Determining the exact percentage of your paycheck that should go toward savings is one of the most pivotal decisions you will make for your long-term financial health. While the “correct” number often feels elusive—fluctuating based on your age, income, and lifestyle goals—establishing a disciplined framework is essential. Saving is not merely about hoarding cash; it is about buying your future freedom, mitigating risk, and ensuring that your future self is as well-cared-for as your present self.

This guide explores the foundational benchmarks of personal finance, delves into the nuances of various life stages, and provides actionable strategies to help you determine and achieve your ideal savings rate.

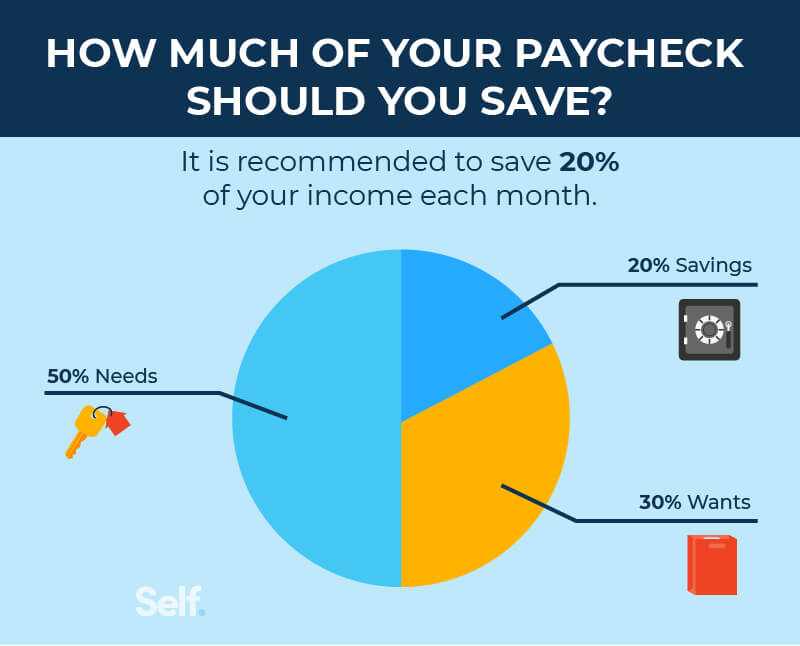

The 50/30/20 Rule: A Universal Starting Point

In the world of personal finance, the 50/30/20 rule is often cited as the gold standard for beginners and seasoned professionals alike. Popularized by Senator Elizabeth Warren in her book All Your Worth, this rule provides a simple, effective template for budget allocation.

Understanding Needs vs. Wants

The first two components of the 50/30/20 rule focus on your expenditures. According to this framework, 50% of your after-tax income should be dedicated to “Needs”—the non-negotiable costs of living such as rent or mortgage payments, groceries, utilities, insurance, and minimum debt repayments.

The next 30% is allocated to “Wants.” This category is often the most difficult to manage, as it encompasses lifestyle choices like dining out, travel, hobby equipment, and streaming subscriptions. By capping these at 30%, you ensure that your current enjoyment does not come at the expense of your future security.

The 20% Savings Mandate

The final 20% is the core of the “How much should I save?” question. Under this rule, at least one-fifth of your take-home pay should be directed toward financial goals. This includes building an emergency fund, contributing to retirement accounts (like a 401(k) or IRA), and making extra payments on high-interest debt.

If 20% feels unattainable initially, the goal is not to give up, but to scale up. Starting at 5% or 10% and gradually increasing your rate as your income grows is a far better strategy than waiting until you can “afford” to save 20%.

Beyond the Basics: Customizing Your Savings Target

While the 50/30/20 rule is an excellent baseline, personal finance is, by definition, personal. Your ideal savings rate may need to be significantly higher or lower depending on your specific circumstances and the timeline of your financial goals.

Savings for Different Life Stages

Your age is a primary factor in determining your savings percentage. If you are in your 20s, time is your greatest asset. Thanks to the power of compound interest, a 15% savings rate starting at age 22 can result in a much larger nest egg than a 30% savings rate starting at age 45.

