The decision to purchase a car is one of the most significant financial commitments many individuals make, second only to buying a home. For many, a used car presents an attractive alternative to a new vehicle, offering significant savings on the initial purchase price and often mitigating the rapid depreciation that new cars experience. However, the seemingly straightforward question, “How much is a used car?” opens up a complex web of factors, variables, and hidden costs that savvy buyers must understand. It’s not just about the sticker price; it’s about discerning true value, anticipating future expenses, and making a financially sound decision that aligns with your budget and lifestyle.

Understanding the true cost of a used car requires a holistic approach, moving beyond superficial comparisons to delve into market dynamics, vehicle specifics, and the often-overlooked ongoing financial obligations. This article will dissect the intricate pricing structure of used cars, providing a comprehensive guide for anyone looking to navigate this crucial financial landscape effectively.

Key Factors Influencing Used Car Prices

The price of a used car is rarely arbitrary; it’s a culmination of numerous interconnected factors that dictate its market value. Dissecting these elements is the first step in understanding and evaluating potential purchases.

Age and Mileage

Perhaps the most obvious determinants of a used car’s price are its age and mileage. A car begins to depreciate the moment it’s driven off the lot, and this rate is steepest in the first few years.

- Depreciation Curve: New cars can lose 20-30% of their value in the first year alone, and up to 50% or more within five years. This rapid initial depreciation makes buying a slightly older used car a financially appealing strategy. A 2-3 year old vehicle often represents a sweet spot, having absorbed the steepest depreciation while still offering modern features and potentially a portion of its original warranty.

- Impact of Mileage: Mileage is a direct indicator of wear and tear. A car with significantly higher mileage, even if it’s relatively new, will generally command a lower price. Conversely, a low-mileage car for its age will often be priced at a premium. While 12,000-15,000 miles per year is considered average, the true impact of mileage depends on how those miles were accumulated (highway vs. city driving) and the vehicle’s maintenance history.

Make, Model, and Trim Level

The manufacturer, specific model, and even the trim level play a pivotal role in dictating a used car’s value, reflecting market demand, brand perception, and inherent features.

- Brand Perception and Reliability: Certain brands consistently hold their value better due to a reputation for reliability, durability, and strong resale markets. Toyota, Honda, and Subaru often feature high on lists for retained value. Luxury brands, while expensive new, can experience significant depreciation, making them more affordable in the used market, though their maintenance costs can remain high.

- Popularity and Resale Value Trends: Vehicles that are currently in high demand, such as fuel-efficient sedans or popular SUVs, will generally retain their value better than less popular models. Market trends, including fuel prices and shifts in consumer preferences (e.g., towards electric vehicles), can influence these dynamics. Researching average resale values for specific makes and models is crucial for informed financial planning.

- Impact of Specific Features/Packages (Trim): A car’s trim level denotes its specific configuration of features, engine options, and amenities. A higher trim level with desirable features like leather seats, navigation systems, or advanced safety technologies will typically fetch a higher price than a base model, even within the same make and model year. However, some advanced features can also become liabilities as they age, potentially leading to expensive repairs down the line.

Condition (Mechanical and Cosmetic)

Beyond age and mileage, the actual physical and mechanical condition of a vehicle profoundly impacts its value and your long-term financial outlay.

- Wear and Tear, Maintenance History: A well-maintained vehicle with a comprehensive service history will always be more valuable and less risky than one with an unknown past. Regular oil changes, tire rotations, and timely repairs indicate a conscientious owner. Conversely, visible cosmetic damage (dents, scratches, interior wear) and signs of neglect (dirty engine bay, warning lights) will depress a car’s price and likely indicate future expenses.

- Impact of Accidents/Repairs: A vehicle that has been involved in a major accident, even if repaired, will almost certainly have a lower resale value due to potential structural damage and insurance implications. Minor fender benders may have less impact, but full disclosure and documentation of any repairs are essential. Vehicle history reports can help uncover past accidents.

Market Demand and Location

The economic environment and geographic location can significantly sway used car prices.

- Supply and Demand Dynamics: When new car production is low (e.g., due to supply chain issues) or demand for used cars is high, prices naturally increase. Conversely, an oversupply of a particular model or a slump in overall demand can lead to price drops. Keeping an eye on broader market trends is beneficial.

