For eligible members of the military community and their families, USAA is often a top contender for car insurance. Renowned for its exceptional customer service and competitive rates, it’s no wonder many wonder about the cost of coverage. However, pinpointing an exact figure for USAA car insurance isn’t straightforward. Premiums are highly personalized, fluctuating based on a myriad of factors unique to each driver, vehicle, and geographic location. This comprehensive guide will delve into the intricacies of USAA car insurance costs, exploring the variables that influence your premium, average price points, and strategies to secure the most favorable rates. Our aim is to provide an insightful, professional perspective on navigating the financial landscape of USAA car insurance, helping you make an informed decision for your personal finance strategy.

Understanding USAA’s Unique Position in the Insurance Market

USAA (United Services Automobile Association) is more than just an insurance company; it’s a financial services group with a distinct mission and a highly loyal membership. This unique structure inherently influences its pricing models and service delivery.

Who is USAA? Eligibility and Membership

Unlike most insurance providers open to the general public, USAA serves a specific demographic: current and former members of the U.S. military and their eligible family members. This includes:

- Active, retired, and honorably discharged officers and enlisted personnel.

- Cadets and midshipmen at U.S. service academies.

- Eligible family members of USAA members, including spouses, widows, widowers, unremarried former spouses who joined USAA while married, and children whose parents have or had a USAA auto or property insurance policy.

This exclusive membership allows USAA to tailor its products and services specifically to the military lifestyle, often leading to a deeper understanding of its members’ needs and risks. This targeted approach can translate into more competitive pricing and specialized benefits not typically found with other insurers.

Why USAA is Often Highly Rated

USAA consistently receives top ratings from organizations like J.D. Power for customer satisfaction in auto insurance, often surpassing its competitors. This reputation isn’t just built on competitive pricing, but also on:

- Exceptional Customer Service: Members frequently praise USAA’s responsive, knowledgeable, and empathetic customer support, especially during claims processing.

- Financial Strength: USAA holds high financial strength ratings, indicating its robust ability to meet its financial obligations, which is crucial for an insurance provider.

- Military-Focused Benefits: Beyond standard insurance, USAA often offers benefits tailored to military life, such as discounts for garaging vehicles on base, coverage during deployments, and assistance with relocation. These specialized offerings enhance its overall value proposition for its niche market.

- Comprehensive Financial Services: USAA is a one-stop shop for many members, offering banking, investments, and various types of insurance, simplifying their financial management.

This strong foundation in service and member focus creates a compelling argument for eligible individuals, often making the question less about “if” USAA is a good choice and more about “how much” it will cost.

Key Factors Influencing USAA Car Insurance Premiums

While USAA’s membership model provides a baseline of value, the actual premium you pay will be determined by a complex interplay of numerous variables. Understanding these factors is crucial for demystifying your insurance quote.

Driver-Specific Variables: Age, Driving Record, Location

Your personal profile is a significant determinant of your insurance risk.

- Age and Experience: Younger, less experienced drivers (especially those under 25) typically face higher premiums due to statistical data indicating a greater likelihood of accidents. Rates tend to decrease as drivers gain experience and age, stabilizing through middle age, and potentially increasing slightly again for very senior drivers.

- Driving Record: This is arguably one of the most impactful factors. A clean driving record, free of accidents, moving violations (speeding tickets, DUIs), or past claims, will almost always result in lower premiums. Conversely, even a single accident or serious violation can significantly elevate your rates for several years.

- Location (Garaging Address): Where you live and primarily garage your vehicle plays a substantial role. Urban areas with higher traffic density, crime rates (theft, vandalism), and accident frequencies often result in higher premiums than rural or suburban areas. Even within the same city, specific zip codes can have vastly different rates.

- Credit Score (where permitted by law): In many states, insurers use a credit-based insurance score as a predictor of future claims. Individuals with higher credit scores often pay less for insurance, as they are statistically less likely to file claims.

- Marital Status: Married individuals often receive slightly lower rates than single drivers, as they are statistically perceived as more responsible.

Vehicle-Specific Variables: Make, Model, Safety Features

The characteristics of the vehicle you drive also heavily influence your premium.

