In the realm of personal finance, investing, and business operations, percentages are ubiquitous. From calculating interest on a savings account to understanding a stock’s multi-year returns or dissecting a series of discounts on a purchase, percentages are the language of financial change. Yet, a common misconception often leads individuals astray: the belief that percentages can be simply added together. The phrase “how to add percentage to percentage” isn’t about rudimentary arithmetic like 10% + 20% = 30%; it delves into the crucial understanding of how successive percentage changes, whether increases or decreases, combine to yield a cumulative effect. Mastering this concept is not merely an academic exercise; it’s a critical skill for informed decision-making, enabling you to accurately project financial growth, analyze investment opportunities, and navigate complex pricing structures with confidence.

Beyond Simple Sums: Unpacking the Logic of Percentage Interaction

The intuitive desire to add percentages linearly is often the first hurdle in truly understanding their financial impact. Financial literacy demands a deeper appreciation of how these numerical representations of parts of a whole interact, particularly when applied sequentially.

The Fundamental Misconception: Why 10% + 10% ≠ 20%

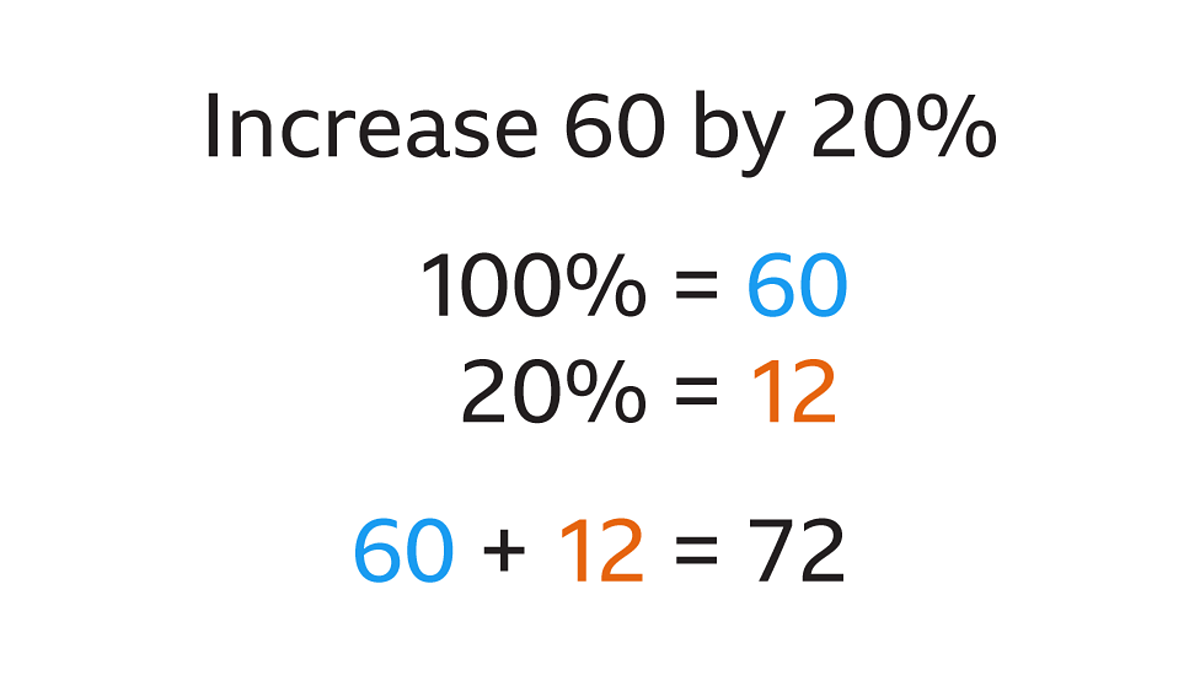

Imagine you have an item priced at $100. If its value increases by 10%, it becomes $110 ($100 + 10% of $100). Now, if that new value of $110 increases by another 10%, it becomes $121 ($110 + 10% of $110). The total increase from the original $100 to $121 is $21, representing a 21% increase, not 20%. This simple example vividly illustrates that when percentages are applied successively, the base amount changes, and thus the subsequent percentage is calculated on a new, adjusted figure. This concept is foundational to compound interest and cumulative returns, forming the bedrock of long-term financial planning.

