In an increasingly digital world, managing personal finances has evolved dramatically. Among the most significant shifts is the ease with which individuals can now access crucial financial tools, including credit cards. Once a process often involving lengthy paper applications and in-person bank visits, applying for a credit card has largely moved online, offering unparalleled convenience, speed, and transparency. However, this accessibility also necessitates a deeper understanding of the process, the implications of credit, and the best practices for responsible financial management.

A credit card, when used wisely, is far more than just a payment tool; it’s a cornerstone of modern personal finance. It can help build a strong credit history, unlock valuable rewards, provide financial flexibility in emergencies, and even offer purchase protection. Yet, without a clear strategy and an understanding of its potential pitfalls, a credit card can also lead to debt and financial stress. This comprehensive guide will navigate you through the entire online credit card application process, from preparation to responsible usage, ensuring you make informed decisions that align with your financial goals within the Money category.

Understanding Credit Cards in Your Financial Toolkit

Before diving into the online application, it’s crucial to grasp the fundamental role credit cards play in your financial ecosystem. They are powerful instruments that, like any tool, require skill and knowledge to wield effectively.

The Dual Role of Credit Cards: Benefits and Risks

Credit cards offer a host of compelling benefits that can significantly enhance your financial life. They provide unparalleled convenience, allowing you to make purchases without carrying large amounts of cash. Many cards offer robust rewards programs, from cashback on everyday spending to travel points that can unlock free flights and hotel stays. For those keen on personal finance, perhaps the most critical benefit is their ability to help build a strong credit history. A good credit score is vital for securing loans for a home or car, renting an apartment, and sometimes even for employment. Furthermore, credit cards often come with consumer protections, such as fraud liability limits and extended warranties on purchases.

However, the convenience of credit cards comes with inherent risks. The primary danger is accumulating high-interest debt. If balances aren’t paid in full each month, interest charges can quickly compound, leading to a debt spiral that can be challenging to escape. Late payments can incur fees and severely damage your credit score, making future borrowing more expensive or impossible. A lack of discipline or an unforeseen financial emergency can turn a useful financial tool into a significant liability. Understanding this delicate balance is the first step toward responsible credit card use.

Types of Credit Cards and Their Financial Implications

The credit card market is diverse, with offerings tailored to virtually every financial profile and spending habit. Choosing the right card is paramount to maximizing benefits and minimizing risks.

- Rewards Cards: These cards offer cashback, points, or miles on purchases. They are ideal for individuals who pay their balance in full monthly and want to be rewarded for their spending. The financial implication is that while rewards are enticing, a high Annual Percentage Rate (APR) means carrying a balance negates any benefits.

- Low-Interest/Balance Transfer Cards: Designed for those who anticipate carrying a balance or wish to consolidate existing debt from higher-interest cards. They often feature introductory 0% APR periods. The financial implication here is the opportunity to save significant money on interest, but only if the balance is paid off before the promotional period ends.

- Secured Credit Cards: These cards require a cash deposit, which typically acts as your credit limit. They are an excellent option for individuals with no credit history or poor credit looking to build or rebuild their score. The financial implication is that they require an upfront commitment but offer a safe way to demonstrate creditworthiness.

- Student Credit Cards: Tailored for college students, often with lower credit limits and educational resources. They help young adults begin building credit responsibly.

- Travel Credit Cards: These cards offer accelerated rewards on travel-related spending, lounge access, and travel insurance benefits. They are best for frequent travelers who can leverage these perks.

Key Factors Lenders Consider

When you apply for a credit card, lenders assess your financial health to determine your creditworthiness. Understanding these factors can help you prepare a stronger application.

- Credit Score: This three-digit number (FICO or VantageScore) is a summary of your credit history. A higher score indicates lower risk.

- Income: Lenders want to ensure you have sufficient income to manage new debt obligations.

- Debt-to-Income Ratio (DTI): This compares your total monthly debt payments to your gross monthly income. A lower DTI indicates more financial flexibility.

- Credit History Length: A longer history of responsible credit use is generally viewed favorably.

- Payment History: A consistent record of on-time payments is crucial.

- Existing Debt: The amount of outstanding debt you currently carry.

Preparing for Your Online Application Journey

A successful online credit card application begins long before you click “submit.” Preparation is key to not only getting approved but also securing the best terms and avoiding potential pitfalls.

Checking Your Credit Score and Report

Your credit score is the most influential factor in a lender’s decision. Before applying, obtain a free copy of your credit report from each of the three major credit bureaus (Equifax, Experian, TransUnion) via AnnualCreditReport.com. Review these reports meticulously for any errors or inaccuracies that could be negatively impacting your score. If you find discrepancies, dispute them immediately. Additionally, knowing your FICO or VantageScore provides a clear benchmark of where you stand and helps you identify cards for which you’re a good candidate. Many banks and credit card companies now offer free credit score access to their customers.

