily revolves around the IRS requirement for third-party payment networks to report certain transactions to both the taxpayer and the IRS via Form 1099-K. Understanding this distinction is crucial for navigating your financial obligations.

The Evolution of 1099-K Reporting for Third-Party Payment Networks

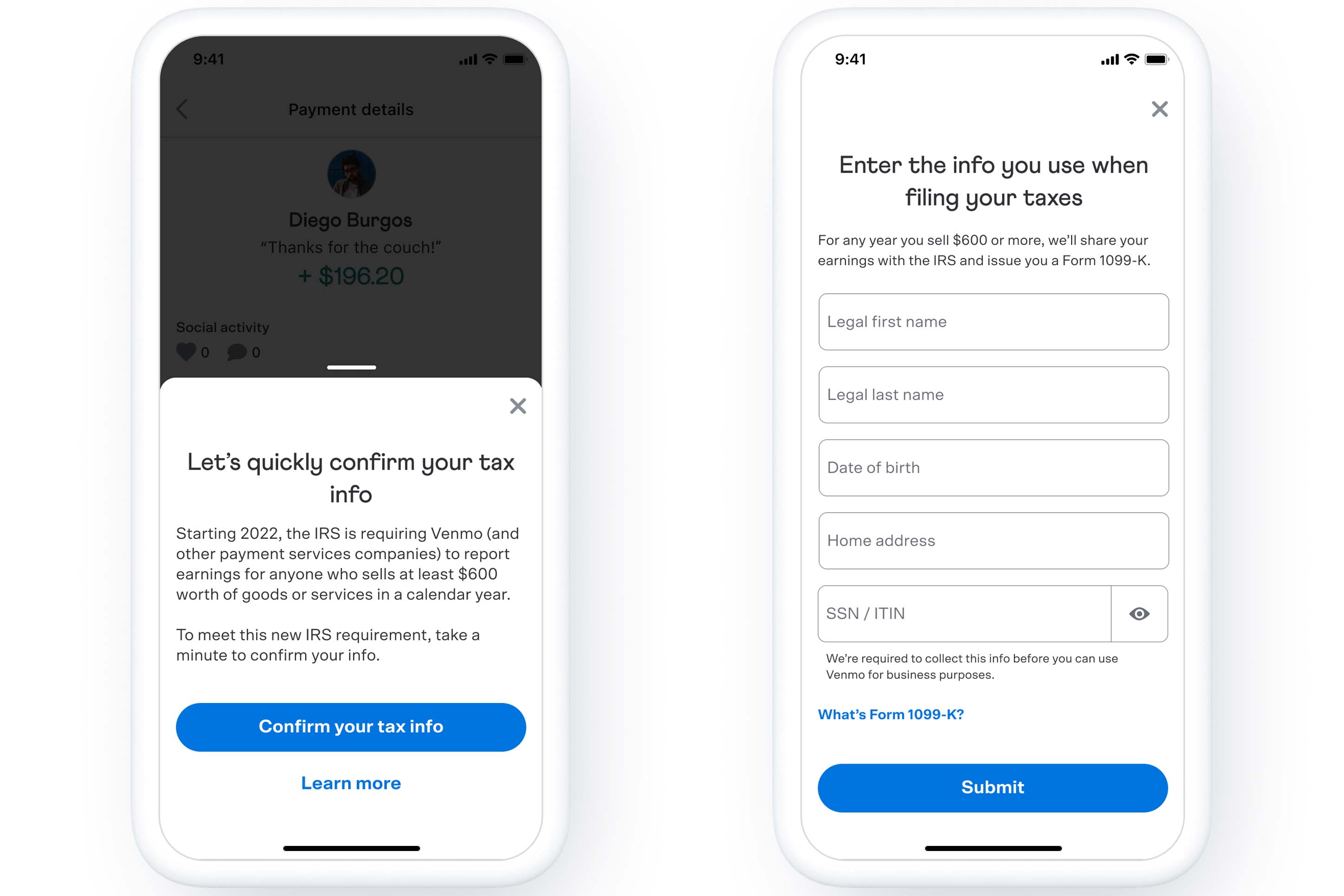

Historically, third-party payment networks (TPPNs) like Venmo, PayPal, and Square were required to issue a Form 1099-K to users if they processed more than 200 transactions AND the gross amount exceeded $20,000 in a calendar year. This threshold meant that many small businesses, freelancers, and gig workers never triggered the reporting requirement, even if their income was technically taxable.

