Car insurance is a non-negotiable expense for drivers in New York, a legal requirement designed to protect you, other motorists, and pedestrians from the financial fallout of accidents. However, the question “how much is car insurance in NY?” is far from straightforward. Unlike a fixed price tag, auto insurance premiums are highly individualized, influenced by a complex web of factors unique to each driver, vehicle, and policy choice. For New Yorkers, understanding these variables is crucial not only for compliance with state laws but also for effective financial planning and ensuring adequate protection without overspending.

New York’s car insurance landscape is distinct, notably characterized by its “no-fault” insurance system. This system mandates that your own insurance company pays for your medical expenses and lost wages up to a certain limit, regardless of who caused the accident. This unique aspect, combined with the state’s dense population centers, varied driving conditions, and specific regulatory environment, contributes to the overall cost structure. This comprehensive guide will dissect the components that determine your car insurance rates in the Empire State, exploring the mandatory minimums, common coverage options, and actionable strategies to secure the most competitive rates for your specific needs. By understanding the intricacies of the New York car insurance market, drivers can make informed decisions that safeguard their finances and ensure peace of mind on the road.

Understanding Car Insurance in New York

Navigating the intricacies of car insurance in New York begins with a fundamental grasp of its legal framework and the primary components of a standard policy. The state’s unique no-fault system significantly shapes how claims are processed and, consequently, how policies are structured and priced.

The Legal Mandate: Why Insurance is Required

In New York, driving without adequate car insurance is illegal and carries severe penalties, including fines, license suspension, and potential vehicle impoundment. The primary purpose of this mandate is to ensure that all drivers have a financial safety net to cover damages and injuries resulting from accidents. This protects not only the at-fault driver from crippling personal liability but also safeguards innocent parties from bearing the full financial burden of someone else’s mistake. The legal requirement underscores car insurance not just as a financial product but as a civic responsibility within the state’s transportation ecosystem.

Key Components of NY Auto Insurance Policies

A typical car insurance policy in New York is a bundle of different types of coverage, each addressing a specific financial risk. Understanding these components is the first step to tailoring a policy that meets both legal requirements and personal financial comfort.

- Liability Coverage (Bodily Injury & Property Damage): This is the bedrock of any policy, legally mandated to protect you if you’re at fault in an accident causing injury to others or damage to their property. New York requires minimums of $25,000 per person for bodily injury, $50,000 per accident for bodily injury, and $10,000 for property damage. These limits are often written as 25/50/10. It’s important to note that while these are minimums, many financial advisors recommend significantly higher limits to adequately protect your assets in the event of a serious accident.

- Personal Injury Protection (PIP) / No-Fault Coverage: This is where New York’s no-fault system comes into play. PIP coverage pays for medical expenses and lost wages for you and your passengers, regardless of who caused the accident, up to a specified limit (the state minimum is $50,000). This aims to streamline accident claims, reduce litigation, and ensure prompt access to medical care.

- Uninsured/Underinsured Motorist (UM/UIM) Coverage: Despite strict laws, some drivers unfortunately operate without insurance or with insufficient coverage. UM/UIM protects you by covering your medical expenses and, in some cases, property damage if you’re hit by a driver who lacks adequate insurance. New York mandates minimums of $25,000 per person/$50,000 per accident for UM bodily injury.

The Role of No-Fault Insurance in NY

New York is one of a handful of “no-fault” states, meaning that after an accident, your own insurance company generally pays for your medical bills and lost wages through your PIP coverage, regardless of who was at fault. This system is designed to expedite the payment of accident-related expenses and reduce the number of minor injury lawsuits. However, there are thresholds – typically involving “serious injury” as defined by state law – that allow an injured party to step outside the no-fault system and sue the at-fault driver for pain and suffering and other non-economic damages. Understanding this system is crucial because it directly influences the structure of required coverage and the typical claims process in New York. While it offers a streamlined approach for initial medical costs, it also necessitates careful consideration of your PIP limits to ensure comprehensive financial protection.

Factors Influencing Car Insurance Costs in NY

The actual cost of car insurance in New York is an intricate calculation, customized by insurers based on a multitude of variables. These factors are assessed to predict your likelihood of filing a claim and the potential cost of that claim.