- Regional Price Variations: Prices for certain types of vehicles can vary by region. For instance, SUVs and trucks might be more expensive in rural areas or regions with harsh winters, while convertibles might command a premium in sunny climates. Local economic conditions and sales tax rates also contribute to regional price differences.

Beyond the Sticker Price: Understanding the True Cost of Ownership

Focusing solely on the purchase price of a used car can lead to a rude financial awakening. The true cost of ownership extends far beyond the initial transaction, encompassing a range of ongoing expenses that must be factored into your budget.

Insurance Costs

Car insurance is a mandatory and often substantial recurring expense that varies wildly based on numerous factors.

- Factors Affecting Premiums: The make, model, year, and trim of your used car all influence insurance rates. Sportier or luxury vehicles, cars with higher repair costs, and those frequently stolen will typically incur higher premiums. Your driving record, age, location, and chosen coverage limits also play a significant role. It’s crucial to get insurance quotes for specific vehicles before purchasing to avoid a costly surprise.

- Impact of Vehicle Choice: A seemingly inexpensive used car might have surprisingly high insurance rates if it’s considered high-risk by insurers. Conversely, a slightly more expensive but statistically safer or less stolen model might result in lower monthly premiums, balancing the overall financial outlay.

Maintenance and Repair Expenses

Older vehicles, by their nature, are more prone to requiring maintenance and repairs. Budgeting for these eventualities is paramount.

- Importance of Service History: A comprehensive service history can provide valuable insight into a car’s past care and potential future needs. A car that has been meticulously maintained is less likely to spring costly surprises.

- Costs of Common Wear Items: Even well-maintained cars require regular replacement of wear items like tires, brakes, batteries, and timing belts. These costs, while predictable, can add up. Researching the cost of parts and labor for a specific make and model can give you an idea of potential future expenses.

- Potential for Unexpected Major Repairs: The older a car gets, the higher the risk of a major component failure (e.g., transmission, engine, air conditioning). Setting aside an emergency fund specifically for car repairs is a wise financial strategy when buying a used vehicle. Consider a pre-purchase inspection to mitigate this risk.

Fuel Efficiency

Fuel costs represent a significant ongoing operational expense, directly impacting your monthly budget.

- Impact of MPG on Long-Term Budget: A car with poor fuel efficiency, even if purchased cheaply, can quickly become expensive to operate over its lifespan. Calculate potential annual fuel costs based on your estimated mileage and current fuel prices to understand the true financial commitment.

- Consideration of Fuel Type: Beyond just miles per gallon, consider the required fuel type. Vehicles that demand premium gasoline will be more expensive to fill up regularly, impacting your overall budget.

Registration, Taxes, and Fees

Don’t forget the various government-imposed charges associated with buying and owning a vehicle.

- Sales Tax, Title Transfer, Annual Registration: When purchasing a used car, you’ll typically pay sales tax on the purchase price (which varies by state), a fee for transferring the title into your name, and recurring annual registration fees. These initial and ongoing costs need to be factored into your total budget.

- Emissions Testing and Inspections: Some states require regular emissions testing or safety inspections, which come with their own fees and potential repair costs if the car doesn’t pass.

Financial Strategies for Buying a Used Car

Approaching the used car market with a sound financial strategy is critical for securing the best deal and avoiding buyer’s remorse.

Budgeting and Affordability

The golden rule of car buying is to determine what you can truly afford before you even start looking.

- The “20/4/10” Rule (or similar financial guidelines): A common financial guideline suggests making a 20% down payment, financing for no more than four years, and ensuring that your total monthly car expenses (payment, insurance, fuel) do not exceed 10% of your gross monthly income. This helps ensure your car doesn’t become a disproportionate drain on your finances.

- Considering Overall Monthly Budget: Look at your entire financial picture. How much disposable income do you have after all essential bills? Factor in all potential car-related expenses—not just the monthly payment—to arrive at a realistic maximum affordable price.

Financing Options

Most people finance a used car purchase, and understanding your options is vital.

