In the rapidly evolving landscape of digital finance, instant access to funds has become less of a luxury and more of an expectation. Venmo, a leading peer-to-peer payment platform, offers a convenient “Instant Transfer” service designed to bridge the gap between your Venmo balance and your bank account with unparalleled speed. However, this convenience comes at a cost, and understanding the nuances of the Venmo instant transfer fee is crucial for making informed financial decisions. For individuals and small businesses alike, every percentage point and every dollar saved contributes to better financial health. This article delves into the specifics of Venmo’s instant transfer fees, explores strategies for managing them, and offers a broader perspective on their impact on personal finance.

Understanding Venmo’s Instant Transfer Service

Venmo has revolutionized the way people send and receive money, particularly for social payments and splitting costs. Its core strength lies in its simplicity and widespread adoption among younger demographics. While sending money between Venmo users is free, and standard bank transfers are also free, the instant gratification of immediate fund availability from your Venmo balance to your linked bank account carries a specific charge.

What is Venmo Instant Transfer?

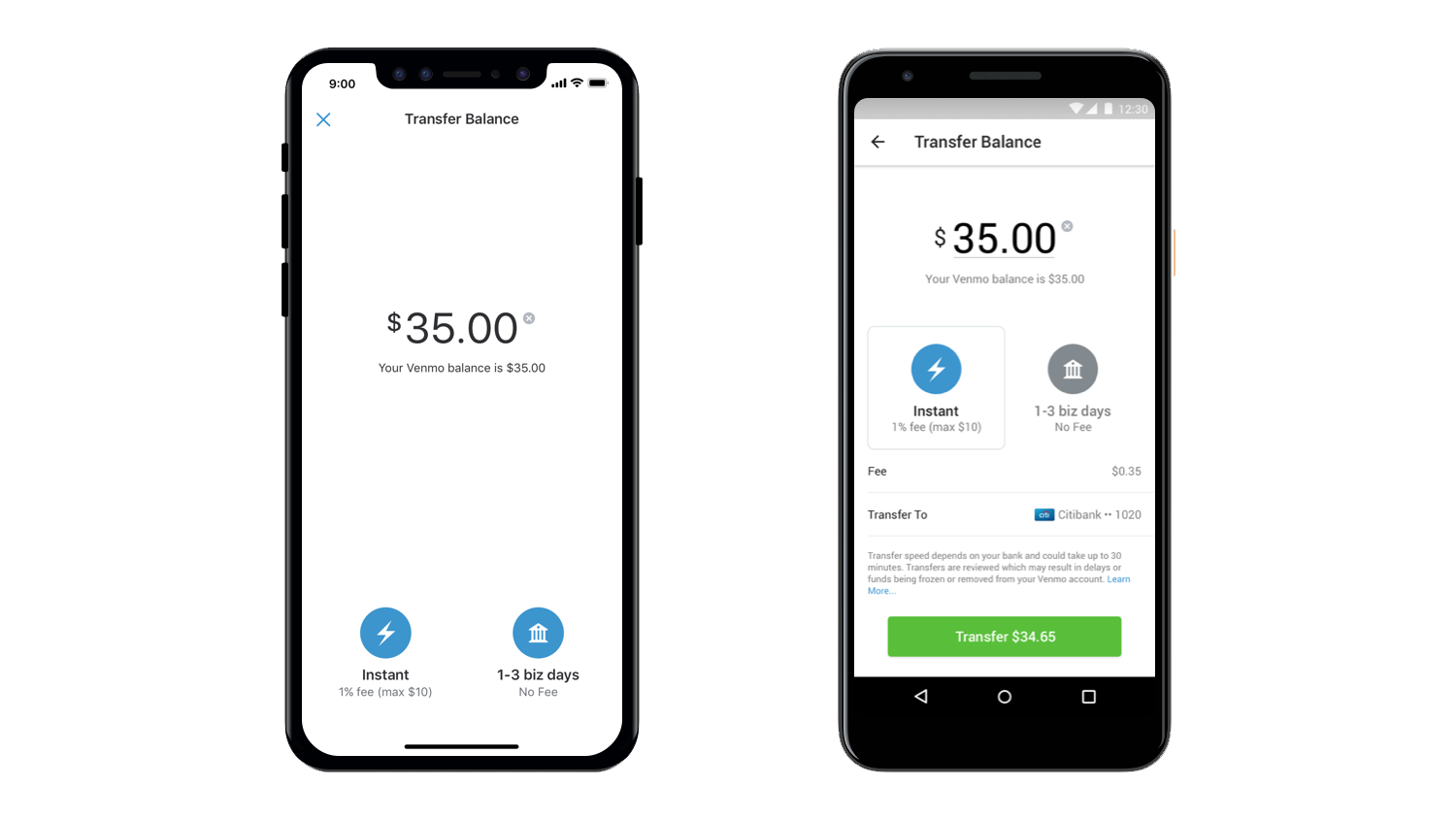

