The annual tax refund check often feels like a bonus, a welcome windfall that many taxpayers eagerly anticipate. For some, it’s a chance to pay down debt, for others, an opportunity to save or invest, and for many, a well-deserved treat after a year of hard work. However, the question “how much tax refund should I get?” isn’t just about the dollar amount; it’s a profound dive into personal finance, financial planning, and understanding how your money works with the government. While a large refund can feel satisfying, it often signifies an interest-free loan you’ve provided to the government throughout the year. Understanding the optimal refund amount, or even whether a refund is truly optimal, is crucial for savvy financial management.

This comprehensive guide will demystify the tax refund process, explore the factors that influence its size, and provide actionable strategies to help you optimize your tax situation, ensuring you get the right amount back, or pay the right amount in, for your specific financial goals.

Understanding the Nature of Your Tax Refund

Before diving into calculations and strategies, it’s essential to grasp the fundamental concept of a tax refund and what it truly represents within your financial landscape. This foundational understanding will empower you to make more informed decisions about your tax planning.

What is a Tax Refund, Really?

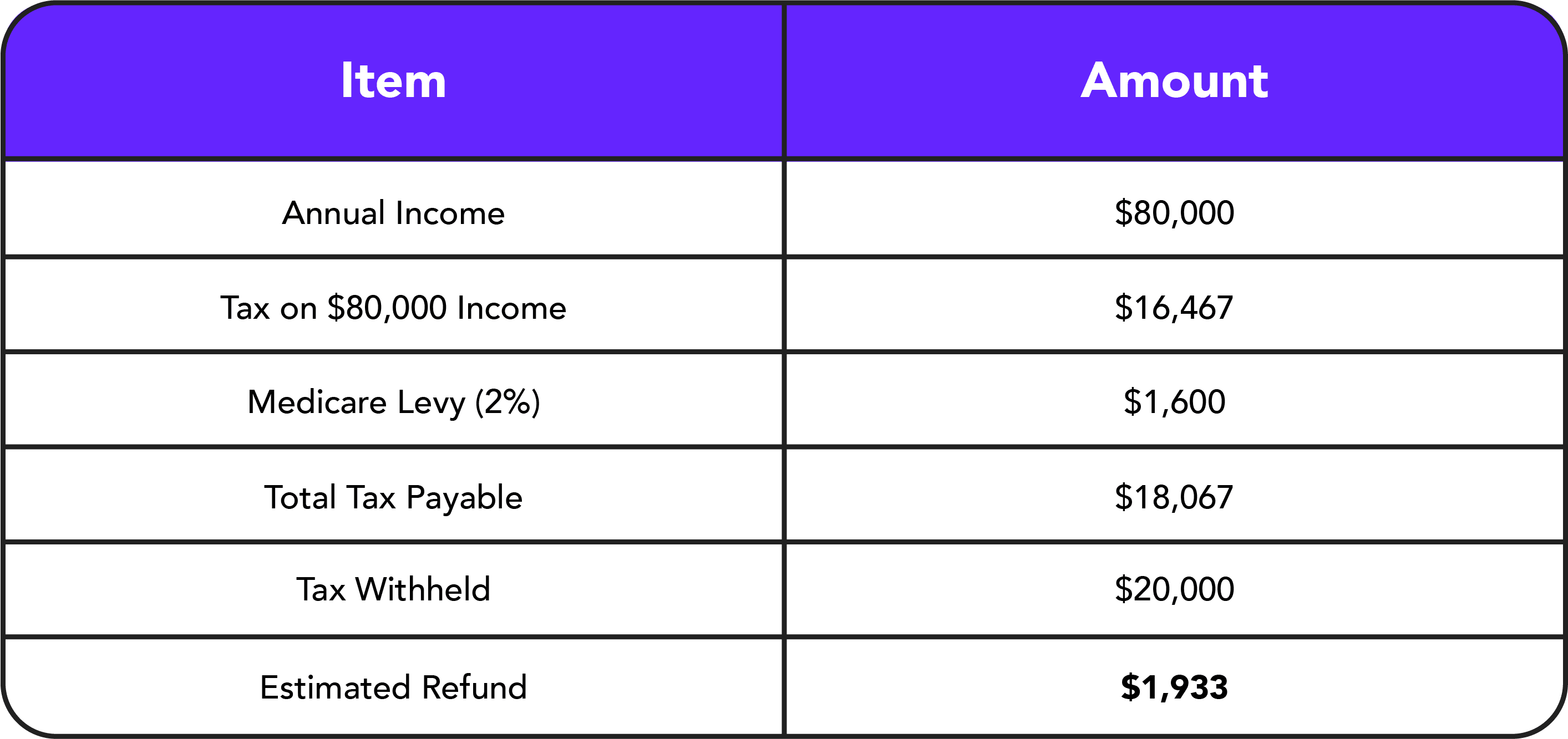

At its core, a tax refund occurs when you have paid more in taxes throughout the year than your actual tax liability. Most employed individuals have federal income tax (and often state income tax) withheld from each paycheck. This withholding is an estimate of what you will owe based on the information you provide on your W-4 form. Self-employed individuals typically pay estimated taxes quarterly. If the total amount withheld or paid through estimates exceeds your final tax bill calculated after accounting for all income, deductions, and credits, the government owes you money back – that’s your refund. It’s not extra money the government is giving you; it’s simply your own money being returned.

The Myth of the “Big Refund”

For many, a large tax refund is celebrated as a financial victory. While receiving a substantial sum can feel good, it’s often a sign of suboptimal financial planning throughout the year. Think of it this way: if you received a $3,000 refund, it means that, on average, an extra $250 of your money was withheld from your paychecks each month. That $250 could have been in your bank account, earning interest, contributing to an investment portfolio, paying down high-interest debt, or simply providing more immediate liquidity for your monthly expenses.

The “big refund” myth perpetuates the idea that it’s “found money,” when in reality, it’s an interest-free loan you’ve given to the government. While some people intentionally overpay to force themselves to save, it’s generally not the most financially efficient strategy.

Why a Refund Isn’t Always a Win

