The question “how much is a Social Security check?” is far more complex than it appears at first glance. It’s not a fixed sum, nor is it a simple average that applies universally. Instead, the amount an individual receives from Social Security is meticulously calculated based on a confluence of factors, primarily reflecting their lifetime earnings, their work history, and crucially, the age at which they choose to begin receiving benefits. Understanding these variables is not just an academic exercise; it’s a vital component of prudent retirement planning, offering insights that can significantly impact one’s financial security in later life.

Social Security, established in 1935, serves as a cornerstone of financial protection for millions of Americans, providing retirement income, disability benefits, and survivor benefits. It’s a pay-as-you-go system, meaning current workers’ contributions largely fund the benefits of today’s retirees and other beneficiaries. While the system aims to provide a safety net, individual benefit amounts vary wildly, ranging from just over $1,000 to nearly $5,000 per month for the highest earners who claim at the optimal age. This article delves into the intricate mechanics behind these calculations, exploring the critical elements that determine the size of your Social Security check and offering strategies to potentially maximize this essential income stream.

Understanding the Foundations of Social Security Benefits

At its core, the Social Security Administration (SSA) uses a standardized, albeit complex, formula to determine an individual’s Primary Insurance Amount (PIA). The PIA is the benefit an individual would receive if they start collecting benefits exactly at their Full Retirement Age (FRA). This calculation hinges on your earnings history and the duration of your contributions to the system.

The Role of Work History and Earnings

To be eligible for Social Security benefits, most individuals need to accumulate 40 “quarters of coverage” over their working career. A quarter of coverage is earned by reaching a certain threshold of earnings within a calendar year; in 2024, you earn one quarter for every $1,730 in earnings, up to a maximum of four quarters per year. This means that to qualify, you generally need to have worked and paid Social Security taxes for at least 10 years.

Once eligibility is established, the SSA looks at your lifetime earnings. Specifically, they identify your highest 35 years of “covered earnings”—earnings on which you paid Social Security taxes. If you have fewer than 35 years of earnings, the missing years are entered as zeros in the calculation, which can significantly reduce your benefit. These annual earnings are then “indexed” to account for changes in average wages over time, bringing earlier earnings into line with more recent wage levels. This process results in your Average Indexed Monthly Earnings (AIME). The AIME is a crucial input, representing your average monthly earnings over your career, adjusted for inflation.

The Primary Insurance Amount (PIA) Formula

With your AIME calculated, the SSA applies a progressive formula to determine your Primary Insurance Amount (PIA). This formula is designed to replace a higher percentage of earnings for low-income workers than for high-income workers, reflecting Social Security’s goal of providing a floor of protection. The formula uses “bend points”—specific dollar amounts that change annually—to apply different percentages to different segments of your AIME.

For example, for someone turning 62 in 2024, the PIA formula would be:

- 90% of the first $1,174 of AIME, plus

- 32% of AIME between $1,174 and $7,078, plus

- 15% of AIME above $7,078.

The sum of these three parts is your PIA, which is the monthly benefit you would receive if you claim at your Full Retirement Age. It’s important to note that there’s an annual maximum for earnings subject to Social Security tax (the “taxable maximum”), which in 2024 is $168,600. This cap means that even if you earn more than this amount, only earnings up to the taxable maximum are considered in your AIME calculation, placing an upper limit on potential benefits.

Key Factors Influencing Your Social Security Benefit

Beyond your earnings history, several other critical factors profoundly influence the final amount of your monthly Social Security check. The most significant of these is your age at the time you elect to start receiving benefits.

Your Age at Claiming Benefits

The decision of when to start collecting Social Security benefits is one of the most impactful financial choices you’ll make regarding your retirement. Your Full Retirement Age (FRA) is the age at which you are entitled to receive 100% of your Primary Insurance Amount (PIA). FRA varies based on your birth year: it’s 66 for those born between 1943 and 1954, gradually increases to 67 for those born in 1960 or later.