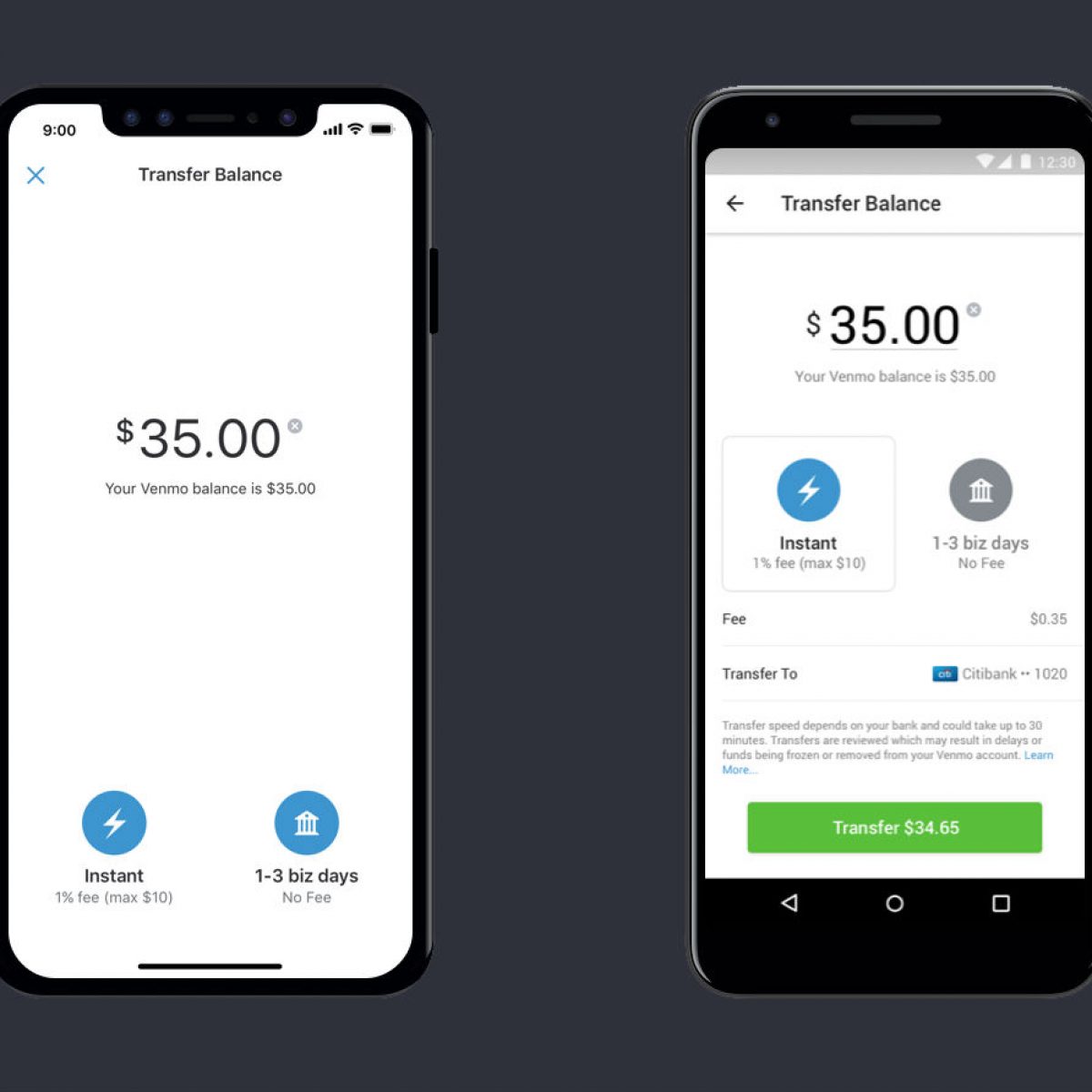

Venmo Instant Transfer is a feature that allows users to move money from their Venmo balance to their eligible U.S. bank account or debit card typically within 30 minutes, although often much faster. This contrasts sharply with standard bank transfers, which can take 1–3 business days to process. The service is particularly appealing in situations where immediate access to funds is critical, such as covering an unexpected expense, making an urgent payment, or simply needing cash in hand from a recent Venmo payment. It’s an on-demand liquidity solution, offering users flexibility and control over their money when time is of the essence.

How It Differs from Standard Transfers

The fundamental difference between Venmo Instant Transfer and a standard transfer boils down to speed versus cost. A standard transfer, which takes 1-3 business days, incurs no fee. Venmo processes these transfers through the Automated Clearing House (ACH) network, a system designed for batch processing of transactions, which inherently takes longer but is cost-effective for financial institutions to offer without direct charges to consumers. Instant Transfer, on the other hand, bypasses this slower system by leveraging faster payment rails, often involving real-time payment networks or direct integrations with card networks. This expedited service incurs a processing cost for Venmo, which is then passed on to the user in the form of a fee. Choosing between the two options is a direct trade-off between the urgency of accessing funds and the desire to avoid additional charges.

The Growing Need for Faster Payments

The demand for faster payments isn’t unique to Venmo users; it’s a global financial trend driven by the digital age. In an economy where transactions happen instantly across various platforms, waiting days for funds to clear can be frustrating and even detrimental to financial planning. Gig economy workers, small business owners, and individuals managing tight budgets often rely on quick access to their earnings. The ability to instantly move money can prevent overdrafts, facilitate timely bill payments, and provide peace of mind. This growing need has propelled services like Venmo Instant Transfer into the mainstream, making understanding their associated costs more important than ever for smart financial management.

Deconstructing the Instant Transfer Fee

To effectively manage your finances when using Venmo, it’s essential to have a clear understanding of the exact fees involved with instant transfers. These fees are not arbitrary but are structured to cover the costs of providing an expedited service.