The American Rescue Plan Act of 2021 initially proposed a drastic reduction of this threshold to a mere $600 with no minimum transaction count, effective for the 2022 tax year. This change caused significant confusion and concern, leading to a deferral by the IRS. For the 2023 tax year, the IRS announced a transitional period, raising the threshold to $20,000 and more than 200 transactions. However, for 2024 and beyond, the IRS intends to implement a $5,000 threshold as a stepping stone to the original $600 target. It is imperative for users to stay updated on the latest IRS guidance, as these thresholds can and do change, significantly impacting who receives a 1099-K.

Distinguishing Between Personal and Business Transactions

The core of understanding “Venmo tax” lies in differentiating between personal transactions and business-related income. The IRS is primarily interested in taxable income, which typically arises from the sale of goods or services.

- Personal Transactions: Payments for shared expenses (e.g., splitting rent, groceries, utilities), gifts between friends or family members, or reimbursements for expenses (e.g., a friend paying you back for concert tickets you bought) are generally not considered taxable income. These are often one-off transfers that do not represent earnings from a trade or business.

- Business Transactions: Payments received for goods sold (e.g., items sold online), services rendered (e.g., freelance writing, tutoring, dog walking), or income from your business activities, regardless of their scale, are generally considered taxable income. This applies whether you’re a full-time entrepreneur or engaging in a side hustle.

This distinction is paramount. While a 1099-K might report gross payments, it does not differentiate between these types. It’s your responsibility as the taxpayer to correctly identify and report only the taxable portion.

The Critical Role of Transaction Purpose and Memos

Venmo, like other platforms, allows users to add a memo or description to each transaction. This feature, often used casually, becomes incredibly important for tax purposes. Clearly labeling transactions can help both you and the IRS understand the nature of the payment.

For personal transactions, using clear descriptions like “rent reimbursement,” “dinner split,” or “gift” helps to substantiate that these are not taxable income. For business transactions, equally clear memos like “freelance writing services,” “graphic design fee,” or “product sale” can help you track your income accurately. While memos aren’t the sole piece of evidence, they form an important part of your overall record-keeping strategy.

Identifying Taxable Income and Non-Taxable Payments via Venmo

Understanding what constitutes taxable income versus a non-taxable payment on Venmo is fundamental to compliance. Many users inadvertently mix personal and business transactions, leading to potential confusion when tax season arrives. A clear delineation helps in accurate reporting and avoids unnecessary scrutiny.

Recognizing Income from Goods, Services, and Business Activities

Any money you receive on Venmo that is a direct result of providing a good or service is taxable income. This encompasses a broad range of activities:

- Freelancing and Gig Work: Payments for services like web design, writing, consulting, photography, or handyman work.

- Small Business Sales: Income from selling products, whether handcrafted items, digital goods, or resale merchandise.

- Commissions and Fees: Money earned through referral programs, affiliate marketing, or other commission-based activities.

- Rideshare and Delivery Earnings: While often processed through dedicated platforms, if a client pays you directly via Venmo for a service (e.g., a special delivery), it’s taxable.

It’s important to remember that taxability doesn’t depend on the amount. Even small amounts of income from these activities are technically taxable, though practical considerations like deductions might reduce your overall tax liability.

Clarifying Personal Gifts, Reimbursements, and Shared Expenses

Conversely, a significant portion of Venmo transactions falls into categories that are generally not subject to income tax:

- Personal Gifts: Money received as a gift, for example, for a birthday or holiday, is typically not taxable income to the recipient (though the giver may have gift tax implications if the amount exceeds the annual exclusion, which is rarely relevant for typical Venmo transactions).

- Reimbursements: If you pay for something on behalf of a friend or family member and they pay you back via Venmo, that reimbursement is not income. Examples include splitting a hotel bill, covering someone’s share of utilities, or getting paid back for concert tickets.

- Shared Expenses: Similar to reimbursements, splitting costs for groceries, rent, or a joint outing through Venmo means you are simply recovering your outlay, not earning income.

To differentiate these, ensuring your Venmo transactions are clearly marked with descriptive memos (e.g., “gift – birthday,” “rent split,” “pizza reimbursement”) is critical for maintaining clear records.

