In today’s dynamic marketplace, the ability to accept credit card payments is no longer a luxury but a fundamental necessity for businesses aiming for growth and sustained financial health. From bustling retail stores to burgeoning e-commerce platforms and service-based operations, credit cards facilitate immediate transactions, broaden customer reach, and significantly impact revenue streams and operational efficiency. This guide delves into the essential financial considerations, tools, and strategies for businesses to effectively integrate credit card acceptance into their financial framework, ensuring compliance, optimizing costs, and fostering a robust financial ecosystem.

The Imperative of Credit Card Acceptance in Modern Business Finance

Embracing credit card payments is a strategic financial decision that resonates across various aspects of a business, from customer acquisition to cash flow management. It reflects a commitment to convenience, professionalism, and staying competitive in an increasingly digital and cashless economy.

Expanding Your Customer Base and Revenue Streams

The most direct financial benefit of accepting credit cards is the immediate expansion of your potential customer base. A significant portion of consumers relies on credit and debit cards for their daily transactions, often preferring them over cash for convenience, security, and rewards. By not accepting cards, businesses inadvertently alienate a large segment of the market, losing out on impulse buys and larger transactions. Offering credit card payment options removes a critical barrier to purchase, encouraging higher average transaction values and fostering repeat business. For online ventures, credit card gateways are non-negotiable, directly correlating to conversion rates and global reach. Financially, this translates to increased sales volume and, consequently, enhanced revenue streams, providing a stronger foundation for business growth and investment.

Enhancing Professionalism and Customer Convenience

From a financial perspective, offering diverse payment options, including credit cards, projects an image of professionalism and reliability. It signals to customers that your business is established, trustworthy, and equipped to handle modern financial transactions efficiently. This perception can lead to greater customer confidence and loyalty, which are invaluable assets for long-term financial stability. The convenience factor cannot be overstated; customers expect seamless payment experiences whether they are shopping in-store, online, or over the phone. Providing this convenience directly impacts customer satisfaction, reducing cart abandonment in e-commerce and streamlining checkout processes in physical locations. Financially, satisfied customers are more likely to become repeat buyers, reducing the cost of customer acquisition over time and contributing to a more predictable revenue stream.

The Competitive Edge in a Cashless Economy

The global trend towards a cashless society is undeniable, accelerated by technological advancements and shifting consumer preferences. Businesses that lag in adopting modern payment methods risk being outmaneuvered by competitors who readily offer credit card acceptance. In a competitive landscape, the ability to accept credit cards can be a significant differentiator, especially for smaller businesses vying against larger enterprises. It allows businesses to tap into market segments that predominantly use cards, such as tourists, corporate clients, or younger demographics. Proactively integrating credit card acceptance ensures your business remains relevant, accessible, and attractive to a broad spectrum of consumers, protecting and enhancing its market share and long-term financial viability. It’s an investment in future revenue and market positioning, safeguarding against obsolescence in an evolving financial ecosystem.

Understanding the Financial Mechanics of Credit Card Transactions

To effectively manage the financial aspects of credit card acceptance, it’s crucial for businesses to grasp the underlying ecosystem and the flow of funds involved in each transaction. This understanding empowers businesses to make informed decisions about payment processors, pricing models, and financial reconciliation.

Demystifying the Payment Processing Ecosystem

A credit card transaction, despite its instantaneous appearance, involves a complex network of financial entities working in concert. When a customer swipes, taps, or enters card details, a series of rapid communications occur between different parties. This intricate ecosystem ensures the validity of the card, the availability of funds, and the secure transfer of money from the customer’s account to the merchant’s. Understanding this process is key to appreciating the costs involved and the robust infrastructure that supports modern commerce. It also highlights the importance of choosing reliable partners for each step of the transaction chain.

Key Players: Merchants, Issuers, Acquirers, and Networks

At the heart of every credit card transaction are several indispensable players, each with a distinct financial role:

- Merchant: Your business, which accepts the credit card payment for goods or services.