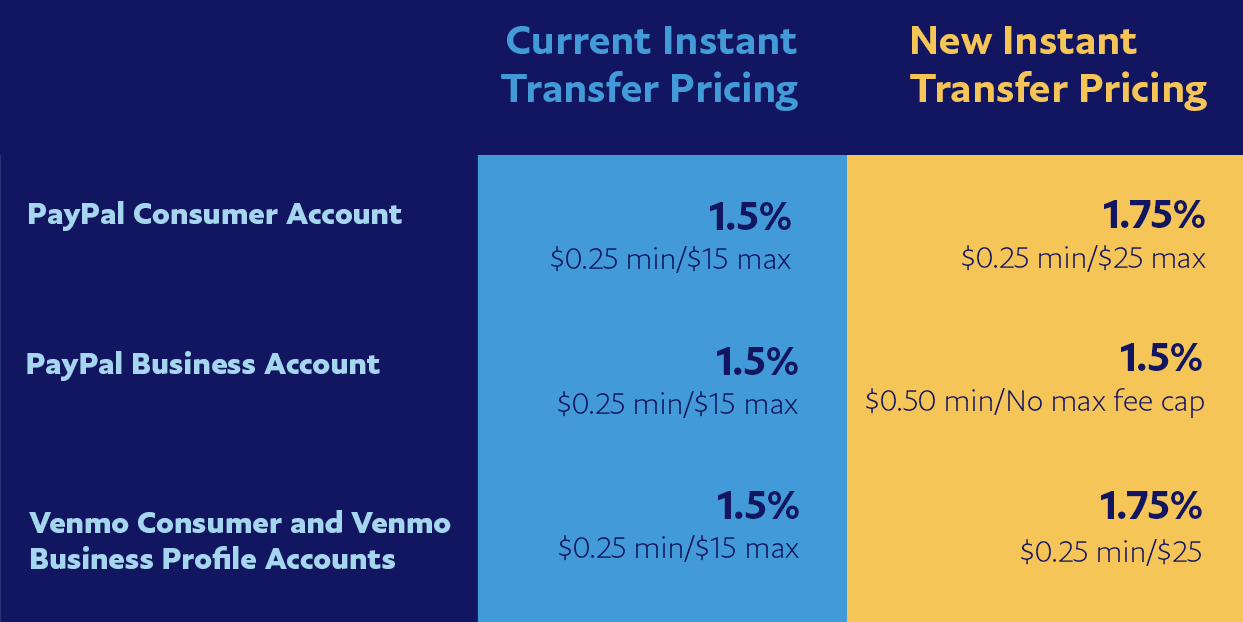

The Standard Venmo Instant Transfer Fee

As of recent policies, the standard Venmo Instant Transfer fee is 1.75% of the amount transferred, with a minimum fee of $0.25 and a maximum fee of $25.00. This percentage-based structure means that the larger the amount you transfer, the higher the fee will be, up to the stated maximum. For instance, if you transfer $100 instantly, the fee would be $1.75. If you transfer $1,000, the fee would be $17.50. However, if you were to transfer a very large sum, say $2,000, the 1.75% would calculate to $35, but due to the $25.00 cap, your fee would only be $25.00. Conversely, for very small transfers, like $10, the 1.75% would be $0.175, but because of the $0.25 minimum fee, you would still be charged $0.25. This fee structure is designed to be relatively straightforward, but users should always double-check the exact amount displayed before confirming an instant transfer.

Venmo Debit Card & Credit Card Instant Transfer Fees

It’s important to distinguish between transferring from your Venmo balance to a bank account or debit card, and using a linked credit card to send money. The 1.75% fee discussed above applies when you’re pulling money out of your Venmo balance instantly to a linked debit card or bank account. When you send money to another Venmo user using a linked credit card as your funding source, Venmo charges a separate fee, typically 3% of the transaction amount. This 3% fee applies because credit card transactions incur significant processing costs for Venmo. Therefore, if you’re trying to move money instantly to your bank, it’s the 1.75% fee. If you’re paying a friend from a credit card, it’s a 3% fee. Using your Venmo balance, linked bank account, or debit card to send money to another Venmo user remains free.

Calculating Your Instant Transfer Cost

To avoid surprises, always calculate the fee beforehand. The calculation is simple:

- For transfers between $14.29 and $1,428.57: Multiply the transfer amount by 0.0175.

- For transfers less than $14.29: The fee will be the minimum of $0.25.

- For transfers greater than $1,428.57: The fee will be the maximum of $25.00.

For example:

- Transferring $50: $50 * 0.0175 = $0.88

- Transferring $5: Fee = $0.25 (due to minimum)

- Transferring $3000: Fee = $25.00 (due to maximum)

Venmo’s app clearly displays the fee amount before you confirm the instant transfer, so there’s no need for manual calculation if you pay attention to the confirmation screen.

Why Does Venmo Charge a Fee?

The instant transfer fee isn’t arbitrary; it’s a fundamental aspect of Venmo’s business model for providing expedited services. Firstly, instant transfers utilize faster payment networks and systems that incur higher interchange and processing fees for Venmo compared to the ACH network used for standard transfers. These real-time payment infrastructures are more expensive to access and operate. Secondly, the fee contributes to Venmo’s overall revenue, helping to support the platform’s development, customer service, and security measures. Like many freemium models, Venmo offers a valuable core service (free peer-to-peer payments) and monetizes premium features (instant transfers, credit card payments to friends). This allows the platform to sustain itself while offering a convenient, often essential, service to its users.