Driver-Specific Data: Age, Experience, and Driving Record

Your personal profile as a driver is a dominant factor. Younger, less experienced drivers (especially teenagers and those under 25) often face the highest premiums due to statistical data indicating a higher risk of accidents. Conversely, mature drivers with decades of clean driving history typically enjoy lower rates. Your driving record is paramount: tickets for speeding, reckless driving, or DUIs will significantly elevate your premiums, often for several years. Accidents, even minor ones, can also lead to rate increases, particularly if you were deemed at fault.

Vehicle Characteristics: Make, Model, and Safety Features

The car you drive plays a major role in your premium calculation. Insurers consider:

- Vehicle Value: More expensive cars cost more to repair or replace, leading to higher comprehensive and collision premiums.

- Safety Ratings: Cars with high safety ratings (e.g., strong crash test results) may qualify for discounts because they are less likely to result in severe injuries to occupants.

- Theft Rates: Models frequently targeted by thieves often incur higher comprehensive coverage costs.

- Engine Size/Performance: High-performance vehicles, statistically associated with more aggressive driving, can result in higher rates.

- Safety Features: Advanced driver-assistance systems (ADAS) like automatic emergency braking, lane-keeping assist, and blind-spot monitoring can sometimes qualify for discounts, as they reduce the likelihood or severity of accidents.

Geographic Location: Urban vs. Rural Rates

Where you live and park your car within New York state has a substantial impact on your premiums. Cities like New York City, Buffalo, and Rochester, with their higher traffic density, increased risk of accidents, theft, and vandalism, typically have significantly higher rates than more rural or suburban areas. Even within a city, specific zip codes can have varying rates based on local crime statistics, accident frequency, and population density.