-

Claiming Early (Age 62): You can begin receiving retirement benefits as early as age 62. However, claiming before your FRA results in a permanent reduction in your monthly benefit. The reduction is approximately 6.67% per year for the first three years before FRA and then 5% per year for each additional year prior to that. For someone with an FRA of 67, claiming at 62 means a permanent 30% reduction in their PIA. This reduction is designed to compensate for the fact that you will be receiving benefits for a longer period.

-

Claiming Late (Up to Age 70): Conversely, if you delay claiming benefits past your FRA, you can earn delayed retirement credits. For each month you delay, up to age 70, your monthly benefit increases. These credits amount to an 8% annual increase for each year you delay past your FRA, up until age 70. For an individual with an FRA of 67, delaying until age 70 would result in a permanent 24% increase in their monthly benefit compared to their PIA. There’s no further benefit increase for delaying past age 70, making it the optimal maximum claiming age for individual benefits.

The decision to claim early, at FRA, or late should be carefully considered based on your health, other retirement income sources, marital status, and individual financial needs.

Other Income and Earnings Limits

While Social Security is intended to be a foundational retirement income, it can be affected by other income sources, particularly if you claim benefits before your FRA and continue to work.

- The Earnings Test: If you claim Social Security benefits before your FRA and continue to work, your benefits may be temporarily reduced if your earnings exceed certain annual limits. For 2024, if you are under FRA for the entire year, $1 in benefits will be withheld for every $2 you earn above $22,320. In the year you reach FRA, a different limit applies, and $1 in benefits will be withheld for every $3 you earn above $59,520 (until the month you reach FRA). Once you reach your FRA, the earnings test no longer applies, and you can earn any amount without your Social Security benefits being reduced. Any benefits withheld due to the earnings test are not lost; they are later factored back into your benefit calculation, often resulting in a higher monthly payment once you reach FRA.

- Taxation of Social Security Benefits: Your Social Security benefits can be subject to federal income tax if your “provisional income” exceeds certain thresholds. Provisional income is generally calculated as your adjusted gross income (AGI) plus non-taxable interest plus half of your Social Security benefits.

- If your provisional income is between $25,000 and $34,000 for an individual ($32,000 and $44,000 for a married couple filing jointly), up to 50% of your benefits may be taxable.

- If your provisional income exceeds $34,000 for an individual ($44,000 for a married couple filing jointly), up to 85% of your benefits may be taxable.

Some states also tax Social Security benefits, adding another layer of complexity to the net amount you ultimately receive.