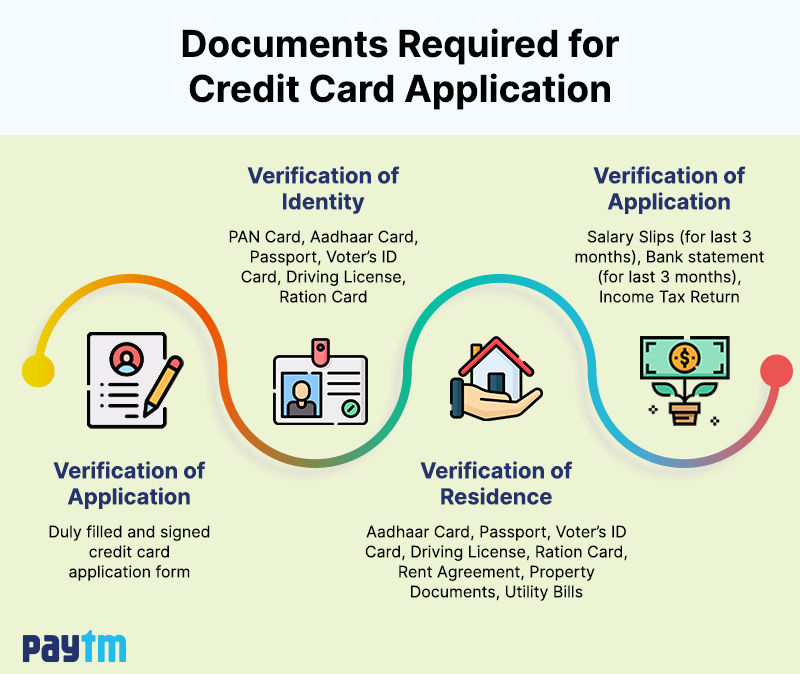

Gathering Necessary Financial Documentation

While online applications streamline the process, you’ll still need specific information readily available. Having these documents on hand prevents delays and ensures accuracy. Typically, this includes:

- Personal Identification: Government-issued ID (driver’s license, passport) for identity verification.

- Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN): Essential for checking your credit history.

- Income Verification: Recent pay stubs, W-2 forms, tax returns, or bank statements if you are self-employed.

- Residential Information: Your current address and previous addresses if you’ve moved recently.

- Employment Information: Employer’s name, address, and phone number.

- Bank Account Information: For setting up payments or confirming financial stability.

Defining Your Credit Card Needs and Goals

Not all credit cards are created equal, and neither are all financial needs. Before applying, honestly assess what you want from a credit card.

- Are you looking to build credit from scratch? A secured card or a student card might be appropriate.

- Do you want to earn rewards on your spending? Consider cashback, travel, or points cards.

- Do you need to transfer a high-interest balance? A 0% APR balance transfer card could save you money.

- Are you trying to minimize fees and interest? Look for cards with no annual fee and a competitive APR.

Aligning your financial goals with the right card type ensures you choose a product that genuinely benefits your money management strategy.

The Step-by-Step Online Application Process

With your preparation complete, you’re ready to navigate the digital landscape of online credit card applications. This process is designed for efficiency but requires careful attention to detail.

Researching and Comparing Card Offers

The internet is awash with credit card offers. Utilize reputable online comparison websites (e.g., NerdWallet, Credit Karma, The Points Guy) to filter and compare cards based on your defined needs. Pay close attention to:

- Annual Percentage Rate (APR): Especially for purchases and balance transfers.

- Annual Fees: Is there one, and is it offset by rewards or benefits?

- Rewards Structure: How are points/cashback earned and redeemed? Are there spending caps?

- Sign-Up Bonuses: What are the requirements to earn them?

- Introductory Offers: 0% APR periods, bonus rewards.

- Other Fees: Foreign transaction fees, late payment fees, cash advance fees.

- Credit Score Requirements: To gauge your likelihood of approval.

Read the fine print (terms and conditions) thoroughly before making a decision.

Navigating the Online Application Form

Once you’ve selected a card, access the application directly from the issuer’s official website. The online form will typically guide you through several sections:

- Personal Information: Name, address, date of birth, SSN/ITIN, contact details.

- Employment Information: Employer name, occupation, annual income.

- Financial Information: Monthly housing payment, total monthly debt payments, other income sources.

- Security Questions: To verify your identity.

It is crucial to fill out every field accurately. Even minor discrepancies can lead to delays or denial. Double-check all entries before proceeding. Some applications might include pre-qualification tools that allow you to check your eligibility without a hard inquiry on your credit report, which can be a valuable first step.

Understanding Application Submission and Decision

After completing the form, you’ll typically be prompted to review and submit your application. What happens next can vary:

- Instant Approval: For applicants with strong credit and clear financial profiles, an immediate approval decision is common. You’ll receive details about your credit limit and how long until your card arrives.

- Pending Review: If your application requires further verification or falls into a gray area, it may go into manual review. The issuer might request additional documents or conduct a more thorough background check. You’ll typically receive an email or letter detailing the next steps.