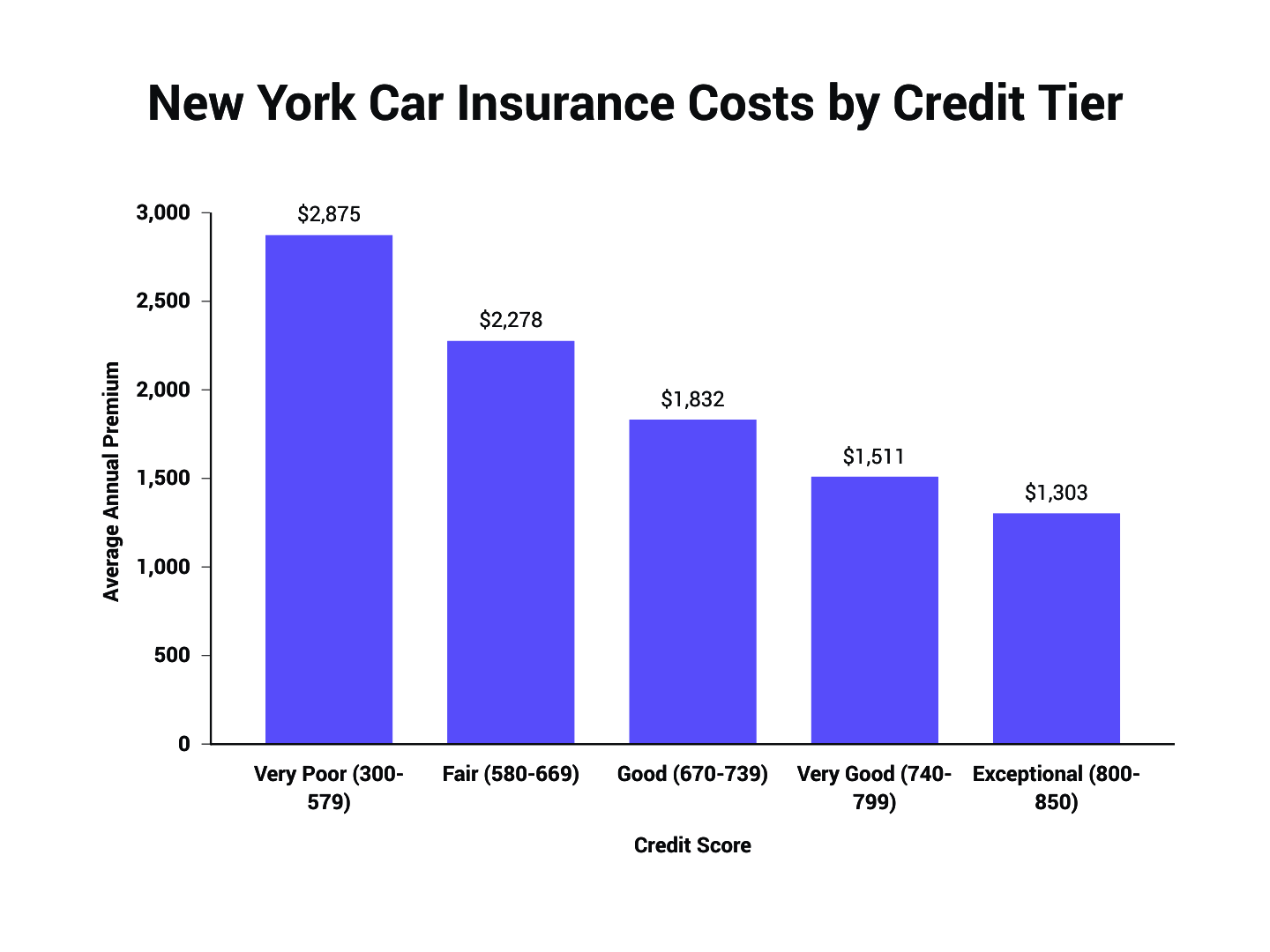

Credit Score and Insurance History

In most states, including New York, your credit-based insurance score (a separate score used by insurers, distinct from your regular credit score) can influence your premiums. Insurers have found a correlation between higher credit scores and a lower likelihood of filing claims. A poor credit history might signal higher risk, leading to elevated rates. Similarly, your insurance history – whether you’ve maintained continuous coverage, had lapses, or filed numerous claims in the past – directly affects your future premiums. Insurers prefer drivers with a consistent history of coverage and fewer claims.

Coverage Limits and Deductibles

The level of coverage you choose directly affects your cost. Opting for higher liability limits (e.g., 100/300/50 instead of 25/50/10) provides greater financial protection but also results in higher premiums. Similarly, your deductible – the amount you pay out of pocket before your collision or comprehensive coverage kicks in – influences your premium. A higher deductible means you take on more financial risk in the event of a claim, which translates to a lower premium, and vice-versa. Finding the right balance between affordable premiums and manageable deductibles is a critical financial decision.

Mandatory Minimum Coverage vs. Comprehensive Protection

Understanding the difference between the bare minimum required by New York law and more extensive coverage options is crucial for making an informed financial decision about your auto insurance. While opting for minimum coverage might seem like a way to save money upfront, it often leaves drivers vulnerable to significant financial risk in the event of a serious accident.

New York’s Minimum Coverage Requirements

As previously mentioned, New York state mandates specific minimum coverages for all registered vehicles:

- Bodily Injury Liability: $25,000 per person / $50,000 per accident

- Property Damage Liability: $10,000 per accident

- Personal Injury Protection (PIP) / No-Fault: $50,000 per person

- Uninsured Motorist Bodily Injury: $25,000 per person / $50,000 per accident

These minimums are designed to provide a basic safety net, but they are often insufficient to cover the full costs associated with serious accidents, especially given the high cost of medical care and vehicle repairs in New York. If you are at fault in an accident and the damages exceed your liability limits, you could be personally responsible for the remaining balance, potentially leading to financial ruin.

Beyond the Basics: Collision and Comprehensive Coverage

For true financial peace of mind, most drivers opt for coverage that goes beyond the state minimums.

- Collision Coverage: This pays for damages to your own vehicle if you hit another car, an object, or if your car rolls over, regardless of who is at fault. It’s especially vital if you have a car loan or lease, as lenders typically require it. The cost of collision coverage is influenced by your car’s value, repair costs, and your chosen deductible.

