In the modern digital economy, the convenience of peer-to-peer (P2P) payment applications has revolutionized how we handle micro-transactions. Venmo, a subsidiary of PayPal, has become the de facto standard for splitting dinner checks, paying rent, or sending birthday gifts. However, as the platform’s popularity has surged, so too have the concerns surrounding its digital security. When we ask, “How safe is Venmo?” we are not just asking about the company’s solvency; we are interrogating the robustness of its encryption, the integrity of its data protocols, and the efficacy of its fraud prevention algorithms.

From a technological standpoint, Venmo operates at the intersection of financial software and social networking. This dual nature introduces unique security challenges that go beyond traditional banking. To understand the safety of the platform, one must look under the hood at the technical safeguards in place and the evolving landscape of digital threats.

The Architecture of Security: How Venmo Protects Your Data

At its core, Venmo utilizes bank-grade security protocols to ensure that every transaction and piece of user data is shielded from unauthorized access. The platform’s security architecture is built on a multi-layered defense strategy designed to protect data both at rest and in transit.

Data Encryption and Transmission Protocols

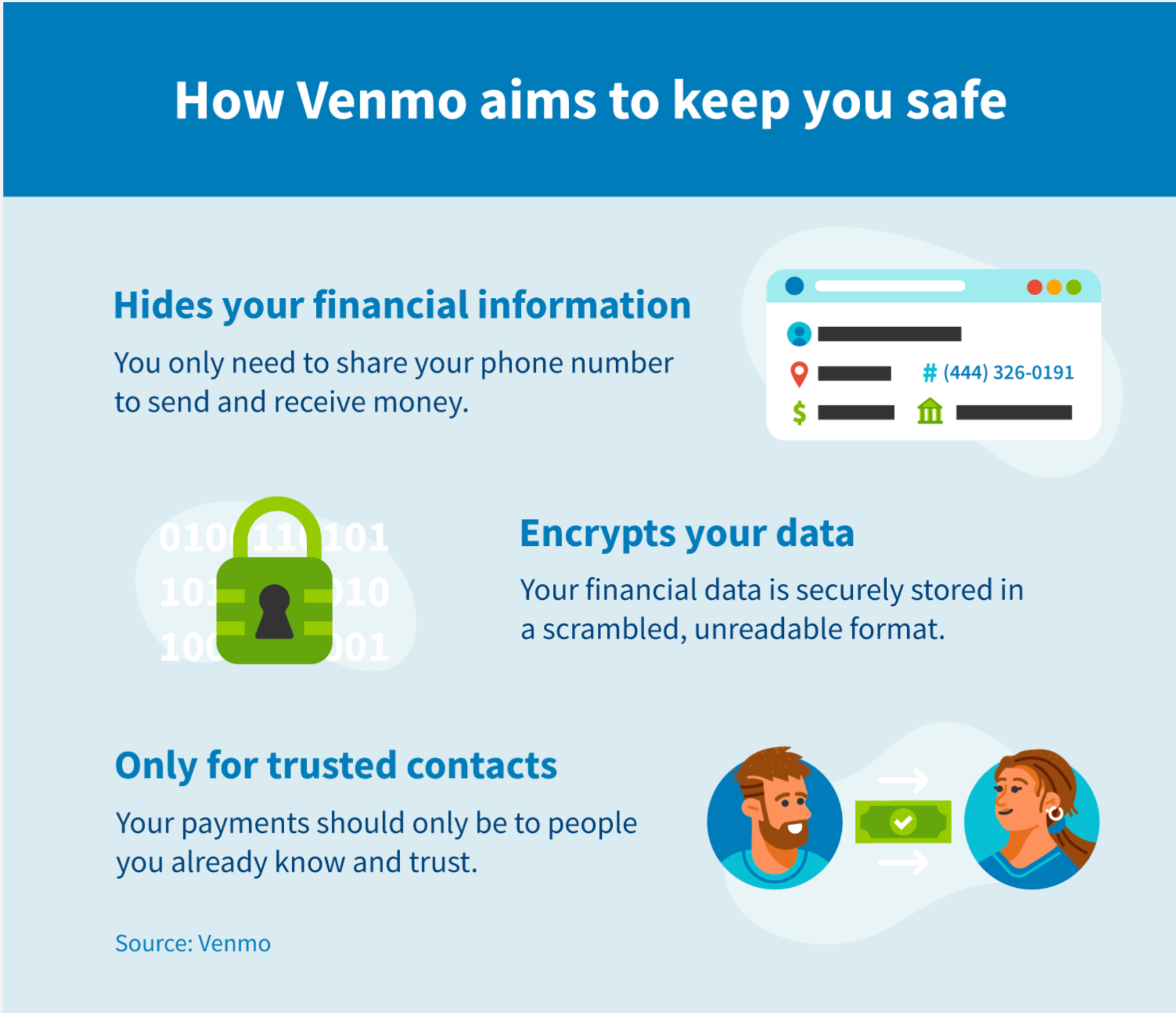

Venmo employs 256-bit encryption, a standard utilized by major financial institutions and government agencies. This means that when you send money, the data is scrambled into a complex code that would take modern computers billions of years to crack through brute force. Furthermore, Venmo utilizes Transport Layer Security (TLS) and Secure Sockets Layer (SSL) protocols for all communications between the app and its servers. These protocols ensure that even if a malicious actor were to intercept the data stream—for instance, over a compromised public Wi-Fi network—they would find nothing but unreadable ciphertext.

Multi-Factor Authentication (MFA) and Biometric Security

The first line of defense for any digital wallet is user authentication. Venmo has integrated sophisticated Multi-Factor Authentication (MFA) that triggers whenever a login attempt is made from an unrecognized device or IP address. This usually involves a time-sensitive numerical code sent via SMS or email.

