In the landscape of personal finance, understanding the transition from an hourly rate to an annual salary is more than just a mathematical exercise; it is the foundation of effective budgeting and long-term wealth building. When you earn $22 an hour, you are positioned at a critical juncture in the modern economy. It is a wage that often sits above the entry-level floor but requires strategic management to ensure it supports a comfortable lifestyle and future financial security.

To navigate your finances successfully, you must look beyond the surface-level “gross” numbers and dive into the mechanics of net income, tax obligations, and cost-of-living adjustments. This guide provides a deep dive into what $22 an hour truly looks like annually and how to optimize that income for a robust financial future.

The Mathematical Breakdown: Calculating Your Gross Income

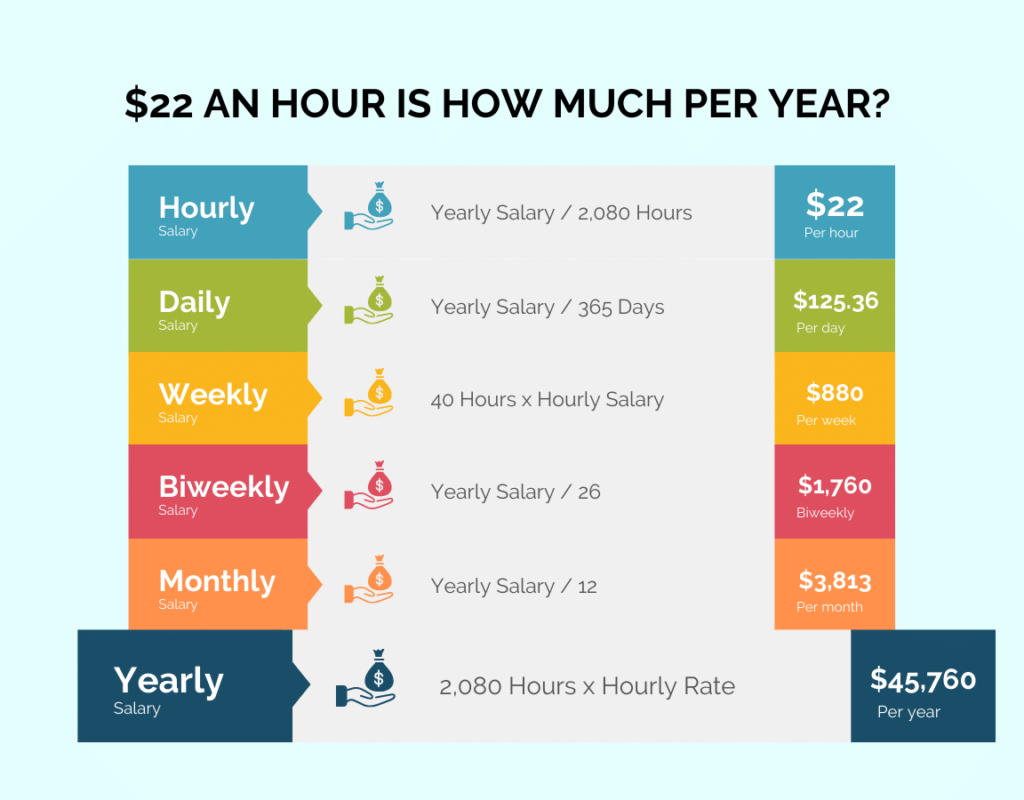

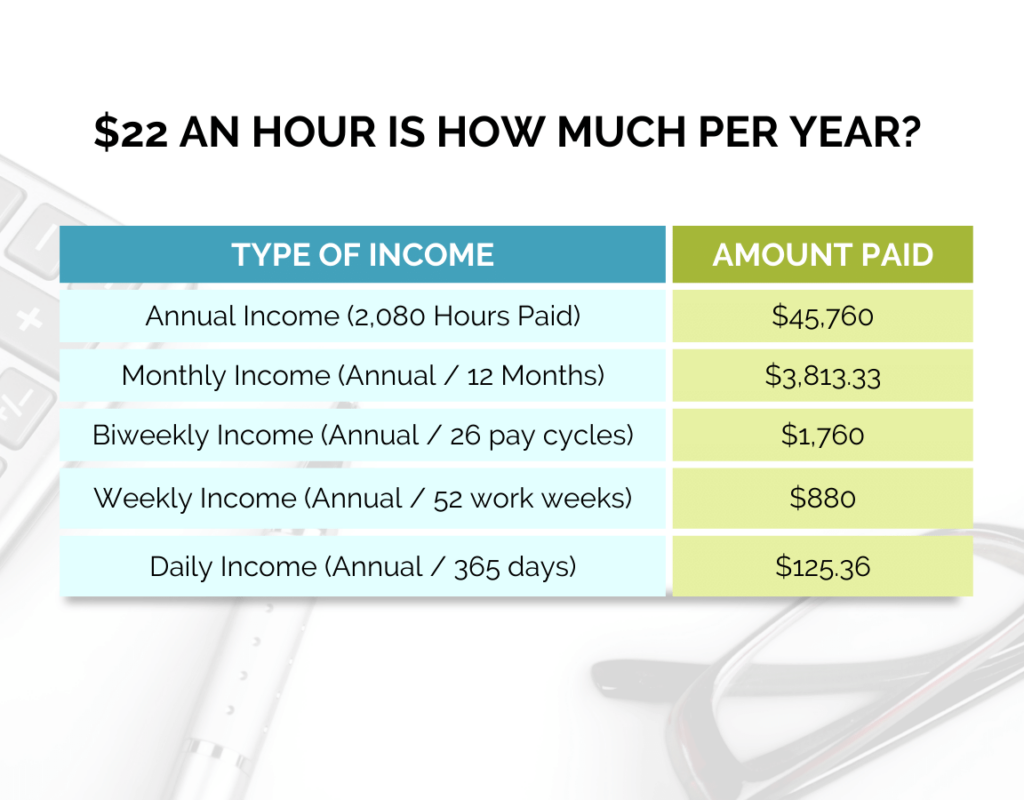

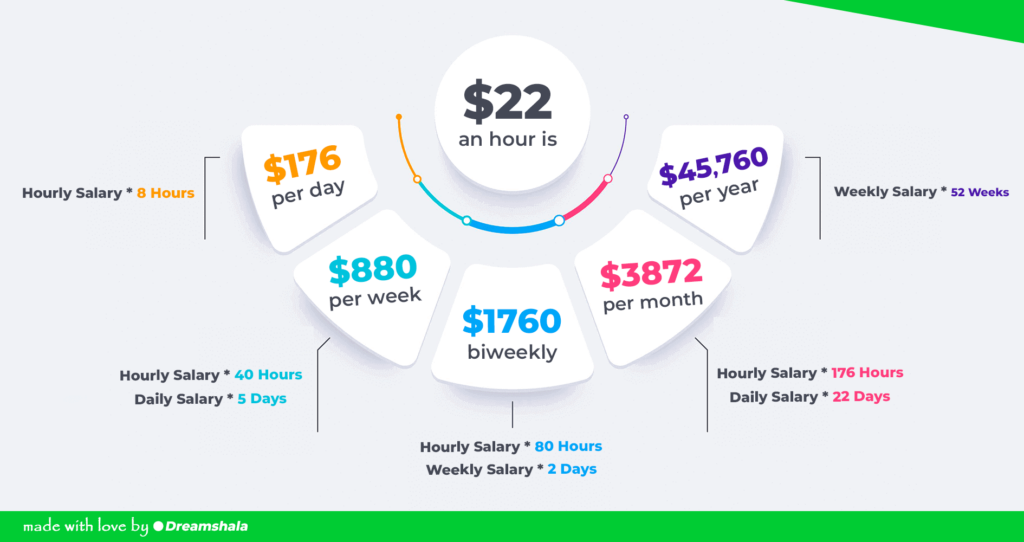

Before factoring in the complexities of the modern tax system or benefit deductions, we must establish the baseline. In the United States, a standard work year for a full-time employee consists of 40 hours per week for 52 weeks, totaling 2,080 working hours.

The Standard Full-Time Calculation

At $22 per hour, the calculation for a standard full-time position is straightforward: $22 multiplied by 2,080 hours equals a gross annual salary of $45,760.

This figure serves as the “top-line” number often used for loan applications, credit card approvals, and rental agreements. However, it is important to recognize that this is the amount before any “leakage”—such as taxes or insurance—occurs. On a monthly basis, this equates to approximately $3,813.33. On a bi-weekly basis, which is the most common pay cycle in North America, your gross paycheck would be roughly $1,760.

Factoring in Overtime and Paid Time Off (PTO)

The annual total can shift significantly based on your employment structure. If your position allows for overtime, the “time-and-a-half” rate for $22 an hour is $33. Just five hours of overtime per week could increase your annual gross income by over $8,500, pushing your total above the $54,000 mark.

Conversely, if your position does not offer Paid Time Off (PTO), your annual income will decrease for every day you don’t work. For example, two weeks of unpaid vacation would reduce your annual gross to $44,000. Understanding these nuances is vital when comparing job offers that might have the same hourly rate but different benefit structures.

Part-Time Variations

For those working part-time, the annual outlook changes. If you work 20 hours a week at $22 per hour, your annual gross income is $22,880. At 30 hours a week, it is $34,320. When assessing a $22-per-hour role, always clarify the “guaranteed hours” in your contract, as the hourly rate is only half of the equation for your total annual earning potential.

