In the intricate world of finance, percentages are not just mathematical symbols; they are the bedrock upon which crucial decisions are made, from personal budgeting to multi-million dollar investments. Understanding “how to add with percentages” transcends mere arithmetic; it empowers individuals and businesses to accurately assess financial scenarios, predict outcomes, and optimize strategies. Whether you’re grappling with interest rates, analyzing investment returns, or simply calculating a tip, a firm grasp of percentage addition is indispensable. This guide delves into the core principles, practical applications, and common pitfalls of adding percentages, providing a professional and insightful exploration tailored for the financially astute.

The Ubiquity of Percentages in the Financial World

Percentages permeate nearly every facet of our financial lives. They provide a standardized way to express proportions, changes, and relationships, making complex financial data digestible and comparable. Their omnipresence makes mastering their manipulation, particularly addition, a fundamental skill for financial literacy and success.

Interest Rates and Loan Calculations

For most individuals, one of the most frequent encounters with percentages is through interest rates. Whether it’s the annual percentage rate (APR) on a credit card, the interest charged on a mortgage, or the yield on a savings account, percentages dictate the cost of borrowing and the return on saving. When considering combining different loans, assessing variable rates, or understanding the cumulative cost over time, adding percentages (or rather, adding their impact) becomes critical. For instance, understanding how a base interest rate combined with various fees (also expressed as percentages) impacts the total cost of a loan is a direct application of this concept. It’s not always about adding the percentage numbers directly, but adding their effect on the principal.

Investment Returns and Portfolio Growth

Investors constantly deal with percentages when evaluating performance. Returns on stocks, bonds, mutual funds, and other assets are almost universally quoted as percentages. To assess the overall performance of a diversified portfolio, one often needs to consider the weighted average of different asset returns. Furthermore, understanding how consecutive percentage gains or losses compound over time is a sophisticated form of “adding” their effect. A 10% gain followed by a 5% gain doesn’t simply result in a 15% overall gain; the base changes after the first increase, leading to a slightly different, more beneficial outcome due to compounding. This illustrates a crucial nuance in percentage addition: context matters immensely.

Discounts, Taxes, and Tips in Daily Spending

Even in everyday transactions, percentages play a pivotal role. Sales taxes are added as a percentage of the purchase price, discounts are subtracted as a percentage, and gratuities are calculated as a percentage of the service cost. Often, these percentages need to be combined. For example, applying a discount to an item, and then calculating sales tax on the discounted price, or adding a tip after tax, requires a clear understanding of the order of operations and the base value at each step. Correctly calculating these “additions” can save money, prevent overspending, and ensure accurate payments.

Fundamental Principles of Percentage Addition

While the phrase “adding percentages” might sound straightforward, its application in finance often involves nuances that distinguish it from simple numerical addition. It’s rarely about adding 5% + 10% to get 15% directly, unless they refer to the same base. More often, it’s about combining the effects of percentages on a given value.

Adding Percentages of the Same Base Value

The simplest form of percentage addition occurs when multiple percentages apply to the exact same base value. In such cases, you can indeed add the percentages directly. For example, if a company offers a 10% bonus for performance and an additional 5% bonus for loyalty, both calculated on the same base salary, an employee effectively receives a 15% bonus on that salary.

- Example: Salary = $50,000. Performance Bonus = 10% ($5,000). Loyalty Bonus = 5% ($2,500). Total Bonus = 15% of $50,000 = $7,500.

This principle holds true for scenarios like multiple taxes on the same item, provided they are applied sequentially to the original price, or when different components of a fee are expressed as percentages of the same principal amount.

Understanding Consecutive Percentage Changes

One of the most common mistakes in financial calculations is incorrectly adding consecutive percentage changes. If an investment increases by 10% in year one and then by another 10% in year two, the total increase is not 20%. This is because the base value for the second year’s increase is the new, increased value after the first year.

- Calculation: Start with $100.

- Year 1: $100 + (10% of $100) = $100 + $10 = $110.

- Year 2: $110 + (10% of $110) = $110 + $11 = $121.

- Total increase: ($121 – $100) / $100 = 21%.

