In the realm of personal and business finance, choosing the right payment method can be as crucial as the transaction itself. While digital payments and personal checks dominate everyday exchanges, certain significant transactions demand a higher level of security and assurance. This is where a cashier’s check often comes into play. It represents a promise of payment directly from the bank, offering an unparalleled level of safety compared to many other instruments. However, this security comes with a cost. Understanding “how much is a cashier’s check” involves more than just a simple fee; it requires delving into the nature of this financial tool, its benefits, the factors influencing its price, and its role in a sound financial strategy.

This comprehensive guide will break down the typical costs associated with obtaining a cashier’s check, explore the underlying reasons for its expense, and help you determine when this particular financial instrument is the most appropriate choice for your needs.

What Exactly is a Cashier’s Check?

Before we discuss the price, it’s essential to grasp the fundamental nature of a cashier’s check. Often confused with other payment methods, a cashier’s check stands out due to the direct involvement and guarantee of the issuing financial institution.

Defining a Secure Payment Instrument

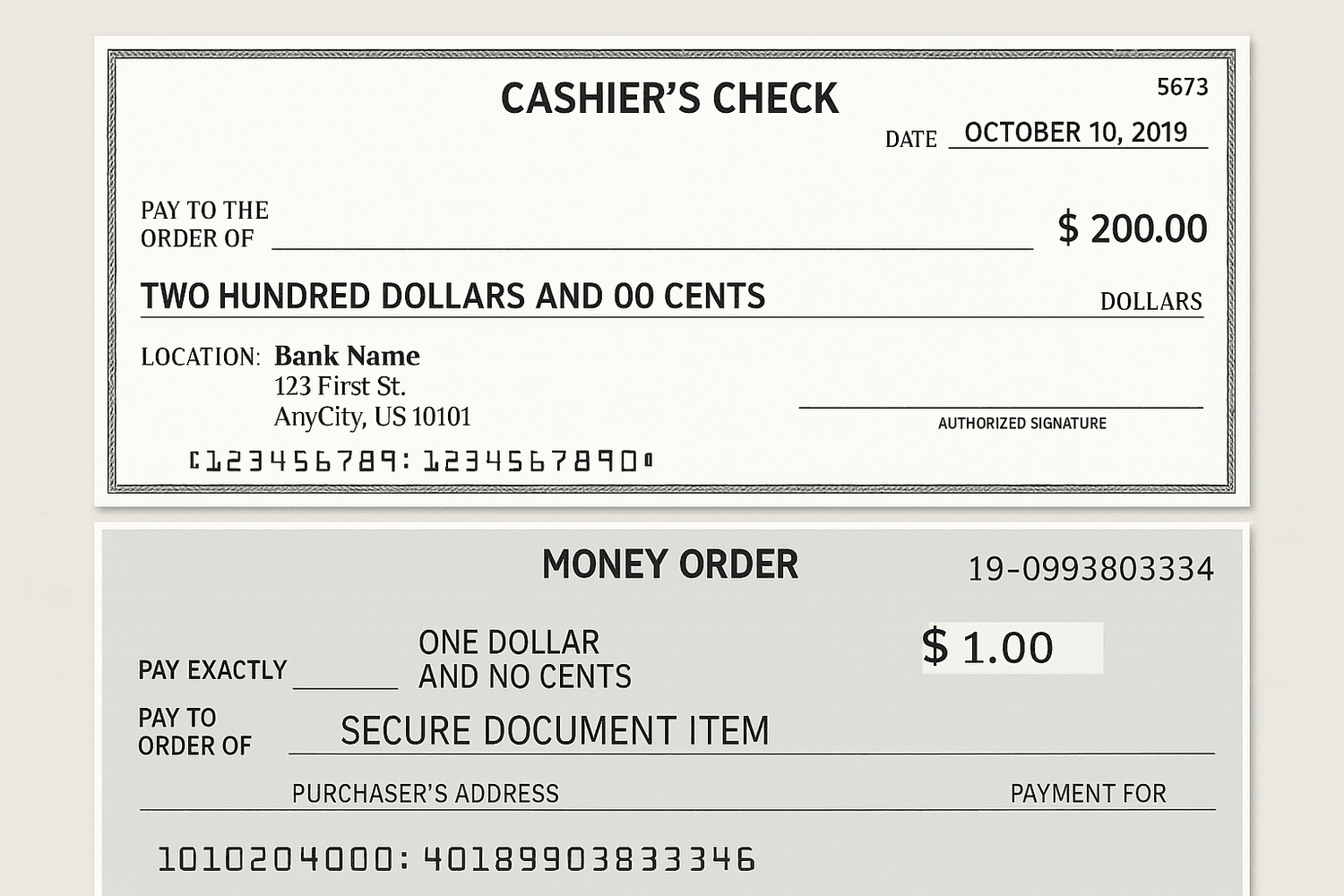

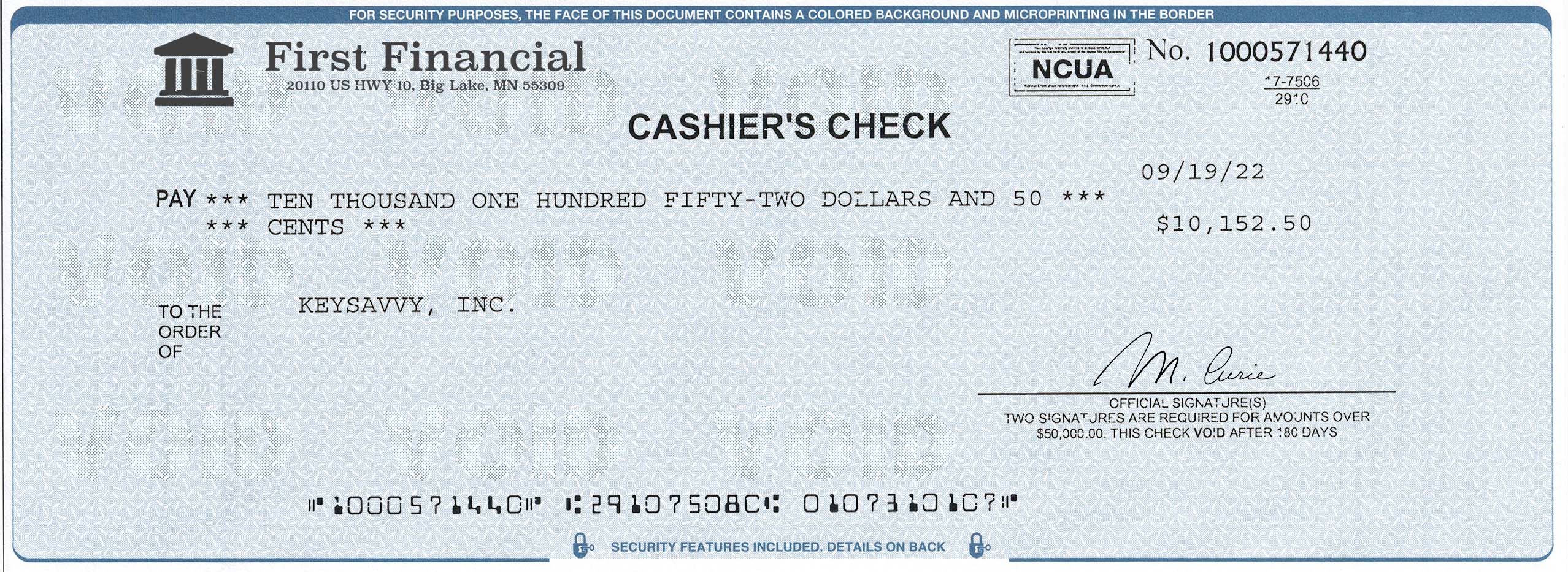

A cashier’s check is a check guaranteed by the issuing bank or credit union. When you purchase one, the funds are immediately drawn from your account (or paid in cash) and transferred into the bank’s own account. The bank then issues the check, making itself the payer, not you. This critical distinction means the bank assumes responsibility for the payment, guaranteeing the funds are available and will clear. This makes it a highly trusted form of payment, especially for large sums where the recipient needs absolute assurance that the payment will not bounce.

Why Banks Issue Them

Banks issue cashier’s checks primarily to provide a secure and verifiable method of payment for their customers. By drawing funds directly from the customer’s account and using their own funds to back the check, the bank mitigates the risk of insufficient funds or fraud that can be associated with personal checks. This service enhances the bank’s offerings and provides a vital tool for transactions that require certainty. For the bank, it’s a service that comes with administrative overhead, security protocols, and a degree of liability, all of which contribute to the fee charged.

Distinguishing from Personal Checks and Money Orders

It’s crucial not to conflate cashier’s checks with other common payment methods:

- Personal Checks: These are drawn directly from your personal checking account. The payment is only guaranteed if you have sufficient funds in your account. The risk of a bounced check lies entirely with the recipient.