- Comprehensive Coverage: This covers non-collision incidents, such as theft, vandalism, fire, natural disasters (hail, floods), and damage from striking an animal. Like collision, it’s often required by lenders. Comprehensive coverage is crucial in urban areas with higher risks of theft or vandalism, or areas prone to severe weather.

These two coverages, often purchased together, are essential for protecting your investment in your vehicle and minimizing out-of-pocket expenses for repairs or replacement. Without them, even a minor accident where you are at fault, or an unforeseen event like hail damage, could result in substantial financial strain.

Optional Add-ons: Rental Reimbursement, Roadside Assistance, etc.

Beyond the core coverages, insurers offer a variety of endorsements or “add-ons” that can enhance your protection and convenience, albeit at an additional cost:

- Rental Reimbursement: Covers the cost of a rental car while your vehicle is being repaired after a covered claim.

- Roadside Assistance: Provides help with flat tires, dead batteries, lockouts, or towing services.

- Gap Insurance: Crucial for new cars, this pays the difference between your car’s actual cash value and the amount you still owe on your loan or lease if your car is totaled or stolen. Without it, you could be stuck paying for a car you no longer have.

- Medical Payments (MedPay): Covers medical expenses for you and your passengers after an accident, regardless of fault, and can supplement PIP coverage.

- New Car Replacement: If your new car is totaled, this coverage pays for a brand-new car of the same make and model, rather than just its depreciated actual cash value.

While these add-ons increase your premium, they can offer significant financial and logistical benefits, turning a stressful situation into a manageable one. The decision to include them should be based on your personal risk tolerance, financial situation, and how much convenience you value.

The Balance Between Cost and Protection

Ultimately, choosing your car insurance coverage in New York involves striking a balance between minimizing premiums and maximizing financial protection. Opting for the absolute minimum might save you money in the short term, but it exposes you to substantial financial risk if you’re involved in a severe accident. Conversely, over-insuring beyond your needs can lead to unnecessary expenses. A thoughtful assessment of your assets, driving habits, vehicle value, and risk tolerance is essential to determine the sweet spot where you are adequately protected without overspending. This strategic financial decision ensures that your car insurance truly serves its purpose: to provide security and peace of mind on New York’s roads.

Strategies to Lower Your Car Insurance Premiums in NY

While many factors influencing car insurance rates are beyond your immediate control, numerous strategies can help New York drivers significantly reduce their premiums without compromising essential coverage. Proactive financial management and informed decision-making are key.

Discounts: Bundling, Good Driver, Multi-Car, and More

Insurance companies offer a wide array of discounts, and leveraging them is one of the most effective ways to cut costs.

- Bundling Discount: One of the most significant savings comes from purchasing multiple insurance policies (e.g., auto and home/renters insurance) from the same provider.

- Good Driver/Accident-Free Discount: Maintaining a clean driving record for a specified period (e.g., 3-5 years) often qualifies you for a discount.

- Multi-Car Discount: Insuring more than one vehicle on the same policy can lead to savings per vehicle.

- Anti-Theft Device Discount: Cars equipped with alarms, GPS tracking, or other anti-theft systems may receive a discount.

- Good Student Discount: High school or college students who maintain a certain GPA can often qualify for reduced rates.

- Defensive Driving Course Discount: Completing an approved defensive driving course can not only refresh your skills but also lead to a discount and potentially points reduction on your license. In NY, the IPIRP (Internet Point and Insurance Reduction Program) offers a 10% reduction on liability and collision premiums for three years.

- Loyalty Discount: Some insurers reward long-term customers.

Always ask your agent about every discount you might be eligible for; you might be surprised by how many apply to you.

Improving Your Driving Record

A clean driving record is arguably the most powerful tool for securing lower insurance rates. Avoid speeding tickets, moving violations, and at-fault accidents. Each infraction can lead to higher premiums for several years. For minor infractions, completing a defensive driving course can sometimes help reduce points on your license, which indirectly helps with insurance rates, or directly provides a discount. Consistently demonstrating responsible driving behavior signals lower risk to insurers, leading to more favorable rates over time.

