Determining the ideal portion of your income to allocate to rent is one of the most critical personal finance decisions you’ll make. Housing is typically the largest monthly expense for most individuals and families, directly impacting your ability to save, invest, and achieve other financial goals. While common rules of thumb exist, a truly responsible approach requires a deeper dive into your unique financial situation, lifestyle, and aspirations. This comprehensive guide will dissect the factors at play, moving beyond simple percentages to help you craft a housing budget that supports your overall financial well-being.

The Foundation: Understanding the 30% Rule

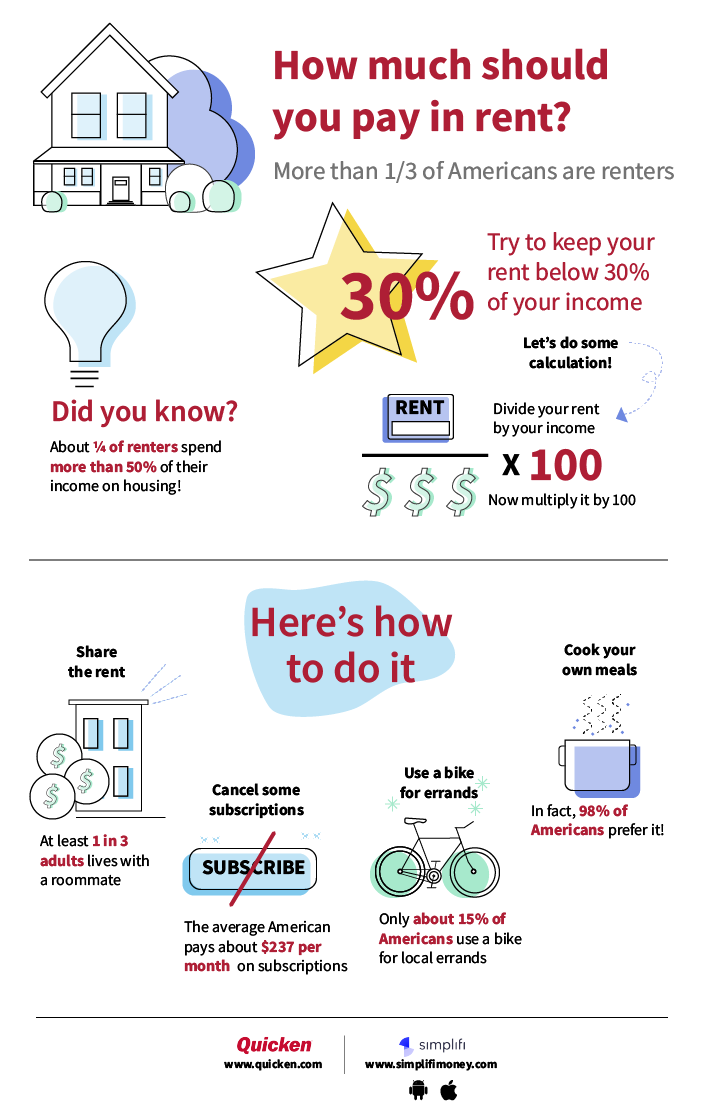

For decades, financial experts and housing authorities have cited a particular guideline for rent affordability. Understanding its origins and limitations is the first step toward informed decision-making.

What is the 30% Rule?

The “30% rule” suggests that your monthly gross income should not exceed 30% of your gross monthly income. Gross income refers to your earnings before taxes and other deductions are taken out. For example, if you earn $5,000 per month gross, your rent should ideally be no more than $1,500. This guideline gained prominence in the U.S. when the federal government established it as a benchmark for “affordable housing” in the 1980s, primarily to determine eligibility for housing assistance programs. It became widely adopted as a general rule for individual budgeting because it offered a straightforward way to assess housing burden.

