Determining the cost of health insurance under the Affordable Care Act (ACA)—commonly referred to as Obamacare—is a critical component of personal financial planning for millions of Americans. Unlike a fixed-price product, the cost of an ACA plan is a dynamic figure influenced by a myriad of variables ranging from personal demographics to federal legislative changes. For the self-employed, early retirees, and those without employer-sponsored coverage, understanding these costs is not just about health; it is about protecting assets and managing monthly cash flow.

To answer “how much is Obamacare,” one must look beyond the sticker price and analyze the interplay between premiums, subsidies, and out-of-pocket maximums. This guide explores the financial mechanics of the Marketplace to help you project your healthcare expenditures accurately.

Understanding the Core Drivers of Marketplace Costs

The price of an Obamacare plan is not arbitrary. Federal law restricts insurance companies to a specific set of criteria when determining your premium. By understanding these drivers, individuals can better predict their monthly financial obligations.

Age and Geographic Location

Age is one of the most significant factors in premium pricing. Under the ACA, insurers can charge older individuals up to three times more than younger individuals for the same plan. From a financial planning perspective, this means healthcare costs should be projected to increase as one approaches Medicare eligibility.

Geographic location also plays a pivotal role. Costs vary by state and even by county due to differences in local competition among insurers, the cost of living, and the density of healthcare providers. For instance, a resident in a rural area with only one participating insurer may face significantly higher premiums than someone in a major metropolitan area with dozens of competing carriers.

Plan Metal Tiers: Bronze, Silver, Gold, and Platinum

The Marketplace categorizes plans into “Metal Tiers” to indicate how you and the insurance company share costs. This is a crucial distinction for your personal budget:

- Bronze Plans: These have the lowest monthly premiums but the highest out-of-pocket costs when you receive care. They are often the best choice for those who want a low monthly overhead and only need “catastrophic” protection.

- Silver Plans: These represent the “benchmark” for subsidies. They offer moderate premiums and moderate out-of-pocket costs.

- Gold and Platinum Plans: These carry high monthly premiums but significantly lower deductibles and copays. These are strategic for individuals with known chronic conditions who prefer a predictable, albeit higher, monthly expense.

Household Size and Smoking Status

Insurers are permitted to charge tobacco users up to 50% more than non-smokers, although many states choose to limit or prohibit this “tobacco surcharge.” Furthermore, the total cost of an Obamacare policy is calculated based on the number of people in the household needing coverage. Financially, adding a spouse or dependents scales the cost, though the availability of tax credits often scales alongside these additions.

The Role of Subsidies in Reducing Monthly Premiums

The “sticker price” of Obamacare is rarely what the consumer actually pays. The financial genius of the ACA lies in its subsidy structure, which acts as a sliding scale based on income.

Premium Tax Credits Explained

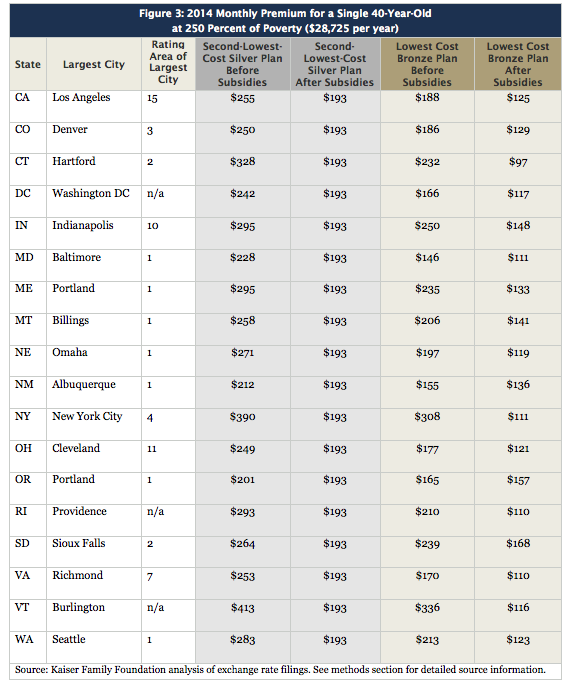

The Advanced Premium Tax Credit (APTC) is the primary tool used to lower monthly insurance costs. This credit is based on your estimated annual household income compared to the Federal Poverty Level (FPL). Historically, these credits were only available to those earning between 100% and 400% of the FPL. However, recent legislative shifts, such as the Inflation Reduction Act, have expanded these subsidies, ensuring that no enrollee pays more than 8.5% of their household income for a benchmark Silver plan. This makes the “cost” of Obamacare highly personal; a person earning $30,000 a year might pay $0 in premiums, while someone earning $100,000 pays the full market rate.