Specific Scenarios: Rental Income, Asset Sales, and Digital Currencies

Beyond the general categories, specific scenarios warrant careful attention:

- Rental Income: If you receive rent payments (e.g., for a spare room or vacation rental) via Venmo, this is unequivocally taxable income. It should be reported on Schedule E (Supplemental Income and Loss) of your tax return.

- Asset Sales: Selling personal items for less than you paid for them (e.g., used furniture, old electronics) generally does not result in taxable income, as you’re not making a profit. However, if you sell an asset for more than its original cost (e.g., a collectible that appreciated in value, or property), the profit is considered capital gains and is taxable.

- Digital Currencies: Venmo has integrated cryptocurrency buying and selling. Any gains realized from selling cryptocurrency for more than its purchase price are taxable as capital gains. Conversely, losses can potentially be deducted, subject to IRS rules. This is a complex area requiring meticulous record-keeping of purchase and sale prices.

Essential Strategies for Compliant Record-Keeping and Financial Management

Accurate record-keeping is not just a best practice; it’s a fundamental requirement for all taxpayers, especially those engaging in transactions that might trigger reporting via a 1099-K. Poor records can lead to overpaying taxes, missed deductions, or, worse, penalties from the IRS.

The Importance of Detailed Transaction Records

Your Venmo transaction history is a starting point, but it’s often insufficient on its own. For every business-related payment received:

- Keep Invoices/Contracts: Maintain copies of invoices, contracts, or agreements with clients that detail the services provided or goods sold.

- Track Expenses: For business income, meticulously track all related expenses (e.g., supplies, software, marketing costs). These can be deducted from your gross income, reducing your taxable profit.

- Utilize Memos Consistently: As mentioned, consistently using clear and descriptive memos in Venmo helps categorize transactions at a glance.

- Regularly Export Data: Periodically export your Venmo transaction history. While convenient, platforms can change their data retention policies. Having your own downloaded records (e.g., monthly or quarterly) provides an independent backup.

For personal transactions, a clear memo is often sufficient, especially if these are truly non-income related.

Best Practices for Segregating Business and Personal Finances

The most effective way to manage “Venmo tax” and overall financial health is to completely separate your business and personal finances.

- Dedicated Business Accounts: Use a separate Venmo business profile (if available and suitable), or even better, a separate bank account and payment method (e.g., a business credit card) for all business income and expenses. This provides a clean audit trail.

- Avoid Commingling Funds: Refrain from using a personal Venmo account to receive business payments or to pay for business expenses. Mixing these funds makes reconciliation incredibly difficult and can raise red flags during an audit.

- Separate Invoicing: If you issue invoices for your services or products, ensure they direct clients to your business payment channels, not your personal Venmo.

This separation simplifies tax preparation, clarifies what’s income and what isn’t, and protects your personal assets in case of business liabilities.

Leveraging Financial Tools for Tracking and Reconciliation

While Venmo provides a transaction history, more robust financial tools can significantly streamline your record-keeping:

- Accounting Software: Small business accounting software (e.g., QuickBooks, Xero, FreshBooks) can link to your bank accounts and Venmo business profile, allowing you to categorize income and expenses, track mileage, and generate financial reports.

- Spreadsheets: For very small-scale operations, a well-organized spreadsheet can suffice. Track dates, payees/payers, amounts, descriptions, and categories (e.g., “freelance income,” “office supplies,” “personal gift”).

- Receipt Management Apps: Apps that allow you to photograph and categorize receipts digitally can be invaluable for tracking deductible expenses, especially for cash or one-off purchases.

Regularly reconciling your Venmo transactions with your external records and financial statements ensures accuracy and catches discrepancies early.

Responding to a 1099-K and Fulfilling Your Tax Obligations

Even with diligent record-keeping, receiving a Form 1099-K can be daunting. It’s not a bill, but rather an information return that the IRS has also received. Your response to it, and how you integrate it into your tax return, is critical.

Understanding Your 1099-K Form and Its Implications

A 1099-K reports the gross amount of all reportable payment transactions processed by a TPPN for you in a calendar year. “Gross amount” means the total without subtracting fees, credits, refunds, or any other adjustments. Crucially, the 1099-K does not distinguish between personal and business payments. It simply reports the total dollar volume of transactions that the payment processor could classify as business-related under their internal algorithms.

