To understand the financial magnitude of the company most people simply call “Google,” one must first distinguish between the consumer brand and the corporate entity known as Alphabet Inc. Since its restructuring in 2015, Alphabet has served as the parent holding company, housing Google as its primary subsidiary alongside various “Other Bets.” When investors and financial analysts ask how much the company is worth, they are looking at a multifaceted valuation that includes market capitalization, enterprise value, and the intrinsic value of its data-driven ecosystem.

As of mid-2024, Alphabet Inc. consistently fluctuates within the elite “trillion-dollar club,” often hovering between $1.7 trillion and $2.1 trillion in market capitalization. This valuation makes it one of the most valuable publicly traded companies in history. However, a company’s worth is not merely a static number on a stock ticker; it is a reflection of its current cash flows, its dominant market share in digital advertising, and its projected growth in the burgeoning field of Artificial Intelligence.

Understanding Market Capitalization and Enterprise Value

The most common way to answer “how much is Google worth” is to look at its market capitalization. This figure is calculated by multiplying the current share price by the total number of outstanding shares. Alphabet has two main classes of shares traded publicly: Class A (GOOGL), which carries voting rights, and Class C (GOOG), which does not.

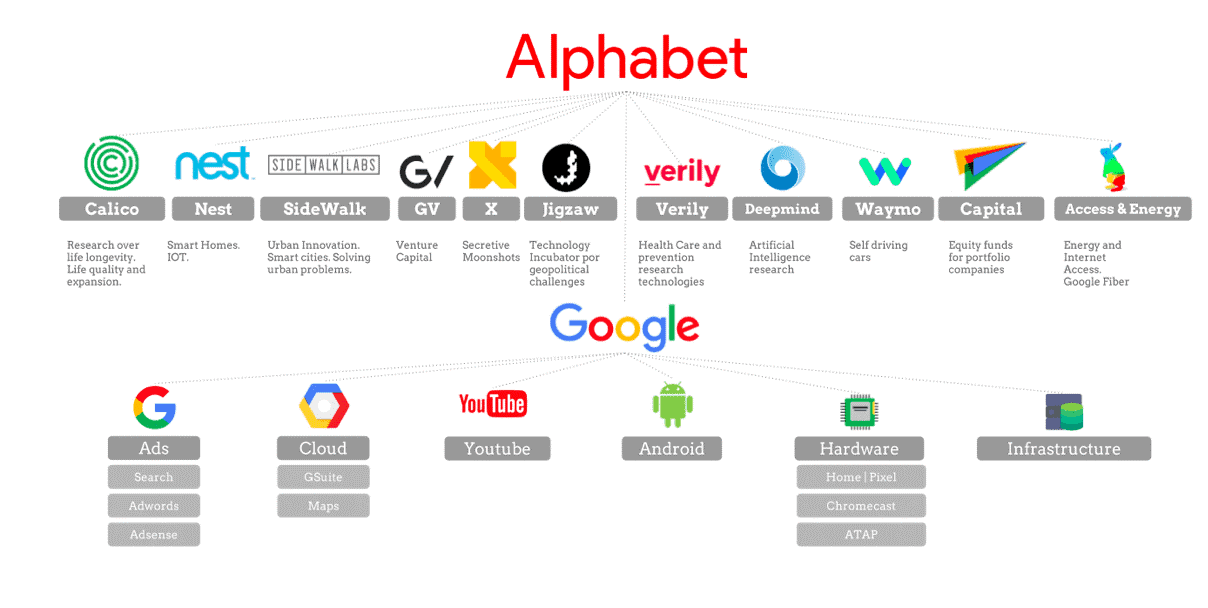

The Distinction Between Alphabet and Google

In the financial world, “worth” is often synonymous with Alphabet Inc. while the “Google” segment represents the core engine. Google encompasses Search, YouTube, Android, Chrome, and Google Cloud. This segment accounts for the vast majority of the parent company’s valuation. When analysts evaluate the company, they often use a “Sum-of-the-Parts” (SOTP) valuation, assigning individual values to YouTube or Search as if they were standalone entities. Many believe that if YouTube were spun off today, it would be a top-tier Fortune 500 company on its own, potentially worth over $400 billion.

Market Cap vs. Intrinsic Worth

While market cap tells us what the public is willing to pay today, intrinsic worth looks at the discounted future cash flows. Alphabet’s balance sheet is famously “cash-rich.” With cash, cash equivalents, and marketable securities often exceeding $100 billion, the company’s enterprise value (EV)—which accounts for debt and cash—reveals a business with unparalleled liquidity. This financial cushion allows the company to weather economic downturns better than almost any other tech peer, adding a layer of “safety value” to its overall worth.

Revenue Streams: The Financial Engines Driving Valuation

A company is worth the sum of the profits it can generate over its lifetime. To understand Google’s trillion-dollar valuation, one must dissect the specific streams of income that convince institutional investors to hold the stock.