Adjusting Deductibles and Coverage Limits

Strategic adjustments to your policy’s financial parameters can also lead to significant savings.

- Increase Your Deductibles: Choosing a higher deductible (e.g., $1,000 instead of $500) for collision and comprehensive coverage means you’ll pay more out-of-pocket if you file a claim, but your monthly or annual premium will decrease. This is a good strategy if you have a robust emergency fund to cover the higher deductible.

- Re-evaluate Coverage Limits: While it’s advisable to have higher liability limits than the state minimums, periodically review your overall financial situation. If your assets have decreased, or if you’re driving an older, less valuable car, you might consider slightly lowering certain coverage limits (e.g., if your car is worth less than the annual comprehensive/collision premium, it might be financially prudent to drop those coverages altogether). However, always be mindful of the financial risks involved with lower liability limits.

Choosing the Right Vehicle

The type of car you drive heavily influences your insurance premiums. When purchasing a new or used vehicle, consider its insurance costs.

- Safety and Reliability: Cars with excellent safety ratings and a reputation for reliability often have lower premiums.

- Theft Rates: Certain makes and models are more frequently stolen, leading to higher comprehensive coverage costs.

- Repair Costs: Vehicles with expensive parts or complex repair procedures will generally cost more to insure.

- Performance: High-performance sports cars typically come with higher insurance rates due to their higher risk profile.

Research insurance costs for specific models before making a purchase decision; this could lead to substantial long-term savings.

Utilizing Telematics Programs

Many insurance companies now offer telematics programs (sometimes called “usage-based insurance” or “pay-as-you-drive”). These programs use a small device plugged into your car’s diagnostic port or a smartphone app to track your driving habits, such as mileage, speed, braking, acceleration, and time of day you drive. Safe drivers who opt into these programs can often qualify for significant discounts based on their actual driving behavior, rather than broad statistical averages. This can be an excellent way for responsible drivers to prove their low-risk status and secure lower rates.

By actively pursuing these strategies, New York drivers can take control of their car insurance costs, ensuring they receive the necessary financial protection without overpaying. A proactive approach to managing your policy and driving habits is essential for long-term savings.

Navigating the Car Insurance Market in New York

Successfully securing the best car insurance rates in New York involves more than just understanding the components and factors; it requires a strategic approach to shopping for and managing your policy. The market is competitive, and leveraging that competition is key to financial prudence.

The Importance of Shopping Around and Comparing Quotes

This is perhaps the single most important action any New York driver can take to find affordable car insurance. Rates for the exact same coverage can vary wildly between different insurance providers, sometimes by hundreds or even thousands of dollars annually. Each insurer uses its own proprietary algorithms to assess risk, so what one company deems a high risk, another might view more favorably.

- Get Multiple Quotes: Don’t settle for the first quote you receive. Obtain quotes from at least 3-5 different insurers, including national carriers (e.g., State Farm, GEICO, Progressive, Allstate) and regional ones (e.g., Travelers, The General).

- Use Comparison Tools: Online comparison websites can be a quick way to get multiple quotes, but always double-check the details directly with the insurers.

- Work with an Independent Agent: Independent insurance agents work with multiple companies and can shop around on your behalf, often finding deals you might miss. They can also provide personalized advice based on your unique situation.

- Compare Apples to Apples: Ensure that when you compare quotes, you are comparing identical coverage limits, deductibles, and optional add-ons. Even slight differences can make a quote appear cheaper than it actually is.

Shopping around should be an annual habit, not just when your policy is up for renewal, but also after major life events like buying a new car, moving, or adding a new driver.