Strategies for Minimizing or Avoiding Instant Transfer Fees

While the convenience of instant transfers is undeniable, consistently paying the fee can add up, especially for frequent users. Adopting smart financial habits can help minimize these costs and ensure you’re getting the most value from your digital payment tools.

Embracing Standard Transfers

The most straightforward way to avoid the instant transfer fee is to opt for a standard bank transfer. These transfers are completely free and typically arrive in your linked bank account within 1-3 business days. If you anticipate needing access to your Venmo balance, initiate a standard transfer a few days in advance. This requires a bit of foresight and planning, but for non-urgent situations, it’s a simple and effective money-saving strategy. Regularly evaluating your cash flow needs can help you determine when you can afford to wait.

Planning Ahead: Timing Your Withdrawals

Effective financial planning is key to mitigating instant transfer fees. Instead of waiting until the last minute, make it a habit to check your Venmo balance periodically, especially after receiving significant payments. If you know you’ll need a certain amount in your bank account for upcoming bills or expenses, proactively initiate a free standard transfer. This approach integrates your Venmo balance into your broader personal finance strategy, allowing you to treat it as a more traditional bank account rather than a temporary holding spot for funds. Budgeting and forecasting your cash needs can significantly reduce reliance on urgent, fee-incurring transfers.

Exploring Alternative Payment Platforms

The digital payment landscape is competitive, and Venmo isn’t the only player offering instant transfer capabilities. Platforms like PayPal (Venmo’s parent company), Cash App, and Zelle each have their own fee structures and transfer speeds. Zelle, for instance, often allows for instant transfers directly between participating bank accounts with no fees, provided both the sender and receiver’s banks support it. While not a direct Venmo alternative for pulling money from a Venmo balance, it can be an alternative for sending and receiving money quickly in other contexts. It’s worth researching these alternatives to understand their fee structures and determine if a different platform might be more cost-effective for specific types of transactions or if you frequently need to move money in ways that incur high fees on Venmo.

Utilizing Direct Deposit for Venmo

Venmo has introduced features like direct deposit for paychecks and government payments. If your employer or benefit provider supports direct deposit to Venmo, receiving funds this way can offer certain advantages. While it doesn’t directly eliminate the fee for pulling money out of Venmo, it ensures your funds arrive in your Venmo balance without any initial fees, and sometimes, depending on the specific product (e.g., Venmo Debit Card), can offer faster access or integration without fees for certain uses. However, the 1.75% fee still generally applies if you wish to instantly transfer these directly deposited funds from your Venmo balance to an external bank account. The primary benefit here is streamlining the initial receipt of funds, which can then be managed strategically with standard transfers.

When Is Paying the Instant Transfer Fee Justified?

Despite the cost, there are indeed valid and often necessary situations where paying the Venmo instant transfer fee is entirely justified. The value of immediate access to funds can sometimes outweigh the small percentage fee, particularly in critical financial moments.

Emergency Situations and Urgent Needs

Life is unpredictable, and emergencies often come without warning. Whether it’s an unexpected medical bill, an urgent car repair, or a sudden travel expense, having immediate access to funds can be a lifesaver. In such scenarios, waiting 1-3 business days for a standard transfer is simply not an option. The small fee pales in comparison to the potential negative consequences of delayed payments, such as late fees, service interruptions, or even health risks. Here, the instant transfer fee acts as an insurance premium for financial agility.

Business Use Cases

For small businesses, freelancers, and sole proprietors who use Venmo for client payments, cash flow is paramount. They might receive a payment via Venmo and immediately need those funds to pay a vendor, purchase supplies, or cover payroll. Delays in accessing funds can disrupt operations, strain relationships with suppliers, or even lead to missed opportunities. In these contexts, the instant transfer fee can be viewed as a legitimate business expense, enabling smooth and efficient financial operations. The cost of delay often far exceeds the instant transfer fee.

