In the contemporary digital economy, the question “how much is Paramount” carries a dual significance. For the individual consumer, it refers to the monthly line item in a household budget—the cost of accessing a library of cinematic history and live sports. For the institutional investor and the market analyst, it refers to the enterprise value of Paramount Global, a legacy media titan navigating a volatile transition from linear broadcasting to direct-to-consumer (DTC) streaming.

Understanding the “cost” of Paramount requires a deep dive into the microeconomics of personal finance and the macroeconomics of corporate valuation. This article explores the financial architecture of Paramount+, the investment profile of its parent company, and the broader economic implications of the ongoing streaming wars.

The Consumer Perspective: Breaking Down Subscription Costs and Personal Finance Impact

From a personal finance standpoint, Paramount represents a variable cost that must be weighed against its utility. As streaming services continue to hike prices across the board, consumers are becoming increasingly surgical about where they allocate their discretionary income. Paramount+ has positioned itself as a mid-tier service in terms of pricing, attempting to balance affordability with a high-volume content library.

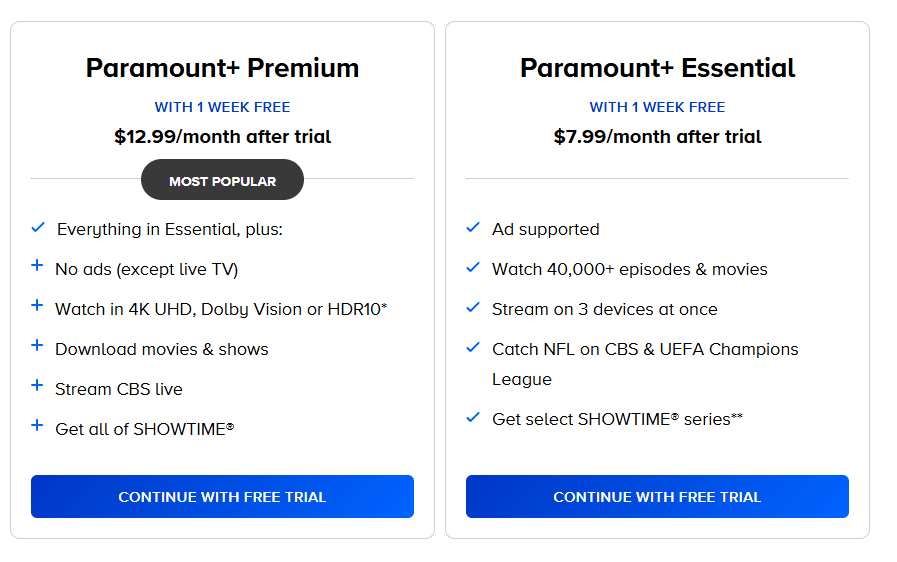

The Tiered Pricing Model: Essential vs. Paramount+ with SHOWTIME

Paramount utilizes a classic “good-better-best” pricing strategy, primarily split into two main tiers. The “Essential” plan, currently priced at $7.99 per month (or approximately $59.99 per year), serves as the entry point. This tier is ad-supported and excludes local live CBS stations, though it does include high-stakes sports like the NFL on CBS and UEFA Champions League.

The premium tier, “Paramount+ with SHOWTIME,” sits at $12.99 per month (or $119.99 per year). This tier is largely ad-free and integrates the entire Showtime library, offering a higher value proposition for fans of premium prestige dramas. From a financial planning perspective, the 15–20% savings found in the annual plans represent a significant “return on investment” for loyal viewers, effectively reducing the monthly cost for those willing to commit capital upfront.

Annual vs. Monthly: Strategic Budgeting for the Modern Streamer

The decision between a monthly and annual commitment is a fundamental exercise in cash flow management. For a household managing a tight monthly budget, the $7.99 “Essential” monthly fee is a low-friction entry point. However, the $59.99 annual fee, while requiring a larger immediate outlay, provides a hedge against potential mid-year price hikes.

In a high-inflation environment, “locking in” a streaming rate is a subtle but effective defensive financial move. Analysts have noted that Paramount, like its competitors Disney+ and Netflix, has shifted its focus from pure subscriber growth to Average Revenue Per User (ARPU). This shift suggests that the “cost” of the service is likely to trend upward, making the annual commitment even more financially sound for long-term users.

Bundling and Hidden Savings: The Walmart+ and Third-Party Synergy

One of the most effective ways to lower the “price” of Paramount is through ecosystem bundling. Currently, the Paramount+ Essential plan is included at no extra cost with a Walmart+ membership ($98/year or $12.95/month). For a consumer who already utilizes Walmart+ for grocery delivery or fuel discounts, the marginal cost of Paramount+ drops to zero.

These B2B2C (Business-to-Business-to-Consumer) arrangements are vital for Paramount’s financial health. They provide the company with a guaranteed “wholesale” revenue stream while offering the consumer a perceived value that far exceeds the out-of-pocket cost. When calculating the “cost” of the service, savvy consumers must look at these cross-platform integrations to optimize their digital spending.

The Investor’s View: Valuation and the Financial Health of Paramount Global

Moving from the living room to the boardroom, the question “how much is Paramount” shifts to market capitalization and enterprise value. Paramount Global (NASDAQ: PARA) has been the subject of intense financial scrutiny as it navigates a declining linear television business while scaling its capital-intensive streaming wing.