The Reality Check: Understanding Taxes and Net Take-Home Pay

The most common mistake in personal finance is budgeting based on gross income rather than “net” income. Your net income, or “take-home pay,” is what actually hits your bank account after the government and your employer take their shares.

Navigating Federal and State Tax Obligations

When earning $45,760 annually, you typically fall into the 12% federal income tax bracket (based on current US tax code for a single filer). However, because the US uses a progressive tax system, you don’t pay 12% on every dollar. You pay 10% on the first portion and 12% on the rest.

Beyond federal taxes, you must account for FICA (Federal Insurance Contributions Act) taxes, which fund Social Security and Medicare. This is a flat 7.65% for most employees. Depending on your location, state and local taxes can take an additional 0% to 7% of your income. In a state with moderate income tax, you can expect your total tax burden to be roughly 15% to 20% of your gross pay.

The Impact of Employer-Sponsored Benefits

If you have access to a 401(k) plan or health insurance through your employer, these premiums and contributions are deducted directly from your check. While a $22 hourly wage is respectable, a high-deductible health insurance plan can take a significant bite out of your monthly liquidity.

For instance, if you contribute 5% to a 401(k) and pay $200 a month for health insurance, your monthly take-home pay might drop from a gross of $3,813 down to a net of approximately $2,800–$3,000. This is the “real” number you must use when building your lifestyle and savings plan.

Budgeting and Lifestyle Strategy for a $45,760 Salary

Living on $22 an hour requires a disciplined approach to budgeting, especially in an era of fluctuating inflation. The goal is to move from “surviving” to “thriving” by allocating funds strategically.

Applying the 50/30/20 Rule

A classic framework for a $22-an-hour income is the 50/30/20 rule. This suggests allocating 50% of your net income to Needs (rent, utilities, groceries, transport), 30% to Wants (entertainment, dining out, hobbies), and 20% to Savings and Debt Repayment.

If your net take-home is $2,900 a month:

- $1,450 (50%) goes to your absolute essentials.

- $870 (30%) goes to lifestyle choices.

- $580 (20%) goes to your emergency fund or retirement.

At this income level, the “Needs” category is often the most challenging to maintain, particularly regarding housing.

The 30% Housing Rule and Cost of Living

Financial experts generally recommend that you spend no more than 30% of your gross income on housing. At $45,760 a year, that means your rent or mortgage should ideally be around $1,144 per month. In many major metropolitan areas, this can be difficult to achieve without roommates or living further from city centers.

If your housing costs exceed this 30% threshold, you must compensate by reducing your “Wants” category or finding ways to decrease other fixed costs, such as transportation or insurance. Understanding the “Cost of Living Index” in your specific city is crucial; $22 an hour in Des Moines, Iowa, offers a vastly different lifestyle than $22 an hour in Seattle, Washington.

Leveraging $22 an Hour for Long-Term Wealth

An annual income of roughly $45,000 is a solid platform for building future wealth, provided you utilize financial tools and keep a “growth mindset” regarding your earnings.

Building an Emergency Fund and Investing

The first priority at this income level should be the creation of an emergency fund. Aiming for 3 to 6 months of expenses provides a safety net that prevents you from falling into high-interest debt when life’s surprises occur.

Once the emergency fund is established, the power of compound interest becomes your greatest ally. Even contributing a small amount to a Roth IRA or an employer-matched 401(k) at this stage can lead to hundreds of thousands of dollars in growth over several decades. At $22 an hour, the “Money” niche secret is not how much you earn, but how much you keep and invest.

Upskilling and Income Diversification

While $22 an hour is a stable wage, it shouldn’t necessarily be the ceiling. Use your current stability to invest in yourself. This might mean pursuing certifications, learning new software, or mastering a trade that could push your hourly rate into the $30 or $40 range.

Furthermore, consider the “Side Hustle” economy. If you can leverage a skill (like freelance writing, graphic design, or consulting) for just 5 hours a week at a higher rate than your day job, you can bridge the gap between a $45,000 salary and a $55,000 salary. This additional income can be used exclusively for aggressive debt repayment or high-yield investments, accelerating your path to financial independence.

Conclusion: Mastering the $22-an-Hour Lifestyle

Determining how much $22 an hour is annually is only the beginning of the journey. While the math tells us the gross figure is $45,760, the true value of that wage is determined by how you manage the net take-home pay, how you navigate the cost of living, and how aggressively you plan for the future.

By understanding your tax obligations, sticking to a structured budget like the 50/30/20 rule, and looking for opportunities to upskill, you can turn a $22 hourly rate into a springboard for long-term financial success. In the world of personal finance, it is rarely the size of the paycheck that determines wealth, but the strategy applied to every dollar earned.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.