- The effective total change is (1 + P1) * (1 + P2) – 1, where P1 and P2 are the percentage changes in decimal form. For the example: (1 + 0.10) * (1 + 0.10) – 1 = 1.10 * 1.10 – 1 = 1.21 – 1 = 0.21 or 21%.

This principle of compounding is critical for understanding long-term investments, inflation, and debt accumulation.

Combining Different Percentage Rates (e.g., Sales Tax + Tip)

When different percentage rates apply to a transaction, the order of operations and the base value become crucial. Consider a restaurant bill where you need to add sales tax and a tip.

- Scenario 1: Tax then Tip on pre-tax amount. Most commonly, tips are calculated on the pre-tax subtotal. Sales tax is also calculated on the pre-tax subtotal.

- Meal Cost: $50

- Sales Tax: 8%

- Tip: 20%

- Sales Tax Amount: 0.08 * $50 = $4

- Tip Amount: 0.20 * $50 = $10

- Total Bill: $50 + $4 + $10 = $64

- Scenario 2: Tax then Tip on post-tax amount. Less common, but sometimes desired, a tip might be calculated on the total after tax.

- Meal Cost: $50

- Sales Tax: 8%

- Cost after Tax: $50 * (1 + 0.08) = $54

- Tip (20% of $54): 0.20 * $54 = $10.80

- Total Bill: $54 + $10.80 = $64.80

This demonstrates that simply adding 8% + 20% = 28% and applying it to the original cost would yield an incorrect result. Each percentage must be applied to its correct base at the appropriate step.

Practical Applications in Personal Finance and Business

The ability to accurately add with percentages has wide-ranging practical implications, driving smarter decisions in both personal finance and business operations.

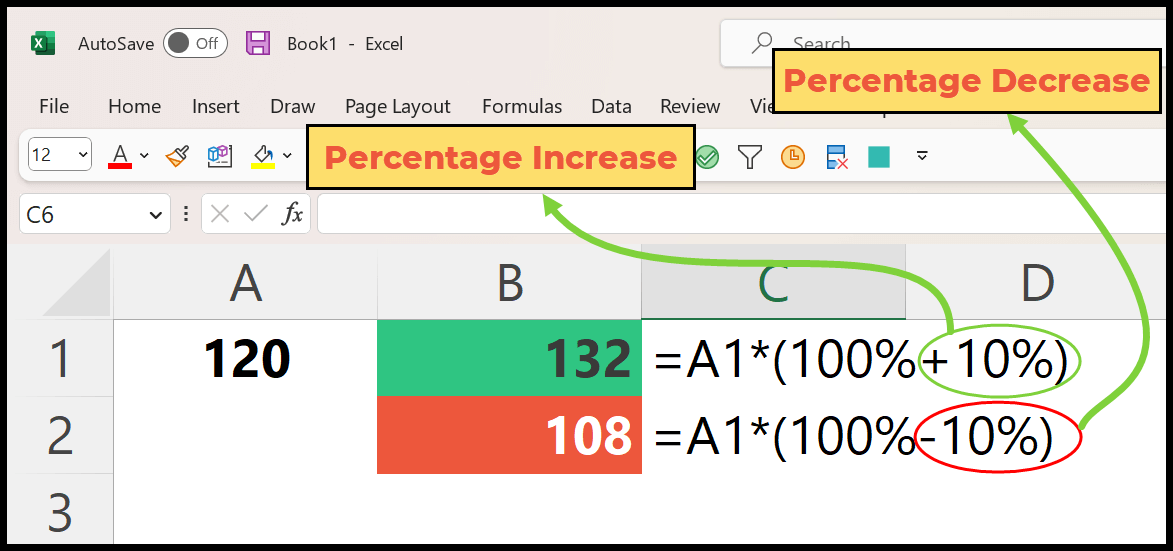

Calculating Cumulative Discounts or Markups

Imagine a retail scenario where an item is first discounted by 20%, and then an additional 10% off is offered during a flash sale. It’s a common misconception to simply add 20% + 10% = 30%. However, the second discount applies to the already discounted price.

- Original Price: $100

- First Discount (20%): $100 * (1 – 0.20) = $80

- Second Discount (10%): $80 * (1 – 0.10) = $72

- Total Discount: ($100 – $72) / $100 = 28%.