- Cardholder (Customer): The individual making the purchase using their credit card.

- Issuing Bank: The financial institution that issued the credit card to the customer (e.g., Chase, Wells Fargo, Bank of America). They extend the credit and handle billing for the cardholder.

- Acquiring Bank (Merchant Bank): The bank that holds your merchant account and processes credit card transactions on behalf of your business. They receive funds from the issuing bank and deposit them into your account.

- Card Networks (Associations): These are the global networks (e.g., Visa, Mastercard, American Express, Discover) that facilitate communication between issuing and acquiring banks. They set the rules, establish interchange rates, and ensure the secure transmission of data.

- Payment Processor: A company that acts as an intermediary between your business and the acquiring bank, handling the technical details of transaction processing, authorization, and settlement. They often bundle services from various acquiring banks.

Each of these entities plays a vital financial role, contributing to the overall cost and complexity of accepting credit cards.

The Flow of Funds: From Swipe to Settlement

The journey of funds in a credit card transaction can be broken down into several stages:

- Authorization: When a customer initiates a payment, your point-of-sale (POS) system or payment gateway sends the transaction details to your payment processor. The processor then forwards the request through the card network to the issuing bank to verify the card’s validity and sufficient funds or credit.

- Authentication: The issuing bank approves or declines the transaction, sending a response back through the card network and processor to your system.

- Batching: At the end of the day (or a set period), your business ‘batches’ or submits all authorized transactions to your payment processor. This initiates the actual financial transfer.

- Clearing: The payment processor sends the batched transactions to the acquiring bank, which then requests the funds from the respective issuing banks via the card networks.

- Settlement: The issuing banks transfer the funds (minus their interchange fees and network assessment fees) to the acquiring bank. The acquiring bank then deposits the net amount (minus processing fees) into your business’s merchant account. This entire process typically takes 1-3 business days.

Understanding this flow is critical for cash flow management and reconciling your accounts, as the deposited amount will always be less than the gross sales due to various fees.

Essential Financial Tools and Methods for Accepting Payments

Choosing the right financial tools and methods for accepting credit cards is paramount to optimizing costs, enhancing operational efficiency, and securing transactions. The selection depends heavily on your business model, transaction volume, and customer interaction points.

In-Person Solutions: POS Systems and Mobile Readers

For brick-and-mortar stores, restaurants, and businesses with physical locations, in-person payment solutions are indispensable.

- Point-of-Sale (POS) Systems: Modern POS systems are comprehensive financial hubs, integrating hardware (terminals, cash drawers, barcode scanners) and software to manage sales, inventory, customer data, and payment processing. They facilitate various payment methods including credit cards (swipe, chip, contactless/NFC), debit cards, and sometimes even digital wallets. Investing in a robust POS system is a significant financial decision but offers unparalleled control over sales data, inventory management, and financial reporting, providing valuable insights into business performance.

