In the rapidly evolving landscape of digital finance, the boundary between online payment platforms and traditional banking continues to blur. PayPal, once primarily a service for peer-to-peer transfers and eBay purchases, has transformed into a comprehensive financial ecosystem. For those looking to bridge the gap between their digital balance and real-world spending, the PayPal card suite offers a bridge. Whether you are looking for a way to access your freelance earnings immediately or seeking a high-yield cashback credit card to optimize your monthly expenses, understanding how to apply for and utilize a PayPal card is a critical step in modern personal finance management.

Understanding the PayPal Card Ecosystem

Before beginning the application process, it is essential to distinguish between the two primary offerings available. PayPal does not offer a “one size fits all” card; rather, it provides options tailored to different financial needs and credit profiles. Selecting the right one is the first step in optimizing your financial strategy.

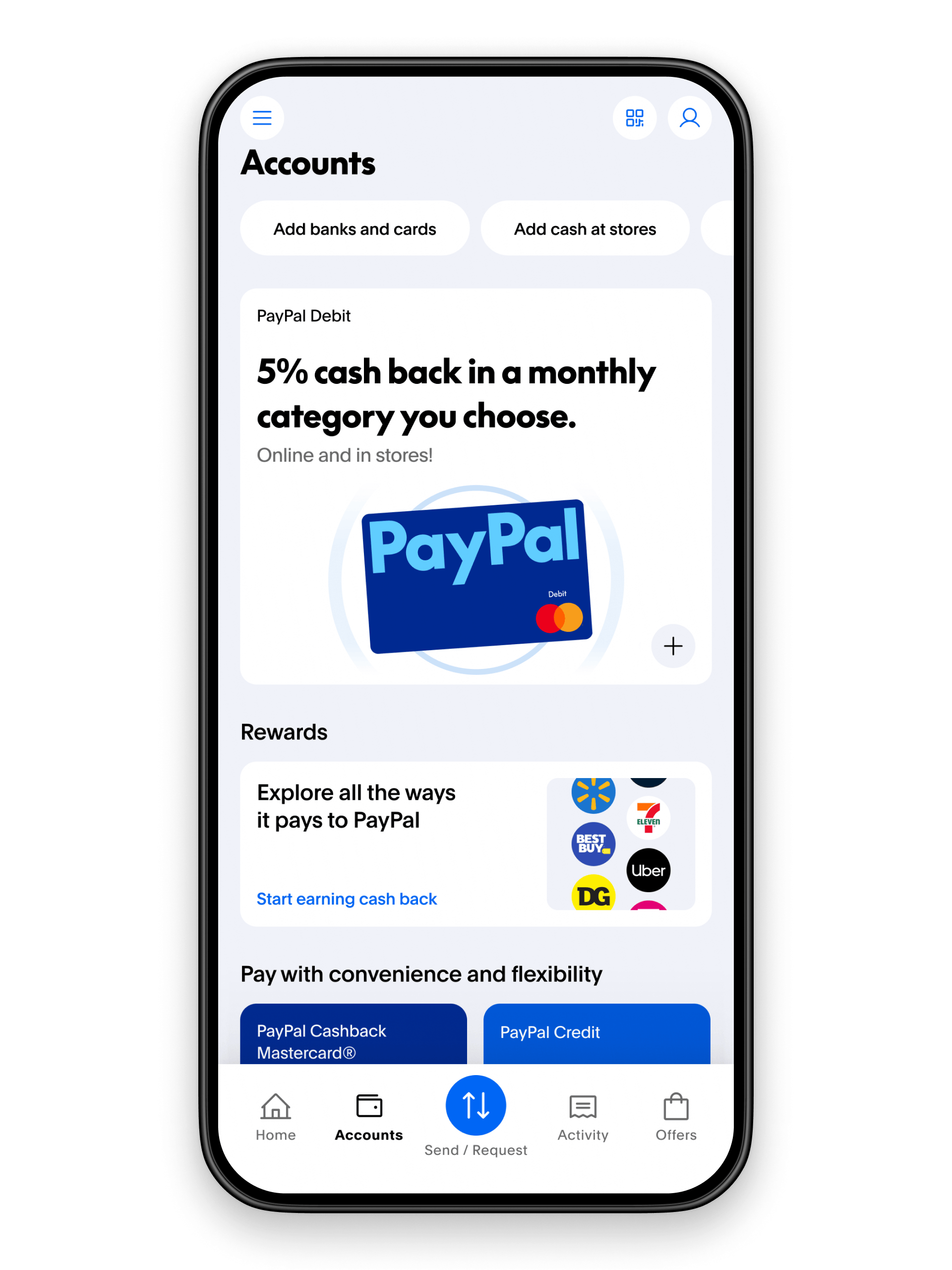

PayPal Cashback Mastercard® vs. PayPal Debit Card

The PayPal Cashback Mastercard is a traditional credit card issued in partnership with Synchrony Bank. It is designed for consumers looking to build credit or maximize rewards, offering significant cashback percentages on purchases made through the PayPal checkout and a flat rate on everything else. On the other hand, the PayPal Debit Card (formerly known as the PayPal Cash Card) is linked directly to your PayPal Balance account. It acts like a standard bank debit card, allowing you to spend the funds you already have without a credit check.

Why Your Choice Depends on Your Financial Goals

If your goal is to earn passive income through rewards, the Mastercard is the superior choice. However, if you are focused on strict budgeting or need immediate access to funds received from a side hustle, the Debit Card is the more practical tool. From a personal finance perspective, the credit card requires disciplined management to avoid interest charges, whereas the debit card provides a safety net against debt by only allowing you to spend what you possess.