- Denial: If your application is denied, the lender is legally required to provide a reason (Adverse Action Notice). This notice is crucial as it highlights areas you need to improve to enhance your creditworthiness for future applications.

What Happens After Approval

Congratulations! If approved, the excitement begins.

- Receiving Your Card: Your physical card will arrive in the mail, usually within 7-10 business days.

- Activation: Follow the instructions to activate your card. This often involves a phone call or an online activation portal.

- Understanding Your Credit Limit and Statement Cycles: Familiarize yourself with your assigned credit limit and the date your statement closes each month, as this impacts when payments are due.

- Setting Up Online Account Access: Create an online account with the issuer to monitor transactions, view statements, and manage payments.

- Reviewing Cardholder Agreement: Take time to read the full cardholder agreement to understand all terms, conditions, and benefits.

Best Practices for Responsible Credit Card Management

Obtaining a credit card online is just the first step. Responsible management is where you truly leverage its benefits and avoid its pitfalls, integrating it seamlessly into your overall financial strategy.

Making Timely Payments

This is the golden rule of credit card management. Always pay at least the minimum amount due, and ideally, the full statement balance, by the due date. Late payments incur fees and are reported to credit bureaus, significantly harming your credit score. Set up automatic payments or calendar reminders to ensure you never miss a deadline.

Managing Your Credit Utilization Ratio

Your credit utilization ratio is the amount of credit you’re using compared to your total available credit. Lenders prefer to see this ratio below 30% (e.g., if you have a $10,000 limit, try to keep your balance below $3,000). A lower ratio indicates responsible credit use and positively impacts your credit score. Avoid “maxing out” your cards.

Understanding Interest and Fees

Be fully aware of your card’s APR, annual fee, foreign transaction fees, cash advance fees, and late payment fees. High APRs make carrying a balance extremely expensive. Minimize fees by avoiding cash advances and paying on time. If your card has an annual fee, ensure the rewards and benefits you receive justify the cost.

Leveraging Rewards and Benefits Wisely

If you have a rewards card, understand how to maximize your points, miles, or cashback. Strategically use the card for categories that offer bonus rewards. Redeem your rewards regularly, whether for travel, statement credits, or gift cards. However, never spend more than you normally would just to earn rewards; this defeats the purpose and can lead to debt.

Monitoring Your Accounts for Security

Regularly review your online statements and transactions for any unauthorized activity. Be vigilant against phishing attempts and identity theft. Report any suspicious charges to your card issuer immediately. Use strong, unique passwords for your online banking accounts and enable two-factor authentication for added security.

Troubleshooting and Next Steps for Aspiring Cardholders

Sometimes, the path to a credit card isn’t straightforward. Understanding how to handle setbacks and continue building your financial profile is crucial.

What to Do If Your Application is Denied

A denial is not the end of your credit journey. First, carefully review the Adverse Action Notice you receive; it will explain why you were denied. Common reasons include a low credit score, high debt-to-income ratio, insufficient income, or too many recent credit inquiries.

- Reconsideration: Some issuers allow you to call their reconsideration line to appeal the decision. Be polite, explain any mitigating circumstances, and highlight any positive aspects of your financial situation.

- Improve Your Credit Profile: Focus on the reasons for denial. If it’s a low credit score, work on paying bills on time, reducing debt, and correcting errors on your credit report.

- Wait and Reapply: If significant improvements are needed, take a few months to enhance your credit before applying again. Applying too frequently can further ding your score.

The Path to Building or Rebuilding Credit

For those with limited or damaged credit, there are viable paths to building a stronger financial foundation.

- Secured Credit Cards: As mentioned, these require a deposit but function like regular credit cards, reporting payments to credit bureaus.

- Authorized User: Becoming an authorized user on a trusted family member’s credit card can help, provided they manage the account responsibly.

- Credit-Builder Loans: Offered by some credit unions and community banks, these loans are designed to help you save money and build credit simultaneously.

- Experian Boost: This free service allows you to add positive payment history from utility and telecom bills to your Experian credit report, potentially increasing your FICO score.

Seeking Professional Financial Advice

If you’re overwhelmed by debt, struggling to manage your finances, or unsure how to navigate the complexities of credit, consider seeking help from a non-profit credit counseling agency. They can offer personalized advice, help create a budget, and even negotiate with creditors on your behalf. A certified financial planner can also provide comprehensive guidance on long-term financial planning, including the strategic use of credit products.

The ability to apply for a credit card online has transformed personal finance, offering convenience and speed that were once unimaginable. However, with this power comes the responsibility to understand the nuances of credit, make informed decisions, and manage your accounts diligently. By preparing thoroughly, understanding the application process, and adhering to best practices for responsible credit use, you can successfully leverage a credit card as a powerful tool to build a robust financial future. Always remember that a credit card is a means to an end – a stronger financial standing – not an end in itself.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.