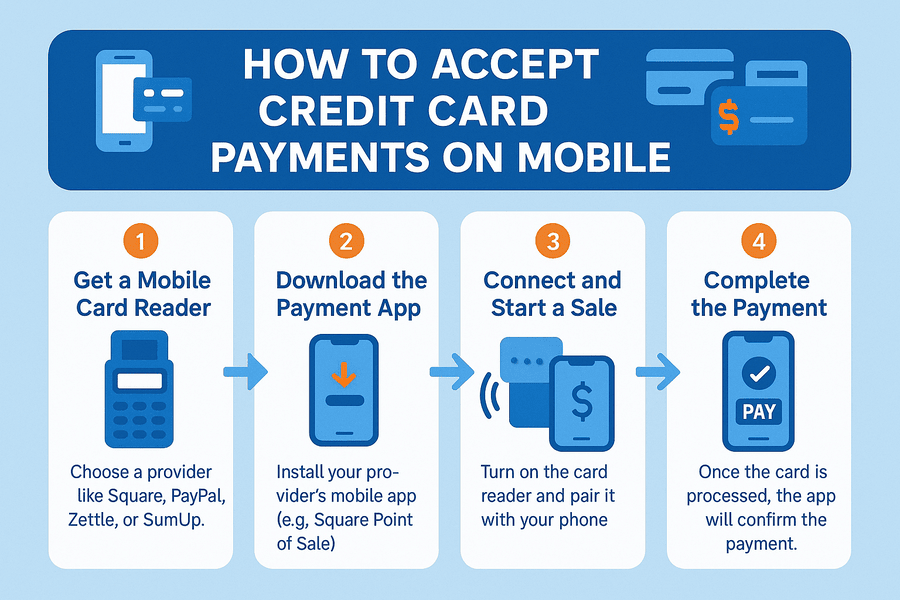

- Mobile Card Readers (mPOS): Ideal for mobile businesses, pop-up shops, food trucks, and service professionals, mPOS devices connect to smartphones or tablets, transforming them into portable payment terminals. Brands like Square, PayPal Zettle, and Clover Go offer affordable readers that process chip, swipe, and contactless payments. These solutions are financially attractive due to their low upfront costs and flexibility, allowing businesses to accept payments wherever they operate, capturing sales opportunities on the go. While transaction fees might be slightly higher than traditional POS systems, the convenience and accessibility often outweigh the incremental cost for specific business models.

Online Payment Gateways and E-commerce Integration

For businesses operating online, payment gateways are the digital equivalent of POS systems.

- Payment Gateways: These services securely authorize credit card payments for online businesses. They encrypt sensitive card information and transmit it between the customer, merchant, and payment processor. Leading gateways include Stripe, PayPal, Authorize.net, and Shopify Payments. Choosing a gateway involves evaluating transaction fees, setup costs, security features, and integration capabilities with your e-commerce platform. A well-integrated gateway minimizes friction in the checkout process, directly impacting online sales conversions and the overall financial health of your e-commerce venture.

- E-commerce Platform Integration: Most e-commerce platforms (e.g., Shopify, WooCommerce, BigCommerce) have built-in payment gateway integrations or offer easy connections to third-party providers. This streamlines the technical setup, allowing businesses to focus on sales and marketing. When selecting an e-commerce platform, consider its payment processing capabilities and the associated financial implications, including platform-specific transaction fees if you don’t use their preferred gateway.

Virtual Terminals and Invoicing for Remote Transactions

For service-based businesses, B2B companies, or those taking payments over the phone, virtual terminals and invoicing solutions offer flexibility.

- Virtual Terminals: These are web-based applications that allow businesses to process credit card payments using a computer and an internet connection, without physical hardware. You simply log in, enter the customer’s card details, and process the transaction. This is ideal for phone orders, mail orders, or payments taken remotely. Many payment processors offer virtual terminal access as part of their service package, making it a cost-effective solution for businesses with lower in-person transaction volumes.

- Online Invoicing with Payment Links: Modern accounting and invoicing software (e.g., QuickBooks, FreshBooks, Wave) allow businesses to create and send professional invoices that include direct payment links. Customers can click these links to pay securely online using their credit card. This streamlines the accounts receivable process, improves cash flow by reducing payment delays, and offers a convenient payment method for clients, thereby improving financial efficiency.

The Role of Merchant Accounts and Payment Processors

At the core of accepting credit cards lies the relationship with a merchant account provider and a payment processor.

- Merchant Account: This is a special bank account that temporarily holds funds from credit card sales before they are deposited into your regular business bank account. It’s a prerequisite for accepting credit card payments. Some providers offer “aggregated” or “third-party” merchant accounts (like Square or PayPal) where you share an account with other businesses, simplifying the setup but sometimes at a higher per-transaction fee. Traditional “dedicated” merchant accounts are typically offered by acquiring banks or specialized providers and can offer better rates for high-volume businesses.

