In the evolving landscape of personal finance, the transition from physical cash to digital liquidity has been spearheaded by innovative fintech solutions. Venmo, originally a simple tool for splitting dinner checks, has transformed into a robust financial ecosystem. For many users, the platform acts as a secondary bank account, a budgeting tool, and a primary gateway for peer-to-peer (P2P) transactions. However, to utilize Venmo to its full potential as a financial instrument, one must understand the nuances of managing its internal balance.

Understanding how to add money to Venmo—and more importantly, why and when to do so—is a fundamental skill in modern fiscal management. This guide explores the strategic methods for funding your account, the financial implications of different transfer types, and how to integrate Venmo into your broader personal finance strategy.

The Mechanics of the Venmo Balance: Why Liquidity Matters

Before diving into the “how,” it is essential to understand the “what.” Unlike traditional credit cards, a Venmo balance functions as a digital ledger of stored value. While you can use Venmo by simply linking a debit card or bank account, maintaining a standing balance offers unique advantages in terms of budgeting and transaction speed.

The Distinction Between Linked Methods and Internal Balances

When you make a payment on Venmo, the app typically draws from your linked funding source (a bank account or debit card) in real-time. However, if you have a Venmo balance, the app defaults to using those funds first. For those practicing strict “envelope budgeting,” keeping a specific amount in your Venmo balance allows you to cap your social spending. Once the digital “envelope” is empty, you are forced to consciously decide whether to dip into your primary savings.

The Role of the Venmo Debit Card

To add money directly to your Venmo balance from a bank account, users generally need to be approved for a Venmo Debit Card or have undergone specific identity verification processes required by federal financial regulations. This card bridges the gap between digital P2P transfers and real-world utility, allowing you to spend your balance at any merchant that accepts Mastercard. Having a funded balance ensures that these point-of-sale transactions are seamless and do not rely on the batch-processing speeds of traditional banking.

Strategic Methods for Funding Your Venmo Account

Adding capital to your digital wallet is a straightforward process, but the method you choose can impact your financial timing and record-keeping. Here are the primary ways to ensure your Venmo account is liquid.

Standard Bank Transfers via ACH

The most common way to add money to your Venmo balance is through a standard transfer from a verified checking account. This uses the Automated Clearing House (ACH) network.

- Verification: First, ensure your bank account is not just linked but verified. This usually involves “Instant Verification” through a service like Plaid or “Manual Verification” using micro-deposits.

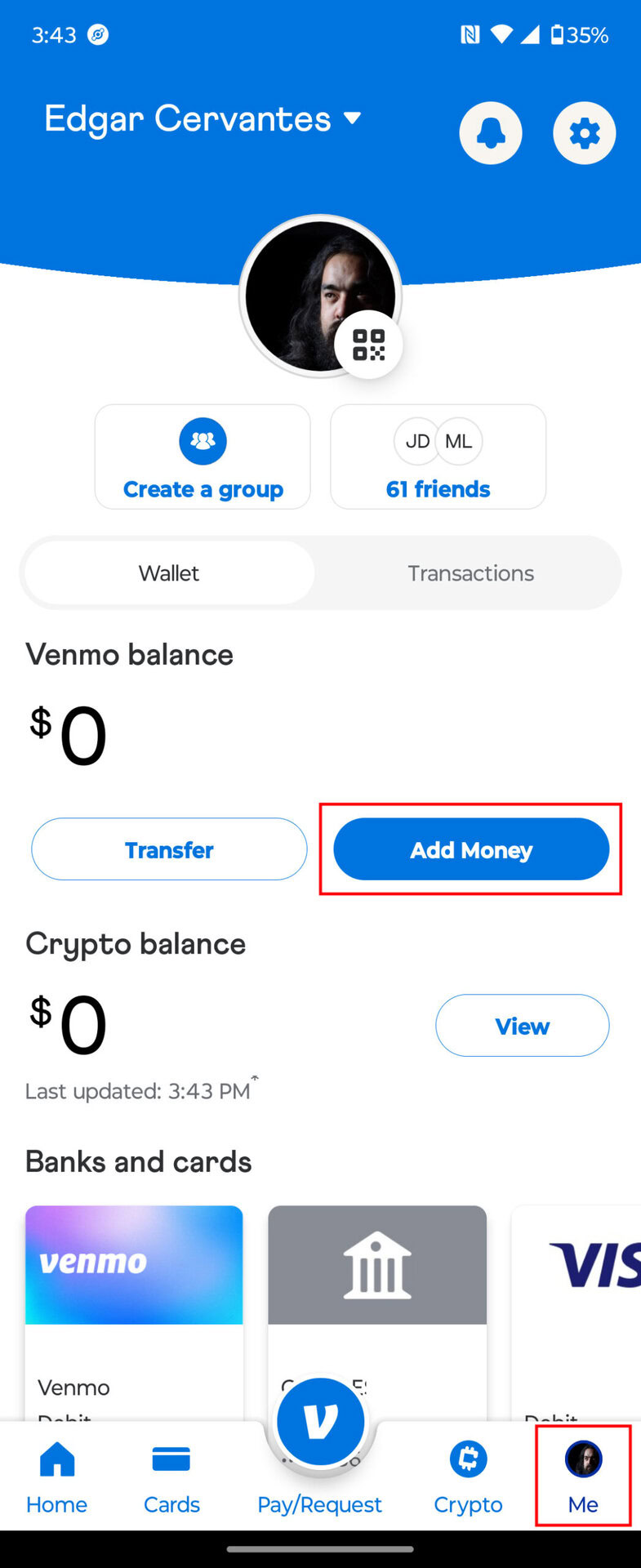

- The Process: Within the app, navigate to the “Me” tab, tap “Manage Balance,” and select “Add Money.”