- Money Orders: These are prepaid instruments for smaller amounts, typically purchased at post offices, convenience stores, or some banks. While also prepaid, they generally have lower maximum limits (e.g., $1,000) and are not issued directly by a bank from its own funds in the same way a cashier’s check is. They offer a level of security but are not suitable for very large transactions.

- Certified Checks: Similar in security, a certified check is also a personal check, but the bank verifies that sufficient funds are in the account, sets those funds aside, and stamps the check as “certified.” While also guaranteed, the payer is still the account holder, not the bank itself. The key difference is that with a certified check, your funds are held; with a cashier’s check, the bank’s funds are used, having already collected the money from you.

The robust guarantee offered by a cashier’s check is its primary distinguishing feature and often justifies its cost.

Deconstructing the Cost: Fees for a Cashier’s Check

The price of a cashier’s check is not uniform across all financial institutions or even all customers within the same institution. Several factors come into play, making it important to understand the typical fee structures and potential ways to minimize these costs.

Typical Fee Structures Across Institutions

The fee for a cashier’s check generally ranges from $5 to $15 at most major banks and credit unions in the United States. This is a common service charge that reflects the administrative effort and the financial guarantee provided by the institution.

- Major Banks: Large national banks like Bank of America, Chase, Wells Fargo, and Citibank often charge in the $8 to $10 range for non-account holders or those with basic checking accounts.

- Credit Unions: Credit unions are member-owned and often operate with a philosophy of lower fees. Many credit unions offer cashier’s checks for free or at a reduced rate (e.g., $3-$7) to their members, especially those with certain account tiers or relationship statuses.

- Third-Party Providers: While less common for cashier’s checks (which require a bank’s direct guarantee), some check-cashing services or money transfer agents might offer similar guaranteed payment options (like money orders) at varying rates, but these are not true cashier’s checks.

Factors Influencing the Fee Amount

Several elements can influence the exact fee you’ll encounter:

- Account Holder Status: This is perhaps the biggest determinant. If you have an account at the institution, you’re more likely to receive a discount or even a free cashier’s check. Non-account holders will almost always pay a higher fee, if the institution even offers the service to them.

- Account Type/Relationship: Customers with premium checking accounts, certain wealth management accounts, or a long-standing relationship with a bank may receive a certain number of free cashier’s checks per month or year. This is a common perk for high-value customers.

- Geographic Location: While less significant than account status, fees can sometimes vary slightly by region or even by specific branch policies.

- The Amount of the Check: In rare cases, for extremely large sums (e.g., hundreds of thousands or millions), a bank might have a tiered fee structure, though for most common transactions, the fee is flat regardless of the check amount.

- Urgency/Special Requests: expedited processing or other special handling requests might incur additional charges, though this is uncommon for standard cashier’s checks.

Avoiding or Minimizing Fees

While the fee for a cashier’s check is generally modest, there are strategies to avoid or reduce it:

- Maintain a Premium Account: As mentioned, many banks waive cashier’s check fees for customers who maintain a minimum balance in specific checking or savings accounts, or for those with certain investment accounts. Review your bank’s fee schedule for details on these benefits.

- Utilize Credit Union Membership: If you’re a member of a credit union, check their fee schedule. They often offer these services at lower costs or for free as a membership perk.

- Shop Around: If you don’t have an account that offers free checks, call a few local banks or credit unions to compare their fees. While a few dollars might not seem like much, it can add up if you need them regularly.

- Consider Alternatives: For smaller transactions where a guarantee is needed, a money order might be a cheaper alternative, though it comes with lower limits. For larger, immediate transfers, a wire transfer might be necessary, but typically carries a higher fee.

The Value Proposition: Why Pay for a Cashier’s Check?

Given that there’s usually a fee, why would someone choose a cashier’s check over a free personal check or a less expensive money order? The answer lies in the unique combination of security, reliability, and widespread acceptance it offers.

Enhanced Security for Large Transactions

The primary reason to use a cashier’s check is the unparalleled security it provides for both the payer and the payee. For the payee, the funds are guaranteed by the bank, eliminating the risk of a bounced check. This is crucial for high-value transactions where the recipient cannot afford to take on the risk of non-payment. For the payer, once the check is issued, the funds are debited from their account, providing a clear record and preventing the payer from having to manage that specific sum in their account until the check clears.

Guaranteed Funds: Peace of Mind for Payee and Payer

The guarantee from the financial institution means the check is as good as cash, but with the added benefits of traceability and security against theft (unlike physical cash). This peace of mind is invaluable in situations where trust is paramount but not fully established, such as between private parties in a major sale. It also provides a clear audit trail, which can be important for tax purposes or in case of disputes.

