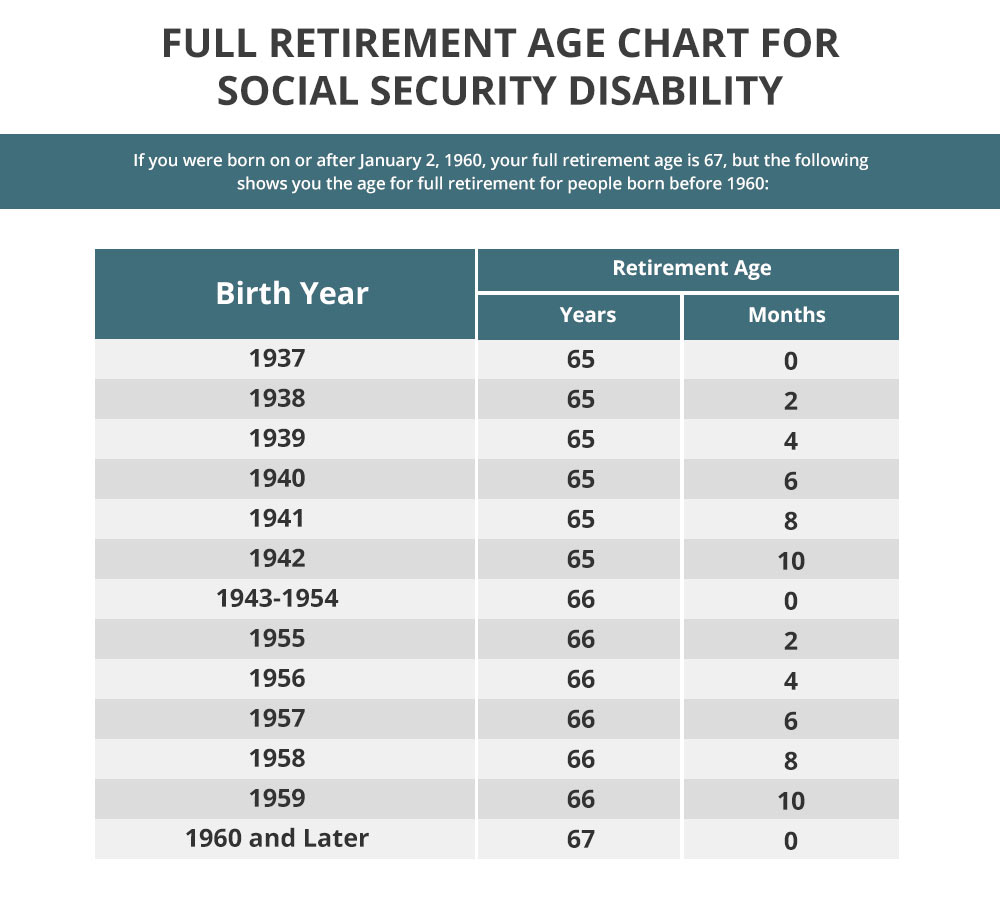

Navigating the financial landscape of Social Security Disability Insurance (SSDI) is a critical task for anyone whose career has been interrupted by a long-term disability. Unlike supplemental programs designed for those with limited resources, SSDI is a formal insurance program funded by your own payroll taxes. Consequently, the answer to “how much will I receive” is not a flat rate, but a personalized figure based on your specific financial history.

For many, this monthly payment becomes the cornerstone of their personal finance strategy. Understanding the calculation methods, the variables that influence the final check, and how to project these figures accurately is essential for long-term budgeting and financial security.

The Foundation of SSDI: Your Earnings History and Work Credits

The first step in determining your SSDI benefit is understanding that the program is intrinsically linked to your “covered” earnings. These are the wages on which you paid Social Security taxes (FICA). From a financial planning perspective, your SSDI benefit is an earned insurance payout, much like a private disability policy, but managed by the federal government.

The Role of Social Security Credits

To be eligible for any payment at all, you must have accumulated enough “work credits.” In 2024, you earn one credit for every $1,730 of earnings, up to a maximum of four credits per year. Generally, most workers need 40 credits, 20 of which must have been earned in the last 10 years ending with the year you become disabled. However, younger workers may qualify with fewer credits. If you haven’t hit these benchmarks, your benefit amount is effectively zero, making this the most crucial prerequisite in your financial assessment.

Verifying Your Social Security Statement

The most accurate tool for a preliminary estimate is your Social Security Statement. Available through a “my Social Security” account online, this document provides a year-by-year breakdown of your taxed earnings. For a professional financial audit, verifying this statement is vital. Errors in your reported income from a decade ago can result in a lower monthly benefit today. Because your payment is based on your lifetime average earnings, ensuring every dollar you earned is recorded correctly is the first step in maximizing your future cash flow.

Decoding the Formula: AIME and PIA

The Social Security Administration (SSA) uses a complex, multi-step formula to arrive at your monthly benefit amount. It is not as simple as taking a percentage of your last paycheck. Instead, the SSA looks at your entire career and adjusts those figures for inflation.

