In the modern financial landscape, the ability to accept credit card payments is no longer a luxury—it is a fundamental requirement for business viability. As the global economy shifts further away from cash, the “Money” aspect of your business depends heavily on how efficiently, securely, and cost-effectively you can process digital transactions. Whether you are a solo entrepreneur or a scaling enterprise, navigating the complex web of merchant accounts, processing fees, and financial risk management is critical to protecting your margins.

This guide explores the financial mechanisms behind credit card processing, helping you choose the right tools to optimize your cash flow and minimize unnecessary expenditures.

Understanding the Financial Infrastructure: Merchant Accounts vs. Payment Service Providers

To accept credit card payments, a business must have a mechanism to move money from a customer’s bank to its own. This is facilitated by two primary financial models: dedicated merchant accounts and Payment Service Providers (PSPs).

Merchant Accounts: The Traditional Financial Foundation

A dedicated merchant account is a specialized bank account established specifically for your business. When you use a merchant account, you enter into a direct agreement with an acquiring bank. This model is often preferred by established businesses with high transaction volumes.

From a financial perspective, a dedicated merchant account offers greater stability. Because your business undergoes a rigorous underwriting process upfront, the risk of “frozen funds” is significantly lower. Furthermore, for businesses processing over $20,000 per month, the custom pricing structures available through dedicated accounts often result in lower per-transaction costs compared to flat-rate alternatives.

Payment Service Providers (PSPs): The Modern Solution for Small Businesses

PSPs, such as Square, PayPal, or Stripe, have revolutionized business finance by aggregating thousands of merchants under a single umbrella account. The primary financial advantage here is the speed of entry and the lack of monthly maintenance fees.

For startups or low-volume side hustles, PSPs eliminate the barrier to entry. There are usually no long-term contracts or setup fees, making it a “pay-as-you-go” financial tool. However, the trade-off is a higher flat-rate fee and a slightly higher risk of account holds, as the PSP performs its risk assessment in real-time rather than during a pre-approval phase.

Comparing Costs and Financial Risks

Choosing between these two systems requires a cost-benefit analysis of your monthly revenue. If your business is seasonal, a PSP prevents “money leakage” through monthly fees during off-peak months. Conversely, if you have consistent, high-volume sales, the 2.9% + $0.30 standard PSP fee will eventually dwarf the $20–$50 monthly fee and lower interchange rates of a dedicated merchant account.

Decoding the Cost Structure of Credit Card Processing

Accepting credit cards is not free, and the fees can quickly erode your profit margins if you do not understand the underlying cost structures. Every time a card is swiped or entered online, several entities take a cut.

Interchange-Plus Pricing: Transparency in Fees

Interchange-plus is widely considered the most transparent and cost-effective pricing model for businesses. “Interchange” is the non-negotiable fee set by card networks (Visa, Mastercard), while the “Plus” is the markup charged by your processor.

By using this model, your business pays the exact cost of the transaction plus a fixed margin. This allows you to benefit from lower rates on debit cards or non-premium credit cards. From a financial management standpoint, interchange-plus makes it easier to track exactly where your money is going, preventing “hidden” markups.

Flat-Rate Pricing: Budgeting for Predictability

Flat-rate pricing is the hallmark of PSPs. You pay a consistent percentage (e.g., 2.6% + $0.10) regardless of the card type. While this is often more expensive on a per-transaction basis, it offers extreme predictability for your accounting department. If you know exactly what percentage of every sale will be deducted, you can factor that cost directly into your product pricing with surgical precision.

Hidden Costs: Chargebacks, Assessments, and Monthly Minimums

Beyond the standard transaction fees, several “hidden” financial drains can impact your bottom line:

- Chargeback Fees: When a customer disputes a charge, the processor often charges a fee (ranging from $15 to $50) regardless of who wins the dispute.

- Assessment Fees: These are small fees paid directly to the card brands for the privilege of using their network.

- Monthly Minimums: Some traditional merchant accounts require you to generate a certain amount in fees each month; if you fall short, you are charged the difference.

Selecting the Right Financial Tools for Your Business Model

The “how” of accepting payments depends largely on your operational environment. The tools you choose should align with your business model to ensure the lowest possible overhead.

In-Person Terminals and Point-of-Sale (POS) Systems

For brick-and-mortar retail or hospitality, the physical hardware is your primary interface. Modern POS systems are no longer just cash registers; they are comprehensive financial tools. They track inventory, manage payroll, and provide real-time sales data. From a money management perspective, an integrated POS system reduces human error in accounting and ensures that your physical sales match your bank deposits.