Receiving a 1099-K means the IRS is aware of the reported amount. Failing to account for this on your tax return can trigger an inquiry or audit. However, receiving one does not automatically mean that the entire amount reported is taxable income.

Reconciling Reported Income with Actual Taxable Revenue

This is where your meticulous record-keeping becomes invaluable. If you receive a 1099-K, you must reconcile the reported gross amount with your actual taxable income.

- Review the 1099-K: Check the payee information, tax identification number, and the gross amount reported.

- Compare to Your Records: Cross-reference the 1099-K amount with your own detailed records of business income received via Venmo.

- Identify Non-Taxable Portions: Subtract any personal reimbursements, gifts, or other non-taxable transactions that might have been inadvertently included in the 1099-K’s gross total. This is particularly common if you use a single Venmo account for both personal and business use.

- Report Net Taxable Income: On your Schedule C (Profit or Loss from Business) or other relevant income schedules, you will report your actual gross receipts, which should only include your taxable business income. If your 1099-K is significantly higher than your actual taxable income, you may need to provide an explanation or attach a statement detailing the reconciliation.

It is always better to proactively address discrepancies with the IRS rather than waiting for them to inquire.

What to Do If You Don’t Receive a 1099-K but Have Taxable Income?

Just because you don’t receive a 1099-K doesn’t mean you’re off the hook for taxes. If you earned taxable income through Venmo (or any other method) that falls below the reporting threshold for a 1099-K, you are still legally obligated to report that income to the IRS. Taxable income is taxable regardless of whether a TPPN issues an information return.

Failing to report taxable income, even small amounts, can lead to penalties, interest, and even criminal prosecution in severe cases. Always err on the side of caution and report all income accurately. Use your own records to determine your total gross receipts from business activities.

Proactive Financial Planning and Seeking Expert Guidance

Managing taxes in the digital age requires a proactive approach. The tax landscape is ever-evolving, and platforms like Venmo are continually adjusting their features and compliance mechanisms. Taking steps now can prevent headaches and potential penalties down the line.

The Value of Regular Financial Reviews

Don’t wait until tax season to sort through a year’s worth of transactions. Implement a system for regular financial reviews:

- Monthly or Quarterly Reconciliation: Set aside time each month or quarter to review your Venmo transactions, categorize them, and reconcile them with your bank statements and accounting software.

- Estimate Quarterly Taxes: If you anticipate earning significant income through Venmo or other self-employment activities, you likely need to pay estimated taxes quarterly. Regular reviews help you accurately estimate these payments, avoiding underpayment penalties.

- Budgeting and Forecasting: Understanding your income and expenses through Venmo (and all other sources) allows for better budgeting and financial forecasting, contributing to overall financial stability.

When and How to Consult a Qualified Tax Professional

For many, the complexities of tax law, especially regarding digital transactions, warrant professional guidance.

- When to Consult: If your income sources are diverse, you’re starting a new business, you’ve received a 1099-K with confusing amounts, or you’re unsure about specific deductions or reporting requirements, consulting a professional is highly recommended.

- Choosing a Professional: Look for a Certified Public Accountant (CPA) or an Enrolled Agent (EA) with experience in small business taxes, self-employment, and digital transactions. They can provide personalized advice, help with reconciliation, and ensure your tax return is accurate and compliant.

- Benefits: A tax professional can help you optimize deductions, navigate complex situations, represent you in case of an IRS inquiry, and provide peace of mind that your financial affairs are in order.

Staying Abreast of Evolving Tax Regulations for Digital Transactions

The regulatory environment for digital payment platforms is dynamic. Government bodies, including the IRS, are continuously adapting rules to keep pace with technological advancements and evolving economic models.

- IRS Publications: Regularly check IRS publications and announcements, especially those related to third-party payment networks and gig economy income.

- Professional Updates: Subscribe to newsletters from reputable tax and financial professionals who provide updates on tax law changes.

- Financial News: Follow reliable financial news sources that report on tax policy developments.

By staying informed and maintaining diligent financial practices, you can confidently navigate the tax landscape of platforms like Venmo, ensuring compliance and optimizing your financial well-being. The goal is not to “avoid Venmo tax” in the sense of evading obligations, but rather to understand and comply with tax laws intelligently and efficiently, ensuring you only pay what you legitimately owe and no more.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.