In the world of personal finance, few expenses are as volatile or as psychologically taxing as the cost of airfare. When a consumer asks, “How much is a plane ticket?” they are rarely met with a static answer. Instead, they enter a complex financial ecosystem governed by real-time algorithms, global economic shifts, and sophisticated yield management strategies.

Understanding the price of a plane ticket is no longer just about searching a website; it is about understanding the intersection of market economics and personal financial planning. To master the art of travel budgeting, one must look beneath the surface of the “sticker price” and analyze the underlying financial structures that dictate what we pay to get from point A to point B.

The Economic Anatomy of Airfare: Understanding Dynamic Pricing

The price of a plane ticket is a masterclass in dynamic pricing, a financial strategy where businesses adjust prices based on real-time demand, competitor behavior, and other external factors. For the savvy traveler, understanding these economic levers is the first step in optimizing travel expenditures.

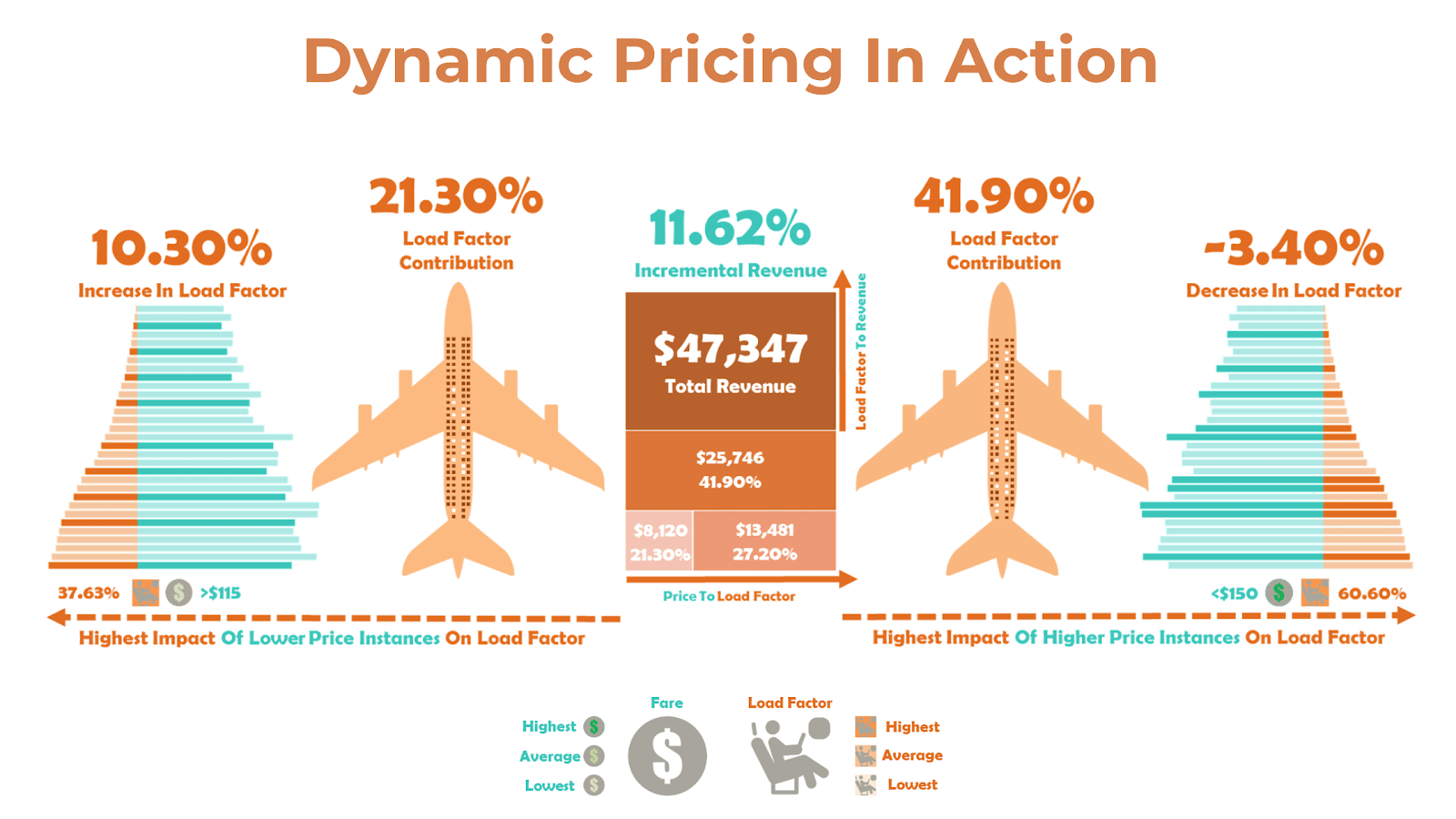

Yield Management and the Scarcity Principle

Airlines do not sell seats; they sell “fare buckets.” This is a core concept in yield management—the process of allocating the right type of capacity to the right kind of customer at the right price to maximize revenue. Each flight is divided into various price points. As the cheaper buckets are filled, the price automatically jumps to the next tier. This creates a financial environment where scarcity drives cost. From a personal finance perspective, this means that “time” is a literal currency; the earlier you commit your capital, the less of it you typically have to spend.

The Impact of Macroeconomic Factors on Retail Prices

Beyond the internal algorithms of an airline, external financial pressures play a significant role. Jet fuel represents one of the largest operating expenses for carriers, often accounting for 20% to 30% of total costs. When global oil prices fluctuate, those costs are passed directly to the consumer in the form of fuel /surcharges or base fare increases. Additionally, currency exchange rates can dramatically shift the “real” cost of a ticket. For an investor or a business traveler, fluctuations in the strength of the dollar or euro can mean the difference between a budget-friendly trip and a significant financial drain.

