The dream of retirement is a universal aspiration, conjuring images of freedom, leisure, and the ability to pursue passions unfettered by daily work. Yet, beneath this idyllic vision lies a crucial question that often keeps individuals awake at night: “How much money do I actually need to retire comfortably?” This isn’t just a rhetorical query; it’s a complex financial puzzle with numerous variables, unique to each individual’s circumstances and aspirations. Fortunately, in an age of sophisticated financial tools, the retirement calculator emerges as an indispensable ally, transforming an intimidating enigma into a manageable, actionable plan.

Understanding your retirement number isn’t merely about having a large sum; it’s about achieving financial independence that supports your desired lifestyle throughout your non-working years. This requires foresight, realistic assumptions, and a clear understanding of the economic landscape. From inflation’s subtle erosion of purchasing power to the unpredictable nature of market returns and the ever-increasing longevity of human life, many factors influence this critical calculation. Far from being a magic bullet, a retirement calculator serves as a powerful projection tool, offering a tangible starting point and guiding you through the intricate pathways of long-term financial planning. It quantifies the gap between your current savings and your future needs, empowering you to adjust your savings rate, investment strategy, or retirement timeline to bridge that divide effectively.

Understanding the Retirement Riddle: More Than Just a Number

Determining your retirement nest egg isn’t a one-size-fits-all calculation. It’s a highly personalized equation influenced by a multitude of factors, many of which evolve over time. Ignoring these nuances can lead to significant shortfalls, impacting your financial security and peace of mind during your golden years. The “number” isn’t static; it’s a dynamic target that requires careful consideration of various personal and economic elements.

Defining Your Retirement Lifestyle

The first step in calculating your retirement needs is to envision your post-work life. Will you downsize your home, travel extensively, pursue expensive hobbies, or simply enjoy a quiet life at home? Your desired lifestyle directly dictates your annual retirement expenses. A common rule of thumb suggests needing 70-80% of your pre-retirement income to maintain your lifestyle, but this can vary wildly. Someone planning to live frugally in a low-cost area might need less, while an avid traveler or someone with significant healthcare costs might need considerably more. Detail your projected expenses: housing, utilities, food, transportation, healthcare, entertainment, travel, and any discretionary spending. This realistic projection forms the bedrock of your retirement income needs.

The Silent Threat of Inflation

Inflation is the quiet destroyer of purchasing power, a factor often underestimated in long-term financial planning. A dollar today will not buy the same amount of goods or services in 20 or 30 years. If your retirement plan assumes current-day costs, you could be setting yourself up for a significant shortfall. For example, if inflation averages 3% annually, something that costs $100 today will cost approximately $180 in 20 years and $240 in 30 years. Retirement calculators typically incorporate an inflation rate to project future expenses more accurately, converting today’s projected lifestyle costs into future dollars. Failing to account for inflation means your carefully calculated nest egg could feel much smaller than anticipated when you actually retire.

Longevity Risk: Planning for a Longer Life

People are living longer, healthier lives, which is fantastic news but also presents a unique financial challenge: longevity risk. While a longer life offers more years to enjoy retirement, it also means more years during which you’ll need your savings to last. A retirement plan based on living until 85 might be insufficient if you live until 95 or even 100. Modern retirement calculators often allow you to input your life expectancy, or they use actuarial tables to provide a reasonable estimate. It’s often prudent to plan for a longer lifespan than you might initially assume, perhaps into your mid-90s, to ensure your funds don’t run out prematurely. This buffer provides peace of mind and flexibility should you enjoy an exceptionally long and fulfilling retirement.

The Anatomy of a Retirement Calculator: Key Inputs and Outputs

A retirement calculator is essentially a sophisticated projection tool that takes a set of inputs and, through a series of financial formulas, produces an estimate of your retirement readiness. To get the most accurate results, it’s crucial to understand what information these calculators need and how they use it. Think of it as providing ingredients for a recipe; the quality and accuracy of your inputs directly determine the quality of the output.

Essential Data Points: Income, Savings, and Expenses

At the core of any retirement calculation are your current financial specifics.

- Current Age and Desired Retirement Age: These define the length of your accumulation phase and the duration of your retirement.

- Current Savings: The existing balance in your retirement accounts (401(k)s, IRAs, brokerage accounts) forms your starting capital.

- Annual Savings Rate: How much you contribute each year to your retirement accounts is a critical driver of your future wealth. Even small increases in your savings rate can have a significant impact over decades due to compounding.

- Current Income: While not always directly an input for the calculator, it’s essential for determining your savings capacity and for projecting a percentage of current income for your retirement lifestyle.