Beyond standard passwords, the app leverages mobile hardware capabilities through biometric security. By utilizing Apple’s FaceID/TouchID or Android’s fingerprint sensors, Venmo ensures that the physical possession of the device is coupled with a biological identifier. This creates a “hardware-backed” security layer, making it significantly more difficult for remote hackers to drain an account even if they have obtained the user’s primary credentials.

Vulnerabilities and the Human Element: Why Security Isn’t Just About Code

Even the most sophisticated encryption can be bypassed if the user is manipulated into opening the door. In the tech world, the “human element” is often the weakest link in the security chain. For Venmo, the risks often manifest through social engineering rather than direct software exploits.

Social Engineering and Phishing Attacks

Phishing remains one of the most prevalent threats to P2P security. Technical “spoofing” allows attackers to send SMS messages or emails that appear to originate from Venmo’s official support tech. These messages often claim there is an “issue with your account” and provide a link to a cloned website designed to harvest login credentials and bank details.

The danger here is not a failure of Venmo’s internal code, but a failure of the interface between the software and the user. Sophisticated attackers may even use “vishing” (voice phishing) to trick users into revealing their MFA codes. Understanding that Venmo will never ask for a password or a verification code over the phone is a critical component of maintaining digital safety.

The Risks of the “Public Feed” Culture

One of Venmo’s unique—and most controversial—features is its social feed. By default, transactions were historically set to “Public,” revealing who you paid, when, and for what (though not the amount). From a cybersecurity perspective, this is a goldmine for “OSINT” (Open Source Intelligence) gathering.

A malicious actor can analyze a user’s public feed to identify patterns, such as where they shop, who their roommates are, and when they typically pay their bills. This data can be used to craft highly targeted spear-phishing attacks. While Venmo has since updated its privacy settings to be more restrictive, the legacy of public data sharing remains a cautionary tale of how social features can inadvertently compromise technical security.

Platform Safeguards and Fraud Prevention Mechanisms

Behind the user interface, Venmo employs advanced machine learning and artificial intelligence to monitor billions of transactions in real-time. This invisible layer of security is designed to catch fraudulent activity before it results in a financial loss.

Behavioral Monitoring and AI-Driven Risk Assessment

Venmo’s backend systems use behavioral analytics to create a “digital fingerprint” of a user’s typical activity. This includes tracking geographic location, device IDs, transaction frequency, and typical payment amounts. If a user who typically sends $20 for coffee suddenly attempts to send $2,000 to an unverified account in another country, the system’s AI triggers an immediate flag.

These algorithms are trained on massive datasets provided by PayPal’s global infrastructure, allowing Venmo to identify “signature” patterns of known fraud rings. When a transaction is deemed high-risk, the system may delay the transfer, require additional verification, or block the transaction entirely to protect the user’s linked bank account.

Purchase Protection: Understanding the Limits

A common technical misunderstanding among users is the difference between “Friends and Family” transfers and “Goods and Services” payments. Venmo’s “Purchase Protection” is a specific software protocol that offers coverage for eligible transactions. When a user marks a payment as a purchase, the platform implements a dispute resolution framework similar to a credit card.

However, the technology is designed specifically for authorized merchants. If a user sends money to a stranger via the “Friends and Family” protocol for a Craigslist purchase, they are essentially bypassing the platform’s security safeguards. In these instances, the tech cannot “undo” the blockchain-style finality of the transfer, leaving the user vulnerable.

Best Practices for Hardening Your Digital Wallet

While Venmo provides a robust framework, the ultimate security of a digital wallet depends on how the user configures the software. Hardening your Venmo account involves diving into the settings menu to minimize the “attack surface.”

Optimizing Privacy Settings for Maximum Anonymity

The most effective way to secure a Venmo account is to transition from a social-first to a security-first configuration. Within the app’s privacy settings, users should set their default transaction visibility to “Private.” This ensures that only the sender and recipient can see the transaction details, effectively blinding OSINT-gathering bots.

Additionally, users should regularly audit their “Friends” list. In the age of digital stalking and social engineering, limiting your visible network prevents attackers from using your social graph to build rapport or verify your identity during a scam attempt.

Managing Linked Accounts and Third-Party Permissions

From a technical standpoint, Venmo is a bridge between your bank and the digital world. To limit potential damage, security experts often recommend linking a credit card rather than a debit card or direct bank account. Credit cards offer an additional layer of legal protection and do not provide a direct pipeline to your primary liquid assets.

Furthermore, users should periodically review “Connected Apps.” Many third-party services request API access to your Venmo data for budgeting or rewards. Each connected app represents a potential backdoor. By navigating to the “Apps” section in settings, users can revoke permissions for any service they no longer use, ensuring that a data breach at a minor startup doesn’t lead to a compromise of their Venmo credentials.

Conclusion: A Balanced View of Digital Safety

Is Venmo safe? From a purely technical perspective, the answer is a resounding yes. Its use of high-level encryption, multi-factor authentication, and AI-driven fraud detection puts it on par with most modern banking applications. The platform’s infrastructure is managed by PayPal, one of the most experienced players in the digital payment space, ensuring that the software is constantly patched and updated against the latest exploits.

However, the “safety” of Venmo is a shared responsibility. The transition of money from a physical wallet to a digital app necessitates a shift in how we perceive security. It is no longer just about keeping a leather folder in a back pocket; it is about managing digital identities, recognizing social engineering tactics, and properly configuring software settings. By leveraging the built-in technological safeguards and remaining vigilant against the human-centric threats that target the platform, users can enjoy the convenience of Venmo without sacrificing their financial or digital security.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.