While it’s certainly better to receive a refund than to owe a large sum, an excessively large refund indicates that your withholding or estimated payments were too high. This effectively means you’ve had less access to your own money throughout the year, missing out on potential opportunities:

- Lost Opportunity Cost: The money sitting with the IRS could have been invested, potentially earning returns.

- Reduced Liquidity: Having less disposable income each month can make budgeting tighter or necessitate borrowing at higher interest rates for unexpected expenses.

- Inflation Erosion: The purchasing power of your money slightly erodes over time due to inflation. While a minor factor over a single year, it’s still worth noting.

The ideal scenario for many financial experts is to have a tax refund that is very small or to owe a small amount. This indicates that your withholding was accurately matched to your tax liability, maximizing your cash flow throughout the year without incurring penalties.

Key Factors Influencing Your Tax Refund Amount

Understanding the variables that contribute to your tax liability and, consequently, your refund or amount due is crucial for effective tax planning. These factors interact in complex ways, and a change in one can significantly impact the final outcome.

Income and Withholding (W-4)

Your gross income is the starting point for calculating your tax liability. The more you earn, generally, the higher your tax bill will be. However, it’s the amount of tax withheld from your paychecks that directly impacts your refund. When you start a new job or experience a life change, you fill out a W-4 form. This form tells your employer how much federal income tax to withhold. Factors on your W-4 include:

- Filing Status: Single, Married Filing Jointly, Head of Household, etc.

- Dependents: The number of qualifying children and other dependents you have.

- Other Income: If you have income from other jobs, self-employment, or investments.

- Deductions and Credits: Anticipated deductions or credits you plan to claim.

An incorrectly filled out W-4 is a primary driver of either a large refund or a large amount owed. If you claim too many allowances or indicate too many deductions/credits, too little tax might be withheld. Conversely, if you claim too few, too much will be withheld.

Deductions: Standard vs. Itemized

Deductions reduce your taxable income, meaning you pay tax on a smaller portion of your earnings. You generally choose between taking the standard deduction or itemizing your deductions, opting for whichever provides a greater reduction in your taxable income.

- Standard Deduction: A fixed dollar amount set by the IRS that varies based on your filing status and age/blindness. For many taxpayers, especially those without significant specific expenses, the standard deduction is the simpler and more beneficial choice.

- Itemized Deductions: If your eligible expenses exceed the standard deduction amount, you can itemize. Common itemized deductions include state and local taxes (SALT, capped at $10,000), home mortgage interest, medical expenses exceeding a certain percentage of your Adjusted Gross Income (AGI), and charitable contributions.