- Payment Processors: These companies handle the technical aspects of processing transactions, from authorization to settlement. They are the gateway between your business, the card networks, and the banks. Many companies bundle merchant accounts and payment processing services into one package. Choosing the right processor is a critical financial decision, as their fee structure directly impacts your profit margins.

Navigating the Costs: Fees, Rates, and Financial Implications

Understanding the financial costs associated with credit card acceptance is crucial for budgeting, pricing strategies, and maintaining healthy profit margins. These costs can be complex, involving multiple types of fees and various pricing models.

Decoding Credit Card Processing Fees (Interchange, Assessments, Markups)

The fees for accepting credit cards are typically broken down into three main components:

- Interchange Fees: These are the largest component of processing costs, set by the card networks (Visa, Mastercard, etc.) and paid directly to the customer’s issuing bank. Interchange fees vary significantly based on the card type (rewards, corporate, debit), transaction type (card-present, card-not-present), and industry. They are non-negotiable for businesses and form the baseline cost.

- Assessment Fees (Network Fees): These are paid directly to the card networks (Visa, Mastercard, etc.) for using their network infrastructure. These are generally a small percentage of the transaction volume plus a small per-transaction fee. Like interchange fees, they are non-negotiable.

- Processor Markup: This is the fee charged by your payment processor (or acquiring bank) for their services. This is where competition among processors comes into play, and it’s the most negotiable part of your processing costs. It covers their operational costs, customer support, and profit.

Understanding Different Pricing Models (Tiered, Flat-Rate, Interchange-Plus)

Payment processors offer various pricing models, each with its own financial implications:

- Tiered Pricing: Processors categorize transactions into “qualified,” “mid-qualified,” and “non-qualified” tiers, each with a different rate. While seemingly simple, this model can be opaque, as the processor decides which transactions fit into which tier, often leading to higher “mid-qualified” or “non-qualified” rates for common transactions. This can make cost forecasting difficult.

- Flat-Rate Pricing: A single, fixed percentage plus a small per-transaction fee, regardless of card type or transaction method (e.g., 2.9% + $0.30). This model, popularized by Square and PayPal, is simple and predictable, making it ideal for small businesses with lower transaction volumes or those just starting. While transparent, it can be more expensive for high-volume businesses or those processing many debit cards, as it doesn’t differentiate between lower-cost transactions.

- Interchange-Plus Pricing: Considered the most transparent model, it charges interchange fees and assessment fees at cost, plus a fixed markup from the processor (e.g., Interchange + 0.20% + $0.10). This model is generally favored by medium to large businesses with higher transaction volumes, as it offers clear cost breakdown and often the lowest overall processing fees once volume increases.

Hidden Costs and Long-Term Financial Planning

Beyond per-transaction fees, businesses must be aware of other potential costs:

- Monthly Fees: Account fees, statement fees, PCI compliance fees, gateway fees.

- Setup Fees: For new merchant accounts or equipment.

- Chargeback Fees: Penalties incurred when a customer disputes a transaction. These can be substantial and directly impact profitability.

- Early Termination Fees: If you switch processors before your contract ends.

- Hardware Costs: For POS terminals or mobile readers.

Diligent financial planning requires understanding all these potential costs, negotiating with processors, and regularly reviewing your statements to ensure you’re getting the best rates and aren’t being overcharged. These fees, collectively, represent a significant operational cost that must be factored into pricing strategies and overall financial projections.

Choosing the Right Payment Solution for Your Business’s Financial Health

Selecting the optimal credit card acceptance solution is a strategic decision that profoundly impacts your business’s financial efficiency, security, and growth potential. It requires a careful assessment of various factors tailored to your specific operational needs.

Assessing Your Business Needs and Transaction Volume

The first step in choosing a payment solution is a thorough financial self-assessment. Consider:

- Business Type: Are you a retail store, an e-commerce site, a service provider, or a hybrid? This dictates the primary payment methods you’ll need (in-person, online, remote).

- Average Transaction Size: Do you process many small transactions or fewer large ones? This influences the impact of per-transaction fees versus percentage-based fees.