- Make and Model: Luxury vehicles, sports cars, and high-performance vehicles generally cost more to insure due to higher repair costs, greater likelihood of theft, and often more aggressive driving profiles associated with them. More common, mid-range sedans or SUVs tend to be cheaper to insure.

- Year: Newer vehicles often have higher replacement costs, leading to higher comprehensive and collision premiums. However, older vehicles might lack modern safety features, which could also be a factor.

- Safety Features: Vehicles equipped with advanced safety features (e.g., anti-lock brakes, airbags, adaptive cruise control, lane departure warning systems, anti-theft devices) often qualify for discounts, as they reduce the risk of accidents or theft.

- Repair Costs: The cost and availability of parts for your specific vehicle can impact collision and comprehensive premiums. Cars with expensive, specialized parts will generally cost more to insure.

Coverage Choices and Deductibles

The type and amount of coverage you select are direct levers for your premium.

- Types of Coverage:

- Liability: Required in most states, covering damages to others. Higher limits mean higher premiums.

- Collision: Covers damage to your own vehicle from an accident, regardless of fault.

- Comprehensive: Covers non-collision damage (theft, vandalism, natural disasters).

- Uninsured/Underinsured Motorist: Protects you if the at-fault driver has insufficient or no insurance.

- Medical Payments/Personal Injury Protection (PIP): Covers medical expenses for you and your passengers.

- Adding more types of coverage or increasing limits will increase your premium.

- Deductibles: This is the amount you pay out-of-pocket before your insurance kicks in for collision and comprehensive claims. A higher deductible (e.g., $1,000 instead of $500) will result in a lower premium, as you’re taking on more financial risk. Conversely, a lower deductible means a higher premium.