The choice between these two can significantly alter your taxable income and, by extension, your refund.

Credits: Reducible Tax Liability Dollar-for-Dollar

Tax credits are particularly powerful because they directly reduce your tax liability dollar-for-dollar, unlike deductions which only reduce the amount of income subject to tax. Some credits are even “refundable,” meaning they can reduce your tax liability below zero, resulting in a payment to you even if you paid no tax.

Examples of common tax credits include:

- Child Tax Credit: For qualifying children.

- Earned Income Tax Credit (EITC): For low-to moderate-income working individuals and families.

- Education Credits: Such as the American Opportunity Tax Credit or Lifetime Learning Credit.

- Child and Dependent Care Credit: For expenses related to care for a qualifying individual.

- Credit for Other Dependents: For dependents who don’t qualify for the Child Tax Credit.

- Retirement Savings Contributions Credit (Saver’s Credit): For low and moderate-income individuals saving for retirement.

The availability and amount of credits you qualify for can dramatically sway your refund amount, often turning a potential payment into a significant refund.

Life Changes and Major Events

Your tax situation is rarely static. Significant life events throughout the year can have a substantial impact on your tax liability and, therefore, your refund. These include:

- Marriage or Divorce: Changes your filing status.

- Birth or Adoption of a Child: Qualifies you for the Child Tax Credit and potentially other benefits.

- Purchase or Sale of a Home: Impacts mortgage interest, property taxes, and potential capital gains/losses.

- Change in Employment Status: New job, job loss, starting a side hustle, or retirement.

- Higher Education Expenses: For yourself or dependents.

- Major Medical Expenses: Potentially leading to itemized deductions.

- Significant Charitable Contributions: Another itemized deduction opportunity.

Failing to adjust your tax planning in response to these events is a common reason for unexpected refund amounts.

Investment and Other Income Sources

Beyond wages, various other income sources can affect your tax bill:

- Investment Income: Capital gains from stock sales, dividends, and interest income.

- Rental Income: Income from properties you own.

- Self-Employment Income: Income from freelancing, consulting, or operating a small business.

- Retirement Account Distributions: Withdrawals from 401(k)s, IRAs, etc.

- Gambling Winnings: Taxable income that often doesn’t have withholding.

Each of these sources can add to your taxable income, and without proper estimated tax payments or adjustments, they can lead to an unexpected tax bill or a smaller-than-expected refund.

Strategies to Optimize Your Tax Situation (and Refund/Payment)

Now that you understand the mechanics, let’s explore proactive strategies to align your tax outcome with your financial goals. The aim is not necessarily to get the largest refund, but the optimal refund or payment, reflecting accurate tax planning.

Adjusting Your Withholding

This is the most direct way to control the amount of tax taken from your paycheck. Review your W-4 form annually, especially after major life events. The IRS Tax Withholding Estimator tool is an excellent resource. By accurately filling out your W-4, you can:

- Increase Take-Home Pay: By reducing over-withholding, more of your money is available throughout the year.

- Reduce a Large Refund: If you consistently get a substantial refund, adjust your W-4 to have less tax withheld.

- Avoid Underpayment Penalties: If you consistently owe a large amount, increase your withholding to avoid penalties for underpaying estimated taxes.

Consider updating your W-4 for each employer if you have multiple jobs or if your spouse also works, to avoid under-withholding collectively.

Maximizing Deductions and Credits

Being diligent about tracking eligible expenses and understanding available credits can significantly reduce your tax burden.

- Keep Meticulous Records: Retain receipts and documentation for all potential deductions and credits, especially for medical expenses, charitable donations, and business expenses.

- Understand Standard vs. Itemized: Annually compare your potential itemized deductions against the standard deduction to ensure you’re taking the most beneficial option.

- Claim All Eligible Credits: Research and ensure you’re claiming every credit you qualify for, as credits offer the most direct tax savings. This is particularly true for education, dependent care, and retirement savings credits.

- Contribute to HSAs: Health Savings Accounts (HSAs) offer a triple tax advantage: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

Utilizing Tax-Advantaged Accounts

Strategic use of retirement and health savings accounts can provide significant tax benefits, reducing your taxable income and improving your overall financial health.