The Multiplicative Nature of Percentage Changes

Instead of addition, the correct way to “add” percentages sequentially is through multiplication. Each percentage change should be converted into a decimal multiplier.

- An increase of X% becomes (1 + X/100). For example, a 10% increase is 1 + 0.10 = 1.10.

- A decrease of Y% becomes (1 – Y/100). For example, a 10% decrease is 1 – 0.10 = 0.90.

To find the cumulative effect of multiple changes, you multiply these multipliers together. Using our previous example:

- Initial value: $100

- First 10% increase: $100 * (1 + 0.10) = $100 * 1.10 = $110

- Second 10% increase: $110 * (1 + 0.10) = $110 * 1.10 = $121

Alternatively, applying the multipliers consecutively to the original base:

- $100 * (1.10 * 1.10) = $100 * 1.21 = $121.

This final multiplier, 1.21, signifies an overall 21% increase (1.21 – 1 = 0.21, or 21%). Understanding this multiplicative approach is the key to unlocking accurate financial calculations.

Establishing the Base: The Critical Starting Point

One of the most frequent errors in percentage calculations is failing to identify the correct base value. When a percentage change is mentioned, it’s crucial to ask: “Percentage of what?” Is it a percentage of the original amount, the current amount, or a different reference point entirely? In financial contexts, the base often changes after each percentage application. Always ensure you are calculating the percentage change based on the figure that exists before that specific change is applied. This meticulous attention to the base value prevents significant inaccuracies, especially in scenarios involving multiple steps.

Navigating Sequential Percentage Changes: Growth and Depreciation

The practical application of understanding “percentage to percentage” addition lies heavily in scenarios where values change over time, experiencing both growth and depreciation.

Compounding Growth: The Investor’s Best Friend

Compound interest is famously dubbed the “eighth wonder of the world” by Albert Einstein, and for good reason. It’s the most powerful illustration of sequential percentage increases. When you earn interest on your initial principal and on the accumulated interest from previous periods, your money grows exponentially.

- If you invest $1,000 at a 5% annual return:

- Year 1: $1,000 * 1.05 = $1,050

- Year 2: $1,050 * 1.05 = $1,102.50

- Year 3: $1,102.50 * 1.05 = $1,157.63

Over three years, the total growth is not 15% ($1,000 * 0.15 = $150), but $157.63, or 15.763%. This seemingly small difference accumulates significantly over longer periods, highlighting the importance of understanding the multiplicative effect.

Cumulative Reductions: Understanding Successive Discounts

Just as percentages can compound positively, they can also compound negatively, as seen with successive discounts. It’s common for retailers to offer an item at a certain discount, and then apply an additional discount to the already reduced price.

- An item is $100. It’s first discounted by 20%, then an additional 10% off the discounted price.

- First discount: $100 * (1 – 0.20) = $100 * 0.80 = $80

- Second discount: $80 * (1 – 0.10) = $80 * 0.90 = $72

The final price is $72. This is a 28% overall discount ($100 – $72 = $28). Had you simply added the percentages (20% + 10% = 30%), you might expect a price of $70, which is incorrect. The order of operations can sometimes matter, though in sequential discounts (or increases) as multipliers, the final product is commutative ($100 * 0.80 * 0.90 = $100 * 0.90 * 0.80 = $72).

Calculating Net Impact: A Step-by-Step Approach

For any series of percentage changes, follow these steps for accuracy:

- Convert each percentage change to its decimal multiplier: (1 + increase/100) or (1 – decrease/100).

- Multiply all the multipliers together: This gives you the net overall multiplier.

- Apply the net multiplier to the original base value: This gives you the final value.

- To find the overall percentage change: Subtract 1 from the net multiplier (if positive, it’s an increase; if negative, a decrease), then multiply by 100.

Real-World Financial Scenarios: Applying the Principles

The ability to correctly calculate sequential percentage changes is invaluable across numerous financial applications.

Investment Returns: From Annual Gains to Total Portfolio Growth

Understanding how to “add percentage to percentage” is paramount for investors.