Google Search and the Advertising Duopoly

The bedrock of Google’s valuation is its advertising business. Google Search remains the most effective advertising machine ever created. It captures “high-intent” traffic, meaning users are often looking for products or services at the exact moment they search. This dominant market share in global search (consistently above 90%) creates a “moat” that is incredibly difficult for competitors to breach. This segment generates the high-margin cash flow that funds the rest of the company’s ambitious projects.

YouTube and the Shift to Digital Video

YouTube has evolved from a video-sharing site into a global media powerhouse that competes directly with traditional television and streaming services like Netflix. Its revenue model is diversified between advertising and subscription services (YouTube Premium and YouTube TV). From a valuation perspective, YouTube is valued at a high multiple because of its social-media-like engagement levels combined with its utility as a search engine (the second largest in the world).

Google Cloud’s Path to Profitability

For years, Google Cloud was a loss-leading segment designed to compete with Amazon Web Services (AWS) and Microsoft Azure. Recently, however, Google Cloud has reached profitability, significantly boosting the company’s overall valuation. As enterprises migrate to the cloud to run AI workloads, this segment has become a critical pillar of Alphabet’s growth thesis. Investors price the Cloud division based on its high growth rates and the long-term “stickiness” of enterprise contracts.

Fundamental Analysis: Profitability and Balance Sheet Strength

Beyond revenue, a company’s worth is tied to its efficiency. Alphabet is a remarkably profitable enterprise, boasting operating margins that are the envy of the S&P 500.

Net Income and Margin Resilience

Alphabet’s ability to maintain high net income margins (often exceeding 20-25%) despite massive investments in infrastructure and personnel is a testament to its scalable business model. Unlike hardware companies that face significant per-unit costs, Google’s software-based ecosystem allows it to serve an additional billion users with relatively low incremental costs. This scalability translates directly into the high valuation multiples (Price-to-Earnings ratios) that investors are willing to pay.

Strategic Capital Allocation

How a company uses its money also dictates its worth. Alphabet has increasingly used its massive free cash flow for share buybacks. By reducing the total number of shares outstanding, the company increases the “Earnings Per Share” (EPS), which typically drives the stock price higher. Furthermore, the company’s research and development (R&D) spend—often topping $30 billion to $40 billion annually—is an investment in future worth, ensuring that the company remains at the forefront of the next technological shift.

Investment Outlook: Valuation Multiples and the AI Factor

To determine if Google is “undervalued” or “overvalued,” investors look at valuation multiples like the P/E (Price-to-Earnings) and P/S (Price-to-Sales) ratios.

Comparative Valuation with Big Tech Peers

Historically, Alphabet has often traded at a slight discount compared to Microsoft or Apple. This is partly due to its heavy reliance on advertising revenue, which can be cyclical. However, when compared to the broader market, Alphabet frequently appears reasonably priced given its growth profile. Analysts often argue that Google’s “Other Bets” (like Waymo, the autonomous driving unit) are currently valued at near-zero by the market, providing “hidden” upside to the company’s total worth.

The Artificial Intelligence Multiplier

The current frontier for Alphabet’s valuation is Generative AI. With the integration of Gemini (its proprietary AI model) across its product suite, Alphabet is positioning itself to lead the next era of computing. The market’s perception of Google’s AI capabilities heavily influences its stock price. If investors believe Google can defend its search dominance against AI-powered competitors, the company’s valuation is likely to expand. Conversely, any perceived lag in AI innovation can lead to temporary contractions in its market worth.

Financial Risks and Headwinds to Valuation

No valuation analysis is complete without considering the factors that could diminish the company’s worth. For a titan like Alphabet, the primary risks are not financial instability, but rather regulatory and competitive shifts.

Antitrust and Regulatory Challenges

Governments in the United States, Europe, and other regions have increased scrutiny of Google’s business practices. Potential outcomes of antitrust lawsuits—ranging from massive fines to the forced divestiture of parts of the business (like the Chrome browser or the ad-tech stack)—pose a significant risk to its current valuation. A forced breakup would fundamentally change how the market values the “sum of the parts.”

Shifting Paradigms in Digital Advertising

The digital advertising landscape is more competitive than ever. The rise of Amazon’s ad business, the growth of TikTok, and changes in privacy regulations (like Apple’s App Tracking Transparency) create “signal loss” for advertisers. While Google is better positioned than most to handle these shifts due to its first-party data, any significant erosion in ad pricing or demand would directly impact the company’s bottom line and, consequently, its market worth.

Conclusion: The Long-Term Value Proposition

In summary, the “worth” of Google (Alphabet Inc.) is a staggering figure that represents more than just a large number of dollars. It represents a near-monopoly on the world’s information retrieval, a leading position in the future of cloud computing, and a massive bet on the future of Artificial Intelligence.

While the $1.7 to $2 trillion market cap is the standard answer, the company’s true financial value lies in its resilient cash flow and its fortress-like balance sheet. For the personal investor or the institutional fund manager, Alphabet remains a foundational asset, valued not just for what it earned yesterday, but for its role as the primary gatekeeper of the digital age. As long as the world continues to search for information and businesses continue to move to the cloud, Google’s financial valuation is likely to remain among the highest in the corporate world.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.