- Monthly Transaction Volume: High-volume businesses often benefit from interchange-plus pricing, while low-volume businesses might find flat-rate pricing more manageable despite potentially higher overall rates.

- Peak Seasons/Fluctuations: Your solution should be able to handle spikes in transaction volume without additional penalties or service disruptions.

- Integration Needs: Does it need to integrate with existing accounting software, inventory management systems, or CRM to streamline financial reconciliation and data analysis?

A clear understanding of these financial metrics will guide you toward solutions that are both cost-effective and operationally sound.

Evaluating Security, Compliance, and Risk Management

Financial security is paramount when handling sensitive customer data. Your chosen solution must prioritize compliance and robust security measures.

- PCI DSS Compliance: The Payment Card Industry Data Security Standard (PCI DSS) is a set of security standards designed to ensure that all companies that process, store, or transmit credit card information maintain a secure environment. Your processor should be PCI compliant, and your business must also adhere to relevant standards to avoid hefty fines, data breaches, and reputational damage.

- Fraud Prevention Tools: Look for features like Address Verification Service (AVS), Card Verification Value (CVV) checks, 3D Secure, and tokenization. These tools reduce the risk of chargebacks and protect your business from financial losses due to fraudulent transactions.

- Data Encryption: Ensure that all payment data is encrypted both in transit and at rest, minimizing the risk of unauthorized access.

- Chargeback Management: Understand the processor’s policies and support for disputing chargebacks. Frequent or unmanaged chargebacks can significantly impact your financial health.

Investing in a secure and compliant solution is not just about avoiding penalties; it’s about protecting your business’s financial assets and maintaining customer trust.

Comparing Providers: Features, Support, and Scalability

With numerous payment processors and solutions available, a detailed comparison is essential.

- Pricing Structure: Request a full disclosure of all fees (transaction, monthly, annual, PCI, chargeback) and compare them across different pricing models. Don’t hesitate to negotiate, especially for interchange-plus rates.

- Features: Beyond basic processing, consider additional financial tools like invoicing, recurring billing, customer management, analytics, and reporting. Do they offer a virtual terminal, integrated POS, or mobile payments if needed?

- Customer Support: Accessible and responsive support is crucial, especially when technical or financial issues arise. Look for 24/7 support, dedicated account managers, and online resources.

- Scalability: Choose a solution that can grow with your business without requiring a complete overhaul of your payment infrastructure. Can it handle increasing transaction volumes, new sales channels, or international payments?

- Contract Terms: Be wary of long-term contracts with early termination fees. Month-to-month or flexible agreements offer greater financial agility.

Thorough due diligence in comparing providers can lead to significant long-term financial savings and operational efficiencies.

Impact on Cash Flow and Financial Reporting

The chosen payment solution directly influences your business’s cash flow and simplifies financial reporting.

- Settlement Speed: Faster settlement times mean quicker access to your funds, improving cash flow. Inquire about the typical deposit time for various processors.

- Reporting Tools: Robust reporting features are invaluable for financial analysis, tax preparation, and reconciliation. Look for platforms that provide detailed sales reports, transaction histories, fee breakdowns, and insights into customer purchasing patterns. These tools empower better financial decision-making.

- Integration with Accounting Software: Seamless integration with your accounting system (e.g., QuickBooks, Xero) reduces manual data entry, minimizes errors, and streamlines the reconciliation process, saving time and money.

By carefully considering these financial impacts, businesses can select a credit card acceptance solution that not only facilitates transactions but also strengthens their overall financial management and strategic planning.

Accepting credit cards is a strategic financial move for any modern business. By understanding the underlying mechanics, selecting the right tools, meticulously navigating the cost structures, and prioritizing security, businesses can leverage credit card payments to drive revenue, enhance customer satisfaction, and secure a competitive edge in today’s evolving economic landscape. This informed approach to payment processing is a cornerstone of sustainable financial success.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.