Bridging Cash Flow Gaps

Even with careful budgeting, temporary cash flow gaps can occur. Perhaps a large bill is due before your next paycheck arrives, but you have sufficient funds sitting in your Venmo balance from recent reimbursements or sales. An instant transfer can provide the necessary liquidity to bridge this short-term gap, preventing overdraft fees at your bank, avoiding late payment penalties, or ensuring a crucial payment is made on time. In these instances, the fee is essentially a convenience charge for maintaining financial stability and avoiding more costly alternatives.

The Value of Time: Quantifying Convenience

Beyond emergencies and business needs, there’s a more subjective but equally valid justification: the value of your time and peace of mind. For some individuals, the convenience of instantly moving funds, knowing they are settled and accessible, is worth the small fee. This can be particularly true for those with very busy schedules, who find the mental load of planning standard transfers or remembering to check their balance to be more taxing than the financial cost of an instant transfer. Ultimately, quantifying the value of convenience is a personal decision, but it’s a legitimate factor in determining when the fee is acceptable.

Broader Financial Implications and Best Practices

Understanding the Venmo instant transfer fee is just one piece of the puzzle in comprehensive personal finance. Integrating this knowledge into broader financial planning can lead to more effective money management and help users leverage digital tools wisely.

Budgeting for Transaction Fees

Any recurring fees, no matter how small, should be accounted for in your personal or business budget. If you frequently use Venmo’s instant transfer service, categorize these fees as a regular expense. By acknowledging and planning for these costs, you prevent them from becoming an unexpected drain on your finances. This could mean allocating a small monthly budget for “digital transfer fees” or simply factoring them into the cost of transactions where they are incurred. Over time, these small amounts can add up, so diligent budgeting ensures you maintain control over your spending.

The Importance of Financial Planning

Reliance on instant transfers often highlights a need for more robust financial planning. While useful in emergencies, frequent use might indicate a lack of sufficient emergency savings or suboptimal cash flow management. Building an emergency fund that can cover 3-6 months of living expenses reduces the need to pull funds instantly from various sources. Similarly, creating a realistic budget and sticking to it can prevent situations where urgent access to funds is required to cover basic needs. Proactive financial planning is the ultimate strategy for minimizing all types of transaction fees by reducing the urgency of financial movements.

Comparing Financial Tools: A Holistic Approach

Venmo is one of many financial tools available to consumers. When managing your money, it’s beneficial to compare the features, benefits, and fee structures of various platforms. This includes not only other peer-to-peer payment apps but also traditional banking services, online banks, and even credit unions. Some checking accounts offer faster direct deposit options, some investment platforms have quick withdrawal processes, and certain debit cards might integrate better with specific payment networks for instant access. A holistic approach involves choosing the right tool for the right job, understanding that no single platform is perfect for all financial needs, and optimizing your toolkit to minimize costs and maximize convenience.

Security Considerations and Best Practices

While not directly related to fees, security is paramount when using any financial tool, including Venmo. Always ensure your Venmo account is secured with a strong, unique password and two-factor authentication. Be wary of phishing scams and only send money to trusted individuals. While Venmo instant transfers are secure in terms of the transaction process itself, ensuring the security of your account prevents unauthorized transfers and protects your overall financial well-being. Regular monitoring of your Venmo activity and linked bank account statements can help detect any suspicious activity promptly.

The Venmo instant transfer fee, at 1.75% with a minimum of $0.25 and a maximum of $25.00, represents the cost of unparalleled speed and convenience in accessing your funds. While it’s a necessary charge for the service Venmo provides, informed users can navigate these fees strategically. By understanding when to opt for free standard transfers, planning financial movements, and leveraging instant transfers only when truly justified by urgency or business need, individuals can maintain better control over their finances. Ultimately, effective money management involves a thoughtful approach to all transaction costs, ensuring that every financial decision contributes positively to your overall fiscal health.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.