Navigating the labyrinthine world of personal finance can be daunting, especially when faced with substantial debt. For millions, the prospect of loan forgiveness offers a beacon of hope – a potential pathway to significant financial relief and renewed economic freedom. Loan forgiveness, in its essence, is the cancellation of all or part of a borrower’s outstanding debt, often under specific circumstances or in exchange for meeting certain criteria. It’s not a universal handout, but rather a targeted mechanism designed to support individuals in particular professions, those facing severe financial hardship, or as a response to systemic economic challenges.

![]()

The process of applying for loan forgiveness is rarely straightforward. It demands meticulous attention to detail, a thorough understanding of eligibility requirements, and often, considerable patience. From student loans that burden graduates for decades to mortgage and small business loans impacted by unforeseen crises, various forms of debt may be eligible for some form of reprieve. Understanding the specific programs available, gathering the correct documentation, and adhering strictly to application protocols are critical steps toward successfully reducing or eliminating your financial obligations. This comprehensive guide will dissect the landscape of loan forgiveness, outlining key pathways, detailing the application process, and offering crucial insights to help you secure the relief you may be entitled to.

Understanding the Landscape of Loan Forgiveness

The concept of loan forgiveness is multifaceted, varying significantly based on the type of loan and the specific program offering the relief. It’s crucial to distinguish between different forms of forgiveness and the underlying reasons they exist.

What is Loan Forgiveness?

At its core, loan forgiveness means that you are no longer required to repay some or all of your loan balance. This is distinct from loan deferment or forbearance, where payments are temporarily paused but the principal balance remains. Forgiveness typically results in the elimination of the debt, though sometimes the forgiven amount might be considered taxable income by the IRS, a critical point often overlooked by applicants. The specific terms of forgiveness are dictated by federal, state, or institutional programs, each with its own set of rules and conditions.

Why is Loan Forgiveness Available?

Loan forgiveness programs are typically established for several key reasons:

- Public Service Incentives: To encourage individuals to enter and remain in critical public service professions (e.g., teaching, nursing, government work) that are often underpaid relative to the education required.

- Financial Hardship Relief: To provide a safety net for borrowers experiencing severe economic distress, making it impossible for them to repay their loans.

- Remedial Action: In cases where borrowers have been defrauded by educational institutions or faced predatory lending practices, forgiveness can serve as a form of restitution.

- Economic Stimulus/Crisis Response: During widespread economic downturns or crises (like the COVID-19 pandemic), governments may institute broad forgiveness or relief programs to stabilize the economy and support struggling sectors.

- Disability or Death: To relieve the burden of debt for individuals who become permanently disabled or for the estates of deceased borrowers.

Common Types of Forgivable Loans

While many types of loans exist, the most common categories for forgiveness programs include:

- Student Loans: The largest and most complex category, encompassing federal and sometimes private student loans. Programs like Public Service Loan Forgiveness (PSLF) and Income-Driven Repayment (IDR) forgiveness are prominent examples.

- Mortgage Loans: While less common for full forgiveness, programs exist for homeowners in distress, often involving principal reductions or partial forgiveness to prevent foreclosure. Examples include programs like the Home Affordable Refinance Program (HARP) or state-specific housing assistance.

- Small Business Loans: Historically, these were less frequently forgiven, but programs like the Paycheck Protection Program (PPP) during the COVID-19 pandemic offered significant forgiveness opportunities under specific conditions related to job retention and eligible expenses.

Understanding which category your loan falls into is the foundational first step, as it dictates the specific programs you might be eligible for and the corresponding application process.

Key Pathways to Student Loan Forgiveness

Student loan debt represents a colossal financial burden for millions, making student loan forgiveness programs particularly impactful. Federal student loans, unlike most private loans, come with various options for forgiveness, discharge, or cancellation.