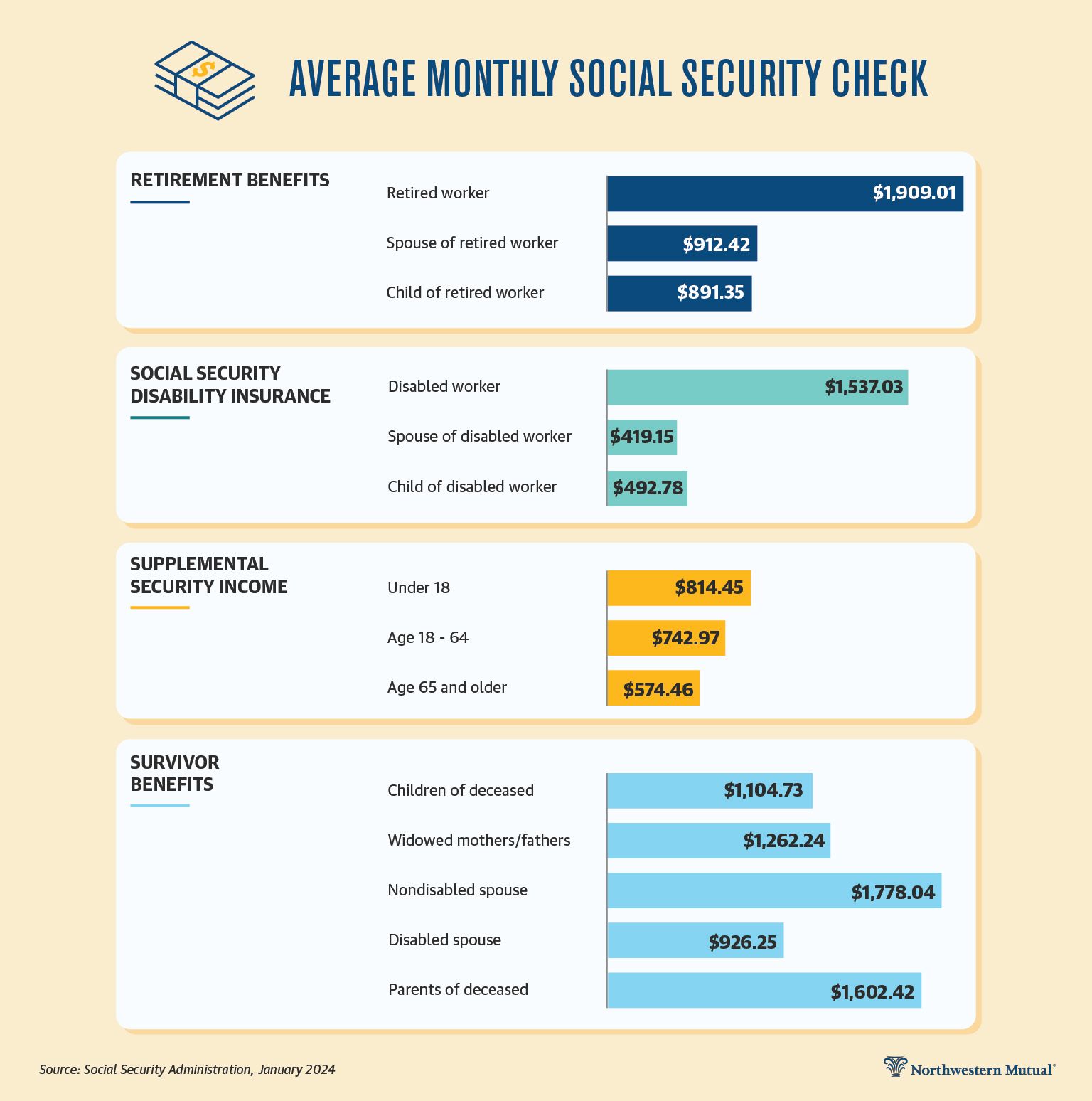

Types of Social Security Benefits and Their Calculation

While retirement benefits are the most commonly discussed, Social Security encompasses several different types of benefits, each with its own eligibility and calculation nuances, all stemming from the primary worker’s earnings record.

Retirement Benefits (Primary Focus)

As detailed earlier, retirement benefits are the most significant component of Social Security. The amount is directly derived from your Average Indexed Monthly Earnings (AIME) and then adjusted by the PIA formula, taking into account your claiming age relative to your Full Retirement Age (FRA). The monthly check you receive is your PIA, increased by delayed retirement credits if you claim late, or decreased by early claiming reductions.

There are maximum and minimum benefits that can be paid. For instance, the maximum Social Security benefit for someone retiring at FRA in 2024 is $3,822 per month. For someone who claims at age 70, this could be even higher, nearing $4,873. These maximums are reserved for individuals who consistently earned at or above the Social Security taxable maximum for at least 35 years. On the other end, while there isn’t a strict “minimum” benefit, low earners who have met the 40-quarter requirement will receive a benefit based on their low AIME and PIA calculation, ensuring a basic level of support.

Spousal and Survivor Benefits

Social Security also provides benefits to certain family members based on the primary earner’s work record, even if those family members have little to no work history themselves.

-

Spousal Benefits: A spouse may be eligible to receive benefits based on their living spouse’s work record. Generally, a spouse can receive up to 50% of their partner’s PIA if they claim at their own FRA. If the spouse claims early, their spousal benefit will be reduced. To claim spousal benefits, the primary earner must generally have already filed for their own benefits.