Common Scenarios Requiring a Cashier’s Check

Cashier’s checks are typically used for situations involving significant amounts of money where security and guaranteed payment are non-negotiable.

- Real Estate Transactions: When buying a home, you might need a cashier’s check for the earnest money deposit, closing costs, or even the down payment.

- Vehicle Purchases: Buying a car, boat, or RV from a private seller or even some dealerships often requires a cashier’s check.

- Large Deposits: Making a security deposit for a rental property, a tuition deposit for a university, or a significant investment might necessitate a cashier’s check.

- Legal Settlements: In many legal cases, a cashier’s check is the preferred method for making or receiving settlement payments.

- International Transactions (Less Common Now): While wire transfers are more common, some cross-border payments still use cashier’s checks, although with increased scrutiny due to fraud concerns.

- Transactions with Unknown Parties: When dealing with someone you don’t know well, a cashier’s check minimizes risk for both parties.

Where to Obtain a Cashier’s Check and What You Need

Acquiring a cashier’s check is a straightforward process, provided you have the necessary information and funds.

Banks and Credit Unions: Your Primary Source

Your own bank or credit union is the easiest and most common place to get a cashier’s check. It’s generally recommended to go to an institution where you have an account, as this simplifies the process, often reduces fees, and ensures the funds are readily accessible. While some banks might issue cashier’s checks to non-account holders, they typically charge higher fees and may require additional verification.

Required Documentation and Information

When you go to get a cashier’s check, you will need:

- Identification: A valid government-issued photo ID (driver’s license, passport, state ID).

- Account Number: If you’re drawing from your bank account.

- Funds: Sufficient funds in your account to cover the check amount plus the fee, or the cash equivalent if you’re paying with cash.

- Payee Information: The full legal name of the person or entity you are paying. Accuracy here is crucial as any error could invalidate the check or cause delays.

- Amount: The exact amount of the check.

The Process of Acquiring One

The process is simple:

- Visit a Branch: Go to a teller at your bank or credit union.

- Request a Cashier’s Check: Inform the teller you wish to purchase a cashier’s check.

- Provide Details: Give them your ID, account information, the payee’s name, and the exact amount.

- Funds Transfer: The teller will debit the amount from your account (or take your cash payment) plus the fee.

- Issuance: The bank will print the cashier’s check, bearing its name as the payer.

- Verification: Always double-check all the details on the check before leaving the bank.

Alternatives to Cashier’s Checks: Weighing Your Options

While a cashier’s check is excellent for specific scenarios, it’s not always the only or best option. Understanding alternatives can help you make a financially savvy decision.

Money Orders: Lower Cost, Lower Limit

For smaller amounts (typically up to $1,000), a money order offers a guaranteed payment at a lower cost (often $1-$2). They are widely available at post offices, Western Union locations, some grocery stores, and even some banks. While secure, their lower limit makes them unsuitable for significant transactions like a car purchase.

Wire Transfers: Speed and Higher Fees

Wire transfers are electronic transfers of funds directly from one bank account to another. They are often the fastest way to send money, sometimes within hours, and can handle very large sums. However, they come with higher fees (typically $25-$50 for domestic transfers) and are irreversible once sent, making careful verification of recipient details paramount. They are ideal when speed is critical, such as closing on a property.

Certified Checks: Bank Endorsement, Payer’s Funds

As discussed earlier, a certified check is your personal check that the bank has guaranteed by verifying funds and setting them aside. It offers similar security to a cashier’s check but is still drawn on your account. Fees for certified checks are often similar to or slightly lower than cashier’s checks. They are suitable when the recipient prefers your check but needs bank assurance.

Digital Payment Solutions: When They’re Appropriate

For everyday transactions or transfers between trusted parties, digital solutions like Zelle, PayPal, Venmo, or bank-to-bank transfers are fast, convenient, and often free. However, they typically have transaction limits, lack the explicit bank guarantee of a cashier’s check for large sums, and may not be accepted by all entities (e.g., car dealerships, closing attorneys). For informal, smaller transactions, they are usually the preferred choice.

In conclusion, “how much is a cashier’s check” is a question with a straightforward answer, usually ranging from $5 to $15. However, the true cost lies not just in the fee, but in the decision of whether its unparalleled security and guarantee are worth that price for your specific transaction. By understanding its benefits, recognizing the scenarios where it’s essential, and knowing your alternatives, you can make informed financial decisions that protect your assets and ensure smooth, secure exchanges.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.