- Timeline: It is important for financial planning to note that ACH transfers are not instantaneous. They typically take 3 to 5 business days to clear. From a personal finance perspective, this means you must anticipate your funding needs in advance to avoid liquidity gaps.

Utilizing the Venmo Debit Card for Instant Access

If you are a holder of the Venmo Mastercard, you gain access to more streamlined funding features. For many users, the “Direct Deposit” feature is a game-changer. By routing a portion of your payroll check directly to Venmo, you bypass the need to manually move money between accounts. This automation is a cornerstone of “lazy” wealth management, ensuring your social and discretionary spending funds are allocated the moment you get paid.

Receiving Payments as a Primary Funding Source

In the ecosystem of online income and side hustles, many freelancers and gig workers use Venmo as a collection point. Instead of “adding” money from a bank, your balance grows through incoming P2P transfers. From a money management standpoint, this creates a “closed-loop” system where side hustle income is used exclusively for discretionary spending or peer-reimbursements, keeping your primary salary untouched for bills and investments.

Navigating Fees, Limits, and Financial Compliance

As with any financial tool, understanding the cost of doing business is vital to maintaining your bottom line. Venmo is a business, and while many of its features are free, certain behaviors incur costs that can eat into your capital.

Understanding Transaction Limits and Identity Verification

To prevent money laundering and fraud, Venmo imposes strict limits on how much money you can add or move. Unverified accounts have much lower ceilings—often a rolling weekly limit of $299.99 for all transactions combined. By completing the identity verification process (providing your SSN and DOB), you can increase your rolling weekly limit significantly, often up to $60,000. For high-net-worth individuals or those managing business expenses, this verification is not optional; it is a prerequisite for financial flexibility.

Avoiding Unnecessary Service Fees

While adding money from a bank account is free, other interactions with your balance are not.

- Instant Transfers: If you need to move money out of Venmo to your bank account immediately, Venmo charges a 1.75% fee (with a minimum of $0.25 and a maximum of $25). To maximize your money, always opt for the “1-3 Business Days” transfer, which remains free.

- Credit Card Funding: While you can pay others using a credit card, you cannot “add money” to your Venmo balance using a credit card. Furthermore, sending money via credit card incurs a 3% fee, which negates the value of almost any rewards program. From a savvy financial perspective, funding Venmo through a credit card is rarely a sound move.

Security Protocols for Large Transfers

When moving significant sums into the Venmo ecosystem, security becomes a paramount concern. Venmo uses encryption and multi-factor authentication (MFA) to protect your assets. However, because Venmo is a digital wallet and not a traditional bank account (though funds may be FDIC-insured if they are moved into specific partner bank products), users should practice “financial hygiene.” This includes never leaving excessively large sums in the balance for long periods and regularly reviewing transaction histories for unauthorized activity.

Integrating Venmo into Your Broader Financial Strategy

Adding money to Venmo should not be an isolated act; it should be part of a cohesive plan for managing your cash flow. Digital wallets represent a shift in how we perceive “spendable” income versus “saved” income.

Using Venmo for Budgeting and Expense Tracking

One of the most effective ways to use the “Add Money” feature is to treat Venmo as a monthly discretionary budget. For example, if your monthly “fun money” budget is $400, you can transfer that amount to Venmo at the start of the month. By using the Venmo Debit Card for coffee, movies, and dining out, you can track exactly how much of your discretionary budget remains in real-time. This prevents the “leakage” that often occurs when small transactions are scattered across multiple credit and debit cards.

The Role of Digital Wallets in Modern Liquidity

In the world of personal finance, liquidity is king. Having money in Venmo provides a level of “social liquidity” that a high-yield savings account cannot. It allows for the instantaneous settlement of debts, which can be crucial for maintaining healthy personal and professional relationships. However, the professional money manager knows that a Venmo balance does not earn interest. Therefore, while keeping a funded balance is convenient for transactions, any surplus capital beyond your monthly spending needs should be moved back into an interest-bearing account or an investment vehicle.

Conclusion: The Future of Frictionless Finance

Learning how to add money to Venmo is the first step in mastering one of the most powerful tools in the fintech era. By understanding the timing of ACH transfers, the benefits of the Venmo Debit Card, and the strategic importance of limits and fees, you can transform a simple app into a sophisticated component of your financial life.

Whether you are using it to silo your side-hustle income or to strictly adhere to a social spending budget, the ability to fund and manage your digital balance effectively is a hallmark of financial literacy in the 21st century. As digital and physical currencies continue to merge, those who can navigate these platforms with professional precision will find themselves better positioned to manage their wealth, minimize their fees, and maximize their financial freedom.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.