- Loans, Interest Rates, Terms: Shop around for the best interest rates from various lenders (banks, credit unions, online lenders) before you visit a dealership. A lower interest rate can save you hundreds or even thousands over the life of the loan. Shorter loan terms mean higher monthly payments but less interest paid overall.

- Impact of Credit Score: Your credit score is a major determinant of the interest rate you’ll be offered. A higher score typically qualifies you for lower rates. If your credit is less than ideal, consider improving it before applying for a loan, or be prepared for higher financing costs.

- Advantages/Disadvantages of Different Loan Types: Secured loans (car loans) are common, but you might consider a personal loan if interest rates are favorable, though they are usually unsecured and come with higher rates.

Negotiating the Price

Negotiation is a standard part of buying a used car and can significantly impact your final financial outcome.

- Researching Market Value: Arm yourself with data. Use resources like Kelley Blue Book (KBB.com), Edmunds, and NADAguides to ascertain the fair market value for the specific make, model, year, mileage, and condition of the car you’re interested in. This research provides leverage in negotiations.

- Factoring in Trade-Ins: If you have a trade-in, negotiate its value separately from the purchase price of the new-to-you car. Dealers often use trade-ins to manipulate the overall deal. Know your trade-in’s value beforehand.

The Role of Pre-Purchase Inspections and Vehicle History Reports

These tools are your financial safeguards against unforeseen future expenses.

- Protecting Your Investment: A pre-purchase inspection (PPI) by an independent, trusted mechanic is invaluable. For a small fee, a mechanic can identify existing mechanical issues, potential future problems, and signs of accident damage that might not be visible to the untrained eye, saving you potentially thousands in post-purchase repairs.