Public Service Loan Forgiveness (PSLF)

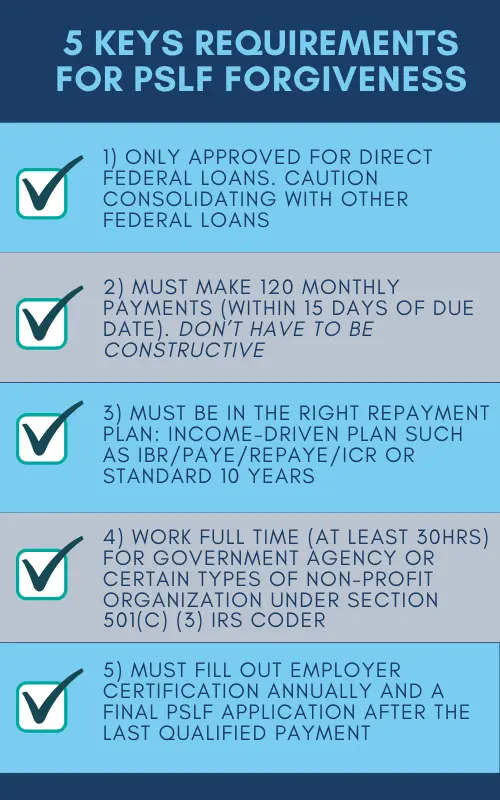

The Public Service Loan Forgiveness (PSLF) program is designed to encourage individuals to work in public service. After making 120 qualifying monthly payments while working full-time for a qualifying employer, the remaining balance on your Direct Loans may be forgiven.

- Eligibility: You must work full-time for a U.S. federal, state, local, or tribal government organization, or a qualifying non-profit organization.

- Qualifying Payments: Payments must be made on a Direct Loan, under a qualifying income-driven repayment plan, and on time.

- Application Process: You must submit the PSLF & Temporary Expanded PSLF (TEPSLF) Certification & Application Form (PSLF Form) annually or whenever you change employers. This form certifies your employment and qualifying payments. After 120 payments, you submit the same form to apply for forgiveness.

Income-Driven Repayment (IDR) Forgiveness

Income-Driven Repayment (IDR) plans (such as SAVE, PAYE, IBR, and ICR) set your monthly student loan payment based on your income and family size. A significant benefit of these plans is that any remaining loan balance is forgiven after 20 or 25 years of qualifying payments, depending on the plan and when you took out your loans.

- Eligibility: Applies to most federal student loans. You must consistently make payments under an IDR plan.

- Qualifying Payments: Payments count towards the 20/25-year timeline. Periods of deferment, forbearance, and economic hardship may also count under certain circumstances or waivers.

- Application Process: You must enroll in an IDR plan and recertify your income and family size annually. The forgiveness is generally automatic once you hit the payment threshold, but it’s crucial to keep meticulous records.

Teacher Loan Forgiveness

This program offers up to $17,500 in loan forgiveness for eligible teachers who teach full-time for five complete and consecutive academic years in certain low-income schools or educational service agencies.

- Eligibility: Must be a highly qualified teacher in a designated elementary or secondary school serving low-income families.

- Qualifying Service: Five consecutive years of full-time teaching. The amount of forgiveness depends on the subject taught (e.g., highly qualified math, science, or special education teachers can receive up to $17,500, while others may receive up to $5,000).

- Application Process: After completing your five years of service, you submit the Teacher Loan Forgiveness Application to your loan servicer.

Borrower Defense to Repayment & Total and Permanent Disability (TPD) Discharge

These are specific types of forgiveness based on particular circumstances:

- Borrower Defense to Repayment: Forgiveness is available if your school misled you or engaged in other misconduct in violation of state law related to your federal student loans or the educational services for which the loans were provided.

- Total and Permanent Disability (TPD) Discharge: If you become totally and permanently disabled, you may be eligible to have your federal student loans discharged. This typically requires documentation from a physician, the Social Security Administration, or the Department of Veterans Affairs.

Each student loan forgiveness program has specific nuances. Diligently researching the one that best fits your situation is paramount.