- Projected Retirement Expenses: As discussed, a realistic estimate of your annual spending in retirement is paramount. This can be a percentage of current income or a detailed breakdown of future costs.

Investment Growth and Rate of Return Assumptions

One of the most impactful, yet often challenging, inputs is your assumed rate of return on investments. This is the average annual percentage gain you expect your investments to generate throughout your working and retirement years. Most calculators will ask for a pre-retirement and a post-retirement rate of return.

- Pre-retirement: During your accumulation phase, you might have a higher allocation to equities, potentially allowing for a higher assumed rate of return (e.g., 6-8%).

- Post-retirement: Once retired, many opt for a more conservative portfolio to preserve capital, which typically implies a lower assumed rate of return (e.g., 4-6%).

It’s vital to be realistic here; overly optimistic assumptions can lead to a misleadingly low “number,” while overly pessimistic ones might discourage saving. Consider historical market averages and your personal risk tolerance when setting these figures. Some advanced calculators may even allow for different rates of return based on asset allocation or Monte Carlo simulations.

Considering Social Security and Other Income Streams

Your retirement nest egg doesn’t necessarily have to cover 100% of your retirement expenses. Many individuals will have other income sources that can significantly reduce the amount you need to save.

- Social Security Benefits: For many, Social Security will be a foundational component of their retirement income. Calculators often ask for your estimated annual Social Security benefit, which you can typically find on your annual Social Security statement or through the Social Security Administration’s website. The age at which you claim benefits will impact the amount you receive.

- Pensions: If you are fortunate enough to have a defined-benefit pension, this will also be a reliable income stream.

- Part-time Work/Side Gigs: Some individuals plan to work part-time in retirement or pursue hobbies that generate income.

- Rental Income/Other Investments: Income from rental properties, annuities, or other passive investments should also be factored in.

By including these guaranteed or highly probable income streams, the calculator can provide a more accurate picture of the supplemental income your personal savings will need to generate, thereby giving you a more precise savings target.

Beyond the Calculator: Essential Strategies for a Secure Retirement

While a retirement calculator provides the roadmap, it’s your consistent action and strategic planning that will ultimately lead you to your destination. The numbers generated by the calculator are not a guarantee but a powerful guide for informed decision-making. Translating those numbers into a tangible reality requires discipline, foresight, and a willingness to adapt.

Starting Early and Compounding Power

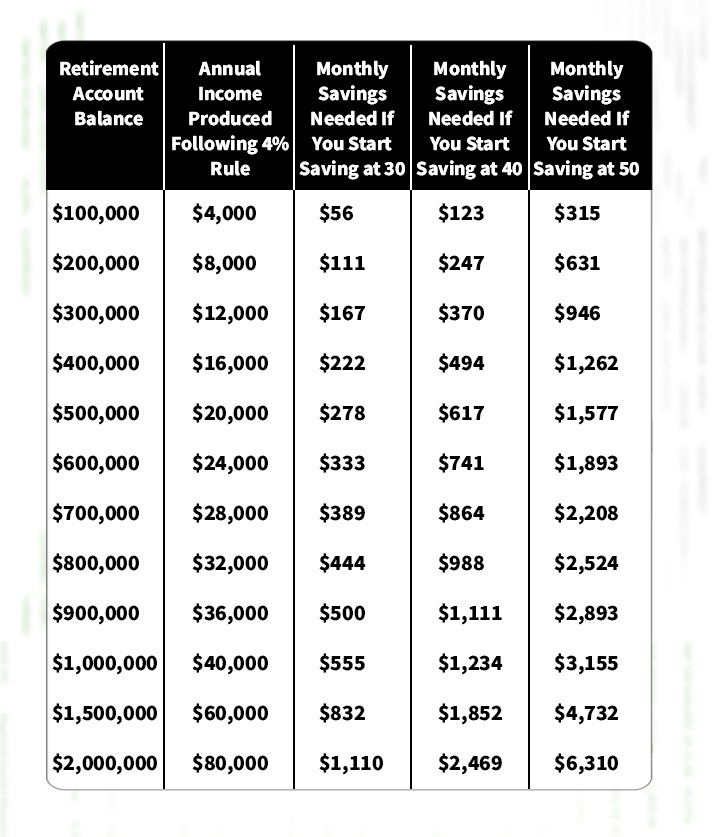

The most impactful strategy for retirement planning is to start as early as possible. The magic of compounding interest is truly astonishing. Even small, consistent contributions made over a long period can accumulate into a substantial sum, far surpassing what you might achieve by saving larger amounts later in life. For example, a 25-year-old saving $500 a month will likely accumulate significantly more by age 65 than a 35-year-old saving $1,000 a month, assuming the same rate of return. The extra decade of compounding works wonders. Delaying even a few years can drastically increase the amount you need to save monthly to catch up, making early action the most potent weapon in your retirement arsenal.