Average Indexed Monthly Earnings (AIME)

The calculation begins with your Average Indexed Monthly Earnings (AIME). The SSA takes your top-earning years (the number of years varies based on your age at the time of disability) and “indexes” them. Indexing is a financial adjustment that brings your past earnings up to date with current wage levels. For example, $20,000 earned in 1995 is worth significantly more in today’s economy, and the indexing process reflects that. These indexed earnings are then averaged and divided by 12 to find your monthly average.

The Primary Insurance Amount (PIA) and Bend Points

Once the AIME is established, the SSA applies a formula to determine your Primary Insurance Amount (PIA). This is where the progressive nature of the benefit becomes apparent. The formula uses “bend points”—specific dollar thresholds that change annually.

For 2024, the formula is:

- 90% of the first $1,174 of your AIME.

- 32% of your AIME between $1,174 and $7,078.

- 15% of any AIME amount over $7,078.

This weighted formula ensures that lower-income earners receive a higher percentage of their previous income as a benefit, while higher-income earners receive a larger absolute dollar amount but a lower “replacement rate.” This is a key consideration for high-earning professionals who may find that SSDI alone does not cover their lifestyle costs, highlighting the need for supplemental private disability insurance.

Variables That Adjust Your Monthly Payment

Even after the PIA is calculated, several external factors can increase or decrease the actual amount deposited into your bank account. Financial planning for SSDI requires an awareness of these moving parts.

Cost-of-Living Adjustments (COLA)

SSDI benefits are protected against inflation through annual Cost-of-Living Adjustments (COLA). Based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), these adjustments ensure that your purchasing power remains relatively stable. For retirees and disability recipients, the COLA is a vital hedge against the rising costs of healthcare and daily living. When budgeting for the long term, it is wise to view SSDI as an inflation-indexed asset.

The Impact of Other Disability Benefits (Offsets)

If you receive other public disability benefits, such as Workers’ Compensation or public disability payments from a state or local government, your SSDI check may be reduced. The “Social Security Offset” rule states that the total amount of SSDI plus other public disability benefits cannot exceed 80% of your average current earnings before you became disabled. If it does, the SSA will deduct the excess from your SSDI payment. Notably, private disability insurance and Veterans Affairs (VA) benefits do not usually trigger this reduction.

Auxiliary Benefits for Family Members

From a household finance perspective, it is important to realize that SSDI is not just for the individual. Certain family members—such as children under 18 or a spouse caring for a child—may be eligible for “auxiliary benefits.” This can increase the total family income by up to 50% to 80% of your PIA. There is a “family maximum” cap, however, which usually falls between 150% and 180% of your individual benefit.

Tax Implications and Financial Management of SSDI

Receiving SSDI is not just about the gross amount; it’s about the net amount you keep after taxes and deductions. Many recipients are surprised to learn that their disability benefits may be taxable, depending on their total household income.

Taxation of Benefits

Whether you pay taxes on your SSDI depends on your “combined income,” which is the sum of your adjusted gross income, non-taxable interest, and half of your SSDI benefits.

- If you are a single filer and your combined income is between $25,000 and $34,000, you may pay income tax on up to 50% of your benefits.

- If it exceeds $34,000, up to 85% of your benefits may be taxable.

- For joint filers, these thresholds are $32,000 and $44,000, respectively.

Understanding these thresholds is critical for tax planning, especially if your spouse is still working or if you have significant investment income.

Medicare Premiums

After receiving SSDI for 24 months, you automatically become eligible for Medicare. While Part A (hospital insurance) is usually free, Part B (medical insurance) requires a monthly premium. This premium is typically deducted directly from your SSDI check. As of 2024, the standard premium is $174.70. When calculating your “take-home” SSDI, you must account for this deduction, as it effectively reduces your monthly liquid cash flow.

Strategies for Supplemental Income and Back Pay

While the monthly SSDI check is the primary focus, there are other financial windfalls and opportunities associated with the program that can bolster your financial position.

Calculating Back Pay and Retroactive Benefits

Because the SSDI application process often takes months or even years, the SSA typically owes you “back pay.” This is a lump sum covering the period from when you applied (or when you became disabled) to when you were finally approved. However, the SSA applies a five-month waiting period from the onset of disability during which no benefits are paid. Calculating this lump sum involves looking at your monthly PIA multiplied by the months of eligibility, minus the waiting period. This lump sum can be used to pay off debts accrued during the waiting period or invested as an emergency fund.

The Trial Work Period (TWP)

For those looking to supplement their income, the SSA offers the Trial Work Period. This allows you to test your ability to work for at least nine months (not necessarily consecutive) while receiving your full SSDI benefits, regardless of how much you earn. In 2024, any month where you earn more than $1,110 counts as a trial work month. This is a powerful financial tool for those who want to transition back into the workforce or explore side hustles without the immediate fear of losing their safety net.

In conclusion, determining “how much SSDI you will receive” requires a deep dive into your professional earnings history, an understanding of the SSA’s mathematical formulas, and a clear-eyed look at tax and insurance deductions. By viewing SSDI through a financial lens—treating it as an earned, inflation-protected annuity—you can more effectively integrate these benefits into a comprehensive wealth management and survival strategy. Knowing your numbers is the first step toward reclaiming financial agency during a challenging period of life.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.