- Traditional IRA/401(k): Contributions are often tax-deductible, lowering your current taxable income. This is an excellent way to reduce your tax bill while saving for retirement.

- Roth IRA/401(k): While contributions are not tax-deductible, qualified withdrawals in retirement are tax-free. This doesn’t reduce your current tax liability but offers future tax advantages.

- Flexible Spending Accounts (FSAs): For healthcare or dependent care, contributions are pre-tax, reducing your taxable income. Be mindful of the “use it or lose it” rule.

- 529 Plans: While contributions aren’t federally tax-deductible, earnings grow tax-deferred, and qualified withdrawals for education expenses are tax-free. Many states also offer a tax deduction for contributions.

The Role of Professional Tax Advice

For complex financial situations, significant life changes, or if you’re unsure about optimizing your taxes, consulting a qualified tax professional (CPA or Enrolled Agent) is invaluable. They can:

- Identify obscure deductions and credits you might miss.

- Provide personalized advice tailored to your unique financial circumstances.

- Help with proactive tax planning, not just reactive filing.

- Ensure compliance and minimize audit risk.

The cost of professional advice is often outweighed by the tax savings and peace of mind they provide.

Planning Throughout the Year

Tax planning shouldn’t be a once-a-year event in spring. Adopt a proactive, year-round approach:

- Quarterly Review: Especially if you’re self-employed or have variable income, review your income, expenses, and withholding quarterly.

- Mid-Year Check-Up: Around July or August, estimate your annual income, deductions, and credits. This allows time to adjust withholding or make estimated payments before year-end.

- Year-End Moves: In December, look for opportunities to make additional deductible contributions (e.g., to IRAs), accelerate or defer income/expenses, or make charitable donations.

When to Expect Your Refund and What to Do With It

After all the planning and filing, the final step is receiving your refund. Understanding the timeline and having a plan for your money is just as important as the tax preparation itself.

The IRS Refund Timeline

The IRS typically issues most refunds within 21 calendar days of receiving your e-filed return, assuming there are no issues. However, several factors can extend this timeline:

- Paper Returns: Take significantly longer to process (6-8 weeks or more).

- Errors on Your Return: Can delay processing while the IRS investigates.

- Returns Claiming EITC or ACTC: Due to fraud prevention measures, the IRS cannot issue refunds that include the Earned Income Tax Credit (EITC) or Additional Child Tax Credit (ACTC) before mid-February.

- Taxpayer Identity Verification: If the IRS needs to verify your identity.

The “Where’s My Refund?” tool on the IRS website is the best resource for tracking your refund status.

Smart Ways to Use Your Refund

While it’s tempting to splurge, a tax refund represents an opportunity to significantly boost your financial well-being. Consider these smart uses:

- Pay Down High-Interest Debt: Credit card debt, personal loans, or other high-interest obligations. This offers an immediate, guaranteed return by reducing interest payments.

- Build an Emergency Fund: Aim for 3-6 months of living expenses. A refund can be a great way to jumpstart or replenish this crucial financial safety net.

- Invest for the Future: Contribute to an IRA, 401(k), 529 plan, or a taxable brokerage account. Even a modest investment can grow significantly over time.

- Fund a Major Goal: Save for a down payment on a home, a new car, or a significant educational expense.

- Home Improvements: Especially those that increase value or reduce energy costs.

- Professional Development: Invest in courses or certifications that can boost your career earnings.

Avoiding Common Refund Pitfalls

Be wary of common mistakes that can diminish the positive impact of your refund:

- Impulse Spending: Resist the urge to blow your refund on non-essential items. Have a plan before it arrives.

- High-Cost “Refund Anticipation Loans”: These loans charge high fees and effectively allow you to borrow against your refund, which is typically issued quickly anyway.

- Ignoring Future Tax Planning: Don’t just celebrate the refund; use the experience to inform your tax planning for the upcoming year. If it was too large, adjust your W-4.

Ultimately, the question “how much tax refund should I get?” is not about a magical number, but about striking a balance. It’s about ensuring you’re meeting your tax obligations efficiently, maximizing your cash flow throughout the year, and strategically using any refund to advance your personal financial goals. By understanding the factors involved and taking proactive steps, you can transform tax season from a stressful obligation into an opportunity for financial empowerment.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.