- Calculating Average Annual Growth (CAGR): When comparing investments over multiple periods, simply averaging annual returns can be misleading. CAGR uses the multiplicative principle to provide a smoothed annual growth rate that accounts for compounding.

- Portfolio Rebalancing: As different assets in your portfolio grow at varying rates, their initial percentage allocations shift. Correctly calculating the new percentages and understanding the impact of these changes helps in rebalancing decisions.

- Dividend Reinvestment: Dividends that are reinvested purchase more shares, which then earn their own dividends, creating a powerful compounding effect often overlooked if one doesn’t grasp the multiplicative growth.

Retail Pricing: Discounts, Markups, and Sales Tax Stacking

Consumers and businesses alike constantly encounter multi-layered pricing structures.

- Multiple Discounts: As discussed, a “20% off plus an extra 10% off” deal requires multiplicative calculation to determine the true saving.

- Markups and Sales Tax: A product might have a base cost, a retail markup, and then a sales tax applied.

- Cost: $50

- Markup: 50% = $50 * 1.50 = $75

- Sales Tax: 8% = $75 * 1.08 = $81

The final price is $81, reflecting a cumulative increase from the base cost.

Budgeting and Inflation: Adjusting for Cost of Living

For personal finance, understanding how inflation compounds is crucial for long-term planning. A consistent 3% annual inflation rate means that the cost of living doesn’t just increase by 3% of the original amount each year; it increases by 3% of the inflated amount. This means your purchasing power erodes faster than a simple additive calculation might suggest, necessitating a greater return on savings and investments just to maintain real value.

Loan Interest and Debt Accumulation

The flip side of compounding growth is compounding debt. Unpaid credit card balances, for example, accrue interest on the principal and on previously accrued interest, leading to rapid debt accumulation. Understanding this mechanism is vital for managing debt effectively and appreciating the cost of borrowing. A “20% APR” isn’t just 20% of your initial loan; it compounds daily, monthly, or annually, dramatically increasing the total repayment amount over time.

Strategic Implications for Personal and Business Finance

Mastering the mechanics of percentage calculation has profound strategic benefits, moving beyond mere calculation to informed financial strategy.

Optimizing Savings and Retirement Planning

The power of compound interest directly influences retirement planning. Small, consistent contributions over long periods, earning even modest returns, can grow into substantial sums due to the multiplicative effect. Understanding this motivates early saving and smart investment choices, maximizing the impact of every dollar saved. Calculating future values with varying annual contribution increases or fluctuating market returns requires this advanced percentage comprehension.

Evaluating Investment Opportunities with Multi-Stage Growth

Many investment scenarios involve multiple stages of growth or decline. A company might project 15% growth in year one, 10% in year two, and 8% in year three. Accurately projecting the cumulative effect helps in evaluating the investment’s attractiveness. Similarly, understanding how different fees (expressed as percentages) can erode returns over time is critical for net profit analysis.

Smarter Spending: Decoding Discounts and Value

For consumers, discerning the true value of sales and promotions becomes effortless. You can quickly compare a “25% off” sale versus a “buy one, get one 50% off” deal by converting them into effective percentage savings, or accurately assess the actual price after multiple layered discounts. This knowledge prevents overestimation of savings and enables more prudent purchasing decisions.

Business Forecasting and Profit Margin Analysis

Businesses regularly deal with multiple percentage changes: cost increases, pricing adjustments, sales growth targets, and profit margin analysis.

- Pricing Strategy: Determining the optimal retail price involves calculating markups from cost, factoring in desired profit margins, and anticipating potential discounts.

- Sales Projections: Forecasting revenue often involves projecting growth rates (percentages) over multiple quarters or years, requiring accurate cumulative calculations.

- Cost Analysis: Understanding how a 5% increase in raw material costs combined with a 2% increase in shipping costs impacts the final production cost necessitates a firm grasp of percentage interaction.

Tools and Techniques for Accurate Percentage Calculations

While the underlying principles are crucial, practical application often benefits from the right tools and techniques to ensure accuracy and efficiency.

Leveraging Spreadsheets for Complex Scenarios

For any financial professional or serious investor, spreadsheet software like Microsoft Excel or Google Sheets is indispensable.