E-commerce Gateways for Online Revenue Streams

If you sell online, you need a payment gateway. This is the digital equivalent of a card swiper, encrypting the data and sending it to the processor. Integrating your gateway directly with your accounting software (like QuickBooks or Xero) is a vital step in financial automation. This ensures that every online sale is automatically reconciled in your books, saving hours of manual data entry.

Mobile Payments and Virtual Terminals for Service Providers

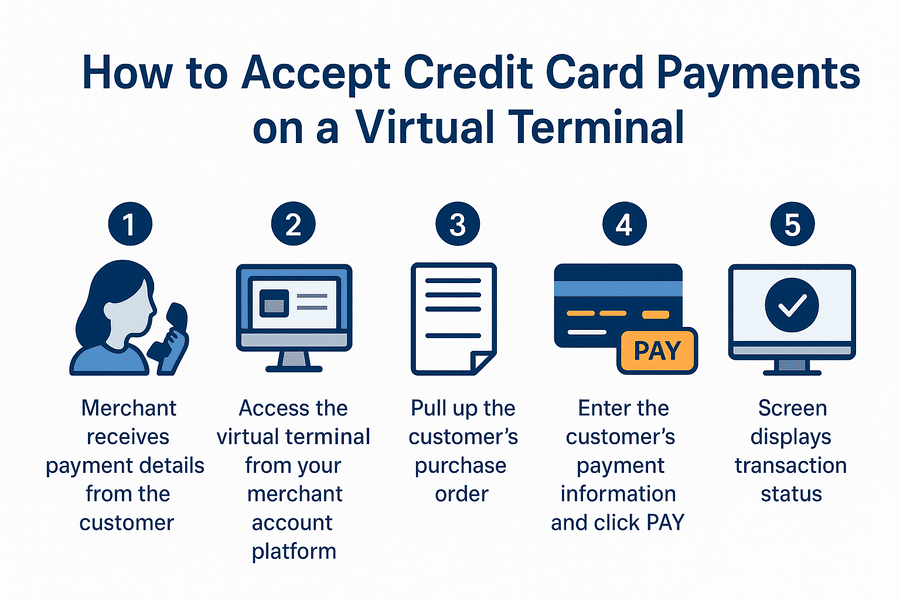

For contractors, consultants, or mobile service providers, hardware-heavy systems are unnecessary. Mobile card readers that plug into a smartphone allow for on-the-spot payment, improving your “Days Sales Outstanding” (DSO). Additionally, virtual terminals allow you to take payments over the phone by typing card details into a secure web browser—a crucial tool for B2B companies or service-based businesses.

Optimizing Cash Flow and Financial Security

Accepting payments is only half the battle; the other half is ensuring that money reaches your bank account quickly and stays there securely.

Speed of Settlements: Getting Your Funds Faster

In business finance, liquidity is king. The time it takes for a credit card transaction to move from “pending” to “available” in your bank account is the settlement period. Most processors offer a 1–2 business day settlement. However, some now offer “Instant Deposit” for an additional fee (usually 1%). While this 1% fee might seem small, it is a high price for liquidity. A strategic financial manager will balance the need for immediate cash with the cost of these expedited transfers.

Mitigating Financial Loss through PCI Compliance and Fraud Prevention

Security is a financial concern, not just a technical one. Data breaches lead to massive fines and the loss of merchant privileges. Adhering to PCI DSS (Payment Card Industry Data Security Standard) is mandatory. Furthermore, implementing advanced fraud detection tools—such as Address Verification Service (AVS) and Card Verification Value (CVV) checks—is essential to prevent chargebacks. Every fraudulent transaction is a direct hit to your net income.

Leveraging Data Analytics for Better Financial Decisions

The data generated from credit card processing is a goldmine for financial planning. Most modern payment platforms provide dashboards that show peak sales hours, customer retention rates, and average transaction values. By analyzing these trends, you can make informed decisions about inventory purchases, staffing levels, and expansion capital. Turning your payment processing into a data-gathering tool transforms a standard expense into a strategic asset.

Conclusion: Building a Scalable Financial Ecosystem

Accepting credit card payments is one of the most significant financial milestones for any business. It bridges the gap between a local operation and a global participant in the digital economy. However, the true value lies not just in the ability to take a payment, but in the strategic selection of the underlying financial infrastructure.

By understanding the difference between merchant accounts and PSPs, decoding complex fee structures, and utilizing data-driven tools, you can ensure that your payment processing system supports, rather than hinders, your profit margins. As your business grows, continue to audit your processing statements and leverage your transaction volume to negotiate better rates, ensuring that your financial ecosystem remains lean, secure, and ready for scale.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.