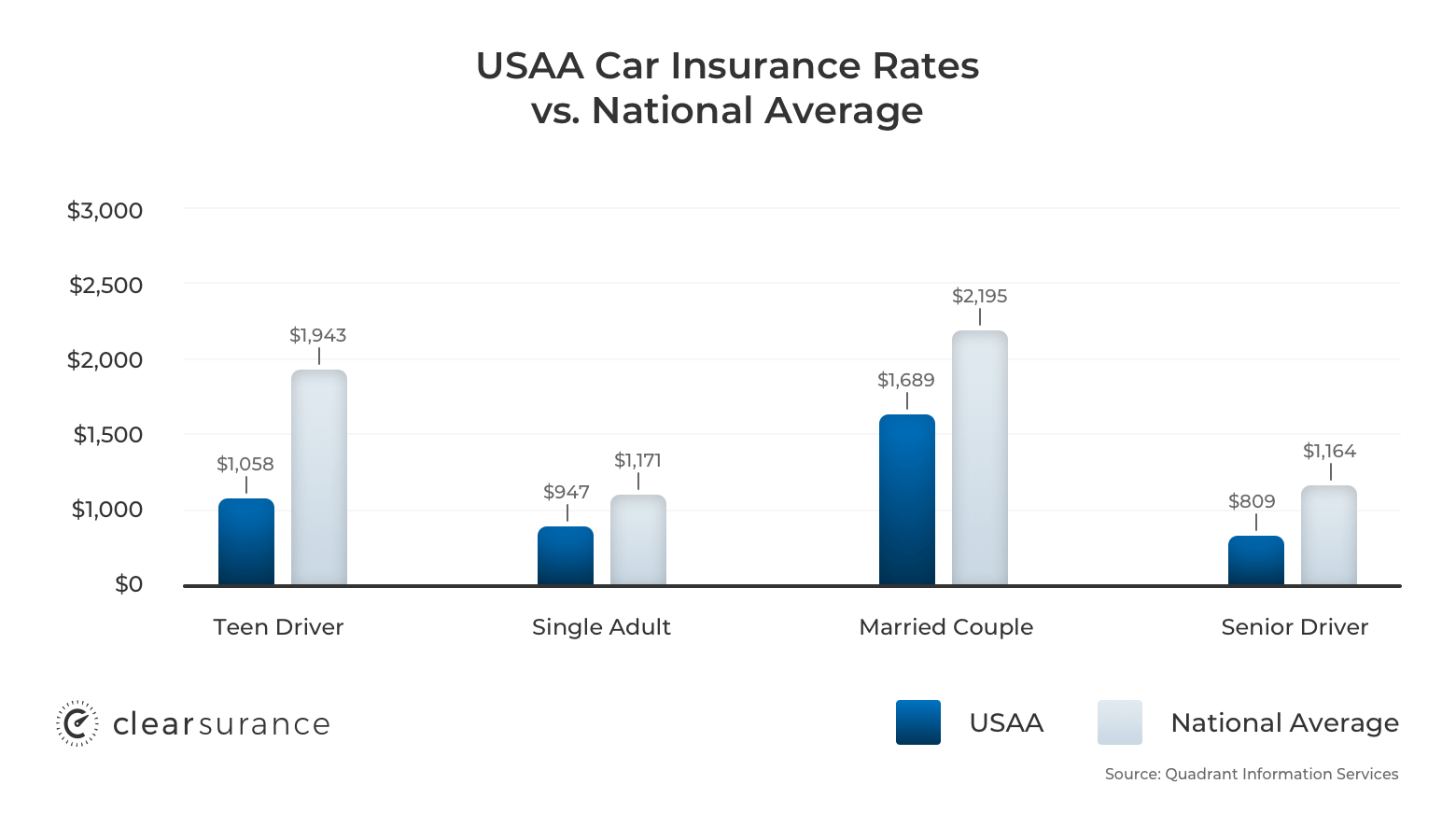

Average Costs of USAA Car Insurance: What to Expect

While providing a single average cost for USAA car insurance is misleading due to the factors above, we can discuss general trends and provide illustrative examples. USAA consistently ranks among the most affordable insurers for eligible individuals, often beating out large competitors.

State-by-State Variations

Insurance premiums are heavily regulated at the state level, and local risk factors vary widely. A driver with an identical profile and vehicle could pay significantly different rates in California versus Ohio or Texas. For instance, states with higher rates of auto theft, more litigious environments, or frequent severe weather events (like hurricanes or hail storms) typically have higher average premiums across all insurers, including USAA. Therefore, while USAA might be cheaper than its competitors in a given state, the absolute dollar amount could still be high if that state generally has elevated insurance costs.

Illustrative Examples Based on Driver Profiles

To give a general idea, consider these hypothetical scenarios (these are illustrative and not actual quotes):

- Young, Single Driver (22, Clean Record, Mid-Range Sedan): Could range from $1,800 – $2,500 annually. Young drivers typically face the highest rates, even with a clean record, due to their inexperience.

- Married, Middle-Aged Driver (40, Clean Record, Family SUV): Might see rates between $1,000 – $1,600 annually. This demographic often enjoys the lowest rates due to perceived stability and experience.

- Senior Driver (65, Clean Record, Sedan): Potentially $1,100 – $1,700 annually. Rates can start to slightly increase again for senior drivers, although a clean record often keeps them competitive.

- Driver with a Recent Accident/Violation: Regardless of age, expect a significant increase, potentially 20-50% or more, depending on the severity of the incident.

It’s important to reiterate that these are broad estimates. Your actual quote will be precise to your circumstances.

The Impact of Discounts on Overall Premiums

One of the most effective ways to manage your USAA car insurance cost is by taking advantage of their extensive discount offerings. These can significantly reduce your overall premium, sometimes by 10-30% or even more when stacked. We’ll delve into specific discounts in the next section. USAA is known for having a wide array of discounts, making it possible for many members to achieve truly competitive rates.

Maximizing Savings on Your USAA Car Insurance Policy

Securing competitive rates with USAA isn’t just about initial eligibility; it’s also about actively utilizing the available tools and discounts to minimize your out-of-pocket expenses. Strategic choices in coverage and participation in specific programs can lead to substantial savings.

Exploring Available Discounts: Multi-Policy, Safe Driver, Good Student, Bundling

USAA offers a robust suite of discounts that can significantly reduce your premium. Proactively identifying and applying for these can lead to substantial savings.

- Multi-Policy/Bundling Discount: This is often one of the largest discounts. If you bundle your car insurance with other USAA policies, such as homeowners, renters, life, or umbrella insurance, you can typically save a significant percentage on all policies.

- Safe Driver Discount: Maintaining a clean driving record for a certain period (e.g., three or five years without accidents or violations) can earn you a discount.

- Good Student Discount: High school or college students who maintain a B average or better can often qualify for a discount, recognizing their responsible behavior extends beyond the classroom.