Why the 30% Rule Exists

The primary rationale behind the 30% rule is to ensure that individuals and households have sufficient income remaining after housing costs to cover other essential expenses, save, and avoid financial distress. When housing costs significantly exceed this threshold, a household is often considered “cost-burdened,” meaning they may struggle to afford necessities like food, transportation, healthcare, and utilities. The rule aims to promote financial stability by preventing housing from becoming an overwhelming drain on personal finances, thereby reducing the risk of debt accumulation and poverty. It acts as a protective measure, encouraging a balanced allocation of resources across different spending categories.

Limitations and Nuances of the 30% Rule

While widely cited, the 30% rule is not a one-size-fits-all solution and has significant limitations, particularly in today’s diverse economic landscape.

Firstly, it doesn’t account for variations in income levels. For very low-income earners, even 30% of their gross income might not be enough to secure decent housing, forcing them to spend a higher percentage out of necessity. Conversely, high-income earners might comfortably spend more than 30% and still have ample disposable income for savings, investments, and discretionary spending without feeling financially strained.

Secondly, the rule often fails to consider the wildly different costs of living in various geographical locations. In high-cost-of-living cities like New York, San Francisco, or London, adhering to the 30% rule can be nearly impossible without significant compromises, such as living far from work or in much smaller spaces. In these areas, a more realistic, albeit still challenging, percentage might climb to 40% or even 50%.

Finally, the 30% rule also overlooks other significant financial obligations that individuals may have, such as student loan debt, credit card debt, car payments, childcare costs, or medical expenses. A person with substantial debt could be severely stressed by a 30% rent payment, whereas someone debt-free might comfortably manage a higher percentage. Therefore, while a useful starting point, the 30% rule must be viewed with a critical understanding of its constraints and adapted to individual circumstances.

Beyond the Rule: Factors Influencing Your Rent-to-Income Ratio

Moving beyond a simple percentage, a more robust financial decision demands a thorough examination of several personal and external factors. This holistic perspective ensures your rent choice aligns with your complete financial picture.

Cost of Living in Your Area

The most significant external factor influencing your rent-to-income ratio is the cost of living in your desired location. Rental markets vary dramatically from one city or neighborhood to another. In competitive urban centers, high demand, limited supply, and robust economies drive rental prices upward, often making the 30% rule impractical. Conversely, in less populated areas or regions with a lower cost of living, adhering to or even staying well below the 30% benchmark might be achievable, freeing up more income for other financial goals. Researching average rental prices, utility costs, transportation expenses, and even grocery prices in your target area is crucial for setting a realistic housing budget. Sites like Numbeo or local real estate platforms can provide valuable insights into regional living costs.

Your Gross vs. Net Income

The 30% rule typically refers to gross income (before taxes and deductions). However, your real purchasing power is determined by your net income (take-home pay). For many, the difference between gross and net can be substantial due to federal, state, and local taxes, social security contributions, health insurance premiums, and retirement plan deductions. If you budget based solely on your gross income, you might overestimate how much you can truly afford, leading to a tight squeeze once rent is due. A more conservative and often safer approach is to calculate your affordability based on your net income or, at the very least, understand the significant gap between gross and net when applying the 30% rule. Some financial advisors even advocate for a “net 25%” rule, meaning your rent should not exceed 25% of your net income, providing a more comfortable buffer.

Your Debt Obligations

Existing debt is a powerful force that dictates your discretionary income. High-interest credit card debt, substantial student loan payments, car loans, or personal loans all reduce the amount of money available for housing without compromising other essential needs or savings goals. Before committing to a rent payment, meticulously list all your monthly debt obligations. A high debt-to-income ratio (DTI) indicates a greater portion of your earnings is already committed, leaving less flexibility for housing. Financial prudence often dictates prioritizing debt reduction, especially high-interest debt, before stretching your budget for a higher rent payment. Consider how a potential rent payment would impact your ability to meet these debt payments comfortably and consistently.