Diversifying Your Investment Portfolio

How you invest your savings is just as important as how much you save. A diversified investment portfolio spreads your risk across various asset classes, such as stocks, bonds, and real estate, reducing the impact of poor performance in any single area. For younger individuals, a higher allocation to equities, which historically offer higher returns but also greater volatility, is often appropriate. As you approach retirement, gradually shifting towards a more conservative mix with a higher proportion of bonds can help protect your accumulated capital from market downturns. Regularly rebalancing your portfolio to maintain your desired asset allocation is also crucial. Remember, diversification doesn’t eliminate risk, but it manages it effectively, helping to ensure consistent growth towards your retirement goal.

Adapting Your Plan: Regular Reviews and Adjustments

Your retirement plan should not be a static document. Life happens: careers change, salaries fluctuate, family needs evolve, and market conditions shift. Regularly reviewing your retirement plan – ideally once a year or whenever a significant life event occurs – is essential.

- Re-run the Calculator: Update your inputs (salary, savings rate, market performance) to see if you’re still on track.

- Assess Progress: Are your investments performing as expected? Are your contributions sufficient?

- Adjust as Needed: If you’re falling behind, consider increasing your savings, adjusting your investment strategy, or potentially rethinking your retirement age or lifestyle. If you’re ahead, you might have the flexibility to retire earlier or enhance your retirement lifestyle.

Proactive adjustments ensure that your retirement plan remains relevant and achievable throughout your working life and into retirement.

Choosing the Right Retirement Calculator and Maximizing Its Use

With a plethora of retirement calculators available online, selecting the right one and understanding how to leverage it effectively can make a significant difference in your financial planning journey. Not all calculators are created equal, and their utility depends on your personal situation and the level of detail you require.

Features to Look for in a Retirement Calculator

When evaluating retirement calculators, consider the following features for a more comprehensive and accurate projection:

- Inflation Adjustment: Essential for realistic long-term planning.

- Social Security Integration: Allows you to factor in estimated benefits.

- Multiple Income Streams: The ability to include pensions, part-time work, or rental income.

- Tax Considerations: Some advanced calculators can factor in taxes on withdrawals, significantly impacting your net retirement income.

- “What If” Scenarios: The ability to easily adjust variables (e.g., retire earlier, save more, different market returns) to see the impact.

- Sensitivity Analysis (Monte Carlo Simulation): Higher-end calculators use this to run thousands of simulations with varied market returns, providing a range of possible outcomes and the probability of success, rather than just a single deterministic number.

- User-Friendly Interface: An intuitive design makes it easier to input data and interpret results.

Different Types of Calculators: Basic vs. Advanced

- Basic Calculators: These are generally free, found on many financial websites, and require minimal inputs (current age, desired retirement age, current savings, annual contributions, estimated rate of return, and desired retirement income). They provide a quick, rough estimate and are good for getting a ballpark figure.

- Advanced Calculators: Offered by brokerage firms, financial planning software, or specialized websites, these delve into much greater detail. They allow for more nuanced inputs like varying inflation rates, specific asset allocations, different tax rates, future healthcare costs, and the ability to model specific spending patterns year by year. They often incorporate Monte Carlo simulations for a more robust analysis of probability. While more complex, they offer a far more precise and personalized projection.

The Calculator as a Starting Point: When to Seek Professional Advice

A retirement calculator is an invaluable self-service tool, providing a solid foundation for your retirement planning. However, it’s crucial to view it as a starting point, not the definitive end-all-be-all of your financial strategy. For complex situations, significant assets, or if you feel overwhelmed by the process, a financial advisor can provide personalized guidance. An advisor can help you:

- Develop a holistic financial plan: Integrating retirement with estate planning, tax planning, and risk management.

- Optimize investment strategies: Tailoring asset allocation to your specific risk tolerance and goals.

- Navigate complex rules: Such as Roth conversions, Social Security claiming strategies, and required minimum distributions (RMDs).

- Provide accountability: Keeping you on track with your savings and investment goals.

The calculator empowers you with knowledge, but a professional advisor can help turn that knowledge into a robust, executable strategy tailored to your unique journey towards a financially secure retirement.

The journey to a comfortable retirement is a marathon, not a sprint. It demands consistent effort, smart decisions, and the willingness to adapt. The “how much money do I need to retire calculator” is more than just a tool; it’s a compass, guiding you through the intricate financial landscape towards your ultimate destination: a fulfilling and financially independent retirement. By leveraging its power and combining it with sound financial strategies, you can transform a daunting question into a confident, well-executed plan.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.