Analyzing PARA Stock: Market Cap and Fiscal Performance

As of mid-2024, the market valuation of Paramount Global has seen significant volatility. With a market cap hovering between $8 billion and $12 billion—down from much higher peaks in previous years—the company is often viewed through the lens of a “value play” or a potential “value trap.”

Investors look at the Price-to-Earnings (P/E) ratio and the Debt-to-Equity ratio to determine if the company is undervalued. Paramount carries a substantial debt load, a legacy of its aggressive content spending and the consolidation of Viacom and CBS. The financial “worth” of the company is intrinsically tied to its ability to service this debt while achieving profitability in its Direct-to-Consumer segment, which has historically operated at a loss during its growth phase.

The M&A Landscape: What is the Company Actually Worth?

The true financial value of Paramount is perhaps best reflected in the various merger and acquisition (M&A) bids it has attracted. In 2024, the company became the center of a bidding war involving Skydance Media, Sony Pictures, and Apollo Global Management.

These entities aren’t just looking at current stock price; they are looking at the “sum-of-the-parts” valuation. Paramount owns a massive film library (including franchises like Mission: Impossible and Top Gun), the CBS broadcast network, and lucrative cable properties like Nickelodeon and MTV. Analysts estimate the intrinsic value of these assets to be significantly higher than the current market cap, suggesting that “how much Paramount is worth” depends entirely on whether it is viewed as a standalone entity or a collection of exploitable intellectual property.

Revenue Streams: Direct-to-Consumer (DTC) vs. Traditional Linear TV

A critical metric for investors is the transition of revenue from linear to digital. Traditional TV advertising and carriage fees still account for a large portion of Paramount’s cash flow, but that “well” is drying up as cord-cutting accelerates. The financial health of the company depends on the DTC segment reaching a “break-even” point. In recent fiscal quarters, Paramount has shown narrowing losses in streaming, a positive sign for the stock’s long-term valuation. The “cost” of maintaining this growth is high, but the potential “reward” is a sustainable, recurring revenue model that mimics the software-as-a-service (SaaS) industry.

The Macroeconomics of the Streaming Wars: Content Spending and ROI

The broader financial context of Paramount is defined by the “Streaming Wars”—a high-stakes economic battle where content is the primary capital expenditure.

The High Cost of Original Content Production

“How much is Paramount” is also a question of how much it spends. Producing prestige content is staggeringly expensive. A single season of a high-end series can cost upwards of $100 million. This capital expenditure is a gamble on subscriber retention.

For Paramount, the financial strategy has been to leverage its existing IP (like the Yellowstone universe or Star Trek) to minimize the risk of new content failure. By spending efficiently on “proven” franchises, Paramount seeks a higher Return on Investment (ROI) than competitors who may be spending more on unproven, original concepts.

Churn Rate and the Lifetime Value (LTV) of a Subscriber

In the subscription economy, the most important financial metric is the Lifetime Value (LTV) of a customer relative to the Customer Acquisition Cost (CAC). If it costs Paramount $50 in marketing to acquire a subscriber who stays for three months (paying $24), the company loses money.

To improve these margins, Paramount focuses on “sticky” content—programming that prevents “churn” (subscribers canceling). Live sports, particularly the NFL, are the ultimate churn-reduction tool. While the broadcast rights cost billions, the financial utility of keeping millions of subscribers paying year-round makes the “cost” of those rights a necessary investment in the company’s financial stability.

Comparative Value: Paramount+ vs. The Competitive Landscape

To truly understand “how much” Paramount costs, one must look at it relative to the rest of the market. Economics is the study of trade-offs, and choosing Paramount+ often means forgoing another service.

Price-per-Hour Metrics: Assessing Utility for the Consumer

When analysts look at the “value” of a streaming service, they often use a price-per-hour-of-viewing metric. Because Paramount+ includes a deep back-catalog of thousands of episodes from procedural hits (like CSI and NCIS), its “cost per hour” of available content is remarkably low compared to niche services like Crunchyroll or even premium services like Netflix, which may have higher turnover in their library. For a budget-conscious consumer, the sheer volume of “background” television provided by Paramount offers a high level of utility for a relatively low monthly price.

Inflation and the Future of Streaming Price Hikes

The macro-trend in the streaming industry is toward consolidation and price increases. As the era of “cheap money” and subsidized growth ends, Paramount—and its peers—must move toward profitability. This suggests that the answer to “how much is Paramount” will likely be a higher number in 2025 and 2026.

From a financial planning perspective, consumers should expect “bracket creep” in their digital subscriptions. For Paramount, the challenge will be to raise prices without triggering a mass exodus of subscribers to competitors like Disney+ or Max. The company’s ability to manage this delicate pricing elasticity will determine its financial fate in the coming decade.

In conclusion, “how much is Paramount” is a multifaceted question. To the viewer, it is a $7.99 to $12.99 monthly investment in entertainment. To the investor, it is an $11 billion legacy giant at a crossroads, representing either a bargain-priced asset or a risky bet on the future of media. In both cases, the value of Paramount is defined by its ability to convert iconic content into sustainable financial growth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.