Navigating Mortgage and Business Loan Forgiveness Programs

While less common than student loan forgiveness, specific circumstances and economic conditions have led to the creation of forgiveness opportunities for mortgage and small business loans.

Mortgage Loan Forgiveness

Direct mortgage loan forgiveness is rare outside of specific, often crisis-driven, government initiatives or as a result of a short sale or deed-in-lieu of foreclosure.

- Historical Context: Programs like the Home Affordable Refinance Program (HARP) or state-specific Hardest Hit Fund (HHF) provided relief during the 2008 financial crisis. These often focused on principal reductions or refinancing, which is a form of partial forgiveness or debt restructuring rather than outright cancellation.

- Foreclosure Alternatives: If you face severe financial distress and cannot make your mortgage payments, your lender might offer options like a short sale (selling your home for less than you owe, with the lender forgiving the difference) or a deed-in-lieu of foreclosure (giving your home back to the lender, who then forgives the debt). These situations often have significant credit implications and potential tax consequences.

- Application Process: Eligibility for mortgage relief programs is highly dependent on your income, hardship, and loan-to-value ratio. You would typically contact your mortgage servicer directly or seek guidance from a HUD-approved housing counselor. Documentation usually includes proof of income, hardship letters, and financial statements.

Small Business Loan Forgiveness (e.g., PPP during COVID-19)

The most prominent recent example of widespread small business loan forgiveness was the Paycheck Protection Program (PPP) implemented during the COVID-19 pandemic. This program provided forgivable loans to small businesses to help them keep their workforce employed during the economic disruption.

- Eligibility: Businesses had to meet specific size standards and demonstrate a need for the loan.

- Forgiveness Criteria: Forgiveness was primarily tied to using a certain percentage (typically 60%) of the loan funds for payroll costs over a specified “covered period” (e.g., 8 or 24 weeks). The remaining funds could be used for other eligible expenses like rent, utilities, and mortgage interest.

- Application Process: Borrowers applied for forgiveness through their lender, submitting detailed documentation of how the funds were spent (payroll records, utility bills, rent receipts, etc.). The process was complex and involved specific forms (e.g., Form 3508, 3508S, 3508EZ) and calculations to determine the forgivable amount.

While the PPP program is no longer active for new loans, its structure provides a template for how future government-led business loan forgiveness programs might operate in response to economic crises. It underscores the importance of stringent record-keeping and adherence to specific usage guidelines.

The Application Process: A Step-by-Step Guide

Regardless of the type of loan or forgiveness program, a systematic approach to the application process significantly increases your chances of success.

Step 1: Determine Eligibility

This is the most critical first step. Do not assume you qualify.

- Research Thoroughly: Visit the official websites of the program (e.g., Federal Student Aid for student loans, SBA for business loans, or your lender for mortgage relief) to understand the precise eligibility requirements.

- Review Your Loan Documents: Confirm the type of loan you have (federal vs. private, Direct Loan vs. FFELP, conventional vs. FHA mortgage, etc.), as this directly impacts program eligibility.

- Assess Your Circumstances: Do you meet the income requirements, employment criteria, or hardship definitions? Be honest and realistic about your situation.

Step 2: Gather Necessary Documentation

Forgiveness applications are document-intensive. Start collecting these items well in advance.

- Proof of Income: Pay stubs, tax returns (W-2s, 1099s), bank statements.

- Proof of Employment/Service: Employer certifications, letters of employment, pay stubs with employer details, service agreements (for PSLF, Teacher Loan Forgiveness).

- Loan Statements: Official statements from your loan servicer showing your loan balances, payment history, and loan type.

- Financial Hardship Documentation (if applicable): Medical bills, unemployment benefits, divorce decrees, foreclosure notices, property tax statements.

- Expense Records (for business loans): Payroll records, utility bills, rent receipts, mortgage interest statements, invoices.

- Identity Verification: Driver’s license, passport, Social Security card.

Organize these documents meticulously, perhaps creating a digital folder and physical binder for easy access and backup.

Step 3: Complete the Application Form

This is where attention to detail is paramount.