Cost-Sharing Reductions (CSRs)

Beyond premium assistance, Silver-level plans offer an additional financial benefit known as Cost-Sharing Reductions. If your income falls within a certain range (typically below 250% of the FPL), you qualify for a version of a Silver plan that has a lower deductible, lower copayments, and a lower out-of-pocket maximum. In financial terms, this essentially upgrades a Silver plan to the level of a Gold or Platinum plan for a fraction of the cost. When calculating the total value of an Obamacare plan, the CSR is often more valuable than the premium subsidy itself.

The Impact of the Inflation Reduction Act

The extension of enhanced subsidies through 2025 has dramatically shifted the “affordability” window. By removing the “subsidy cliff”—the point where earning one dollar over the 400% FPL limit resulted in the total loss of financial aid—the government has made Obamacare a viable financial option for middle-to-high-income earners. For those managing a business or side hustle, this means more capital can remain in the business rather than being diverted to high-cost private health insurance.

Out-of-Pocket Expenses: Beyond the Monthly Premium

When evaluating “how much is Obamacare,” focusing solely on the monthly premium is a common financial pitfall. The “Total Cost of Ownership” for a health plan includes what you pay when you actually use medical services.

Deductibles and Their Impact on Cash Flow

The deductible is the amount you must pay out-of-pocket for covered services before your insurance begins to pay. In the Marketplace, Bronze plan deductibles can exceed $7,000 for an individual. For a family living paycheck to paycheck, a high-deductible plan creates a significant financial risk. From a money management perspective, if you choose a low-premium, high-deductible plan, you must ensure you have an emergency fund or a dedicated savings account to cover that deductible should a medical emergency arise.

Copayments vs. Coinsurance

Once the deductible is met, you still share costs with the insurer via copayments (fixed dollar amounts, e.g., $30 for a doctor visit) or coinsurance (a percentage of the total bill, e.g., 20% of a hospital stay). Understanding the difference is vital for budgeting. Copayments offer predictability, while coinsurance can lead to large, unexpected bills for expensive procedures.

Maximum Out-of-Pocket Limits

The ACA provides a critical financial safety net by capping the total amount an individual or family can spend on covered services in a year. For 2024 and 2025, these limits are strictly regulated. Once you hit this “ceiling,” the insurance company pays 100% of covered benefits. This cap is the most important figure for long-term financial protection; it prevents a single catastrophic illness from leading to medical bankruptcy, which was a leading cause of financial ruin prior to the ACA.

Strategic Financial Planning for Health Coverage

Selecting an Obamacare plan is a sophisticated financial decision that requires balancing monthly cash flow against long-term risk.

Comparing Marketplace Plans vs. Employer-Sponsored Insurance

For those with access to a job-based plan, the “cost” of Obamacare is often higher because employers typically subsidize 70-80% of a premium. However, if the employer’s plan for a family is deemed “unaffordable” (exceeding a certain percentage of household income), the employee may become eligible for Marketplace subsidies. This is known as the “family glitch” fix, and it allows families to compare the net cost of a work-based plan against a subsidized Marketplace plan to find the most cost-effective route.

Utilizing Health Savings Accounts (HSAs) with Marketplace Plans

Many Bronze and Silver plans on the Marketplace are “HSA-eligible.” An HSA is one of the most powerful financial tools available. Contributions are tax-deductible, growth is tax-free, and withdrawals for medical expenses are tax-free. If you are in a higher tax bracket but qualify for some Marketplace coverage, choosing an HSA-compatible plan allows you to lower your taxable income, potentially increasing your eligibility for subsidies while simultaneously building a “health IRA.”

Factoring in Tax Implications

Because Obamacare subsidies are based on estimated income for the coming year, there is a year-end reconciliation process on your tax return (Form 8962). If you earn more than you predicted—perhaps through a successful side hustle or a year-end bonus—you may have to pay back a portion of the subsidies you received. Conversely, if you earned less, you may receive a larger tax refund. Accurate income forecasting is therefore a prerequisite for managing the true cost of Obamacare.

In conclusion, the cost of Obamacare is a multi-dimensional calculation. It ranges from $0 for those qualifying for maximum subsidies to over $1,000 a month for high-income individuals in expensive regions. By analyzing the metal tiers, maximizing available tax credits, and planning for out-of-pocket maximums, consumers can transform a complex healthcare requirement into a structured and manageable part of their broader financial strategy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.