Understanding this helps consumers accurately gauge real savings and helps businesses correctly price promotions to maintain profit margins. The same logic applies to markups where a product’s price is increased sequentially.

Analyzing Multi-Stage Investment Performance

For investors, understanding how to add (or, more precisely, combine the effects of) percentages over multiple periods is fundamental to evaluating portfolio performance. A portfolio might experience varying returns each year. To calculate the compound annual growth rate (CAGR) or the total cumulative return, one must multiply the growth factors (1 + percentage change) for each period, rather than simply summing the annual percentages. This provides a true picture of the investment’s long-term trajectory and the power of compounding returns.

Budgeting and Tracking Financial Goals with Percentages

Effective personal budgeting often involves allocating income as percentages to different categories (e.g., 50% for needs, 30% for wants, 20% for savings). As income changes, these percentages scale, but the proportions remain. Similarly, tracking progress towards financial goals, like saving for a down payment or retirement, involves seeing what percentage of the goal has been achieved. If your goal increases due to unforeseen circumstances, understanding how the additional percentage affects your overall target and timeline is crucial for adjusting your savings strategy.

Common Pitfalls and How to Avoid Them

Despite their apparent simplicity, percentages are often a source of error in financial calculations. Awareness of common mistakes can significantly improve accuracy.

Misinterpreting the Base Value

The most frequent error is applying a percentage to the wrong base value. As seen with consecutive discounts or investment returns, the base value can change after each step. Always ask: “What is this percentage of?” This simple question can prevent significant miscalculations, especially in scenarios involving multiple layers of fees, taxes, or discounts.

Incorrectly Adding Consecutive Percentage Increases/Decreases

As detailed earlier, directly adding consecutive percentage changes (e.g., a 10% increase followed by a 10% increase is 21%, not 20%) leads to incorrect results. The correct method involves multiplying the factors (1 + percentage change in decimal form) for increases, and (1 – percentage change in decimal form) for decreases, or a combination thereof. This distinction is vital for understanding compounding interest, investment returns, and inflation.

Overlooking the Impact of Compounding

The power of compounding, both positive (investments) and negative (debt), is often underestimated. While it’s tempting to think of an annual interest rate as a simple addition over time, compound interest means that interest is earned (or charged) on previously accumulated interest. This accelerates growth or debt dramatically. Understanding this exponential effect, which is a sophisticated form of percentage “addition” over time, is paramount for long-term financial planning.

Tools and Strategies for Accurate Percentage Calculations

While a solid understanding of the underlying principles is key, modern tools and smart strategies can enhance accuracy and efficiency in percentage-based financial calculations.

Leveraging Spreadsheets and Financial Calculators

For complex scenarios involving multiple percentage changes, varying base values, or long-term compounding, spreadsheets (like Microsoft Excel or Google Sheets) are invaluable. They allow users to set up formulas that dynamically calculate outcomes, reducing manual error. Financial calculators, both physical and app-based, also offer dedicated functions for percentage calculations, present value, future value, and interest, making them indispensable for detailed financial analysis.

Mental Math Shortcuts for Quick Estimates

While precision is crucial, sometimes a quick estimate is all that’s needed. Learning mental math shortcuts for percentages can be incredibly useful. For example, to find 10% of a number, simply move the decimal one place to the left. To find 5%, halve the 10% value. For 20%, double the 10% value. These quick estimations can help in real-time decision-making, such as quickly calculating a tip or roughly estimating a discount.

The Importance of Double-Checking Your Work

Regardless of the method or tools used, always double-check your calculations. Even minor errors in percentage application can lead to significant discrepancies in financial outcomes. This is particularly true for large sums of money or long-term financial commitments. A quick review, perhaps by performing the calculation a second time using a different method or tool, can save substantial time and money in the long run.

In conclusion, “how to add with percentages” is a fundamental skill that underpins sound financial management. By understanding the nuances of base values, consecutive changes, and the power of compounding, individuals and businesses can navigate the financial landscape with greater confidence and accuracy. Mastering these calculations not only prevents common pitfalls but also unlocks opportunities for optimized budgeting, smarter investing, and more informed financial decision-making.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.