Strategic Budgeting: Beyond the Base Fare

A common mistake in personal finance is budgeting for a plane ticket based solely on the initial search result. In the modern aviation industry, the “base fare” is often just the entry point into a multi-layered financial transaction.

The Rise of Ancillary Revenue and Unbundled Fares

The aviation industry has shifted toward an “unbundled” model, particularly among low-cost carriers. This strategy separates the core service—transportation—from traditional inclusions like baggage, seat selection, and on-board refreshments. Financially, this is known as ancillary revenue. For the consumer, this requires a more granular approach to budgeting. A $99 ticket can quickly escalate to $250 once “hidden” fees are accounted for. When calculating how much a plane ticket truly costs, one must perform a total cost of ownership (TCO) analysis, factoring in every potential fee to ensure an apples-to-apples comparison between carriers.

Taxes, Fees, and Regulatory Surcharges

A significant portion of any plane ticket price is not actually kept by the airline. It is collected on behalf of governments and airport authorities. These include passenger facility charges (PFCs), segment fees, and international arrival/departure taxes. In some jurisdictions, these regulatory costs can represent up to 40% of the total ticket price. Understanding these fixed costs helps travelers realize why certain routes (like those through major international hubs) remain expensive regardless of airline competition.

Financial Tools and Optimization Strategies

To answer “how much is a plane ticket” accurately, one must utilize the modern fintech tools designed to track, predict, and lower these costs. Just as an investor uses a terminal to track stock prices, a traveler should use data-driven platforms to manage their travel capital.