- Defensive Driving Course Discount: Completing an approved defensive driving course can not only improve your driving skills but also net you a discount, especially if you have points on your license.

- Vehicle Safety Features Discount: Cars equipped with anti-lock brakes, airbags, anti-theft devices, or other advanced safety technology often qualify for reduced rates.

- New Vehicle Discount: Some insurers offer discounts for newer vehicles due to their advanced safety features and lower likelihood of immediate mechanical failure.

- Military-Specific Discounts: While USAA is already for the military, they sometimes offer additional savings related to garaging vehicles on base or during deployments.

- Loyalty Discount: Long-term USAA members may receive loyalty discounts.

It’s crucial to ask your USAA representative about all available discounts and ensure you are taking advantage of every one for which you qualify.

Optimizing Coverage Levels and Deductibles

Your choices regarding coverage types and deductibles have a direct impact on your premium.

- Adjusting Deductibles: Raising your collision and comprehensive deductibles from, say, $500 to $1,000 or even $2,500 can significantly lower your premiums. However, ensure you have the emergency funds available to cover that deductible should you need to file a claim.

- Reviewing Coverage Needs: As your vehicle ages, its market value decreases. At some point, the cost of full collision and comprehensive coverage might outweigh the potential payout if the car is totaled. Consider dropping these coverages for older vehicles if the premium savings are substantial and you can afford to replace the car out-of-pocket. Always maintain sufficient liability coverage, however, to protect your assets.

- Eliminating Redundant Coverage: If you have excellent health insurance, you might not need very high limits for Medical Payments/PIP, though some level is often required or advisable. Review what your other insurance policies already cover.

Leveraging Telematics Programs

USAA offers DriveSense®, a telematics program that monitors your driving habits (e.g., mileage, braking, acceleration, time of day). By enrolling in this voluntary program and driving safely, you can often earn an additional discount. This is an excellent option for responsible drivers looking to further personalize their rates based on actual driving behavior rather than just generalized statistics. The data collected helps USAA assess your individual risk more accurately, potentially rewarding safer drivers with lower premiums.