However, if you are starting your savings journey later in life, you may need to “catch up.” For those in their 40s or 50s with minimal retirement assets, a savings rate of 30% to 40% might be necessary to ensure a comfortable retirement. In this stage of life, the focus shifts from growth to aggressive accumulation and wealth preservation.

High-Income Earners vs. Entry-Level Realities

Income levels also dictate the feasibility of certain percentages. For entry-level workers in high-cost-of-living cities, “Needs” might consume 70% of their income, making a 20% savings rate nearly impossible without extreme frugality. In these cases, the focus should be on “the gap”—the difference between what you earn and what you spend—and finding ways to increase income while keeping expenses flat.

Conversely, high-income earners should aim well beyond the 20% mark. If you are earning a significant salary, your “Needs” likely represent a much smaller fraction of your income. This creates an opportunity to save 40%, 50%, or even more. This philosophy is common in the FIRE (Financial Independence, Retire Early) movement, where individuals prioritize a high savings rate to exit the workforce decades ahead of schedule.

Prioritizing Your Savings Allocation

Knowing how much to save is only half the battle; knowing where to put that money is equally important. Not all savings are created equal, and there is a logical hierarchy you should follow to maximize the efficiency of every dollar.

The Emergency Fund: Your Financial Safety Net

Before investing in the stock market or saving for a down payment on a house, you must establish an emergency fund. Most financial experts recommend saving three to six months’ worth of essential living expenses. This fund should be kept in a high-yield savings account (HYSA) where it is liquid and easily accessible.

The emergency fund serves as your insurance policy against the unexpected—job loss, medical emergencies, or major car repairs. Without this safety net, a single financial shock could force you into high-interest credit card debt, erasing months of progress.

Retirement and Long-Term Compound Growth

Once your emergency fund is stable, the next priority is retirement. If your employer offers a 401(k) match, that should be your first destination. A company match is effectively a 100% return on your investment, and failing to take advantage of it is equivalent to leaving part of your salary on the table.

After securing the match, look toward tax-advantaged accounts like a Roth IRA or a traditional IRA. The goal here is long-term growth. Because these funds are invested in the market, they benefit from the compounding effect over decades. Even a small increase in your savings rate today can result in hundreds of thousands of dollars in additional wealth by the time you retire.

Sinking Funds for Major Purchases

After addressing emergencies and retirement, you can begin saving for “Sinking Funds.” These are dedicated savings buckets for specific, mid-term goals, such as buying a home, purchasing a car, or funding a wedding. By separating these from your general savings, you can track your progress toward specific milestones without dipping into your retirement or emergency reserves.

Strategies to Increase Your Savings Rate Without Deprivation

Many people struggle to save because they view it as a form of deprivation. However, increasing your savings rate is often more about systems and psychology than it is about willpower.

Automating Your Finances

The most effective way to ensure you hit your savings target is to take human error out of the equation. By automating your savings, you “pay yourself first.” Set up your direct deposit so that a portion of your paycheck goes directly into a savings or investment account before it ever hits your checking account. When the money is out of sight, you are forced to live on the remaining balance, naturally aligning your spending with your goals.

The “Lifestyle Creep” Trap

One of the biggest enemies of a high savings rate is lifestyle creep—the tendency to increase your spending as your income rises. When you receive a raise or a bonus, it is tempting to upgrade your car, move to a more expensive apartment, or buy more expensive clothes.

To combat this, apply a “Savings Split” to every raise. For every additional dollar you earn, commit 50% of it to your savings and 50% to improving your current lifestyle. This allows you to enjoy the fruits of your labor while simultaneously accelerating your path to financial independence. This balanced approach ensures that your savings rate increases proportionally with your career progression.

Conclusion: The Power of Consistency

There is no magic percentage that guarantees financial success, but the discipline of saving consistently is the common thread among all financially secure individuals. Whether you start with the 50/30/20 rule or create a bespoke plan that fits your high-income or late-start reality, the act of prioritizing your future is what matters most.

By focusing on an emergency fund first, capturing employer matches, and aggressively avoiding lifestyle creep, you can transform your salary from a monthly survival tool into a powerful engine for wealth creation. Remember, the best time to start saving was yesterday; the second-best time is today. Determine your percentage, automate the process, and let time and compound interest do the heavy lifting for your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.