Other Essential Expenses

Beyond rent and debt, a myriad of other essential monthly expenses must be factored into your budget. These include utilities (electricity, gas, water, internet), groceries, transportation costs (car payments, fuel, public transit, insurance), healthcare premiums and out-of-pocket medical expenses, phone bills, and personal care items. These “non-negotiable” costs can quickly accumulate, eating into the remaining percentage of your income. An accurate assessment of these expenses is vital. Failing to account for them can lead to a situation where, despite your rent being “affordable” by the 30% rule, you find yourself constantly short on cash or dipping into savings for everyday necessities.

Your Financial Goals

Ultimately, your housing decision should align with your broader financial aspirations. Are you saving for a down payment on a home? Building an emergency fund? Investing for retirement? Planning a significant purchase or vacation? A higher rent payment may impede these goals by limiting your ability to save and invest. Conversely, choosing a more modest rental that allows you to comfortably hit your savings targets can accelerate your path to financial freedom. Your rent choice isn’t just about what you can afford today; it’s about what you want to achieve tomorrow. Be honest about your priorities, and let them guide your housing budget.

Practical Strategies for Managing Your Rent Budget

Once you understand the financial landscape, implementing practical strategies becomes key to securing suitable housing without overstretching your budget.

Creating a Comprehensive Budget

The cornerstone of any sound financial plan is a detailed budget. This involves meticulously tracking all your income sources and categorizing every expense. Start by listing your net monthly income. Then, itemize all fixed expenses (like debt payments, subscriptions, insurance) and variable expenses (groceries, entertainment, dining out). Once you have a clear picture, you can determine how much truly remains for rent. This exercise might reveal areas where you can cut back, such as reducing discretionary spending, to allocate more towards housing or, ideally, increase your savings. Budgeting isn’t about deprivation; it’s about intentional spending and ensuring your money serves your priorities. Tools like the 50/30/20 rule (50% needs, 30% wants, 20% savings/debt repayment) can offer a broader framework, with rent falling squarely into the “needs” category.

Negotiating Rent and Finding Deals

Many renters mistakenly believe that rental prices are always non-negotiable. While not always possible, there are instances where you can negotiate. If you have excellent credit, a stable job, or are signing a longer lease (e.g., 18-24 months), landlords might be willing to offer a slight discount or waive certain fees (like application fees or pet deposits). Look for properties outside the most sought-after neighborhoods or consider older buildings that might offer more space for less money. Timing can also play a role; rents often drop in the colder months or during times of lower demand. Being prepared to move quickly when a good deal appears can also be advantageous.

Considering Alternatives: Roommates or Smaller Spaces

If your desired living area’s rental prices seem insurmountable based on your income, it’s time to explore alternatives. Taking on one or more roommates can drastically reduce your individual housing cost, allowing you to live in a better location or save significantly. While it requires compromise, the financial benefits can be immense. Another option is to consider a smaller living space. Downsizing from a two-bedroom to a one-bedroom, or from a one-bedroom to a studio, can lead to substantial savings. Minimalist living is not just a trend; it’s a financial strategy that frees up funds for other priorities. Evaluate your true space needs versus your wants.

Increasing Your Income

Sometimes, the most direct path to making rent more affordable is to increase your income. This can involve several strategies:

- Salary Negotiation: If you’re employed, assess your market value and prepare to negotiate for a raise during performance reviews or when accepting a new position.

- Side Hustles: Explore opportunities to earn extra income outside your primary job. This could range from freelancing in your field, driving for ride-sharing services, delivering food, or selling goods online. Even a few hundred extra dollars a month can significantly impact your rent affordability.

- Skill Development: Investing in new skills or certifications can open doors to higher-paying roles, either within your current company or in a new industry.

Increasing your income provides more flexibility than simply cutting expenses, as it expands your overall financial capacity.

The Broader Financial Picture: Rent as Part of Your Wealth Journey

Your rent payment isn’t an isolated expense; it’s an integral part of your long-term financial strategy, influencing everything from savings to retirement.