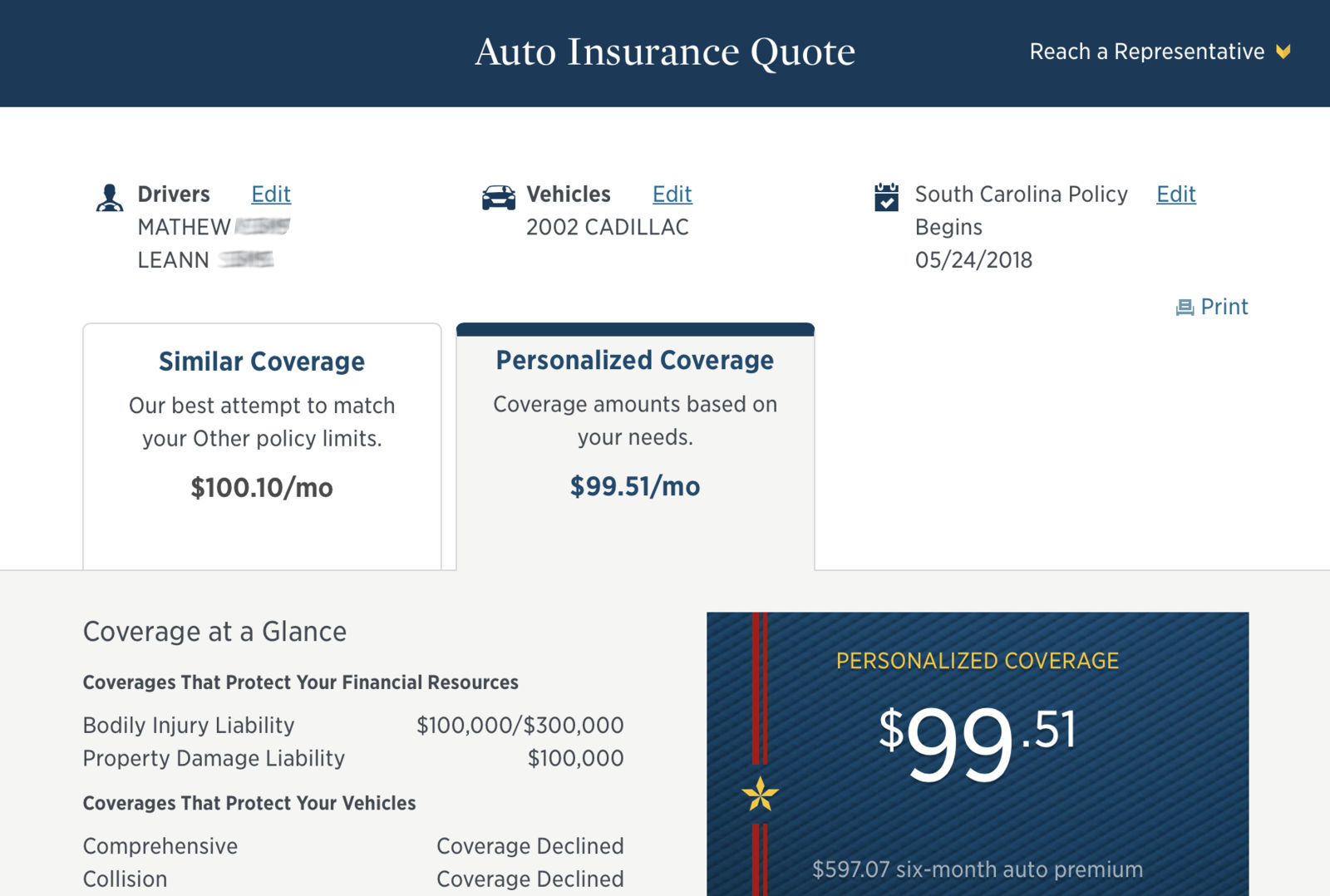

Getting a USAA Car Insurance Quote and Making an Informed Decision

Ultimately, the best way to determine “how much is USAA car insurance” for your specific situation is to get a personalized quote. This process is straightforward and typically quick, providing you with concrete figures tailored to your unique profile.

The Quote Process: What Information You’ll Need

To get an accurate quote from USAA, be prepared to provide the following information:

- Personal Information: Your full name, date of birth, driver’s license number, marital status, and occupation. For all drivers on the policy.

- Eligibility Details: Proof of your military service or relationship to an eligible USAA member.

- Vehicle Information: Make, model, year, VIN (Vehicle Identification Number), and approximate annual mileage for each vehicle you wish to insure.

- Driving History: Details on any accidents, tickets, or claims within the past three to five years for all drivers on the policy.

- Desired Coverage: An idea of the types of coverage and limits you’re looking for, though a USAA representative can help you navigate these choices.

- Existing Policies: If you plan to bundle, have details of your existing homeowners or renters insurance policies ready.

You can typically obtain a quote online through USAA’s website, by phone, or via their mobile app.

Comparing USAA with Other Top Insurers

While USAA is highly regarded and often provides excellent rates, it’s always prudent to compare quotes from other reputable insurers, even if you are eligible for USAA. This ensures you are truly getting the best value for your money.

- Other highly-rated insurers to consider might include: Geico, Progressive, State Farm, Allstate, and local independent agents who can shop multiple carriers for you.

- Consider the “Total Value”: Don’t just look at the premium. Evaluate the insurer’s customer service reputation (especially for claims), financial stability, available discounts, and unique benefits. USAA often shines in these non-price categories, which contribute significantly to overall value.

- Review Quotes Annually: Insurance rates can change, and your personal circumstances evolve. Make it a habit to get new quotes from USAA and other providers at least once a year to ensure you’re always getting the most competitive rates.

Beyond Price: Evaluating Value and Service

While cost is a primary concern, the true value of car insurance extends far beyond the monthly premium. With USAA, members often cite the peace of mind derived from their exceptional claims service, understanding of military life, and robust financial products as a significant part of its appeal. A slightly higher premium might be justified for superior service, especially when faced with the stress of an accident.

For eligible military members and their families, USAA car insurance consistently offers a compelling combination of competitive pricing, outstanding customer service, and tailored benefits. By understanding the factors that influence your premium, proactively seeking out discounts, and regularly reviewing your coverage, you can ensure you’re getting the best possible value from your USAA policy, aligning perfectly with sound personal financial management.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.