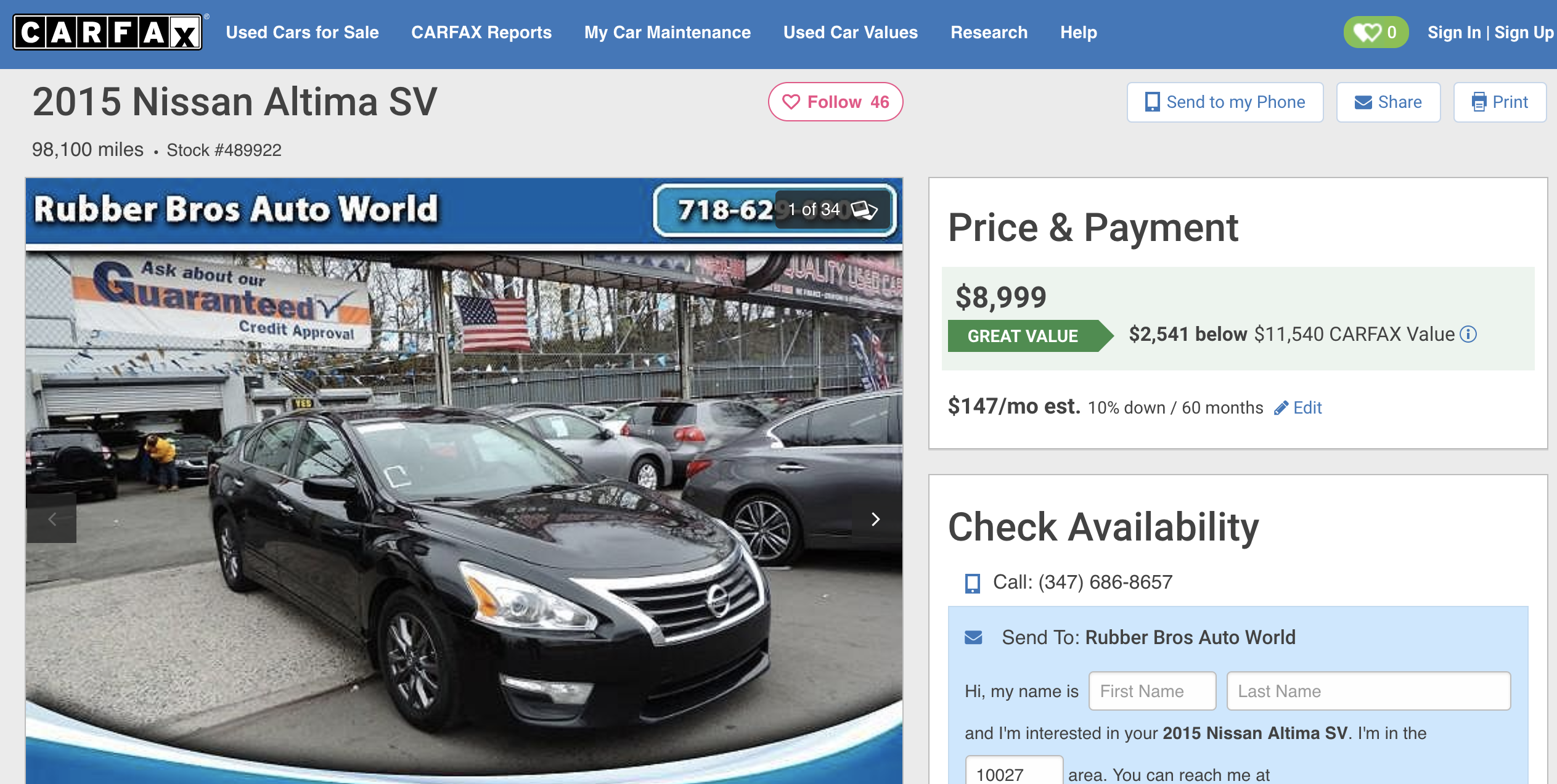

- CARFAX, AutoCheck: These vehicle history reports provide crucial information about a car’s past, including accident history, previous owners, title issues (salvage, flood), service records, and odometer discrepancies. They are a worthwhile investment to avoid buying a lemon.

Where to Buy a Used Car and Its Financial Implications

The venue from which you purchase a used car can influence both its price and the level of financial risk you assume.

Dealerships (New and Used)

Dealerships are a common choice for their convenience and perceived reliability, but come with their own financial considerations.

- Pros: Many dealerships offer certified pre-owned (CPO) vehicles, which come with extended warranties and rigorous inspections, providing added peace of mind. They also typically offer in-house financing, handle all paperwork, and may accept trade-ins.

- Cons: Prices at dealerships are often higher than private sales due to overhead costs and profit margins. You might also encounter pressure tactics or attempts to upsell on unnecessary add-ons, increasing your overall financial outlay.

Private Sellers

Buying from a private seller can often lead to the best financial deal, but requires more diligence.

- Pros: Generally lower prices and more room for negotiation, as private sellers don’t have the overhead of dealerships. You often deal directly with the owner, who can provide more detailed information about the car’s history.

- Cons: Most private sales are “as-is,” meaning no warranty or recourse if problems arise after purchase. You’re responsible for all paperwork, and vetting the seller and the car’s history requires more legwork. The financial risk is higher without due diligence.

Online Marketplaces and Auctions

These platforms offer a vast selection but demand a cautious approach.

- Pros: Online marketplaces (like AutoTrader, Craigslist) and auction sites (like eBay Motors) provide access to a wider inventory and potentially very competitive pricing, especially at auctions.

- Cons: Higher risk, especially with auctions where you often can’t inspect the vehicle beforehand. Misrepresentation is a concern. Logistics for viewing, inspecting, and transporting the vehicle can be complex and add to costs. It requires a high degree of financial savviness and risk tolerance.

Conclusion

The question “How much is a used car?” transcends a simple numerical answer. It involves a sophisticated understanding of market dynamics, the vehicle’s specific attributes, and a comprehensive assessment of both the initial purchase price and the long-term costs of ownership. From the immediate impact of age, mileage, and condition to the enduring expenses of insurance, maintenance, and fuel, every factor plays a role in the financial viability of your chosen vehicle.

By thoroughly researching market values, budgeting realistically, securing favorable financing, conducting diligent pre-purchase inspections, and understanding the nuances of different buying venues, you can transform a potentially overwhelming financial decision into a confident and astute investment. A used car, when chosen wisely, offers significant financial advantages, providing reliable transportation without the heavy financial burden of new vehicle depreciation. Empower yourself with knowledge, and you’ll not only find a great car but also make a financially sound decision for your future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.