Rent vs. Buying: A Long-Term Perspective

The decision between renting and buying is complex and heavily influenced by your financial stability, market conditions, and personal goals. Renting offers flexibility, predictable monthly costs (excluding utilities), and freedom from maintenance responsibilities, making it ideal for those who anticipate moving or prefer not to tie up capital in property. However, it doesn’t build equity. Buying, on the other hand, allows you to build equity, potentially benefit from property appreciation, and offers tax advantages. But it comes with significant upfront costs (down payment, closing costs), ongoing expenses (mortgage, property taxes, insurance, maintenance), and reduced liquidity. The “rent vs. buy” calculation should consider factors like how long you plan to stay in an area, current interest rates, property values, and your savings for a down payment. Sometimes, renting cheaply and aggressively saving for a down payment is a smarter long-term move than rushing into a costly home purchase.

The Importance of an Emergency Fund

Regardless of your rent amount, maintaining a robust emergency fund is paramount. This fund, typically 3-6 months’ worth of essential living expenses (including rent), acts as a financial safety net for unexpected events like job loss, medical emergencies, or unforeseen home repairs (if you own). Without an emergency fund, a sudden financial shock could quickly lead to an inability to pay rent, risking eviction or forcing you into high-interest debt. Ensure that your rent budget allows you to consistently contribute to and maintain this vital financial buffer. It’s the foundation of financial security.

Aligning Rent with Your Savings and Investment Goals

Every dollar spent on rent is a dollar that cannot be saved or invested. Therefore, your rent decision directly impacts your ability to achieve long-term financial independence. If your rent is too high, it can hinder contributions to your retirement accounts (401k, IRA), limit your ability to save for a child’s education, or delay investment in other assets. Aim for a rent payment that leaves ample room for consistent savings and investments. Prioritize automated transfers to your savings and investment accounts immediately after payday, before you have a chance to spend the money elsewhere. This “pay yourself first” strategy ensures your financial future is not sacrificed for a larger living space or a more desirable address today. A balanced approach ensures your current living situation supports, rather than detracts from, your future wealth creation.

Tools and Resources for Smart Rent Decisions

Navigating the complexities of housing affordability is made easier with the right financial tools and expert advice.

Budgeting Apps and Software

In the digital age, managing your money has become more accessible than ever. Budgeting apps like Mint, YNAB (You Need A Budget), Personal Capital, or Simplifi can sync with your bank accounts and credit cards, automatically categorizing your transactions. This provides a real-time, granular view of your spending, making it easy to see exactly where your money is going and identify areas for adjustment. Many also offer features to set spending limits, track financial goals, and create custom budgets, which are invaluable for ensuring your rent payment fits comfortably within your overall financial plan. Using these tools regularly can transform a daunting task into an empowering habit, giving you control over your housing and other expenses.

Rent Affordability Calculators

Before you even start house hunting, an online rent affordability calculator can be an indispensable tool. These calculators, often found on real estate websites or financial planning platforms, allow you to input your gross income, debt, and other expenses to estimate a comfortable rent range. While they often rely on the 30% rule as a baseline, many allow for adjustments based on your specific financial situation, providing a more personalized estimate. They can help set realistic expectations, preventing you from looking at properties beyond your means and saving valuable time and frustration in your rental search.

Financial Advisors

For complex financial situations, significant life changes (like a new job or relocation), or simply a desire for expert guidance, consulting a certified financial advisor can be highly beneficial. A financial advisor can help you analyze your complete financial picture, including your income, assets, debts, and long-term goals. They can offer personalized advice on housing affordability, assess the impact of different rent scenarios on your wealth accumulation, and help you integrate your housing decisions into a holistic financial plan. While there is a cost associated with their services, the long-term clarity and optimized financial strategy they provide can be an invaluable investment.

In conclusion, while the 30% rule offers a useful starting point, determining how much of your salary should go to rent is a nuanced decision that demands careful consideration of your individual income, expenses, debt, location, and financial aspirations. By taking a comprehensive approach, utilizing available tools, and making informed choices, you can secure housing that not only meets your needs but also propels you toward your broader financial goals, ensuring a stable and prosperous future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.