Leveraging Predictive Analytics and Price Tracking

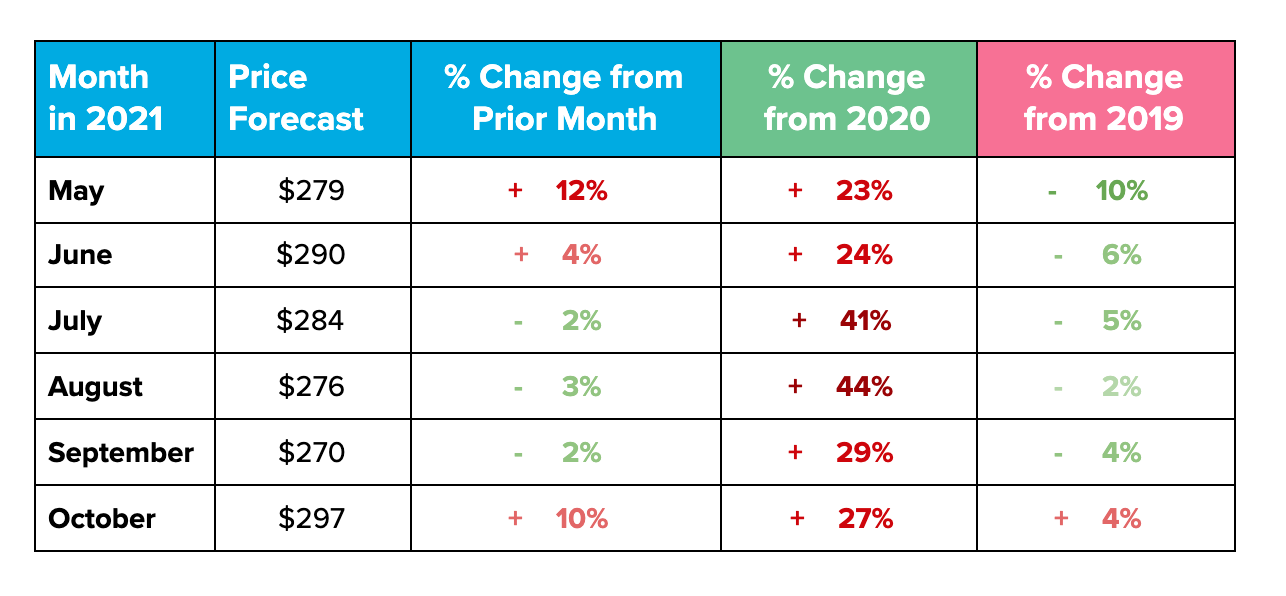

We live in an era of “Big Data” for travel. Tools like Google Flights, Hopper, and Skyscanner use historical data and machine learning to predict whether a fare will rise or fall. Using these tools is a form of financial risk management. By setting price alerts, a consumer can wait for a “buy” signal, ensuring they are not purchasing at a local maximum. This disciplined approach to buying can save hundreds of dollars, which can then be redirected into other financial goals or investment vehicles.

The Arbitrage of Loyalty Points and Credit Card Rewards

In the modern economy, “miles” and “points” act as a secondary form of currency. For many, the answer to how much a plane ticket costs is “zero dollars plus 60,000 points.” However, points have a specific “cent-per-point” (CPP) value. High-level financial planning involves calculating the ROI of using points versus cash. If a ticket costs $500 or 50,000 points, the value is 1 cent per point—often a poor redemption. If the ticket is $1,500 for the same 50,000 points, the value is 3 cents per point, representing a significant financial win. Treating loyalty programs as a diversified asset portfolio is key to long-term travel affordability.

Tactical Financial Planning for High-Cost Travel

For those looking to integrate travel into their broader financial life, viewing airfare as a planned expenditure rather than a spontaneous impulse is vital. This requires a shift from “spending” to “allocation.”

The 21-Day Rule and Booking Windows

Historical financial data suggests that for domestic flights, the “sweet spot” for booking is often 21 to 60 days in advance. This is the period where airlines have enough data to know if a flight is underperforming but haven’t yet entered the “last-minute” premium phase where business travelers are forced to pay high prices. By planning your cash flow around these windows, you avoid the “desperation premium” that occurs when booking within the 14-day window.

Implementing Sinking Funds for Travel

A “sinking fund” is a strategic way to save for a specific expense over time. Instead of putting a $1,200 international ticket on a high-interest credit card, a sound financial strategy involves reverse-engineering the cost. If you plan to travel in 12 months, allocating $100 a month into a high-yield savings account (HYSA) allows you to pay for the ticket in cash. Not only does this prevent debt, but the interest earned on the sinking fund effectively “discounts” the price of the ticket.

Travel as an Investment: Analyzing the ROI of Mobility

Finally, it is worth considering the “Return on Investment” (ROI) of a plane ticket. In business finance, travel is often categorized as an expense, but it should be viewed as an investment in human capital or market expansion.

Professional Networking and Market Expansion

For an entrepreneur or a career-focused professional, a plane ticket is a tool for networking, closing deals, or attending industry-defining conferences. The financial cost of the ticket is often negligible compared to the lifetime value (LTV) of a new client or a strategic partnership formed in person. When seen through this lens, the question isn’t just “how much is the ticket,” but “what is the potential return on this expenditure?”

The Value of Personal Well-being and Productivity

In personal finance, we often focus on the “save” side of the equation, but the “spend” side is equally important for long-term sustainability. Investing in travel can prevent burnout, increasing a professional’s long-term earning potential. While harder to quantify on a balance sheet, the “utility” gained from travel is a real economic benefit. A well-timed vacation can be a hedge against productivity loss, making the cost of the plane ticket a necessary maintenance expense for one’s most valuable asset: themselves.

Conclusion

The question “How much is a plane ticket?” serves as a gateway into a deeper understanding of modern market dynamics. By recognizing that airfare is a commodity influenced by yield management, ancillary fees, and macroeconomic shifts, consumers can move away from reactive spending and toward proactive financial management. Whether through the strategic use of credit card rewards, the disciplined application of sinking funds, or the utilization of predictive analytics, the goal is the same: to maximize the value of every dollar spent on mobility. In the end, the true cost of a plane ticket is not just the number on the receipt, but the efficiency with which you navigate the financial systems that put you in the air.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.