The Step-by-Step Application Process

Applying for a financial product should never be done impulsively. It requires a clear understanding of the requirements and a systematic approach to ensure a high probability of approval and a seamless integration into your digital wallet.

Eligibility Requirements and Credit Score Factors

For the PayPal Debit Card, the barrier to entry is low. You must have a PayPal Balance account in good standing and a verified identity. There is generally no credit pull for the debit version, making it an excellent tool for those rebuilding their financial standing.

The PayPal Cashback Mastercard, however, requires a hard credit inquiry. While PayPal does not publicly disclose a minimum credit score, a “Good” to “Excellent” rating (typically 670 or higher) significantly increases your chances of approval. Before applying, it is wise to check your credit report for any inaccuracies that might hinder your application. Ensure your income information is up to date within your PayPal profile, as debt-to-income ratios play a pivotal role in Synchrony Bank’s lending decisions.

Navigating the Digital Application via Web or App

The application process is designed to be frictionless. Log in to your PayPal account and navigate to the “Cards” or “Finances” section.

- Selection: Choose between the Credit or Debit option.

- Verification: You will be asked to confirm your legal name, Social Security Number, and residential address. For the credit card, you must also provide your annual gross income.

- Review: Carefully read the Terms and Conditions. Pay close attention to the Schumer Box for the Mastercard, which outlines the APR, late fees, and grace periods.

- Submission: Once submitted, debit card approvals are usually instant. Credit card applications may receive an instant decision, or they may be put into “pending” status if the bank requires additional verification.

Maximizing Financial Benefits and Rewards

Once you have successfully applied for and received your card, the focus shifts from acquisition to optimization. In the world of personal finance, a card is only as valuable as the benefits you extract from it.

Strategies for 3% Cashback and Merchant Offers

The PayPal Cashback Mastercard currently stands out in the market by offering 3% cashback on purchases made through PayPal at checkout. This is a significant margin compared to the industry standard of 1.5% to 2%. To maximize this, you should audit your recurring bills—such as insurance, utilities, or streaming services—to see which can be paid via the PayPal portal.

Additionally, the PayPal app often features “Merchant Offers” that provide stackable rewards. By activating these offers before using your PayPal card, you can effectively earn double rewards: once from the card’s base rate and again from the specific merchant promotion. This “stacking” method is a cornerstone of savvy online income management and wealth preservation.

Integrating the Card into Your Monthly Budget

For the PayPal Debit Card user, the card serves as an excellent tool for “envelope budgeting.” By transferring a specific “discretionary spending” amount into your PayPal balance each month, you can use the card for coffee, dining out, or entertainment. Once the balance is zero, your spending for that category stops. This prevents the “leakage” often seen in primary bank accounts where automated bills and daily spending mingle, making it difficult to track net savings.

Security and Financial Management Features

In an era of increasing digital fraud, the security of your financial tools is as important as the rewards they offer. PayPal’s infrastructure provides layers of protection that traditional plastic cards often lack.

Real-Time Monitoring and Fraud Protection

Both the debit and credit versions of the PayPal card offer instant push notifications. The moment a transaction occurs, you receive an alert on your smartphone. This real-time feedback loop is essential for identifying unauthorized transactions immediately.

Furthermore, if you misplace your card, the PayPal app allows you to “freeze” the card instantly. This prevents any new transactions without requiring you to cancel the card entirely—a feature that provides peace of mind for the frequent traveler or the busy professional. From a digital security standpoint, using a PayPal card also adds a layer of obfuscation between your primary bank account and the merchants you frequent, reducing the risk of your main checking account being compromised.

Managing Debt and Interest Rates Responsibly

For Mastercard users, the primary financial risk is the interest rate. To truly benefit from a rewards card, the balance must be paid in full every month. PayPal’s interface makes this easy by allowing you to set up Autopay directly from your linked bank account or your PayPal balance. Within the “Money” niche of personal finance, the goal is to use the bank’s money for 30 days for free, collect the cashback, and exit the month with zero debt. If you carry a balance, the high APR associated with most store and tech-branded credit cards will quickly negate any rewards earned.

The Role of PayPal in a Modern FinTech Portfolio

Applying for a PayPal card is more than just getting a new piece of plastic; it is an entry into a broader FinTech strategy. As traditional banks struggle to keep pace with the speed of digital commerce, platforms like PayPal offer a more agile alternative.

Comparing PayPal to Traditional Banking Alternatives

Traditional bank cards often have lag times in transaction posting and rigid rewards structures. PayPal’s integration with thousands of online vendors gives it a “home-field advantage” in the e-commerce space. While a traditional bank might offer a 1% “everything” card, the specialized 3% tier offered by PayPal for online shopping makes it a powerful secondary or tertiary card in a “trifecta” credit card strategy, where different cards are used for specific categories (e.g., one for groceries, one for gas, and PayPal for online retail).

Long-term Financial Health and Digital Payments

Ultimately, the decision to apply for a PayPal card should align with your long-term financial health. For those participating in the gig economy or receiving online income, the PayPal card provides the liquidity necessary to manage a business or a household. By centralizing spending, rewards, and security within a single app, you reduce the cognitive load of financial management.

In conclusion, the application process for a PayPal card is straightforward, but the strategic implications are deep. By choosing the card that aligns with your credit profile and spending habits, and by employing rigorous repayment and security habits, you can transform a simple payment tool into a powerful engine for cashback and financial organization. As we move toward a more digital-centric economy, leveraging these specialized financial tools is no longer optional—it is a prerequisite for financial success.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.