-

Survivor Benefits: When a primary earner dies, certain family members—including a surviving spouse, minor children, or disabled adult children—may be eligible for survivor benefits. A surviving spouse can receive up to 100% of the deceased worker’s benefit amount if they claim at their own FRA, or a reduced amount if they claim earlier (as early as age 60, or age 50 if disabled). The amount depends on the deceased worker’s PIA and the survivor’s age and relationship.

Disability Benefits

Social Security Disability Insurance (SSDI) provides benefits to individuals who have worked and paid Social Security taxes but are now unable to engage in substantial gainful activity due to a severe medical condition that is expected to last at least one year or result in death. Eligibility for SSDI requires sufficient “work credits,” similar to retirement benefits, but with a recent work test. The amount of a disability check is essentially equivalent to the individual’s PIA, meaning it is calculated as if they had reached their FRA and started collecting benefits, based on their earnings history up to the point of disability.

Strategies to Maximize Your Social Security Check

Given the profound impact Social Security can have on your financial well-being in retirement, understanding strategies to maximize your benefits is crucial. While some factors are immutable (like your birth year), others are within your control.

Working Longer and Earning More

The most straightforward way to increase your Social Security check is to increase your lifetime indexed earnings.

- More High-Earning Years: Since the SSA uses your highest 35 years of indexed earnings to calculate your AIME, working beyond 35 years, especially if your current earnings are higher than some of your earlier, lower-earning years, can replace those lower years with higher ones in the calculation, thereby increasing your overall AIME and subsequent PIA.

- Working to 35 Years: If you haven’t worked for 35 years, ensuring you reach this milestone is paramount. Every year short of 35 will result in a zero-earnings year being averaged into your AIME, significantly depressing your benefit.

Strategic Claiming Age

As previously discussed, your claiming age is arguably the most powerful lever you have over your Social Security benefit.

- Consider Delaying Beyond FRA: For many, delaying benefits past their Full Retirement Age (up to age 70) is the most effective strategy to boost monthly income. The 8% annual delayed retirement credits can lead to a significantly higher monthly check for the rest of your life. This strategy is particularly beneficial if you have other sources of income to cover your expenses in your early 60s, are in good health, and expect to live a long life.

- Weighing Early Claiming: While early claiming results in a permanent reduction, it might be appropriate for individuals facing severe health issues, immediate financial needs, or those who simply do not expect to live long enough to benefit from delaying. The key is to run the numbers and understand the trade-offs.

Coordinating with Your Spouse

For married couples, strategic claiming can unlock even greater combined benefits.

- Focus on the Higher Earner’s Delay: Often, the optimal strategy for a couple involves the higher-earning spouse delaying their claim until age 70 to maximize their benefit. This not only increases their individual check but also provides a higher base for survivor benefits, which is crucial if that spouse predeceases the other.

- Spousal Claiming Flexibility: The lower-earning spouse might choose to claim their own benefit early, or claim a spousal benefit (if eligible) once the higher earner files. The rules around spousal benefits and the coordination of claims can be complex, and consulting with a financial advisor or the SSA directly is highly recommended to explore all available options for maximizing household benefits.

Conclusion

The question “how much is a Social Security check?” reveals a complex interplay of personal history, economic policy, and strategic decisions. It’s not a one-size-fits-all answer but rather a deeply personal calculation influenced by decades of work, your earnings trajectory, and your pivotal choice of when to begin receiving benefits. Understanding the calculation—from the indexing of earnings and the Average Indexed Monthly Earnings (AIME) to the Primary Insurance Amount (PIA) and the impact of claiming age—is fundamental to effective retirement planning.

While Social Security is designed to provide a foundational income, individuals have agency in optimizing their benefits through thoughtful planning. By working consistently, maximizing high-earning years, and making informed decisions about when to claim, especially in coordination with a spouse, you can significantly influence the size of your monthly Social Security check. The Social Security Administration provides personalized estimates through your online “My Social Security” account, which is an invaluable tool for planning. Proactive engagement with these figures and an understanding of the underlying mechanics are not just recommended but essential for securing a more robust financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.