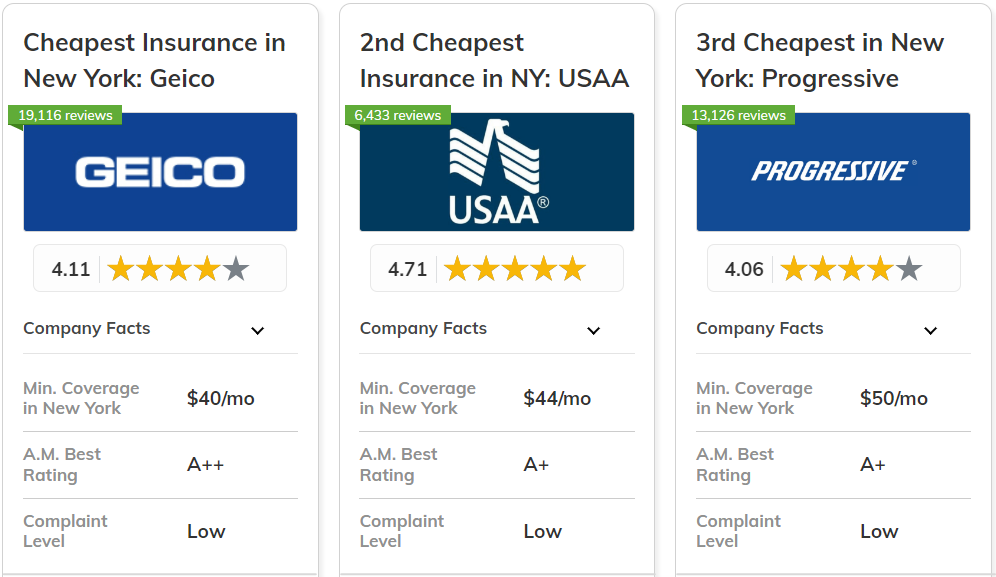

Reputable Insurers Operating in NY

New York is home to a robust insurance market with many reputable carriers. While specific recommendations depend on individual needs, some of the consistently top-rated and widely available insurers in the state include:

- GEICO: Known for competitive online rates and extensive discounts.

- State Farm: Often praised for its strong agent network and customer service.

- Progressive: Offers a wide range of coverage options and telematics programs.

- Allstate: Provides personalized service and various discount programs.

- Travelers: Often a good choice for bundling home and auto policies.

- Liberty Mutual: Known for customized coverage and a variety of discounts.

- Erie Insurance: Often highly rated for customer satisfaction and competitive pricing in areas they serve.

Researching customer reviews, financial stability ratings (from agencies like A.M. Best), and JD Power customer satisfaction scores can help you narrow down your choices and select a company that aligns with your priorities, whether that’s price, service, or claims handling.

Understanding Your Policy Documents

Once you’ve chosen an insurer and purchased a policy, take the time to thoroughly read and understand your policy documents. This includes your declarations page, which summarizes your coverage types, limits, deductibles, and premiums, as well as the full policy booklet.

- Verify Coverage: Ensure all the coverages and limits you discussed and intended to purchase are accurately reflected.

- Know Exclusions: Understand what your policy does not cover.

- Claims Process: Familiarize yourself with the claims process, including contact numbers and necessary steps after an accident.

- Renewal Information: Understand how your policy will renew and any implications for your rates.

A clear understanding of your policy empowers you to make informed decisions and avoids surprises in the event of a claim. Don’t hesitate to ask your agent or insurer’s customer service any questions you have.

When to Re-evaluate Your Coverage

Car insurance is not a “set it and forget it” expense. Your needs and the market conditions change, so it’s financially prudent to regularly re-evaluate your coverage.

- Annually at Renewal: This is the easiest time to review your policy.

- Major Life Events:

- Buying a New Car: Your insurance needs and costs will change dramatically.

- Moving: Even a short distance can alter your rates.

- Adding/Removing Drivers: A new teenage driver will significantly increase costs, while an adult child moving out can lower them.

- Marriage or Divorce: These changes often warrant a policy review.

- Homeownership: Bundling home and auto can provide significant savings.

- Changes in Driving Habits: If you start telecommuting and drive significantly less, you might qualify for low-mileage discounts.

- Paying Off Your Car: Once your loan is paid off, you might consider dropping collision and comprehensive coverage if the car’s value doesn’t justify the premium.

By proactively navigating the New York car insurance market, regularly comparing quotes, and understanding your policy, you can ensure you’re always getting the best possible rates for the coverage you need. This diligence not only helps manage your personal finances but also provides the security essential for driving on New York’s diverse roads.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.