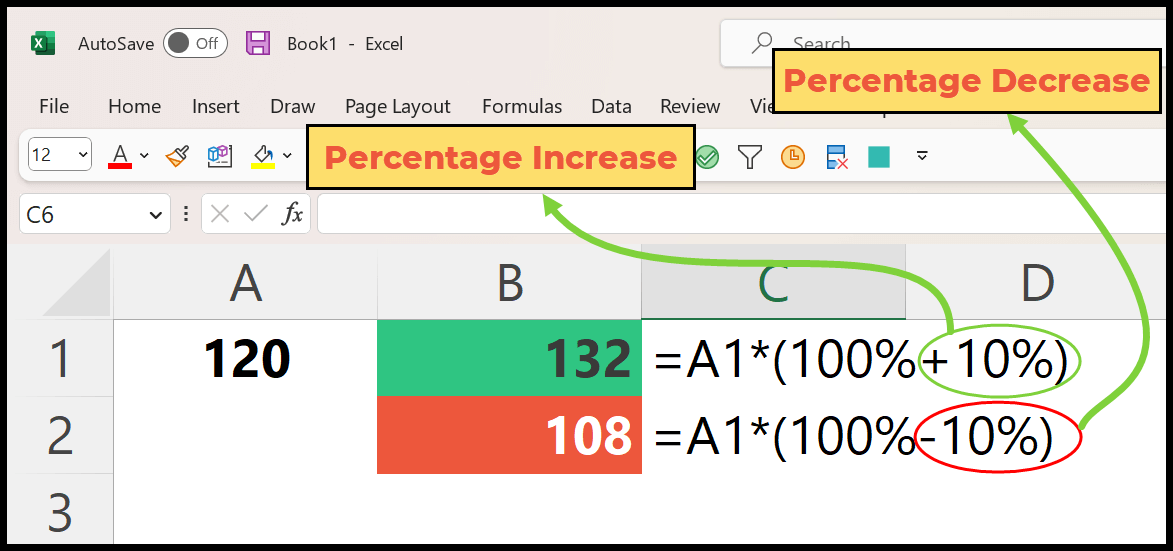

- Formulas: Using formulas like

=(1+A1)*(1+B1)*(1+C1)for cumulative increases, or=(1-A1)*(1-B1)*(1-C1)for cumulative decreases, streamlines calculations. - Scenario Analysis: Spreadsheets allow you to quickly model different scenarios (e.g., varying interest rates, different discount structures, or inflation rates) to see their financial impact.

- Financial Functions: Excel offers powerful functions like

FV(Future Value) orRATEwhich inherently account for compounding, simplifying complex percentage growth calculations.

Online Calculators and Financial Software

Numerous online calculators are available for specific financial scenarios, such as compound interest calculators, mortgage calculators, or discount calculators. Financial planning software often incorporates these calculations, providing visual representations and comprehensive reports. While these tools handle the arithmetic, understanding the underlying “percentage to percentage” logic helps in interpreting the results and ensuring correct data input.

Developing Your Mental Math Acumen

For simpler, quick assessments, developing some mental math proficiency can be beneficial. Understanding that a 10% increase followed by another 10% increase is roughly 21% (a bit more than double the original 10%) can help you estimate and quickly identify if a more precise calculation is needed. This intuition grows with practice and a solid grasp of the multiplicative principle.

Double-Checking Your Work: Mitigating Errors

Even with tools, errors can creep in. Always double-check your calculations, especially when dealing with large sums of money or critical financial decisions. One common method is to work the problem backward, if feasible, or to use a different method/tool to verify the result. A small percentage error can lead to significantly incorrect financial projections over time, making diligence paramount.

In conclusion, the question of “how to add percentage to percentage” is far more profound than it appears on the surface. It’s a gateway to understanding the dynamic, multiplicative nature of financial change. By moving beyond simple linear addition and embracing the power of decimal multipliers and sequential application, individuals and businesses can gain a crucial edge in financial planning, investment analysis, and everyday decision-making. Mastering this concept is not just about crunching numbers; it’s about cultivating a sophisticated financial intuition that empowers smarter, more accurate, and ultimately, more prosperous financial outcomes.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.