- Obtain the Correct Form: Ensure you are using the most current version of the application form for your specific program.

- Read Instructions Carefully: Follow all instructions precisely. Incomplete or incorrectly filled-out applications are the most common reason for delays or denials.

- Be Truthful and Accurate: Provide accurate information. Misrepresentation can lead to severe penalties.

- Fill Out Completely: Do not leave any sections blank. If a question is not applicable, mark it as such (e.g., “N/A”).

- Seek Clarification: If you are unsure about any part of the application, contact the program administrator, your loan servicer, or a financial advisor.

Step 4: Submit and Follow Up

Submission is not the end of the process.

- Submission Method: Follow the specified submission method (online portal, mail, fax). If mailing, use certified mail with a return receipt requested to have proof of submission.

- Keep Copies: Always keep a complete copy of your submitted application and all supporting documents.

- Confirm Receipt: Follow up with the recipient (loan servicer, government agency) to confirm that your application was received and is being processed.

- Monitor Status: Regularly check the status of your application. Be prepared to respond to requests for additional information promptly.

- Be Patient: Forgiveness processes can take weeks or even months, especially for complex programs or during periods of high volume.

Step 5: Understand Tax Implications

Forgiven debt can sometimes be considered taxable income by the IRS.

- Consult a Tax Professional: Before applying, understand the potential tax consequences of the forgiveness you are seeking.

- Insolvency Exclusion: If you are insolvent (your total liabilities exceed your total assets) at the time the debt is forgiven, you may be able to exclude the forgiven amount from your taxable income. However, this is complex and often requires professional guidance.

- Specific Program Exemptions: Some forgiveness programs (e.g., PSLF for federal student loans) specifically state that the forgiven amount is tax-free. It’s crucial to verify this for your particular program.

Common Pitfalls and Expert Tips

The path to loan forgiveness can be fraught with challenges. Being aware of common pitfalls and leveraging expert advice can significantly improve your odds.

Avoiding Application Errors

- Incomplete Applications: The single most common reason for denial. Double-check every field.

- Incorrect Documentation: Submitting the wrong type of document or documents that don’t meet the program’s specifications.

- Missed Deadlines: Failing to submit applications or required follow-up documents by the specified deadlines.

- Misunderstanding Eligibility: Applying for a program you do not fully qualify for, wasting time and effort.

The Importance of Record-Keeping

Maintain an organized system for all correspondence, submitted forms, payment histories, and any documentation related to your loans and the forgiveness process. This is invaluable for tracking progress, resolving discrepancies, and proving your case if issues arise. Digital and physical backups are highly recommended.

Seeking Professional Guidance

- Non-Profit Credit Counselors: Reputable non-profit organizations offer free or low-cost advice on managing debt and navigating forgiveness programs. Ensure they are accredited.

- Financial Advisors/Planners: For complex situations, particularly those involving tax implications or significant assets, a certified financial planner or advisor can provide tailored advice.

- Attorneys: In cases of borrower defense claims or disputes with lenders, legal counsel may be necessary.

Be wary of companies that charge hefty fees promising guaranteed forgiveness. Official programs are generally free to apply for, and any fees usually relate to professional advice, not the application itself.

Staying Informed About Program Changes

Loan forgiveness programs, especially those administered by the government, can change. Requirements might be updated, new waivers introduced, or programs phased out.

- Subscribe to Official Updates: Sign up for email alerts from official sources (e.g., Federal Student Aid website, SBA announcements).

- Regularly Check Websites: Periodically revisit the program’s official website for the latest news and FAQs.

- Consult Reliable News Sources: Follow reputable financial news outlets that cover personal finance and government policy changes.

Successfully applying for loan forgiveness requires diligence, patience, and a methodical approach. It is not an overnight solution but a strategic financial maneuver that, when executed correctly, can lead to substantial relief and a healthier financial future. By understanding the available programs, meticulously preparing your application, and proactively managing the process, you can significantly enhance your chances of achieving the debt relief you seek.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.